-

Oopsie

Posted by Eddy Elfenbein on January 12th, 2008 at 1:16 pmFrom the Chicago Sun-Times:

Ace employee makes $152 million accounting error

BY SANDRA GUY

Ace Hardware discovered that a mid-level employee made innocent but enormously expensive and incorrect entries in ledger books that eventually led to a $152 million accounting error, Ace Hardware CEO Ray Griffith said today.

The poorly trained employee, who worked in the finance department at the co-op’s headquarters in Oak Brook, is no longer employed at Ace Hardware, Griffith said.

The accounting error initially was revealed last summer.

Ace Hardware will be forced to restate its earnings for fiscal years 2004, 2005 and 2006, and will correct its numbers for fiscal 2007.

Investigators hired by Ace Hardware’s board of directors told the board of their findings Tuesday, and Griffith revealed the situation to Ace Hardware store owners today. The five-month investigation cost roughly $10 million.

The unidentified employee, who had worked at Ace Hardware for at least eight years, made journal entries of a “sizeable amount” that “masked” a difference in numbers between two ledger books.

The ledgers looked as though they were reconciled, but were not.

The journals are the general ledger and the perpetual inventory journal.

“Numbers were flowing through one of the ledgers but not flowing into the other,” Griffith said.

About 25 percent of the error, or $34.6 million, dates back to 1995, Griffith said. The remainder, $117.4 million, occurred from 2002 through 2006.

The employee did nothing fraudulent, and no inventory or money is missing, Griffith said.

The person was not properly trained or equipped to do the job, and Griffith conceded that that was Ace Hardware’s fault.

“We are embarrassed by it,” Griffith said. “We did not provide the training, oversight or checks and balances to help that person do [his or her] job,” Griffith said. “[The employee’s] only intent was to try to do the best job for the boss and for our company.”

Part of the problem is the increasingly complex and competitive situation that hardware stores face, Griffith said. -

Mississippi Fred McDowell

Posted by Eddy Elfenbein on January 12th, 2008 at 12:04 pm -

Mishkin: Stop Obsessing about the Fed

Posted by Eddy Elfenbein on January 11th, 2008 at 2:41 pmI have to agree with Frederic Mishkin of the Fed:

I think there is too much focus on what decision will be made about the federal funds rate target at the next FOMC meeting. What is important for pricing most financial assets is the path of monetary policy, not the particular action taken at a single meeting.

One of the great myths of the market is the over-agency of the Federal Reserve. In reality, the Fed is much less powerful than is commonly believed.

I think some people have to believe that there’s some mysterious group that’s in charge and running things. Ron Paul even blames the Fed for higher oil prices.

Nobel Laureate, Edward Prescott, wrote in the Wall Street Journal:I am not saying that there are no real costs to inflation — there certainly are. And if we get too much inflation we can exact high costs on an economy (witness Argentina as an example). However, I am talking here of the vast majority of industrialized countries who live in a low-inflation regime and who are in no danger of slipping into hyperinflation. It is simply impossible to make a grave mistake when we’re talking about movements of 25 basis points.

-

Zacks Earnings Commentary

Posted by Eddy Elfenbein on January 11th, 2008 at 10:07 amHere’s an interesting breakdown of the upcoming earnings season from Zacks.

-

Goldman Sachs sees recession in 2008

Posted by Eddy Elfenbein on January 10th, 2008 at 11:04 amFrom Reuters:

Goldman Sachs on Wednesday said it expects the U.S. economy to drop into recession this year, prompting the Federal Reserve to slash benchmark lending rates to 2.5 percent by the third quarter.

In a note to clients, Goldman said real gross domestic product would contract by 1 percent on an annualized basis in both the second and third quarters. For all of 2008, the investment bank said GDP would rise by 0.8 percent.

The unemployment rate will rise to 6.5 percent in 2009 from the current 5 percent, it said.

The weakening economy will force the Fed to lower policy rates by an additional 1.75 percentage points from the current 4.25 percent. Starting in September, the Fed cut rates at the last three meetings of the Federal Open Market Committee, reducing the target rate on loans between banks by 1 percentage point from 5.25 percent.I think that might be right.

-

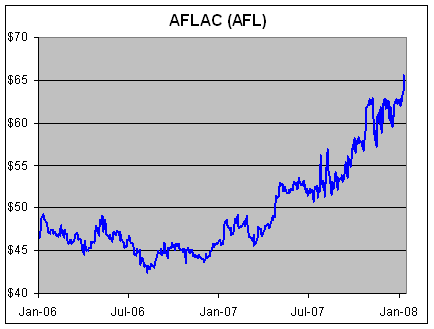

AFLAC Hits New High

Posted by Eddy Elfenbein on January 10th, 2008 at 11:00 amFinancial stocks may not be doing well, but AFLAC (AFL) continues to rally.

-

Bennie and the Feds

Posted by Eddy Elfenbein on January 9th, 2008 at 11:46 pm -

Hey European Central Bank: STFU!

Posted by Eddy Elfenbein on January 9th, 2008 at 11:17 pm

Bundchen Denies She Only Accepts Euros

RIO DE JANEIRO, Brazil (AP) — Euros? Dollars? Pounds? Gisele Bundchen insists she’s perfectly happy with them all, again denying reports that the Brazilian supermodel is shunning the weak U.S. dollar in favor of European currency.

Bundchen — known to U.S. sports fans as the girlfriend of quarterback Tom Brady — has been struggling for months to knock down recurring reports that she insists on being paid in euros, which have been rising against the dollar.

“The story of the euro is a lie,” she told the Brazilian newspaper O Globo in comments published Wednesday. “I work with many international companies, I earn salaries in different currencies, that’s all.” -

10 Tips on How to Clear Your Credit Report

Posted by Eddy Elfenbein on January 9th, 2008 at 11:09 pmFrom MSNBC. Here’s a sample:

1. Reflect on the ways errors can creep in. Sometimes automated processes take over and creditors send inaccurate information about people’s bill-paying habits to one of the major credit bureaus. In other cases, people’s identities accidentally get mixed up at the credit bureau when a staffer enters a Social Security number incorrectly. And sometimes people with fabulous credit histories become victims of blatant identity theft.

2. Check out your credit report. You can examine your credit report carefully all on your own without paying a dime. Order free annual reports from the three major credit bureaus (Equifax, Experian and TransUnion) by visiting AnnualCreditReport.com or calling 1-877-322-8228. (Note: This is the only place where you can get free credit reports once a year without any strings attached. The “free” credit reports advertised by other sources aren’t really free!)

3. Contact the credit bureau first. If you find mistakes in your report, take the matter up with the credit-reporting agency immediately. Rather than dispute the mistake via an online form, send a letter that includes your complete name and address, a description of each item you dispute, an explanation of why you dispute it and a request for deletion or correction of the information.

4. Keep good records. Along with your letter, enclose copies (NOT originals) of documents that support your position, as well as a photocopy of your credit report with the items in question circled. Send the letter and enclosures by certified mail, return receipt requested, so you can document what the credit bureau received. Keep copies of all correspondence, and jot down and save notes about each phone conversation you have. -

The Nasdaq’s Losing Streak

Posted by Eddy Elfenbein on January 9th, 2008 at 3:32 pmThe Nasdaq Composite (^IXIC) looks to snap its eight-session losing streak today.

The Dow’s record is 12 straight down days which happened twice, once in 1941:

28-Jul-41 130.06

29-Jul-41 129.19

30-Jul-41 128.95

31-Jul-41 128.79

1-Aug-41 128.22

4-Aug-41 128.17

5-Aug-41 128.14

6-Aug-41 128.10

7-Aug-41 128.09

8-Aug-41 127.48

11-Aug-41 126.01

12-Aug-41 125.81

13-Aug-41 125.65

And another in 1968:

8-Jan-68 908.92

9-Jan-68 908.29

10-Jan-68 903.95

11-Jan-68 899.79

12-Jan-68 898.98

15-Jan-68 892.74

16-Jan-68 887.14

17-Jan-68 883.78

18-Jan-68 882.80

19-Jan-68 880.32

22-Jan-68 871.71

23-Jan-68 864.77

24-Jan-68 862.23

Strange. Today is the 40th anniversary of the second one.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His