-

Wall Strip Looks at Crocs (CROX)

Posted by Eddy Elfenbein on April 17th, 2007 at 11:41 am

Ugly shoes, but a nice looking chart. Call me a skeptic. I tend to shy away from fad-like products. There’s no accounting for taste. But I have to admit that the company, and the shares, have performed very well. -

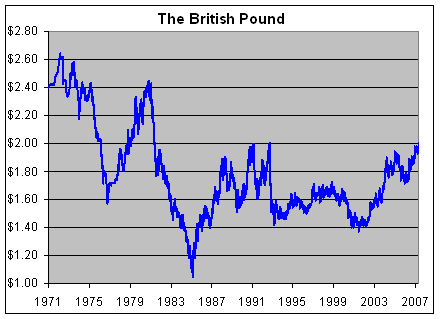

The Pound Hits $2

Posted by Eddy Elfenbein on April 17th, 2007 at 10:40 am

You know your currency is in rough shape when even the British pound is doing well against it. Today, the pound reached $2 for the first time in 15 years.

By the way, that big plunge on the chart in 1992 is when Britain dropped out of the ERM. It’s believed that George Soros made over $1 billion that day. -

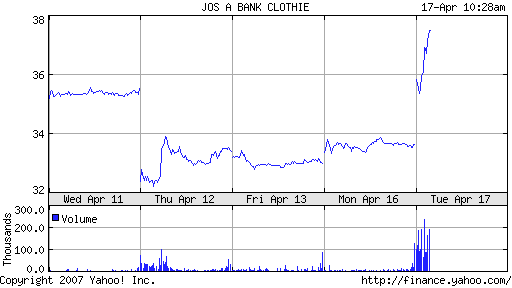

JOSB’s Earnings

Posted by Eddy Elfenbein on April 17th, 2007 at 10:08 amHere’s an interesting lesson on how irrational the stock market can be in the short-term. Last week, Bed Bath & Beyond’s (BBBY) stock fell after its earnings report. I follow that stock pretty closely and there wasn’t one single item in the earnings report that came as a surprise. It was basically what any reasonable person should have expected. Yet the shares opened Thursday morning much lower, and they’ve rallied almost continuously since then. Right now, BBBY is slightly above where it was before the earnings report. Looking back at what happened, it just doesn’t make much sense. This is why I try to caution investors against timing the market.

Well, now a similar story has happened with Jos. A Bank Clothiers (JOSB). The company just reported terrific earnings of $2.36 a share, 11 cents more than Wall Street’s forecast. Yet the stock was hit last week on a poor sales report. Now the stock is higher than where it was before.

One of the great things about investing is that doing absolutely nothing can work to your advantage.

Unfortunately, the big jump in JOSB is being cancelled out by the fall in Fair Isaac (FIC). -

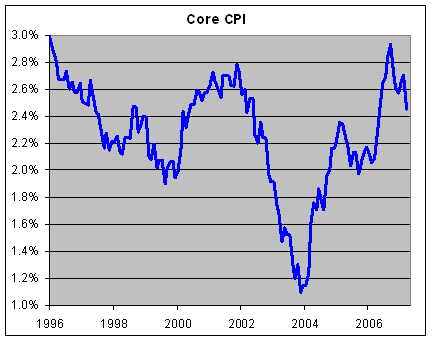

Today’s CPI Report

Posted by Eddy Elfenbein on April 17th, 2007 at 9:36 am

The bad news is that consumer prices shot up last month. The good news is that it was largely due to rising energy costs. The core rate of inflation, which excludes food and energy costs, was up just 0.1%, less than the 0.2% expected by Wall Street.

Last summer, Ben Bernanke set off a big rally when he said that the Federal Reserve sees core inflation (he uses the PCE) cooling off in 2007. It looks like the Fed was right. -

From the Citigroup Conference Call

Posted by Eddy Elfenbein on April 16th, 2007 at 7:04 pmMike Mayo – Deutsche Bank:

And so do you think this quarter is an inflection point with all these savings ahead for this year?

Chuck Prince: Well, I don’t like to predict anymore, Mike. People kind of throw my predictions in my face. I know you wouldn’t do that, but others do, and so I think I would just like to stay away from predictions for right now. -

Fair Isaac Guides Lower. A Lot Lower.

Posted by Eddy Elfenbein on April 16th, 2007 at 5:08 pmUgh.

Preliminary Second Quarter Fiscal 2007 Results

The company expects to report second quarter revenues in the range of $200 to $202 million in second quarter of fiscal 2007 versus $208.2 million reported in the prior year period. This is lower than the second quarter revenue guidance of $215 million provided by the company last quarter. Net income for the second quarter of fiscal 2007 is expected to total in the range of $20 to $22 million, or $0.35 to $0.37 per diluted share, versus $27.0 million, or $0.40 per diluted share, reported in the prior year period. This is lower than the second quarter GAAP earnings per diluted share guidance of $0.48 provided last quarter.

Revised Third Quarter and Full Year Fiscal 2007 Guidance

Total revenues are expected to be $195 to $200 million for the third quarter of fiscal 2007 with GAAP earnings of approximately $0.33 to $0.38 per share. Full year fiscal 2007 revenue is now expected to be $795 to $805 million with GAAP earnings per diluted share of $1.55 to $1.65. The previously announced sale of our mortgage product line accounts for approximately $7 million to $8 million of the reduced revenue guidance. This full year fiscal 2007 guidance is lower than the guidance of $870 million in revenue and GAAP earnings per diluted share of $2.15 provided earlier by the company.The shares are down over 11% after hours.

-

The Talented Mr. Pastorini

Posted by Eddy Elfenbein on April 16th, 2007 at 3:01 pmHere’s a fun story. Last week, Bloomberg reported that Edward Pastorini was planning to bid for Gold Fields (GFI). The Financial Times’ excellent Alphaville blog, raised some interesting questions. For example, who the fuck is Edward Pastorini? (They used “hell”—British, you know). Google had never heard of him. Alphaville also noticed that Edward Pastorini is an anagram for “Top Insider Award.” Clever, no?

Mr. Pastorini is apparently now quite upset. And what’s the best way to prove you exist? An email of course!I challenge FTAlphaville to produce even one iota of irrefutable proof that I am not Edward Pastorini and that our offer for Gold Fields is not genuine. Send us your IRREFUTABLE PROOF. Now I hope you will have the decency to give us as much truthful coverage as you gave us negative coverall in your publications. You owe us a public apologiy [sic]. Just because we loathe the media and prefer to remain behind the scenes – with good reason when there are idiots like you out there – that does not mean that we are not genuine. We are waiting for your public apology and for your 100% irreefutable [sic] proof that I am not Edward Pastorini and that our offer for Gold Fields is not real. We’re waiting. Send us your NEW article now – or do you not ever admit your mistakes?

-

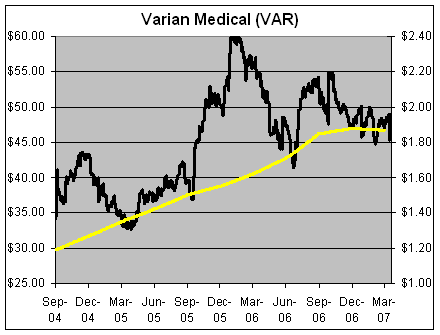

Varian Medical: A Smart Buy

Posted by Eddy Elfenbein on April 16th, 2007 at 1:05 pm

Varian Medical Systems (VAR) took a big hit on Friday, dropping 7.3% on news of lower revenue guidance. But the stock’s defenders are coming out in full force. Joshua Lipton of Forbes noted the positive views of many analysts:In a client note, Citigroup analyst Amit Bhalla wrote that while North America has not displayed signs of weakness in past quarters, the results do appear explainable.

The North America miss, Bhalla wrote, was due to timing of customer buying patterns and had the quarter been one week longer, orders would have been $20 million higher and total North America oncology net orders would have been flat, instead of down 10%.

Bhalla said, “As was the case in Europe last quarter, the company does not believe that it has lost orders to competitors in North America and we believe this to be the case as well.”

Bhalla maintained a “buy” rating on the shares. He lowered his price target by $2 to $60.

Standard & Poor’s Equity Research analyst Robert Gold also continued to believe that Varian is a wise buy.

In a client note, Gold wrote that he was disappointed by the 10% decline in U.S. oncology orders.

“However, we believe an increased size of average orders, and a slightly more competitive market are extending the selling cycle a bit and have pushed some booking into the third-quarter,” Gold wrote.

He said that he still sees full fiscal 2007 revenues of about $1.8 billion and earnings per share of $1.83. He maintained a “strong buy” opinion on the shares. -

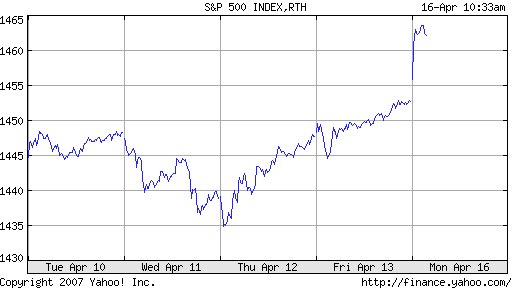

The S&P 500 Hits 6-1/2 Year High

Posted by Eddy Elfenbein on April 16th, 2007 at 10:33 am

So much for the Shanghai Surprise from seven weeks ago. The market has now made up everything it lost, and is at a fresh 6-1/2 year high. The index is still over 4% from the all-time reached in 2000. The good news is that the S&P is inches away from being in the black for the decade (and century and millennium). -

Tom Wolfe Leads Off for Portfolio

Posted by Eddy Elfenbein on April 16th, 2007 at 9:45 amTom Wolfe looks at the New Masters of the Universe:

While fathers all over America tend to become overzealous, even violent, these days in trying to turn their children into little sports superstars, in Greenwich a father who is one of these people will try to take control of every element in a game: his child’s teammates, their coach, the opposing team’s coach, its players, and most definitely the referees. In a famous instance, one of these people came to watch his teenage daughter play in an ice hockey game against a team from neighboring Port Chester, New York, a town known in Greenwich as the place where one’s plumbers, electricians, computer swamis, roofers, glaziers, air-conditioning mechanics, wall-to-wall-carpet humpers, and household servants live. The man began bellowing so loudly, nobody at the rink could shut out the sound. He upbraided the referees for their poor eyesight and worse judgment. He told his daughter’s coach how to play her and all her teammates and kept him abreast of his mistakes in strategy. He scolded the Port Chester coach and the players for their incessant cheating and malicious roughness. Finally a Port Chester player, a big girl, an Amazon on ice, skated to the stands, charged up the stairs on her skates, and accosted the Mouth, putting her gloved fist six inches from his face and saying, “If you don’t shut the fuck up, I’m gonna come back and beat the shit outta you!” He shut up. The tales are endless: the hedge fund founder desperate to get his son into one of Greenwich’s socially swell private schools who clips a six-figure check to the first page of the application, witlessly forcing the school to reject both his son and his check or lose all credibility—

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His