-

An Open Letter to Biomet Shareholders

Posted by Eddy Elfenbein on December 19th, 2006 at 2:02 pmVote Against the Private Equity Buyout

Dear Shareholders of Biomet,

On Monday, the Board of Directors of Biomet (BMET) announced that it agreed to a buyout offer from a consortium of private equity frims. The consortium consists of the Blackstone Group, Goldman Sachs Capital Partners, Kohlberg Kravis Roberts, Texas Pacific Group and one of Biomet’s founders, Dane Miller. The deal is for $10.9 billion ($44 a share) and is due to be completed by October 31, 2007.

We believe this is a poor deal for shareholders of Biomet and we urge all shareholders to vote against it.

Biomet’s track record is known to everyone. For the last three decades, the company has been one of the great success stories of American free enterprise. Biomet has delivered record sales and earnings every year since it began operations in 1977. This is an astounding achievement. Moreover, the company’s products have helped millions of people all over the world lead a better life. This is something we all should be proud of.

In 1977, the company had sales of just $17,000. For FY 2006, Biomet’s sales exceeded $2 billion. Today Biomet employs over 6,000 people. Since 1982, the stock has split nine times. In the last 20 years, shares of Biomet have increased by more than 40-fold.

Biomet has regularly had its return-on-equity top 20%. Additionally, the company has no long-term debt and a very healthy cash position.

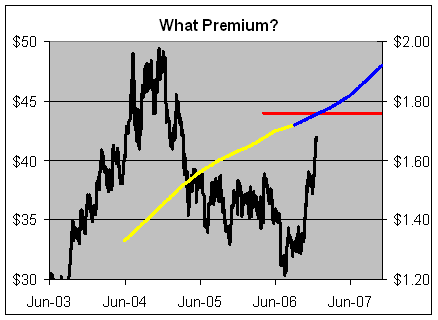

Give all these facts, we’re very disturbed by management’s decision to sell Biomet for such a low price. Monday’s press release notes that $44 is “a 27% premium over Biomet’s closing price on April 3, 2006.”

This is a misleading fact that was repeated with question through much of the financial media. This “premium” is measured from over eight months ago to more than ten months in the future. Annualized, this premium works out to 16.1% which is less than the shares’ long-term performance.

Additionally, we believe the shares were unusually low-priced in April so the appearance of a premium is illusionary. Forty-four dollars a share is not only well below Biomet’s high price from 2004, but it’s also below the average share price for the entire second half of 2004. Since that time, Biomet’s sales and earnings have continued to increase.

The graph above shows Biomet’s share price (black line) with the $44 buyout offer (red line). The yellow line is Biomet’s earnings-per-share (right scale), and the blue portion is Wall Street’s consensus projection. The earnings and share prices and scaled by a ratio of 25 to 1.

For a number of reasons, shares of Biomet and the entire health care sector have been punished over the past year. This should not be a reflection on Biomet’s long-term intrinsic value. And it should not be a reason to sell the company at a distressed price. Bear in mind that the stock often traded above 25 times earnings. Despite being called a premium, the private equity deal represents a substantial discount to Biomet’s historic valuation. We have to asked the Board of Directors, “What’s the hurry?”

While there certainly are problems with Biomet’s business, particularly in the spinal business, these problems are a small part of the company’s overall business. Consider that over the next decade, the number of Americans aged 55 to 75 will nearly double. David Phillips at 10-Q Detective notes that “hip and knee and extremity joint replacements account for more than 95% of all orthopedic implants and Biomet holds about 12% of this market, which accounted for 68% of the company’s net sales in FY 2006.”

We’re not opposed to a buyout offer, but we encourage the Board of Directors to consider other offers. The present offer undervalues Biomet’s potential and does not adequately reflects its proper value.

We encourage all shareholders to let the board know that this deal is unsatisfactory and not in the best interest of shareholders. If it comes to vote, we encourage a no vote on the present offer.

Sincerely,

Eddy Elfenbein

Crossing Wall Street -

FactSet Earns 47 Cents a Share

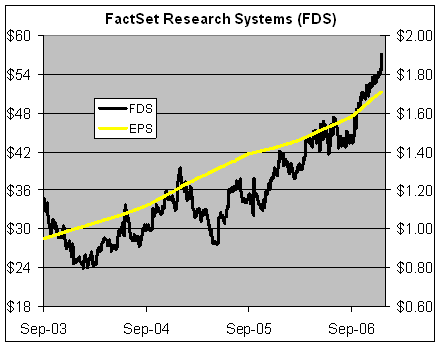

Posted by Eddy Elfenbein on December 19th, 2006 at 11:00 amFactSet Research Systems (FDS) just reported earnings of 47 cents a share, a penny better than estimates. The company made 38 cents a share last year. Sales were up 21% to $108.9 million.

The stock is up $3 a share today to a new high. It’s now a 40%+ winner for the year.

-

What to Look for This Week

Posted by Eddy Elfenbein on December 18th, 2006 at 4:55 pmWe have two Buy List stocks reporting earnings this week. FactSet (FDS) reports tomorrow. The company already gave guidance for revenues ($106 to $109 million) and operating margins (31.5% to 33.5%), but not EPS. Fortunately, I own a calculator so I’m expecting EPS of 47 cents a share. Maybe 48.

I should add that FDS is by far the most expensive stock on the Buy List. Ultimately, I decided to keep it on the 2007 Buy List. Its business is strong and I think it deserves to be richly priced.

Bed Beth & Beyond (BBBY) is set to report on Wednesday. BBBY has been one of my favorite stocks. Wall Street is expecting 52 cents a share, but I think BBBY can top that. This can easily be a $45 – $50 stock. -

Moron of the Year

Posted by Eddy Elfenbein on December 18th, 2006 at 12:40 pmA former UBS PaineWebber employee was sentenced to eight years in prison on Wednesday for planting a computer “logic bomb” on company networks and betting its stock would go down.

The investment scheme backfired when UBS stock remained stable after the computer attack and Roger Duronio lost more than $23,000.

A federal judge in New Jersey sentenced Duronio, 64, to 97 months in prison and ordered him to make $3.1 million in restitution to his former employer, the U.S. attorney’s office said in a statement.

Duronio was convicted on July 19 of one count of securities fraud and one count of computer fraud in the 2002 case.

Duronio quit his job as a systems administrator in February 2002 after repeatedly expressing dissatisfaction about his salary and bonuses, the statement said.

He then planted malicious computer code known as a “logic bomb” in about 1,000 of PaineWebber’s approximately 1,500 networked computers in branch offices. On March 4, 2002, the “bomb” detonated and began deleting files.

Duronio attempted to profit from the attack, the statement said. He bought more than $23,000 in put option contracts for UBS AG stock, betting the stock’s price would go down after his “logic bomb” went off.

But, according to testimony at his trial, the stock remained stable after the computer attack and Duronio lost all of his investment.He would have gotten away with it, too. If it weren’t for those meddling kids.

-

Biomet Goes Private Equity

Posted by Eddy Elfenbein on December 18th, 2006 at 8:20 amAt $44 a share. Here’s the press release:

Biomet, Inc. to Be Acquired by Private Equity Consortium for $10.9 Billion or $44 Per Share in Cash

WARSAW, Ind.–Biomet, Inc. a worldwide leader in the design and manufacture of musculoskeletal medical products, announced today that it has entered into a definitive merger agreement to be acquired by a private equity consortium in a transaction with a total equity value of approximately $10.9 billion. The consortium includes affiliates of the Blackstone Group, Goldman Sachs Capital Partners, Kohlberg Kravis Roberts & Co. and TPG.

Under the terms of the merger agreement, Biomet shareholders will receive $44 per common share, representing a 27% premium over Biomet’s closing price on April 3, 2006, the trading day prior to public speculation, which was subsequently confirmed by Biomet on April 6, 2006, that it had retained Morgan Stanley to assist it in exploring strategic alternatives.

The board of directors of Biomet has unanimously approved the merger agreement; the merger and the transactions contemplated thereby, and will also recommend approval by Biomet’s shareholders.

The transaction will be financed through a combination of equity contributed by the private equity consortium and debt financing that has been committed by Bank of America and Goldman Sachs. There is no financing condition to the obligations of the private equity consortium to consummate the transaction.I’m not happy with this price, and I think it’s a lousy idea. This is just $2 a share above Friday’s close, and it’s lower than where Biomet was two years ago. Earlier I said that $45 a share was a minimum, but I didn’t think the board would consider anything below that. I don’t see how this deal helps shareholders.

If I were in Medtronic’s shoes, I would consider making an offer. The worst they can say is no.

Update: Speaking of Medtronic, Barron’s had a good piece on the stock last week. -

Einstein and Keynes

Posted by Eddy Elfenbein on December 17th, 2006 at 12:44 pmHere’s a fascinating article by James K. Galbraith, John Kenneth. Galbraith’s son, about the influence of Albert Einstein on John Maynard Keynes.

One of the most intriguing and little-noted facts about John Maynard Keynes’s masterwork, The General Theory of Employment Interest and Money, concerns the first three words of its title. These are evidently cribbed from Albert Einstein. Alone that would be only a curiosum; but there is more. The parallels between Keynes’s economics and Einstein’s relativity theory are deep enough, and evidently intentional enough, to provide a useful framework for thinking about what Keynes meant to do with his scientific revolution.

-

What’s Alan Up to These Days?

Posted by Eddy Elfenbein on December 16th, 2006 at 8:07 amFrom The Onion:

-

The Pessimism of Crowds

Posted by Eddy Elfenbein on December 15th, 2006 at 10:48 amThe Dow is at another all-time today. The index is now up to 12,468.

Last year, Business Week asked its readers to vote on where the Dow would be at the end of 2006. Here are the results:10,000 or below…………………….15.1%

Around 10,500……………………….13.1%

Around 11,000……………………….24.3%

Around 11,500……………………….28.3%

12,000 or higher…………………….15.8%

Not sure………………………………..3.4%Sheesh, what was everyone so gloomy about? For from being irrational or even exuburent, the crowd was very tame. Less than one in six got it right. Here’s what I wrote at the time:

That means that the median is “around 11,000.” I won’t predict that the Dow will hit 12,000, but I think it’s entirely reasonable that it could. That’s a little over 10% from where it is today which is in the middle of the long-term average. Yet only one in six respondents said “12,000 or higher.” Strange.

I normally would expect polls like this to be overly optimistic. Maybe I’m reading too much into this, or perhaps the public is much more pessimistic that I realized.The professionals were even gloomier. Here were the predictions of 76 market pros. The Dow is currently higher than all but three of their forecasts.

Ticker Sense points out that the latest Barron’s roundup of market pros sees the Dow headed to 13,220. That’s only 6% from where we are now. -

The 2007 Buy List

Posted by Eddy Elfenbein on December 15th, 2006 at 10:46 amHere’s the Buy List for 2007:

AFLAC (AFL)

Amphenol (APH)

Bed Bath & Beyond (BBBY)

Biomet (BMET)

Donaldson (DCI)

Danaher (DHR)

FactSet Research Systems (FDS)

Fair Isaac (FIC)

Fiserv (FISV)

Graco (GGG)

Harley-Davidson (HOG)

Jos. A Bank Clothiers (JOSB)

Medtronic (MDT)

Nicholas Financial (NICK)

Respironics (RESP)

SEI Investments (SEIC)

Sysco (SYY)

UnitedHealth Group (UNH)

Varian Medical Systems (VAR)

WR Berkley (BER)

I’ll start tracking their performances on January 1. As the rules say, I can’t make any changes for the entire year.

You might think the list looks very familiar. Well, you’re right. I’ve only made five changes. Some of you might be surprised but such little activity, but it’s actually quite reasonable. This implies a holding period of four years. Investing is one of few areas where doing nothing is often the best thing that needs to be done. And frankly, I like to think of myself as a pioneer in the field of idleness.

The five stocks I’m removing are:

Brown & Brown (BRO)

Dell (DELL)

Expeditors International (EXPD)

Home Depot (HD)

Wachovia (WB)

The new additions are :

Amphenol (APH)

Nicholas Financial (NICK)

Graco (GGG)

WR Berkley (BER)

Jos. A Bank Clothiers (JOSB)

I’ll discuss these stocks more in the days ahead. I’ll start tracking the new stocks at the start of the year. Just like this year, I’ll consider the stocks to be equally weighted on January 1. -

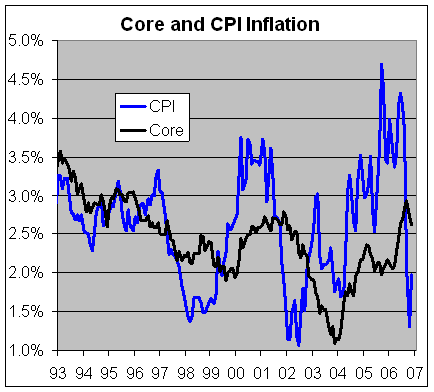

CPI Unchanged in November

Posted by Eddy Elfenbein on December 15th, 2006 at 9:25 amToday’s CPI report shows that consumer prices didn’t change during November. Both the headline and core numbers came in flat. This is good news for Bernanke’s credibility. In July, he testified that core CPI would fall later this year.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His