-

Varian Medical: A Smart Buy

Posted by Eddy Elfenbein on April 16th, 2007 at 1:05 pm

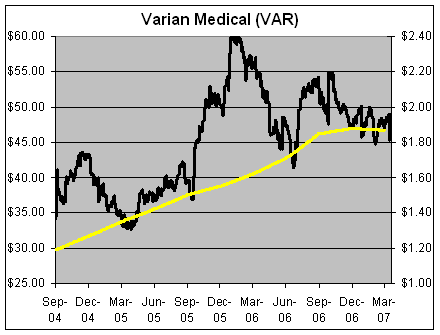

Varian Medical Systems (VAR) took a big hit on Friday, dropping 7.3% on news of lower revenue guidance. But the stock’s defenders are coming out in full force. Joshua Lipton of Forbes noted the positive views of many analysts:In a client note, Citigroup analyst Amit Bhalla wrote that while North America has not displayed signs of weakness in past quarters, the results do appear explainable.

The North America miss, Bhalla wrote, was due to timing of customer buying patterns and had the quarter been one week longer, orders would have been $20 million higher and total North America oncology net orders would have been flat, instead of down 10%.

Bhalla said, “As was the case in Europe last quarter, the company does not believe that it has lost orders to competitors in North America and we believe this to be the case as well.”

Bhalla maintained a “buy” rating on the shares. He lowered his price target by $2 to $60.

Standard & Poor’s Equity Research analyst Robert Gold also continued to believe that Varian is a wise buy.

In a client note, Gold wrote that he was disappointed by the 10% decline in U.S. oncology orders.

“However, we believe an increased size of average orders, and a slightly more competitive market are extending the selling cycle a bit and have pushed some booking into the third-quarter,” Gold wrote.

He said that he still sees full fiscal 2007 revenues of about $1.8 billion and earnings per share of $1.83. He maintained a “strong buy” opinion on the shares. -

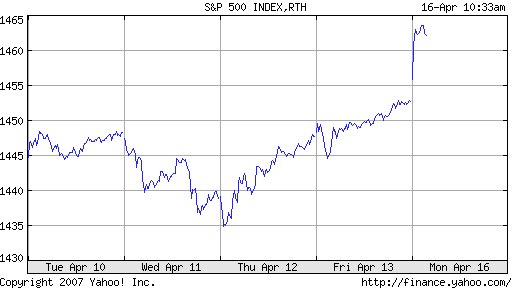

The S&P 500 Hits 6-1/2 Year High

Posted by Eddy Elfenbein on April 16th, 2007 at 10:33 am

So much for the Shanghai Surprise from seven weeks ago. The market has now made up everything it lost, and is at a fresh 6-1/2 year high. The index is still over 4% from the all-time reached in 2000. The good news is that the S&P is inches away from being in the black for the decade (and century and millennium). -

Tom Wolfe Leads Off for Portfolio

Posted by Eddy Elfenbein on April 16th, 2007 at 9:45 amTom Wolfe looks at the New Masters of the Universe:

While fathers all over America tend to become overzealous, even violent, these days in trying to turn their children into little sports superstars, in Greenwich a father who is one of these people will try to take control of every element in a game: his child’s teammates, their coach, the opposing team’s coach, its players, and most definitely the referees. In a famous instance, one of these people came to watch his teenage daughter play in an ice hockey game against a team from neighboring Port Chester, New York, a town known in Greenwich as the place where one’s plumbers, electricians, computer swamis, roofers, glaziers, air-conditioning mechanics, wall-to-wall-carpet humpers, and household servants live. The man began bellowing so loudly, nobody at the rink could shut out the sound. He upbraided the referees for their poor eyesight and worse judgment. He told his daughter’s coach how to play her and all her teammates and kept him abreast of his mistakes in strategy. He scolded the Port Chester coach and the players for their incessant cheating and malicious roughness. Finally a Port Chester player, a big girl, an Amazon on ice, skated to the stands, charged up the stairs on her skates, and accosted the Mouth, putting her gloved fist six inches from his face and saying, “If you don’t shut the fuck up, I’m gonna come back and beat the shit outta you!” He shut up. The tales are endless: the hedge fund founder desperate to get his son into one of Greenwich’s socially swell private schools who clips a six-figure check to the first page of the application, witlessly forcing the school to reject both his son and his check or lose all credibility—

-

Geoffrey Raymond’s Latest

Posted by Eddy Elfenbein on April 16th, 2007 at 9:34 amI’m not sure what to say about this, but here’s Geoffrey Raymond describing his latest painting of Maria Bartiromo.

-

Happy 300th Leonhard Euler

Posted by Eddy Elfenbein on April 15th, 2007 at 3:28 pm

The Washington Post has more on the “Mozart of Mathematics.” -

Fama Factors Out French: “I Did All The Work”

Posted by Eddy Elfenbein on April 15th, 2007 at 3:25 pmAt long last, we now know the truth:

After 15 years of sharing the credit for groundbreaking research with Ken French, Eugene Fama is on a mission to expose his former colleague, and himself. The result is an alarming behind-the-scenes look at how academic careers are made and broken.

“I hired Ken French in 1990 when he was a driving instructor in Winnetka. Chicago was pressuring me to partner with another researcher; I couldn’t stand the idea so I hired a stooge. The man has never contributed a single idea to my research, and yet his name is constantly mentioned in the same breath as mine. On top of it all, the American Finance Association has nominated him as president-elect! That’s a travesty and I won’t have it.” -

2007 Wharton Economic Summit

Posted by Eddy Elfenbein on April 13th, 2007 at 7:58 amNot much blogging today. I’ll be in Philadelphia at the 2007 Wharton Economic Summit.

It’s sort of like Davos, except the odds of being car-jacked are a lot higher. Wish me luck. -

Brady Quinn on Power Lunch

Posted by Eddy Elfenbein on April 12th, 2007 at 12:12 pm -

JOSB Down 8%

Posted by Eddy Elfenbein on April 12th, 2007 at 11:10 amJoS. A. Bank Clothiers (JOSB) is down sharply today on a poor same-store sales report:

Men’s clothing retailer JoS. A. Bank Clothiers Inc. said Thursday that its same-store sales grew 1.4 percent in March, but missed analysts’ expectations.

Analysts polled by Thomson Financial were looking for a same-store sales increase of 2.7 percent for the month.

Same-store sales, or sales at stores open at least a year, are a key measure of retailer (or restaurant) performance, because they measure growth at existing stores rather than from newly opened ones.

Total sales for the period ended April 7 climbed 10.1 percent to $45.7 million from $41.5 million in the year-ago period.

Quarter-to-date, same-store sales were up 2 percent while total sales were ahead 11.8 percent to $84.1 million versus $75.2 million in the prior-year period. -

Bed Bath & Beyond Earned 79 Cents a Share

Posted by Eddy Elfenbein on April 12th, 2007 at 8:28 amThe company just wrapped up its 15th straight record year. For the fourth quarter, Bed Bath & Beyond (BBBY) earned 79 cents a share, although that doesn’t include a charge of seven cents a share.

For the year, BBBY earned $2.15 a share, which is a nice improvement over the $1.92 a share it made last year. Annual sales rose from $5.8 billion to $6.6 billion.

Here are the quarterly results going back a few years:Quarter Sales Gross Profit Operating Profit Net Profit EPS $356,633 $146,214 $28,015 $17,883 $0.06 $451,715 $185,570 $53,580 $33,247 $0.12 $480,145 $196,784 $50,607 $31,707 $0.11 $569,012 $238,233 $77,138 $48,392 $0.17 $459,163 $187,293 $36,339 $23,364 $0.08 $589,381 $241,284 $70,009 $43,578 $0.15 $602,004 $246,080 $64,592 $40,665 $0.14 $746,107 $311,802 $101,898 $64,315 $0.22 $575,833 $234,959 $45,602 $30,007 $0.10 $713,636 $291,342 $84,672 $53,954 $0.18 $759,438 $311,030 $83,749 $52,964 $0.18 $879,055 $370,235 $132,077 $82,674 $0.28 $776,798 $318,362 $72,701 $46,299 $0.15 $903,044 $370,335 $119,687 $75,459 $0.25 $936,030 $386,224 $119,228 $75,112 $0.25 $1,049,292 $443,626 $168,441 $105,309 $0.35 $893,868 $367,180 $90,450 $57,508 $0.19 $1,111,445 $459,145 $155,867 $97,208 $0.32 $1,174,740 $486,987 $161,459 $100,506 $0.33 $1,297,928 $563,352 $231,567 $144,248 $0.47 $1,100,917 $456,774 $128,707 $82,049 $0.27 $1,273,960 $530,829 $189,108 $120,008 $0.39 $1,305,155 $548,152 $190,978 $121,927 $0.40 $1,467,646 $650,546 $283,621 $180,980 $0.59 $1,244,421 $520,781 $150,884 $98,903 $0.33 $1,431,182 $601,784 $217,877 $141,402 $0.47 $1,448,680 $615,363 $205,493 $134,620 $0.45 $1,685,279 $747,820 $304,917 $197,922 $0.67 $1,395,963 $590,098 $148,750 $100,431 $0.35 $1,607,239 $678,249 $219,622 $145,535 $0.51 $1,619,240 $704,073 $211,134 $142,436 $0.50 $1,994,987 $862,982 $309,895 $205,842 $0.72 Two things to note. This last quarter was based on 14 weeks while the other quarters were just 13 weeks. Also, the 2006 fiscal year had 53 weeks compared with 52 for last year.

Some analysts have noted the company’s lower gross margins. This is what BBBY had to say on their conference call:The gross profit margin for the full fiscal year improved slightly from fiscal 2005. The approximate 110 basis point decline in the fiscal fourth quarter was primarily due to higher inventory acquisition costs. Inventory acquisition costs were higher, primarily due to a shift in purchase volume incentives earned during our fiscal third quarter, which as we discussed in December, benefited that quarter.

This is the first decline in gross margins in five years.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His