-

Emotions Versus Finance

Posted by Eddy Elfenbein on November 5th, 2006 at 3:15 pmThe Washington Post looks at how ego and vanity are affecting the housing crash…er, slowdown.

Evidence is mounting that people set prices, particularly for housing, as much on ego and self-image as on an objective review of the market. That’s one reason for the phenomenon known as “sticky prices” — home sellers who won’t cut their demands enough to make a deal. It helps explain why the unsold inventory of homes has risen so high, and why, despite this rise, home prices in the Washington area have fallen only slightly. There were 24,741 homes for sale in September in Washington and the close-in suburbs, up from 13,950 a year earlier.

Economic researchers have found that emotions are a bigger influence than was previously believed in how people make financial decisions. For a long time, economists believed that human beings made decisions like robots, that people applied simple logic in making financial choices. But a body of research developed over the past two decades, known as neuroeconomics or behavioral economics, has shed light on how powerful a role the unconscious mind plays. New imaging technology, meanwhile, is allowing scientists to peer inside people’s brains while they wrestle with financial decisions.

These studies have illuminated a few key concepts: Many people will pass up sure profits for illusory ones. Some will turn down profits if they believe someone else is unfairly profiting more. Some will even refuse to sell if they believe they may come to regret it, because fear of future regret can be as powerful a motivator as money in the pocket today.

In other words, people will cling to prices they recall from a brighter day, even when market conditions have changed; they will walk away from a sale if they feel the buyer is getting too good a deal at their expense; and they are terrified that [if they sell now] the market will rebound and they will feel like fools. -

Evaluating Greenspan

Posted by Eddy Elfenbein on November 4th, 2006 at 3:58 pmReason discusses Alan Greenspan’s legacy as Fed Chairman with Milton Friedman, Ron Paul, James Grant, Bryan Caplan and Jeff Saut. Here’s a sample:

Reason: Analysts often complain that Greenspan did nothing to help solve our low savings rates and our trade deficits. Is the Fed relevant to these problems? Are they problems at all?

Friedman: I do not think you or I can say what the right savings rate is or should be. There’s nothing wrong with a person, family, or country saying, “We have high enough income. We don’t need more. We’re going to spend it all.” We can have a perfectly prosperous and active economy along those lines. I don’t think it’s helpful to ask, “Is this rate right or wrong?” Instead we should ask, “Have we adopted polices that reduce incentives to save?”

In that respect, there’s a great deal to be done. The tax system distorts the incentive to save, sometimes pro-saving and sometimes anti. Government should ask itself how best to maintain institutions under which you have an undistorted market in savings.

So far as foreign balance of payments is concerned, we have to let the dollar float. You shouldn’t try to control the price of foreign exchange any more than you should try to control the price of other things. The country seems to have learned that price controls are not good.

I do not believe that [mass foreign holding of U.S. securities] is something to be feared. The only reason [a widespread loss of will to buy U.S. Treasury securities] would happen is if our central bank followed inflationary policies that made it undesirable to hold American securities, and that’s our fault, not theirs. I think the concern that has been expressed about foreign balance of payments is in large part mistaken and in large part reflects the defects of statistics available.

If you have a foreign owner of a bond or stock who loses confidence in the American economy and sells, whom do they sell it to? They have to sell it to people with a stronger confidence in the U.S. economy who are willing to hold on to it. If the foreigners dump bonds or stock and use dollars to buy other U.S. assets, there’s no net effect. If they use them to buy consumer goods, then that means an increase in balance of payments, a plus on income accounts. -

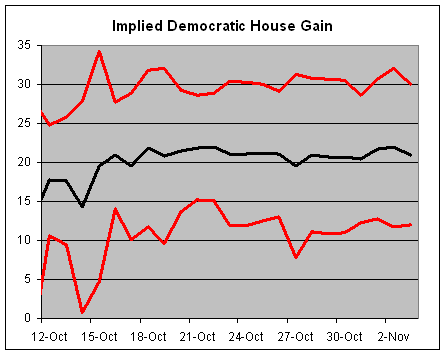

Implied Tradesports Markets

Posted by Eddy Elfenbein on November 3rd, 2006 at 3:13 pm

This is a favorite topic of mine. In investing, we can look at two markets and imply a third. That’s basically how options work. Well…we can do the same for predictions markets.

At Tradesports, they offer futures contracts for how many seats they Democrats will pickup in the house. They offer contract for several different scenarios (i.e., greater than 14.5 seats, or greater than 19.5 seats). Assuming a logonormal distribution, we can find an implied mean and standard devation.

The chart above shows the mean number seats the Democrats looks to gain (black line) with plus and minus one standard deviation bands (red lines).

As of the last trade, the market believes the Democrats have a 60.2% chance of gaining at least 19.5 seats, and a 46.9% of gaining 24.5 seats. A 60.2% chance is +0.258 standard deviations, and a 46.9% chance is -0.078 standard deviations. So those 5 seats are worth 0.336 standard deviation. Therefore, one standard deviation is nearly 15 seats. The Democrats are now projected to gain over 23 seats, but the market still believes its wide open. -

Whole Foods Crashes

Posted by Eddy Elfenbein on November 3rd, 2006 at 11:33 amWhole Foods Market (WFMI) is down over 23% in today’s session. I wonder if anyone saw this coming.

-

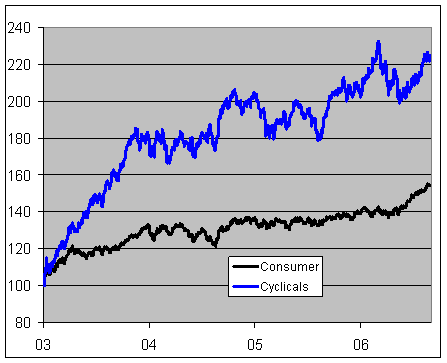

A Story of Two Bulls

Posted by Eddy Elfenbein on November 3rd, 2006 at 11:20 am

Not all Bull Markets look the same. The chart above shows the Morgan Stanley Cyclical Index (^CYC) and the Morgan Stanley Consumer Index (^CMR) since March 2003. While cyclical stocks have been highly volatile, especially in recent months, the conumser stocks have quietly rallied. -

These Strange Employment Numbers

Posted by Eddy Elfenbein on November 3rd, 2006 at 10:56 amEach month’s employment report grows increasingly bizarre. First, the government suddenly discovered 800,000 Americans who were employed yet the Feds somehow missed them. The details on that still haven’t been released.

Today we’re told that the nonfarm payroll number for August was revised higher by 42,000. The number for September was adjusted higher by 139,000. Plus, the economy added 132,000 new jobs last month. Add it all up, and the unemployment rate for October is now down to 4.415% which is lower than it was eight years ago.

I’m not sure why anyone pays attention to these numbers. I don’t see any value in them. -

Reader Quiz: Gay Sex or Investing?

Posted by Eddy Elfenbein on November 2nd, 2006 at 2:16 pmToday’s reader quiz: Are the following phrases associated with gay sex or investing? Good luck!

1. Working for a bulge bracket

2. Doing a mon back

3. Buying a naked straddle

4. Hanging with the odd lots

5. Looking for a double bottom

6. Going deep in-the-money

7. Sliding under the pink sheets

8. Front running the hedges

9. Hunting for bears

10. David Faber

11. Getting fined by Cox

Results next week. -

Random Run Down Wall Street

Posted by Eddy Elfenbein on November 2nd, 2006 at 11:14 amAt DealBreaker, Bess Levin looks at Wall Street’s obsession with marathoning. Frankly, I’d think any sport where defecating oneself is acceptable would be popular on the Street. (Look, I’ve partied with bondtraders.) In today’s NYT, Daniel Gross examines another angle: they give away lots of free stuff (the marathons, not Wall Street).

-

Dell Hits $25

Posted by Eddy Elfenbein on November 2nd, 2006 at 10:19 amBreifly. That’s the highest price in four-and-a-half months. Goldman upgraded the stock to neutral.

That said, in the absence of Dell restructuring — which we are not modeling into our assessment since there has been no inclination that Dell wants to do that — we think Dell’s choice is ultimately between growth and margins which in our model tops out at 7 percent normalized growth, 17 percent gross margin, and 6 percent operating margin, meaning that this is not the ‘Dell of old.’

-

Fair Isaac and Biomet

Posted by Eddy Elfenbein on November 2nd, 2006 at 9:18 amAfter the bell yesterday, Fair Isaac (FIC) reported earnings of 60 cents a share. That was three cents higher than the Street was expecting. Charges related to stock-based compensation and one-time expenses pushed FIC’s net income down to 35 cents a share.

For the full fiscal year, net income fell to $103.5 million, or $1.59 per share, from $134.5 million, or $1.86 per share. Revenue rose to $825.4 million from $798.7 million.

Looking ahead, Fair Isaac said it expects first fiscal-quarter earnings per share of about 48 cents on revenue of about $210 million. The outlook includes stock-based compensation charges.

Analysts forecast quarterly profit of 59 cents per share on sales of $211.9 million.

For the full fiscal year, Fair Isaac said it expects earnings per share of about $2.10, including stock-based compensation expenses, on sales of about $870 million.

Wall Street expects full-year earnings of $2.44 per share on sales of $873.1 million.

Fair Isaac also said its board authorized a stock buyback program of up to $500 million.The company also announced that its CEO, Thomas G. Grudnowski, has resigned.

The other big story is that Smith & Nephew has said that it’s in preliminary talks with Biomet (BMET) about a possible merger. Both companies have very similar market values. Interestingly, what may have lead Biomet down this path was then Dane Miller, the CEO, suddenly resigned earlier this year.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His