-

Varian Joins the S&P 500

Posted by Eddy Elfenbein on February 8th, 2007 at 9:44 amCongratulations to Varian Medical Systems (VAR) for its inclusion in the S&P 500. This is Wall Street’s equivalent of being a “made man.” The opening was made thanks to Blackstone’s acquistion of Equity Office.

Also, Joe Bank (JOSB) just raised its forecast for this year to $2.25 a share from its earlier estimate of $2.15.

Finally, Harley (HOG) said it will miss Q1 shipment targets due to the strike. -

The Disposition Effect

Posted by Eddy Elfenbein on February 8th, 2007 at 7:02 amFrom Wikipedia.

The Disposition Effect is an anomaly discovered in Behavioral Finance. It relates to the tendency of investors to sell shares whose price is increasing, while keeping assets that have dropped in value.

Don’t let this happen to you.

-

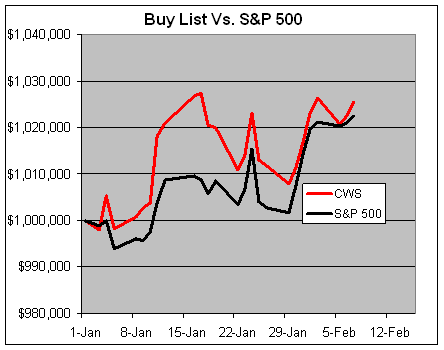

The Buy List So Far

Posted by Eddy Elfenbein on February 7th, 2007 at 5:07 pmThrough today, the Buy List is up 2.54% (the red line) versus 2.24% for the S&P 500 (the black line).

WR Berkley (BER), one of our weaker stocks this year, reports tomorrow after the close. -

CNBC Newsbabes in Cocktail Dresses

Posted by Eddy Elfenbein on February 7th, 2007 at 2:14 pmFeaturing Liz and her Clamen in a Vera Wang.

-

Welcome Back, Carney

Posted by Eddy Elfenbein on February 7th, 2007 at 1:42 pmWe at Crossing Wall Street are very pleased to welcome back John Carney of DealBreaker to the world of blogging.

For the last three weeks, John was out while he was recuperating from a (ahem) “car accident” of some sort. We’ve constructed a timeline of the relevant events.

January 13: Lindsay Lohan checks into rehab.

January 14: John’s “accident.”

February 6: Lindsay Lohan checks out of rehab.

February 7: John returns.

We encourage you not to put two and two together* (although didn’t the Beatles try something like this).

Welcome back, John. We’ve missed you.

*And rehab is so ’05 anyway. -

Highlights from Cisco’s Conference Call

Posted by Eddy Elfenbein on February 7th, 2007 at 12:13 pmCourtesy of SeekingAlpha:

#1Operator: Thank you. And our first question from Brant Thompson, Goldman Sachs.

(The call doesn’t go through)

We’ll move to our next question.

John Chambers: Brant, we’ll get back to you. If you’d replace the phone call for some reason it didn’t go through. Probably not using a Cisco IP phone. We’ll give you a special discount if you want one.#2

Charlie Giancarlo: So we view it as a very promising new area for us. Already many hundreds of millions of dollars for us in revenue. And we really see it as being something that will allow us to gain market share and achieve our growth goals there.

John Chambers: Jeff, two comments. For those of you that haven’t heard Charlie talk very often, that’s has excited as Charlie gets.#3

John Chambers: The exciting thing is that video in my opinion. I’ve never seen there was a killer App until I talked about video.

Flashback to 2001.

“E-learning is the next major killer application,” Cisco CEO John Chambers proclaimed in his keynote here Monday.

#4

Bill Choi – Jeffries: Okay. Thanks. Maybe two quick questions, sir. One, you talked about loosely and then tightly coupling of product architecture strategy. As far as video strength we’re seeing, so far it seems to be very assay specific.

Can you talk about when you anticipate the tight coupling of this, particularly in the 9K as our markets into the routing space when do you expect the strength to occur? And then a follow-up question on switching.

John Chambers: Let me ask, which one do you want? I apologize, because Blair is going to shoot me about talking too long. Give us one question. And I apologize for holding you to one? Would you want the answer to that first one or would you want us to do the second one?

Bill Choi – Jeffries: Let’s do the second one. Switching…

John Chambers: I had a good answer to that first one.(Hat Tip: Owen Thomas).

-

S&P 1450

Posted by Eddy Elfenbein on February 7th, 2007 at 11:34 amThe S&P 500 just got up to 1452. It was briefly — very, very briefly — above 1450 yesterday.

The first time the index closed above 1450 was December 23, 1999. The last time was September 28, 2000. Once we hit 1469.25, then we can say we’re flat for the millennium. The Dow is also in record territory and briefly touched 12,700.

On our Buy List, both FactSet Research Systems (FDS) and Fiserv (FISV) are at new all-time highs. -

The Biggest Secret on Wall Street

Posted by Eddy Elfenbein on February 7th, 2007 at 10:52 amWell, I already used that title before, but here’s another very big secret on Wall Street — mutual savings banks.

Don’t laugh, whenever you hear that a mutual savings bank is about to go public, pay attention. A mutual savings bank is a bank that’s “owned” by its depositors. Most of these institutions are a zillion years old. They’re well run, and they basically have zero overhead.

Most are still based in the Northeast. Every year, a few more decide to go public, and that can be very good news. When the bank’s IPO, the depositors usually get first crack at buying the shares. Also, the IPOs tend to do very well. This is from the Wealth Effect Web site:Historically, these IPOs have been very profitable. The biggest reason for this is the unusual advantage a mutual bank has going into the public offering: the book value (assets minus liabilities) of a bank is essentially cash, and this cash remains the property of the bank after the offering; add to this the cash the bank receives from the IPO, and you will always be buying shares for less than the book value of the newly public bank.

Another reason why mutual bank IPOs have done well, some suggest, is that the bank managements — which receive shares at the offering price — want that price set low enough to leave plenty of room for future gains. A third reason for the success of bank IPOs is that many of these banks were eventually purchased (at a premium) by larger banks looking to consolidate a banking industry strewn far and wide by the legislation of the Great Depression.A few days ago, a reader asked me about Hampden Bancorp (HBNK), which is a MSB that just went public. The bank was founded in 1852, and it has seven branches in and around Springfield, MA.

Last month, the bank sold 7.6 million shares to its depositors at $10 a pop, and the stock is already around $12.50. I found the prospectus at the bank’s Web site. The prospectus also lists the seven MSB IPOs since the beginning of 2005, and the performance of their shares.

Stock……………………………….IPO……After 1 Day….Through 9/1/06

Chicopee Bancorp (CBNK)…..7/20/06……..44.6%…….46.1%

Newport Bancorp (NFSB)…….7/7/06……….28%……….36.2%

Legacy Bancorp (LEGC)………10/26/05……30.3%…….50.4%

BankFinancial (BFIN) ………….6/24/05…….36%……….74.7%

Benjamin Franklin (BFBC)…….4/5/05……….0.6%……..40.7%

OC Financial (OCFL)……………4/1/05………20%……….10%

Royal Financial (RYFL)………..1/21/05……..16%………..51% -

Put this Guy at the Fed

Posted by Eddy Elfenbein on February 6th, 2007 at 9:23 pmCalgary man fined for charging 207,981% interest:

Actually, I do not feel bad for what happened. I was doing like everybody else does. A bunch of other pawn shops in Calgary are doing the same.

-

Bernanke Warns

Posted by Eddy Elfenbein on February 6th, 2007 at 5:07 pm

Bernanke Warns of Possible ‘Crisis’ From Budget Gap

Bernanke warns of falling economy

Bernanke warns of growing rich-poor gap

Bernanke warns action needed soon on budget

Bernanke warns US about burden of ageing population

Bernanke warns against protectionism

Bernanke warns of deficit balloon

Bernanke warns of threat to US prosperity

Greenspan: I’m Totally Broke

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His