-

Silgan Approves Buyback

Posted by Eddy Elfenbein on March 7th, 2022 at 9:59 amThe stock market is down again today as the financial world continues to be impacted by the war in Ukraine. One example is palladium, a metal which you probably don’t think much about. It’s used in catalytic converters, and Russia is a major producer. Palladium is more valuable than gold and it’s nearly doubled in the past three months.

Energy stocks are doing the best today while many financial stocks are lagging. JP Morgan made a new 52-week low.

On Friday, Silgan Holdings (SLGN) said that is has approved a buyback for $300 million worth of its stock through the end of 2026.

“This authorization replaces our prior similar authorization which had expired at the end of 2021 and will allow us to repurchase common stock from time to time through December 31, 2026,” said Adam Greenlee, President and CEO. “As in the past, we maintain a disciplined approach to capital deployment with a priority towards growth investments for the Company,” concluded Mr. Greenlee.

This week, we’re going to get an earnings report from Miller Industries (MLR). That will be the final report of the Q4 earnings season. Later this month, we’ll get earnings reports from SAIC (SAIC) and FactSet (FDS). SAIC’s quarter ended in January while FactSet’s ended in February. FactSet will be on March 24 and SAIC’s will be on March 28.

After that, everything gets back to normal and the Q1 earnings reporting season will start in mid-April.

-

Morning News: March 7, 2022

Posted by Eddy Elfenbein on March 7th, 2022 at 7:01 amIndian Police Arrest Former National Stock Exchange Head

Bankers Are Abandoning Hong Kong as Beijing and Covid Remake the City

Fraud Is Flourishing on Zelle. The Banks Say It’s Not Their Problem.

How War in Ukraine Drives Up Inflation at U.S. Farms, Supermarkets, Retailers

Oil Prices Jump as U.S. Discusses Russian Import Ban

This Russian Metals Giant Might Be Too Big to Sanction

Russian Banks May Issue Cards With China’s Unionpay As Visa, Mastercard Cut Links

How U.S. Law Enforcement Could Take Control Of Russian Oligarchs’ Assets

UBS Has $200 Million Exposure to Russian Assets in Loans to Rich

Uniqlo Owner Pledges to Stay in Russia as Wave of Companies Exit

Congress’ Police Force Declares Emergency Over Trucker Convoys

Car Industry Woes Show How Global Conflicts Will Reshape Trade

Carmakers Race to Control Next-Generation Battery Technology

Dreaming of Suitcases in Space

Why American Mask Makers Are Going Out of Business

Cathie Wood Says She Still Expects To See ‘Spectacular Returns’ Over The Next 5 Years

Be sure to follow me on Twitter.

-

February Jobs Report

Posted by Eddy Elfenbein on March 4th, 2022 at 8:35 amThe February jobs report is out. Last month, the U.S. economy created 678,000 net new jobs. That’s a big beat. Expectations were for 440,000. The unemployment rate ticked down to 3.8%.

The revisions for the previous two months were +92,000. The broader U-6 rate was 7.2%.

The surprise is that the average hourly earnings figure was unchanged. Over the last year, average hourly earnings are up 5.1%.

Private payrolls increased by 654,000. Expectations were for 400,000. Manufacturing added 36,000 jobs.

The labor force participation rate was 62.3%. That’s a post-Covid high.

-

Morning News: March 4, 2022

Posted by Eddy Elfenbein on March 4th, 2022 at 7:02 amGlobal Markets Fall After Russia Shells Ukrainian Nuclear Plant

How China Embraces Russian Propaganda and Its Version of the War

Putin’s Financial Isolation by World’s Powerful Is a Cautionary Tale for Xi Jinping

JPMorgan Warns Russia Headed for 1998-Like ‘Collapse’ in Economy

Economic Ties Among Nations Spur Peace. Or Do They?

Companies Scrap IPOs Amid Russian Invasion of Ukraine

What Is Ukraine Going to Do With All That Donated Cryptocurrency?

London’s Billionaire Playground Is Challenged by Reality of War

Saudi Crown Prince Plays the Oil Card in Quest for U.S. Recognition

UAE Poised for Global Watchdog’s ‘Gray List’ Over Dirty Money

Grab Shares Crash Nearly 40% After Posting A $1 Billion Loss

Amazon Moves to Force FTC Antitrust Decision on MGM Deal

Tech Companies Are Reopening Their Offices, but Tech Work Has Changed Forever

REI Workers in New York Vote to Unionize

Sony And Honda Announce Tie-Up To Make Electric Cars

Be sure to follow me on Twitter.

-

Morning News: March 3, 2022

Posted by Eddy Elfenbein on March 3rd, 2022 at 7:06 amTurkey’s Inflation Rate Hits A New 20-Year High Of 54%

Oil Surge Turns India’s Bonds Into Most Risky in Emerging Asia

Europe’s Biggest Port Is Very Worried About Russian War Impact

Russia-Ukraine Conflict Highlights Wheat Supply Vulnerability

Talking War and Market Volatility With a Giant of Economics

Sanctions Significantly Increase Chance Of Russia International Debt Default, Analysts Warn

Russia Exposure Wipes $100 Billion From European Stocks

Norway Wealth Fund Prepares $2.8 Billion Loss on Russian Holdings

The End of the Oligarch Era Nears With Putin’s Miscalculation in Ukraine

The Teenager Who Tracked Elon Musk’s Jet Is Now Tracking Russian Oligarchs

U.S. Activist Investors, Icahn Cry Foul Over Proposed Stock Disclosure Rule

Twitter Wants to Reinvent Itself, by Merging the Old With the New

‘We Were Terrified’: Block Co-Founder Explains How The Fintech Giant Avoided ‘Death By Amazon’

This Social Club Runs on Crypto Tokens and Vibes

Nissan Ex-Executive Gets Suspended Sentence in Carlos Ghosn Case

Be sure to follow me on Twitter.

-

Powell Said the Fed Is Ready to Raise Rates

Posted by Eddy Elfenbein on March 2nd, 2022 at 3:15 pmThe stock market is having another good day today. Of course, it’s gotten so much more volatile recently that tomorrow could easily wipe out today’s gains. Today’s move seems fairly broad and no major areas are being left behind.

Yesterday, the ISM Manufacturing Index fell to 57.7. That’s still pretty good even though it’s the lowest in 14 months. That’s probably an Omicron effect. Any number above 50 means that the factory sector is growing.

This morning’s ADP jobs report said that 475,000 private payroll jobs were added last month. ADP also revised their January jobs number from a loss of 301,000 to a gain of 509,000. That just wrecks their credibility.

Jerome Powell said today that rate hikes are coming and that the events in Ukraine probably won’t change that. The next Fed meeting is two weeks from today. The futures market now shows a 98% chance of a rate hike.

-

Morning News: March 2, 2022

Posted by Eddy Elfenbein on March 2nd, 2022 at 7:01 amMajor Western Companies Retreat From Russia

Russian Aviation Sector Isolated As Boeing Suspends Parts, Maintenance

Russia’s Top Bank Quits Europe Due To Sanctions

Russia Keeps Stock Market Closed in Longest Pause Since 1998

Eurozone Inflation Hits Fresh High as Ukraine Invasion Confronts ECB With Dilemma

China Moves to Secure Commodities Rocked by Ukraine War

As Oil Soars, OPEC and Its Allies Are Not Likely to Offer Relief

Crypto Has Become a Tool in Conventional Warfare. But Not for Long.

Millions for Crypto Start-Ups, No Real Names Necessary

How the Russia-Ukraine War Threatens the Dollar’s Dominance

War Risk, Liquidity Squeeze Spur Bets on a Less Aggressive Fed

$10 Toothpaste? U.S. Household Goods Makers Face Blowback On Price Hikes

Biden Says Fighting Inflation Is ‘Top Priority’ as Prices Bite Consumers

Ford Splits Into Electric and Gas Divisions to Speed Up Transition

Struggling EV Startup Lordstown Motors Loses GM As Investor

A Billionaire’s Heir Hangs Up His Healing Crystal to Fix Capitalism

Be sure to follow me on Twitter.

-

CWS Market Review – March 1, 2022

Posted by Eddy Elfenbein on March 1st, 2022 at 8:53 pm(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

The Finance War

I’ve been impressed by the way the world has come together to denounce Russia’s invasion of Ukraine. For our purposes, I’ve been especially impressed by the way the global financial markets can make an entire country’s finances persona non grata.

I can’t think of a similar event where a rogue country was virtually erased from any financial dealings. The results have been breathtaking. The Russian ruble has been reduced to rubble. The Russian currency plunged to less than one penny. At one point, the ruble got to 117 to the dollar. To give you another example, shares of Sberbank, Russia’s largest bank, had a rather unpleasant day on Monday.

The Russian Fed hiked interest rates to 20%. That’s the same level that our Fed had in 1981. Some Russian bonds are trading at 30 or 40 cents on the dollar. The Putin regime is nearly completely unable to pay its bills and some Russian banks were kicked off the SWIFT messaging system.

The Russian Fed has even temporarily banned western companies from exiting Russian investments. If you happen to be a Russian oligarch, I’d be very cautious about what happens to your yacht or bank account.

We’ve seen a reaction in our markets. On Tuesday, shares of JPMorgan (JPM) fell to a new 52-week low. Many other banks came under pressure. Conversely, defense stocks like Raytheon (RTX) and Lockheed Martin (LMT) both made new 52-week highs on Tuesday.

In the commodity pits, the price for wheat has been soaring. Futures contracts for natural gas soared 23%.

On our Buy List, shares of SAIC (SAIC) have crept higher over the past few days. This company is basically the IT support desk for the entire Pentagon. I’m exaggerating, but not by much. On February 23, SAIC closed at $79.10 per share. Today it closed at $88.18 per share. That’s an 11.5% gain in four trading days. I don’t have the next earnings date yet, but it will probably be in late March.

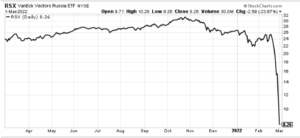

The Russia ETF (RSX), which is priced in dollars, has lost 68% in the last eight trading days.

We’re seeing something rather new in warfare: financial warfare. Of course, there have been sanctions before, but nothing quite like this. The closest I can think of is the People Power Revolution in the Philippines in 1986.

In 1983, Benigno Aquino, an opposition leader to the Marcos regime, returned from exile. He was immediately assassinated at the airport which now bears his name. Once the assassination happened, world financial markets wanted nothing to do with the Marcos regime. How can you trust a country to pay its bills when it kills people in broad daylight?

The currency and their bonds plunged. Inflation soared and it turned more and more people against the government. Many revolutions in history were preceded by nasty bouts of inflation. An unsound currency is a good tell that a government is not to be trusted. Interestingly, Ukraine has been able to raise lots of money from crypto contributors. There’s a new twist.

I won’t make any predictions. (I’m only a former PFC.) But I’ll caution you not to worry that what happens in Europe will greatly impact our portfolios. People will still buy Hershey’s (HSY) chocolate and Stepan’s (SCL) chemicals. We’ll probably pay more for certain items. The price for oil surged past $100 per barrel to hit an eight-year high.

As awful as the events are, the impact to the U.S. economy will probably be small. At least for now.

The Limits to Growth Turns 50

Fifty years ago today, a fascinating book was published called The Limits to Growth. The book claimed that the world would run out of valuable resources by the 1980s and 1990s. Its forecast was based on computer models by Jay Forrester of MIT. The book claimed that the world population and industrial production would soon massively decline.

Yikes! Predicting the end of the world is big business. Apparently, the public loves being told that the end is nigh. The disaster stuff was especially popular in the 1970s. Remember Soylent Green? That film takes place in…2022.

The Limits to Growth was a smash hit. It was published in 30 languages, and it sold 30 million copies. Despite its popularity, all of the book’s predictions completely flopped. The book was being updated as recently as 2012.

Why did they get it so wrong? Julian Simon pinpointed their error. Let me turn it over to Wikipedia:

[Simon argued that] the very idea of what constitutes a “resource” varies over time. For instance, wood was the primary shipbuilding resource until the 1800s, and there were concerns about prospective wood shortages from the 1500s on. But then boats began to be made of iron, later steel, and the shortage issue disappeared. Simon argued in his book The Ultimate Resource that human ingenuity creates new resources as required from the raw materials of the universe. For instance, copper will never “run out”. History demonstrates that as it becomes scarcer its price will rise and more will be found, more will be recycled, new techniques will use less of it, and at some point a better substitute will be found for it altogether.

This is a subtle point that’s simple but explains a lot. People are smart. They constantly innovate and update. I bring this up because that’s why the stock market has been such a great long-term investment. It’s the only investment that taps peoples’ ability to create and innovate. It’s also why we’re focused on the long term.

The winning strategy has been to ignore the fearmongers and stick with the companies that have a loyal following. Speaking of investing wisdom.

Warren Buffett’s Shareholder Letter

Last weekend, Warren Buffett released his most-recent shareholder letter. He’s been writing these for over 50 years. They often contain valuable insights from the legendary investor. I wanted to pass along a few items.

Buffett noted that Berkshire used to pay $100 in taxes per day in the 1950s and 60s. Today, it pays $9 million in taxes each day.

Buffett said that Berkshire’s balance sheet now has $144 billion in cash. Of that, $120 billion is held in short-term Treasuries. That means that Berkshire finances 0.5% of Americans’ publicly-held debt.

He says that he doesn’t want to hold that much debt, but there’s not much he sees that excites him. Why is that?

“That’s largely because of a truism: Long-term interest rates that are low push the prices of all productive investments upward, whether these are stocks, apartments, farms, oil wells, whatever. Other factors influence valuations as well, but interest rates will always be important.”

The bold is mine. This is very true and this fact hangs over the entire market right now. Rates are low and that distorts everything.

Buffett also came to the defense of share buybacks.

Our final path to value creation is to repurchase Berkshire shares. Through that simple act, we increase your share of the many controlled and non-controlled businesses Berkshire owns. When the price/value equation is right, this path is the easiest and most certain way for us to increase your wealth. (Alongside the accretion of value to continuing shareholders, a couple of other parties gain: Repurchases are modestly beneficial to the seller of the repurchased shares and to society as well.)

Buffett is correct. A few years ago, share buybacks emerged as a public enemy. This is nonsense. They’re perfectly fine as long as the company isn’t vastly over-paying for the shares.

Finally, I have to highlight this: “I taught my first investing class 70 years ago.”

Wow.

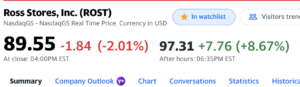

Ross Stores Beats Earnings and Raises Its Dividend

As I was writing this newsletter, Ross Stores (ROST) released its Q4 earnings report and it was a good one. For Q4, Ross earned $1.04 per share which beat expectations by seven cents per share. The deep-discounter is also raising its dividend by 9%.

The shares are up nicely in the after-hours market. I’ll have more details on Ross and its earnings report in our premium issue on Thursday. (That’s called a tease.) If you haven’t signed up for the premium issues, you can just use this link. Thank you!

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

-

Ross Stores Earned $1.04 per Share for Q4

Posted by Eddy Elfenbein on March 1st, 2022 at 4:08 pmRoss Stores (ROST) reported Q4 earnings of $1.04 per share. This compares with $1.28 per share for the same quarter one year earlier.

Sales for Q4 were $5.0 billion, with comparable store sales up 9% versus the same period in 2019.

For the whole year, Ross made $4.87 per share up from $4.60 in 2019. Total sales for 2021 grew 18% to $18.9 billion, up from $16.0 billion in fiscal 2019, with comparable store sales up 13%.

Barbara Rentler, Chief Executive Officer, commented, “We achieved strong sales results in the fourth quarter despite the negative impact from both the surge in Omicron cases during the peak holiday selling period and continued supply chain congestion.”

She continued, “Fourth quarter operating margin of 9.8% was down from 13.3% in 2019 mainly due to ongoing headwinds from higher freight, wages, and COVID-related costs.”

Ross also raised its dividend by 9% to 31 cents per share. The company approved a two-year buyback program to repurchase up to $1.9 billion of common stock through fiscal 2023.

For this year, Ross projects earnings of $4.71 to $5.12 per share. For Q1, they see earnings of 93 cents to 99 cents per share.

-

Morning News: March 1, 2022

Posted by Eddy Elfenbein on March 1st, 2022 at 7:10 amWar in Ukraine Disrupts Ships Around the Globe

Russia To Temporarily Ban Foreigners From Selling Assets

The List of Foreign Companies Pulling Out of Russia Keeps Growing

U.S. Expects Chinese Tech Firms to Help Choke Off Russia Supply

China Spy Think Tank Advising Xi Predicts Russia Sanctions Will Backfire

As Sanctions Batter Economy, Russians Face the Anxieties of a Costly War

Ukraine War Tests the Power of Tech Giants

Google, Meta Face Penalties In Russia As Deadline Passes To Open Local Offices

Nord Stream 2 Owner Considers Insolvency After Sanctions

Toyota Stops Production In Japan After A Cyberattack At A Supplier

Toshiba Replaces CEO Again but Sticks With Two-Way-Split Plan

Target Surges on Robust Outlook, Strong Holiday Earnings

Here Comes the Full Amazonification of Whole Foods

Companies Seize March as a Moment to Reopen the Office

Summer Interns Back Out for Better Pay and Perks

Be sure to follow me on Twitter.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His