-

3Q GDP Revised to 2.0%

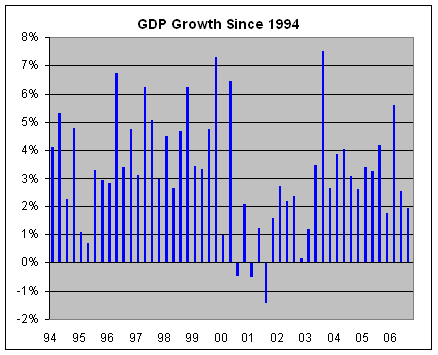

Posted by Eddy Elfenbein on December 21st, 2006 at 10:11 amThis morning, the government revised third-quarter GDP growth to 2.0%. The initial estimate was for 1.6%. Then it went to 2.2%, and now it’s back to 2.0%.

Here’s a look at GDP growth going back to 1994:

-

Sarkozy Calls Shareholders Hooligans

Posted by Eddy Elfenbein on December 21st, 2006 at 9:45 amFrom Nicolas Sarkozy, a candidate for president of France:

Our country has to get organised to stop the actions of shareholders who… aren’t entrepreneurs but who behave like hooligans….

As a proud shareholder hooligan, I almost take offense. By the way, Sarkozy is running as the free-market reformer.

-

Biomet PE Group to Bid for Smith & Nephew

Posted by Eddy Elfenbein on December 21st, 2006 at 9:33 amThis is getting interesting. There’s a report that the private equity group that’s buying Biomet is now considering a bid for Smith & Nephew.

Just before Biomet’s board accepted the private equity group’s buyout offer, Smith & Nephew considered making a bid for Biomet. Their bid must have been very low, or Biomet’s board wanted to make it clear that it had explored all options.

In any event, the idea of Biomet merging with Smith & Nephew still lives. -

Have Dwight Call Your Friends

Posted by Eddy Elfenbein on December 21st, 2006 at 7:16 am

If you’re a fan of The Office, go to this site. Click on “Get a Call,” and follow the steps from there. -

Update on Bed Bath & Beyond

Posted by Eddy Elfenbein on December 21st, 2006 at 7:07 amI’ve had some time to review the Bed Bath & Beyond (BBBY) conference call (see here, via Seeking Alpha). First, the company had a charge to SG&A last quarter of $7.2 million related to the review of stock option grants and procedures. We already new this was coming. In fact, the company said it was going to be $8 million. After tax, that comes to about two cents a share, so we have our earnings shortfall right there. The company said there might be a little more this quarter.

Next, CEO Steven Temares commented on employee tax charges the company was taking as a result of its stock options grants.We anticipate the potential cash payments pursuant to the program to be approximately $40 million. While we are still reviewing the accounting treatment related to the potential program, we anticipate the pre-tax income statement impact in the fourth quarter to be slightly higher than the total cash payments. The potential cash outlay primarily represents payments to our employees in connection with increasing the exercised prices on certain stock option grants so as to protect them from certain potential adverse tax consequences.

It’s currently believed it is likely the company will recoup a substantial portion of the cash outlay over the next several years through higher proceeds from future stock option exercises, although this recovery will not flow through the income statement.

I want to emphasize that any program arrived at by our Board will be consistent with our company’s beliefs that our people are the reason for our success. As such, we would want to protect them against any adverse tax consequences for events that were beyond their control.

While the program has not been finalized, Warren, Len and I as executive officers, who are also members of the Board of Directors, has informed the Board that we decline to be considered for payments.That only seems fair. Employees shouldn’t be punished for this, and the company did the right thing. The charge will amount to about nine cents a share.

Now let’s turn to SG&A, which I initially found a little troubling:Selling, general and administrative expenses for the fiscal third quarter were about $493 million, compared with approximately $410 million in the corresponding quarter a year ago. As a percentage of net sales, SG&A expenses were 30.4% compared with 28.3% a year ago, as a result of the previously mentioned $7.2 million increase in stock-based compensation expense along with legal and accounting charges related to the stock option review and a relative increase in advertising, which includes an increase in paper cost and postal rates.

In addition, there were one-time benefits experienced in the prior year for settlement of credit card litigation and certain insurance recoveries which we did not have in this year’s third quarter. As a result of the deleverage in SG&A expense partially offset by the improvement in gross profit margin, the operating profit margin in the fiscal third quarter decreased by approximately 115 basis points. The company’s results also benefited from a reduction in its year-to-date effective tax rate from 36.6 to 36.3%, resulting in a third quarter effective tax rate of 35.8%.The company also said that it’s targeting earnings of 78 cents a share for the February quarter, which is a penny less than what it said on its last conference call.

My view is that the operationally, BBBY look just fine. The company’s sales-per-share increased by 17.4% from last year. That’s darn good. It’s been helped by the company’s aggressive buyback program. Share buybacks don’t impress me much, but with BBBY, it really has an effect on its earnings statement. Today, BBBY said it’s going buy back another $1 billion worth of stock.

Unfortunately, the company hasn’t had all the benefits of its growth in gross margins reach the bottom line. Gross profits-per-share were up 20% last quarter. Unfortunately, they dug around looking for one thing (back-dating), and the probe found an even bigger charge (this tax thing)!

On today’s call, the company said that it’s looking for sales- and earnings-per-share growth of 10% next year…(cough)…low-ball..(cough).

Conservatively, I’d say that BBBY’s calendar year-earnings will be about $2.34 a share next year. (Their fiscal year doesn’t follow the calendar year, but I’m estimating for sake of comparison.) That means that the stock is going for just 17 times next year’s earnings, which strikes me as a very good price. -

In China Feng Shui Guys See Market Top

Posted by Eddy Elfenbein on December 21st, 2006 at 6:51 amFrom Reuters:

Forget fund flows and profit predictions, 2007 is about “fire sitting on water”. Buy oil, avoid metals, and don’t get your fingers burnt.

Feng shui experts steeped in the ancient Chinese knowledge of geomancy, or natural energies, see a turbulent year ahead for both markets and mankind.

“The elements — they are in conflict,” said Raymond Lo, a practitioner for more than 10 years, whose office close to Hong Kong’s Victoria Harbour is considered a repository of positive feng shui energies in this hotbed of capitalism.

“Because it’s fire and water, and they’re not in harmony. So therefore next year in January, it’s not so peaceful.”Wait, don’t get my fingers burnt! Oh, that does make more sense.

-

Bed Bath & Beyond Earned 50 Cents a Share

Posted by Eddy Elfenbein on December 20th, 2006 at 4:29 pmBed Bath & Beyond (BBBY) just reported earnings of 50 cents a share, two cents below estimates. Wall Street was expecting earnings of 52 cents a share. Last year, BBBY made 45 cents a share.

Quarter Sales Gross Profit Operating Profit Net Profit EPS $356,633 $146,214 $28,015 $17,883 $0.06 $451,715 $185,570 $53,580 $33,247 $0.12 $480,145 $196,784 $50,607 $31,707 $0.11 $569,012 $238,233 $77,138 $48,392 $0.17 $459,163 $187,293 $36,339 $23,364 $0.08 $589,381 $241,284 $70,009 $43,578 $0.15 $602,004 $246,080 $64,592 $40,665 $0.14 $746,107 $311,802 $101,898 $64,315 $0.22 $575,833 $234,959 $45,602 $30,007 $0.10 $713,636 $291,342 $84,672 $53,954 $0.18 $759,438 $311,030 $83,749 $52,964 $0.18 $879,055 $370,235 $132,077 $82,674 $0.28 $776,798 $318,362 $72,701 $46,299 $0.15 $903,044 $370,335 $119,687 $75,459 $0.25 $936,030 $386,224 $119,228 $75,112 $0.25 $1,049,292 $443,626 $168,441 $105,309 $0.35 $893,868 $367,180 $90,450 $57,508 $0.19 $1,111,445 $459,145 $155,867 $97,208 $0.32 $1,174,740 $486,987 $161,459 $100,506 $0.33 $1,297,928 $563,352 $231,567 $144,248 $0.47 $1,100,917 $456,774 $128,707 $82,049 $0.27 $1,273,960 $530,829 $189,108 $120,008 $0.39 $1,305,155 $548,152 $190,978 $121,927 $0.40 $1,467,646 $650,546 $283,621 $180,980 $0.59 $1,244,421 $520,781 $150,884 $98,903 $0.33 $1,431,182 $601,784 $217,877 $141,402 $0.47 $1,448,680 $615,363 $205,493 $134,620 $0.45 $1,685,279 $747,820 $304,917 $197,922 $0.67 $1,395,963 $590,098 $148,750 $100,431 $0.35 $1,607,239 $678,249 $219,622 $145,535 $0.51 $1,619,240 $704,073 $211,134 $142,436 $0.50 Historically, more than one-third of the company’s earnings comes during this (the February) quarter. I have to say that I’m very impressed with BBBY’s gross margins. For this quarter, gross margins topped 43%. That’s an improvement of 2.6% in the last six years.

Perhaps I’m missing something, but I don’t see where the big increase in SG&A is coming from (that’s gross profit minus operating profit). This had been decreasing for several quarters. It jumped in the four quarters prior to this one, but that was due to that FASB 123(R) jazz. That I understand, but this I don’t get.

Like I said, I could be missing something. This is just a first look. Perhaps the company will address it on the call (btw, BBBY is one of the few companies that doesn’t take on questions on its call).

The company also announced a $1 billion share buyback program. The AP also notes:Bed Bath & Beyond expects a $40 million charge during its fiscal fourth quarter as part of “a program intended to protect over 1,600 employees from certain potential adverse tax consequences.” The tax consequences are a result of historical issues with some of the company’s stock option grants disclosed through a company stock option review.

The Securities and Exchange Commission is conducting an informal investigation into Bed Bath & Beyond’s stock option grant practices. The U.S. Attorney for the District of New Jersey is conducting a similar inquiry. Both probes are looking at backdating, in which the vesting date of a stock option is changed to make it more valuable to the holder. While not illegal, the practice must be properly disclosed to shareholders. -

Vornado Realty Trust

Posted by Eddy Elfenbein on December 20th, 2006 at 11:54 amMore boring stocks. Today, I give you Vornado Realty Trust (VNO). Over the last 32 years, shares of Vornado are up more than 600-fold.

The flat gold line on the chart is the S&P. It’s not really flat, it just looks that way in comparison to Vornado.

By the way, that 60,000% doesn’t include dividends. Since VNO is a REIT, it pays fairly generous dividends. The current yield is 2.8%. If I had to estimate, I’d say that dividends by themselves gave VNO shareholders about a 200% return since 1974, meaning the stock’s total return is about 180,000%. -

Blankfein Rakes In $54 Million

Posted by Eddy Elfenbein on December 20th, 2006 at 6:46 amThe WSJ reports that Lloyd Blankein’s, Goldman Sachs’ CEO, bonus was for $54 million, the biggest in Wall Street history.

Mr. Blankfein’s pay package reflects the firm’s performance atop the Wall Street heap over the past year, when its profits rose 70% to $9.54 billion and its stock price surged 59%, increasing its stock-market value by $31 billion.

But it also reflects the inflation in Wall Street CEO pay packages, which last year generally came in at between $30 million and $40 million, with the stock market in the fourth year of a bull run and a boom in private-equity buyouts and hedge-fund trading.

A former tax lawyer and gold salesman who rose to become head of the firm’s fixed-income, currency and commodities division in 1998, the 52-year-old Mr. Blankfein epitomizes Goldman’s risk-taking culture.

His latest pay package includes a cash bonus of $27.3 million, restricted shares valued at $15.7 million and options valued at $10.5 million, according to a filing yesterday by Goldman, which disclosed the stock awards and included the cash bonus. He also earned a salary of $600,000.Goldman has 450 million shares, so Blankfein’s pay comes to 12 cents a share. In the past year, the stock is up $76.

-

An Open Letter to Biomet Shareholders

Posted by Eddy Elfenbein on December 19th, 2006 at 2:02 pmVote Against the Private Equity Buyout

Dear Shareholders of Biomet,

On Monday, the Board of Directors of Biomet (BMET) announced that it agreed to a buyout offer from a consortium of private equity frims. The consortium consists of the Blackstone Group, Goldman Sachs Capital Partners, Kohlberg Kravis Roberts, Texas Pacific Group and one of Biomet’s founders, Dane Miller. The deal is for $10.9 billion ($44 a share) and is due to be completed by October 31, 2007.

We believe this is a poor deal for shareholders of Biomet and we urge all shareholders to vote against it.

Biomet’s track record is known to everyone. For the last three decades, the company has been one of the great success stories of American free enterprise. Biomet has delivered record sales and earnings every year since it began operations in 1977. This is an astounding achievement. Moreover, the company’s products have helped millions of people all over the world lead a better life. This is something we all should be proud of.

In 1977, the company had sales of just $17,000. For FY 2006, Biomet’s sales exceeded $2 billion. Today Biomet employs over 6,000 people. Since 1982, the stock has split nine times. In the last 20 years, shares of Biomet have increased by more than 40-fold.

Biomet has regularly had its return-on-equity top 20%. Additionally, the company has no long-term debt and a very healthy cash position.

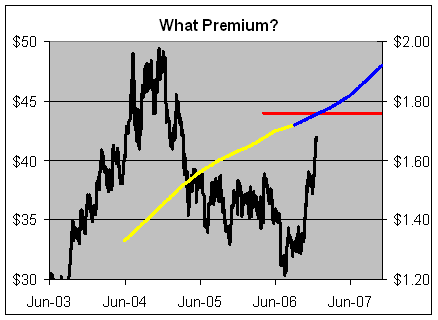

Give all these facts, we’re very disturbed by management’s decision to sell Biomet for such a low price. Monday’s press release notes that $44 is “a 27% premium over Biomet’s closing price on April 3, 2006.”

This is a misleading fact that was repeated with question through much of the financial media. This “premium” is measured from over eight months ago to more than ten months in the future. Annualized, this premium works out to 16.1% which is less than the shares’ long-term performance.

Additionally, we believe the shares were unusually low-priced in April so the appearance of a premium is illusionary. Forty-four dollars a share is not only well below Biomet’s high price from 2004, but it’s also below the average share price for the entire second half of 2004. Since that time, Biomet’s sales and earnings have continued to increase.

The graph above shows Biomet’s share price (black line) with the $44 buyout offer (red line). The yellow line is Biomet’s earnings-per-share (right scale), and the blue portion is Wall Street’s consensus projection. The earnings and share prices and scaled by a ratio of 25 to 1.

For a number of reasons, shares of Biomet and the entire health care sector have been punished over the past year. This should not be a reflection on Biomet’s long-term intrinsic value. And it should not be a reason to sell the company at a distressed price. Bear in mind that the stock often traded above 25 times earnings. Despite being called a premium, the private equity deal represents a substantial discount to Biomet’s historic valuation. We have to asked the Board of Directors, “What’s the hurry?”

While there certainly are problems with Biomet’s business, particularly in the spinal business, these problems are a small part of the company’s overall business. Consider that over the next decade, the number of Americans aged 55 to 75 will nearly double. David Phillips at 10-Q Detective notes that “hip and knee and extremity joint replacements account for more than 95% of all orthopedic implants and Biomet holds about 12% of this market, which accounted for 68% of the company’s net sales in FY 2006.”

We’re not opposed to a buyout offer, but we encourage the Board of Directors to consider other offers. The present offer undervalues Biomet’s potential and does not adequately reflects its proper value.

We encourage all shareholders to let the board know that this deal is unsatisfactory and not in the best interest of shareholders. If it comes to vote, we encourage a no vote on the present offer.

Sincerely,

Eddy Elfenbein

Crossing Wall Street

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His