-

Bambi on What Yahoo Did Wrong

Posted by Eddy Elfenbein on December 11th, 2006 at 3:51 pmBambi Francisco does a good take down on how Yahoo (YHOO) missed, and keeps missing, the ball.

-

Craig’s List: Delightfully Communist

Posted by Eddy Elfenbein on December 11th, 2006 at 12:58 pmDealBook writes about the appearance of Craig’s List at the UBS global media conference.

When one analyst asked how CL plans to maximize its revenue, the company said, “um yeah, we’re really not interested in that stuff.”

A riot nearly broke out.Following the meeting, Mr. Schachter wrote a research note, flagged by Tech Trader Daily, which suggests that he still doesn’t quite get the concept of serving customers first, and worrying about revenues later, if at all (and nevermind profits). Craigslist, the analyst wrote, “does not fully monetize its traffic or services.”

Mr. Buckmaster said the company is doubling in size every year, as measured by page views and listings.

Larry Dignan, writing on Between the Lines blog at ZDNet, called Mr. Buckmaster “delightfully communist,” and described the audience as “confused capitalists wondering how a company can exist without the urge to maximize profits.”A Web site that doens’t run ads? What-EVER!

-

Smith & Nephew Poised to Bid for Biomet

Posted by Eddy Elfenbein on December 11th, 2006 at 10:32 amWhoa, this is big. The Financial Time‘s Alphaville is reporting that Smith & Nephew is in merger talks with Biomet (BMET). Coming after Golden West Financial, this would be our second Buy List merger of the year.

Smith & Nephew is in preliminary merger discussions with Biomet, its US rival best known for its artificial hips and other replacement joints, in a deal that could double the size of the British healthcare group. While sources stressed last night that the talks were at a very early stage, the deal is aimed at creating an orthopaedic specialist worth up to $20bn and capable of competing against the US sector leaders, Zimmer and Stryker.

Morgan Stanley, Biomet’s financial adviser, was drafted in to work on the company’s options in the spring following the sudden resignation of its co-founder and president, Dane Miller. Biomet is believed to have also held discussions with JPMorgan private equity.

S&N is valued at £4.8bn ($9.2bn), while Biomet’s market cap is $8.9bn. S&N would likely demerge Biomet’s dental business, which has been valued at $2bn. Zimmer has been mooted as a possible buyer.Biomet is up big today. My hope is that they accept nothing less than $45 a share.

-

Damn It Feels Good to be a Trader

Posted by Eddy Elfenbein on December 11th, 2006 at 7:26 amCheck out these results from the big houses.

This week begins around round of earnings reports from the brokers. Goldman (GS) leads off tomorrow, Bear Stearns (BSC) and Lehman (LEH) on Thursday and Morgan (MS) follows next Tuesday.

The party, however, could be coming to an end. Bloomberg notes:Merrill’s Guy Moszkowski, the No. 1-ranked U.S. brokerage analyst by Institutional Investor magazine, estimates the combined profits of Goldman, Morgan Stanley, Lehman and Bear Stearns will fall 5.8 percent in 2007. Revenue will decline about 2 percent, compared with a 31 percent gain this year.

Trading revenue, which accounts for about half of the firms’ total, will fall 3.7 percent next year, Moszkowski said. Revenue from investment banking, which includes securities underwriting and providing mergers advice, probably will rise 7.8 percent, he forecast. Asset management will gain 11 percent.

Investment banking executives, including Goldman CEO Lloyd Blankfein, say their traders thrive on price swings. The volatility of U.S. Treasury bonds slipped this year to the lowest in five years and is the lowest in a decade for U.S. stocks, reducing the firms’ opportunity to make money on hedging and trading for clients and themselves. Trading volume in stocks on the S&P 500 fell in each of the past three months from a year earlier.Citigroup‘s (C) stock has badly lagged this sector. As I’ve said before, I think it would be a good move to spin off both Smith Barney and Salomon Brothers.

-

Five Macroeconomic Myths

Posted by Eddy Elfenbein on December 11th, 2006 at 7:03 amNobel Prizer Edward Prescott looks at Five Macroeconomic Myths in today’s Wall Street Journal. Here’s #1, “Monetary policy causes booms and busts.”

Greg Mankiw, former chairman of the Council of Economic Advisers, wrote the following in a 2002 paper: “No aspect of U.S. policy in the 1990s is more widely hailed as a success than monetary policy. Fed Chairman Alan Greenspan is often viewed as a miracle worker.” Or, as Mr. Mankiw later asks, was Mr. Greenspan just lucky?

One of the mysteries of the 1990s is how to explain the economic boom when the increase in capital investments — as measured by the national accounts — grew at a subdued pace. The numbers simply don’t add up. However, it turns out that something special happened in the 1990s, and it wasn’t monetary policy. In a recent paper, Minneapolis Fed senior economist Ellen McGrattan and I show that intangible capital investment — including R&D, developing new markets, building new business organizations and clientele — was above normal by 4% of GDP in the late 1990s.

This difference is key to understanding growth rates in the 1990s: Output, correctly measured, increased 8% relative to trend between 1991 and 1999, which is much bigger than the U.S. national accounts number of 4%. Associated with this boom in unmeasured investment is the huge amount of unmeasured savings that showed up in the wealth statistics as capital gains. This was the people’s boom, the risk-takers’ boom. We should hang gold medals around these entrepreneurs’ necks. So indeed, it does seem that Mr. Greenspan was lucky in that a boom happened under his watch; but we can at least say that he did a pretty good job of keeping inflation in check. Here’s hoping for the same performance from our current chairman.

What about busts? Let’s begin with the assumption that tight monetary policy caused the recession of 1978-1982. This myth is so firmly entrenched that I could have called this downturn the “Volcker recession” and readers would have understood my reference. To accept the myth, you have to accept a consistent relationship between monetary policy and economic activity — and as we’ve just seen, this relationship is simply not evident in the data.

Between 1975 and 1980, the inflation-corrected federal funds rate was low; at the same time, output trended upward until late 1978. So far, things look somewhat promising for the mythmakers. But looking closer at the data we see that output began its downward trend in late 1979 while monetary policy was still easy through most of 1980. Also, output continued its decline through 1982, when it began to climb at a time when monetary policy remained tight.

These facts do not square with conventional wisdom. Our obsession with monetary policy in the conduct of the real economy is misplaced.

One caveat: I am not saying that there are no real costs to inflation — there certainly are. And if we get too much inflation we can exact high costs on an economy (witness Argentina as an example). However, I am talking here of the vast majority of industrialized countries who live in a low-inflation regime and who are in no danger of slipping into hyperinflation. It is simply impossible to make a grave mistake when we’re talking about movements of 25 basis points.It’s true, the Fed doesn’t run the world. Please don’t tell the gold bugs.

-

The Limits of Economics

Posted by Eddy Elfenbein on December 9th, 2006 at 3:40 pmHere’s a fascinating article from Christopher Hayes on the limits of economics:

The simple models have an explanatory power that is thrilling. Once you’ve grasped the aggregate supply/aggregate demand model, you understand why stimulating demand may lead, in the short run, to growth, but will also produce inflation. But the content of that understanding turns out to be a bit thin. Inflation happens because, well, that’s where the lines intersect. “A little economics can be a dangerous thing,” a friend working on her Ph.D in public policy at the U. of C. told me. “An intro econ course is necessarily going to be superficial. You deal with highly stylized models that are robbed of context, that take place in a world unmediated by norms and institutions. Much of the most interesting work in economics right now calls into question the Econ 101 assumptions of rationality, individualism, maximizing behavior, etc. But, of course, if you don’t go any further than Econ 101, you won’t know that the textbook models are not the way the world really works, and that there are tons of empirical studies out there that demonstrate this.”

-

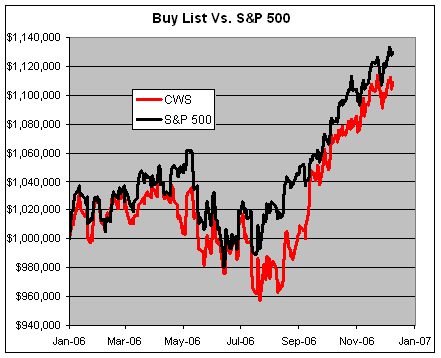

The Buy List So Far

Posted by Eddy Elfenbein on December 8th, 2006 at 9:49 pmWith three weeks left, our Buy List is up 10.88% for the year, compared with 12.94% for the S&P 500 (not including dividends). The Buy List is about 20% more volatile than the rest of the market.

By looking at the current results of each stock on the Buy List, you can see why diversification is so important. Look at the spread of the results (from a high of 61% to a loss of -19%). Five stocks are currently up over 29%, yet eight stocks are down for the year.

I should add that Biomet (BMET) finally made a new high today. This stock has been terrified of $40 a share, but nevertheless, it finally hit that number for the first time in 21 months.

I’ll unveil the new Buy List for 2007 next Friday. The rules are, once the Buy List is set, I can’t touch it for the entire year. -

Good Stocks No One Knows About

Posted by Eddy Elfenbein on December 8th, 2006 at 12:49 pmI’m always amazed at the number of stocks that have been great long-term performers, yet no one knows about them. Many highly profitable stocks are completely ignored by Wall Street. Here are a few examples:

Hawkins (HWKN) is a small chemical company in Minnesota. The stock has creamed the market for decades (the gold line is the S&P 500). Hawkins has just 235 employees. They made $9 million last year, which Wal-Mart makes in about eight hours. No analysts cover it, and yesterday it had zero volume. They might as well be private equity.

Here’s a good one. Weyco Group (WEYS) is a 110-year-old shoe company based in Milwaukee. Thirty-two years ago, you could have picked up a share for 20 cents (adjusted for splits totaling 54-for-1). Weyco also pays a dividend. One analyst covers it.

Met-Pro (MPR) makes pollution control equipment. The company has a market cap of $160 million.

-

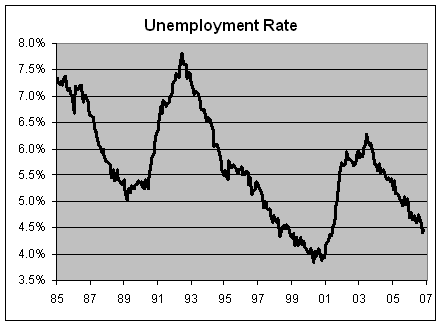

Today’s Jobs Report

Posted by Eddy Elfenbein on December 8th, 2006 at 10:18 amThe media is reporting that the unemployment rate increased from 4.4% to 4.5% in November. This is technically true, but it owes some credit to rounding. I got the raw data and the jobless rate increased from 4.42% to 4.47%.

Here’s what the past twenty-odd years have looked like:

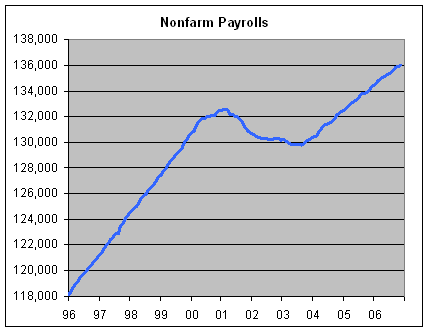

And here’s nonfarm payrolls over the past ten years:

You can see that job growth is slower in this recovery than in the 90s. -

Hedge Funds Now An Official Cultural Phenomenon Fit to Print

Posted by Eddy Elfenbein on December 8th, 2006 at 6:19 am

So sayeth The New York Times:In October, John Wiley & Sons rolled out its latest how-to book, “Hedge Funds for Dummies.’’ Doug Ellin, the creator of “Entourage” on HBO, is seeking to transplant that show’s successful premise of dudes living large to the world of seeking alpha. And for those who just want to look like a hedge fund manager, Kenneth Cole offers the Hedge Fund — a leather loafer available in black or brown, recently available on its Web site at a clearance price of $119.98.

Hedge funds have become the new cultural shorthand for fast money. In the 1980s, corporate raiders and bond traders, as represented by Gordon Gekko and Sherman McCoy, were models for those seeking to be masters of the universe. The 1990s brought the Internet entrepreneur and the day trader, two variations on the Generation X slacker who made millions without leaving his apartment, using only a computer and his savvy.Read the whole thing. “Wall Street Warriors” makes an appearance.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His