-

Dell’s Battery Recall

Posted by Eddy Elfenbein on August 15th, 2006 at 1:48 pm

I just checked Dell’s Web site, and I’m in the clear. My battery isn’t one of the exploding ones.

Here’s more info from Dell on their battery recall. -

Tame PPI Report

Posted by Eddy Elfenbein on August 15th, 2006 at 12:07 pmThe market is relieved today by a tame report on producer prices. The government’s PPI report showed that wholesale inflation rose just 0.1% last month. Economists were expecting a rise of 0.4%. Core wholesale prices fell -0.3%, the first decline since October.

Blomberg surveyed 60 economists, not a single one was expecting a decline in core wholesale prices. The S&P 500 is up slightly over 1%. The NASDAQ 100 is up close to 2%. Bond yields across the board are much lower. The best sector today is tech, and energy is the only sector that’s trading lower. -

The Yield Curve’s Impact on Stock Prices

Posted by Eddy Elfenbein on August 15th, 2006 at 9:49 amThe yield curve has a dramatic impact on equity prices. The steeper the yield curve, the better stocks perform.

I looked at the S&P 500 data along with the yields on the 90-day and 10-year Treasuries. Since 1962, the yield curve has been negative (i.e., the 10-year minus the 90-day) for a total of five years. In that time, the market has lost about 37%.

In fact, the S&P 500 is net flat (not including dividends) for all the periods when the yield curve is less than 78 basis points, which is about one-third of the time. The yield curve hasn’t been that wide since last November.

Interestingly, the market also does poorly when the yield curve is at its steepest. At 286 basis points, the S&P 500 starts falling. Perhaps the market senses that the yield curve is about to turn around.

If you want to geek out on the data, here’s my spreadsheet. I used weekly data, and I compared the S&P’s return to the prior week’s yield curve. -

Exploding Dells

Posted by Eddy Elfenbein on August 15th, 2006 at 9:20 amI recently read Copies in Seconds the brilliant biography of Chester Carlson, the inventor of the Xerox machine. The early machines were, I guess you could say, a tad bit unreliable. Xerox actually sold fire extinguishers along with the copiers for when, not if, the copiers burst into flames.

If there’s any one thing to avoid in a product, it’s spontaneous combustion. Now Dell is recalling 4.1 million laptops because the batteries also burst into flames.The batteries were manufactured by Sony Corp. and used in Latitude, Inspiron, and Dell Precision portable PCs sold between April 2004 and July 18, 2006, Jess Blackburn, a spokesman for Round Rock, Texas-based Dell, said yesterday in an interview.

The action follows Dell’s slowest sales growth in four years after US consumers complained that the company’s discounts are confusing and telephone hold times too long for service.

Dell in May said it will spend $100 million to improve service and product quality to regain market share lost to Hewlett-Packard Co.

“Dell is trying to bolster its image and this is certainly not going to help,” said Brent Bracelin, an analyst at Pacific Crest Securities in Portland, Ore., who rates the shares “sector perform” and doesn’t own them. “Another recall is yet another setback for the company that is struggling to regain share in the market.” -

Sysco Misses By a Penny a Share

Posted by Eddy Elfenbein on August 14th, 2006 at 9:54 amFrom the AP:

Sysco Corp., the largest foodservice distributor in North America, said Monday its fiscal fourth-quarter profit dropped 11 percent, hurt in part by higher fuel costs and pension expenses.

Profit for the quarter ended July 1 fell to $254.1 million, or 41 cents per share, compared with a profit of $284.7 million, or 44 cents per share during the same period last year.

Revenue grew 7 percent to $8.51 billion, from $7.98 billion during the year-ago quarter.

Analysts predicted a profit of 42 cents on revenue of $8.63 billion, according to a Thomson Financial poll.

Fuel costs and pension expenses led to an 8 percent increase in total costs and expenses year over year.

For the full fiscal year, Sysco’s profit fell 11 percent, to $855.3 million, or $1.36 per share, compared to $961.5 million, or $1.47 per share a year ago. Revenue climbed 8 percent to $32.63 billion, from $30.28 billion last year. -

The Hidden Bull

Posted by Eddy Elfenbein on August 11th, 2006 at 9:57 amThis came as a surprise to me but the Morgan Stanley Consumer Index (^CMR) is right at an all-time high. Earlier this year, the index took out its 2000 high, and it’s been slowly crawling higher ever since.

Ironically, today’s report on consumer confidence showed that it dropped to a three-month low. According to the AP, “Economists blamed the deterioration in confidence mostly on galloping energy prices and a cooling in the once-hot housing market.”

That may be true, but it’s not showing up in the shares of consumer stocks. Despite Wall Street’s sour mood, it’s important to remember that the market’s troubles since early-May have largely been confined to cyclical stocks (industrials, materials and technology in particular). Transportation stocks, like Expeditors (EXPD), have been especially ugly lately.

We often talk about the stock market as if it’s one big stock that’s traded every day, but there are thousands of stocks in dozens of industries. Difficult markets don’t affect all stocks the same way.

Health care has been a little unusual. Normally, health care moves with the other consumer stocks, but the sector starting dropping in March. The good news, however, is that health care seem to be making up lost ground.

Bed Bath & Beyond (BBBY) is finally showing some life. I try not to be surprised by what I see the market do, but seeing these shares drop below $32 did catch me off guard.

Next week, we’ll have a few more earnings reports from our Buy List stocks. Sysco (SYY) reports on Monday. Home Depot (HD) on Tuesday, and Dell (DELL) on Thursday. Medtronic (MDT) reports the following Tuesday. -

New Ticker for Harley-Davidson: HOG

Posted by Eddy Elfenbein on August 10th, 2006 at 5:17 pmOn August 15, Harley’s ticker will change from HDI to HOG.

The new symbol reflects the long-time nickname for the heavyweight motorcycles manufactured by the Milwaukee-based company. The current symbol is HDI.

Harley-Davidson holds trademarks to the term HOG. H.O.G. is also the acronym for the Harley Owners Group. Started by the company in 1983, the Harley Owners Group has more than one million members and is the largest factory-sponsored rider organization in the world.In March, I listed my 10 favorite stock symbols:

1. (BUD) Anheuser-Busch

2. (WOOF) VCA Antech (veterinary services)

3. (BOOM) Dynamic Materials

4. (FIZ) National Beverage

5. (LVB) Steinway Musical Instruments (in honor of Ludwig Van Beethoven)

6. (ZEUS) Olympic Steel

7. (CHUX) O’Charley’s Inc.

8. (TAP) Molson Coors Brewing

9. (BID) Sotheby’s Holdings

10. (LENS) Concord Camera -

The Election Cycle Revisited

Posted by Eddy Elfenbein on August 10th, 2006 at 6:03 amA few months ago, I wrote about the stock market’s election cycle. This is one of those bits of market trivia that I usually don’t have much faith in. But I have to admit that the evidence is pretty strong that the market follows a four-year cycle.

The indexes seem to have had several major bottoms during mid-term election years (see here). In April, I crunched the data from Ibbotson and Associates to see what the average cycle looks like, and this is what I got:

You can see that the market runs into a wall in the year after an election, and stays flat through most of the mid-term election year. The theory is that the incumbent president tries to make the economy look great for Election Day, and everything goes to hell shortly afterward. This data was based on the market’s total return (dividends included) from 1926 through 2005.

The data I had was monthly, and I wanted to see if I could narrow it down some. I looked at all the daily closings for the Dow Jones from the start of 1929 through this past Tuesday. That’s roughly 19-1/3 election cycles. This is slightly different because it’s just one index and dividends aren’t included, but I do have the benefit of zeroing in on a specific day.

This is the average Dow election cycle looks like:

You can certainly see a similar pattern here. The market hits its low on September 30 of the mid-term year (not too far away!) and peaks on August 3 of the post-election year. In that 14-month period, the market declines an average of 9.4%. The market is up 46.8% over the other 34 months.

What I really found surprising is that the bullish period is very heavily concentrated within the first 12 months.

From September 30 of the mid-term to September 13 of the pre-election year, the Dow is up an average of 31.6%. To put that in perspective, the Dow averages a gain of 33.1% over the entire four-year period. So every four years, 95% of the market’s capital gains is squeezed into a one-year period (on average).

If you’re curious, the market’s best day during the four-year cycle is September 21 of the election year (+1.15%, thank you 1932) and the worst day is October 19 of the pre-election year (-2.04%, thank you 1987). And most importantly, Leap Day is slightly positive (+0.12%). -

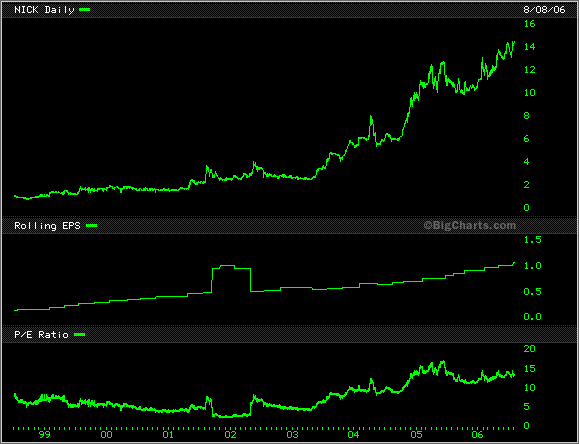

Nicholas Financial

Posted by Eddy Elfenbein on August 9th, 2006 at 11:30 amFor today’s edition of “Widdle Biddy Stocks That Ain’t No One Never Heard Of,” I give you Nicholas Financial (NICK).

Nicholas is a Florida-based company that provides auto loans for used cars, a segment that’s often not served by larger lenders. I’m not joking when I say this is a small company, about 200 employees and a market value of $140 million. Citigroup, by comparison, is over 1,500 times larger.

But dude, check out NICK’s results:

Year…………Sales (mil)………EPS

1997…………..$6.21…………$0.12

1998…………..$7.94…………$0.13

1999…………$10.42…………$0.22

2000…………$14.07…………$0.34

2001…………$17.80…………$0.45

2002…………$20.22…………$0.50

2003…………$22.38…………$0.54

2004…………$25.50…………$0.64

2005…………$32.83…………$0.80

2006…………$42.68…………$1.01

That grabs my attention. NICK has certainly found a niche for itself. The company recently reported first-quarter results (the fiscal year ends in March). Net income grew 29%. The company earned 29 cents a share compared with 23 cents last year. This brings their trailing four-quarter earnings up to $1.07 a share. That means that the company is going for less than 14 times earnings.

There’s not much info on Nicholas, but here’s part of article on the company from 2004:The interest rate Nicholas can charge is dictated by state regulations, and it won’t go into a state where it can’t get a rate of at least 20 percent.

Generally, Nicholas borrowers don’t qualify for traditional sources. The economy has made more people “credit-challenged,” but Finkenbrink says that doesn’t mean they are bad risks.

“We try to finance people who may have had trouble because of a divorce, medical problems or job loss, as opposed to ‘credit criminals,'” he said.

Creating relationships

The company’s branch system is key. Branches require overhead, but they put employees in touch with customers.

“Customers like to come into the office,” Finkenbrink said. “We create relationships, and employees often will counsel customers.”

The result is low delinquency. For the past few years, about 1 percent to 2.5 percent of total loans due at any one time are more than 30 days past due, according to an April 14 research report from Atlanta-based Westminster Securities.

Many larger companies pulled out of the sub-prime auto loan business in the 1990s when they failed to make a lot of money at it, said Will Lyons, Westminster director of equity research.

Currently, GMAC and Ford Motor Credit dominate the industry, and Nicholas has only one-tenth of 1 percent of the market, according to an investors presentation by Nicholas.

“Nicholas takes a personal approach to every loan they do,” Lyons said. “It costs a lot of money to do that, and big companies don’t want to take that kind of approach.”Here’s the chart:

-

The Fed Pauses

Posted by Eddy Elfenbein on August 8th, 2006 at 2:52 pmSeventeen and done…for now. Not a good move in my opinion.

Here’s the statement:The Federal Open Market Committee decided today to keep its target for the federal funds rate at 5-1/4 percent.

Economic growth has moderated from its quite strong pace earlier this year, partly reflecting a gradual cooling of the housing market and the lagged effects of increases in interest rates and energy prices.

Readings on core inflation have been elevated in recent months, and the high levels of resource utilization and of the prices of energy and other commodities have the potential to sustain inflation pressures. However, inflation pressures seem likely to moderate over time, reflecting contained inflation expectations and the cumulative effects of monetary policy actions and other factors restraining aggregate demand.

Nonetheless, the Committee judges that some inflation risks remain. The extent and timing of any additional firming that may be needed to address these risks will depend on the evolution of the outlook for both inflation and economic growth, as implied by incoming information.

Voting for the FOMC monetary policy action were: Ben S. Bernanke, Chairman; Timothy F. Geithner, Vice Chairman; Susan S. Bies; Jack Guynn; Donald L. Kohn; Randall S. Kroszner; Sandra Pianalto; Kevin M. Warsh; and Janet L. Yellen. Voting against was Jeffrey M. Lacker, who preferred an increase of 25 basis points in the federal funds rate target at this meeting.Lacker is the President of the Richmond Fed.

Two other bank presidents, Moskow and Poole, were probably for another rate increase. Since the bank president’s rotate turns, those two won’t be able to vote until next year.

Can you tell when the announcement came?

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His