-

US Economy Added 210,000 Jobs in November

Posted by Eddy Elfenbein on December 3rd, 2021 at 9:03 amThis morning’s jobs report showed that the U.S. economy created just 210,000 net new jobs last month. That’s another big miss. Wall Street had been expecting an increase of 573,000 jobs.

The unemployment rate fell to 4.2%. The unemployment rate is currently lower than it was at any point from March 1970 until February 1999.

A more encompassing measure of unemployment that includes discouraged workers and those holding part-time jobs for economic reasons dropped even more, tumbling to 7.8% from 8.3%. The survey of households painted a more optimistic jobs picture, indicating an employment gain of 594,000 for the month.

Leisure and hospitality, which includes bars, restaurants, hotels and similar businesses, saw a gain of just 23,000 after being a leading job creator for much of the recovery.

Despite the disappointment, markets largely shrugged off the numbers, with stocks pointing to a higher open on Wall Street.

In the last year, wages are up 4.8%. The workforce participation rate rose to 61.85% from 61.65%.

-

Morning News: December 3, 2021

Posted by Eddy Elfenbein on December 3rd, 2021 at 7:02 amWith Its Exit, Didi Sends a Signal: China No Longer Needs Wall Street

France Says UAE Arms Deal Secures Supply Chain, Jobs

Turkish Cenbank Again Stops Lira from Sliding to Record

F.T.C. Sues to Stop Blockbuster Chip Deal Between Nvidia and Arm

The Markets Are Confused, but Wall Street Is Still Making Predictions

Berkshire’s Munger Says Now ‘Even Crazier’ Than Dotcom Bust

A Journalist, a Philosophy Major and the Mad Scramble for Video Game Consoles

Where’s the Paper, Ink, Lightbulbs? U.S. Offices Struggle with Supply Shortages

A Car a Minute Used to Flow Through Here, but Chaos Now Reigns

Elon Musk’s Tesla Share Sales Pass the $10 Billion Mark

The Hot New Trend For Hedge Funds Is—Finally—Female Founders

China Star Trader’s New Fund Attracts $16 Billion in One Day

CEO of Firm Behind Kay Jewelers and Zales Says Anticipating Early Holiday Shoppers Paid Off

California Scheming – Getting Rich Off the Affordability Crisis

Bloomberg 50: The People and Ideas That Defined Global Business in 2021

Be sure to follow me on Twitter.

-

Morning News: December 2, 2021

Posted by Eddy Elfenbein on December 2nd, 2021 at 7:07 amBritain Turns to Bankers to Blaze a Green Trail

Omicron Could Knock a Fragile Economic Recovery Off Track

Investors Flee U.S. Corporate Junk Debt on Inflation, Omicron Concerns

OPEC Faces Omicron Uncertainty and Rebellious Customers

A Top Official Says the Fed Will ‘Grapple’ With a Faster Bond-Buying Taper

White House Delay on Fed Regulation Chief Bodes Badly for Bank M&A

Debt Collectors Can Now Text, Email and DM You on Social Media

Apple Tells Suppliers iPhone Demand Has Slowed as Holidays Near

Twitter and Facebook Hit Back at Chinese Propaganda Campaigns

Square, Jack Dorsey’s Payments Company, Changes Its Name to Block

Disney Names Susan Arnold as Board Chair, Replacing Bob Iger

Toys R Us Is Opening a New Store With a 2-Story Slide and an Ice Cream Parlor

Goldman’s Leaders Push New, Creative Ways to Juice Their Own Pay

U.S. Seeks Break for Swiss Trader Who Made $70 Million Illegally

Be sure to follow me on Twitter.

-

The S&P 500 Closed Below Its 50-DMA

Posted by Eddy Elfenbein on December 1st, 2021 at 10:16 pmThe S&P 500 lost its early rally today and for the first time since October 13, the index closed below its 50-day moving average.

-

December Is Off to a Good Start

Posted by Eddy Elfenbein on December 1st, 2021 at 11:42 amThe stock market is getting a nice rebound this morning. Yesterday the S&P 500 closed at its lowest level in over a month. As I write this, the S&P 500 is up 1.78%. Energy and Financials are doing particularly well.

Historically, December is one of the best months of the year for stocks. November has been even better. Since 1928, December has been an up month for stocks 74% of the time. That’s the highest of all months. The S&P 500 gained 0.83% in November.

We got the ADP private payrolls report this morning. It showed an increase of 534,000 private jobs. Wall Street had been expecting an increase of 525,000.

Still, the big report is the government’s jobs report which is due out on Friday. Historically, the ADP report has not been a good predictor of the government’s report.

Also this morning, the ISM Manufacturing report came in at 61.1. That’s an increase of 0.3% over October. That’s a good number and it indicates that the factory sector is still expanding.

The construction spending report showed an increase of 0.2%. In the last year, construction spending is up 8.6%.

-

Morning News: December 1, 2021

Posted by Eddy Elfenbein on December 1st, 2021 at 7:06 amOECD Says Inflation Is Main Risk to Economic Outlook

Factories Facing Supply Headaches as Omicron Risks Emerge

Retailer CEOs and Biden Appear to Be Split on the Supply-Chain Crisis

History Says Expect Strong December for U.S. Stocks, Despite Omicron and Fed Worries

Hawkish Powell Is a Force Markets Haven’t Faced in Three Years

Credit-Card Applications Hit Pandemic High

Dorsey’s Twitter Departure Hints at Tech Moguls’ Restlessness

Exxon to Continue Leaner Spending as Covid-19 Threat Lingers

IEA Says Renewable Power Installations Are Set for A Record Year, Warns of Net-Zero Uncertainty

The Long and Winding Road for Green Startups

Elon Musk Warns SpaceX Faces ‘Genuine Risk of Bankruptcy’

Bloomberg 50: The People and Ideas That Defined Global Business in 2021

These Are the World’s Most Expensive Cities to Live in Right Now

FDA Advisors Vote Narrowly in Favor of Merck Covid Pill

Sackler Family May Have ‘Abused’ Bankruptcy Process, Purdue Pharma Judge Says

Be sure to follow me on Twitter.

-

CWS Market Review – November 30, 2021

Posted by Eddy Elfenbein on November 30th, 2021 at 7:46 pm(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Omicron Rattles Wall Street

I find it interesting that on Wall Street, a market drop of more than 10% is called a “correction.” But if you take a long-term perspective, then, properly speaking, every market drop has truly been the error while the rally has been the correction.

It’s odd to think that way, but it’s true. The S&P 500 last hit an all-time high less than two weeks ago. Thanks to fears of the Omicron strain, the stock market got shaken up on Friday. It was the worst day for the S&P 500 in nine months, and for the Dow, it was the worst day in more than a year.

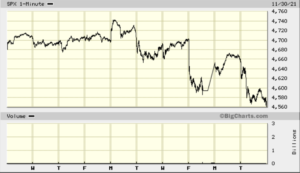

It was also a calm market. Before last Friday, the S&P 500 had gone 29 days in a row without closing up or down by more than 1%. In fact, that understates how relaxed the market had been. Of those 29 days, 22 had market daily moves that were less than 0.5%. Now we’ve had three 1% days in a row.

Here’s the minute-by-minute chart for the last two weeks:

As a general rule, volatility tends to feed on itself in the markets. In other words, high volatility often produces higher volatility, while low volatility produces even lower volatility. Consider that this year, the stock market has fallen more than 1% 17 times. In eight of those times, it rebounded by more than 1% the next day.

Today, the S&P 500 lost 1.90% and the index closed at its lowest level in over a month. All 11 sectors were down. For November, the index lost 0.83%. This was the second monthly loss in the last three months. Prior to that, the S&P 500 had rattled off seven straight monthly gains.

The stock market’s drop on Friday was very reminiscent of the kinds of days we saw in March 2020. The worst-performing stocks were travel and leisure companies while many of the top performers were defensive stocks. For example, Clorox had a very good day.

The trouble with the Omicron strain is that we don’t have a lot of information yet. Whenever this happens, Wall Street is more than happy to fill in the gap with fear. On Monday, the market made back some of those gains as we heard that Omicron may not be that bad, but on Tuesday, Wall Street reverted to fear.

My guess is that we’re going to witness Wall Street wrestle with the “lockdown trade.” That means that on most days, cruise stocks will be either the best- or worst-performing stocks, and there won’t be much left over in the middle. Today was a good day for the cruise stocks. Apple and Tesla also did well. In other words, investors are willing to take on more risk. Only seven stocks in the entire S&P 500 closed higher today.

By the way, our Buy List as whole skews towards being a classic defensive portfolio. That’s not a macro prediction on my part. It’s simply how our stock-picking worked out. In plain English, when folks get scared, they flee toward our stocks.

A good example is Hershey (HSY), a Buy List favorite. Shares of Hershey fell about 1.69% on Friday. That’s bad, but it was better than the overall market’s drop of 2.27%. Today, the S&P 500 fell 1.9% while shares of Hershey only fell 0.93%. Whatever Omicron may do or not do, I doubt it will impact chocolate sales.

By the way, investors shouldn’t overlook “downside Alpha.” That’s a fancy word for not falling as much as everyone else. I’ve found that most of the long-term outperformance comes during rough markets. Everyone can look brilliant in a rally but emerging from a harsh bear market mostly unscathed is an impressive feat.

Powell Said It’s Time to Retire “Transitory”

Besides Omicron, probably the main reason for today’s selloff was hawkish comments from Federal Reserve Chairman Jay Powell. At a Senate hearing, Powell said that it may be appropriate to speed up the tapering of bond purchases and that inflation will “linger well into next year.”

No, duh.

Jay, look around. Just recently, General Mills said that it will increase prices next year. That means you’ll be paying more for Cheerios or Lucky Charms. Even Dollar Tree is raising prices to $1.25.

Here’s a look at gasoline prices over the last 18 months:

Until now, the Fed has often described inflation as being “transitory.” Today, Powell conceded that it’s “probably a good time to retire” that word. Still, he’s pinning most of the blame on supply/demand imbalances.

The Fed’s original plan was to pare back bond purchases until they reached zero by June. After that, the Fed would start to hike interest rates.

Now that timeline is uncertain. According to the futures market, traders are placing a 45% chance of the Fed hiking by early May. That’s up 10% from yesterday. Traders narrowly see a second hike coming by September.

The bond market is reacting as well. I like to look at the spread between the 10- and 2-year Treasury yields. The spread got down to just 91 basis points today. That’s the narrowest since January. In March, the spread was 159 basis points.

For being such a simple metric, the 2/10 Spread has an eerily good track record. Whenever it turns negative, you know bad times aren’t far behind. The last time the 2/10 turned negative was in August 2019, only a few months before Covid rocked the world.

Jack Quits Twitter

On Monday, Jack Dorsey announced that he’s stepping down as Twitter’s CEO. The stock responded by vaulting 11% higher. That’s got to sting when news of your departure causes investors to celebrate. At its peak, Jack’s leaving added $4 billion to Twitter’s market value. Ouch!

Parag Agrawal will take over as CEO. He’ll be the youngest CEO in the S&P 500. At 91, Warren Buffett is the oldest. Agrawal is a little younger than Mark Zuckerberg. The Bloomberg story contained this curious sentence, “Citing security concerns, Twitter wouldn’t disclose Agrawal’s date of birth, but confirmed he was born later in 1984 than Zuckerberg’s May 14 birthday.”

Despite Wall Street celebrating Jack Dorsey’s departure, shares of Twitter closed lower yesterday and they were down 4% today. This brings up a good point that often isn’t discussed, namely that Twitter isn’t that profitable as a business enterprise.

You’ll have to excuse me for relying on antiquated notions, such as return-on-equity, a balance sheet, or “profits,” but Twitter really doesn’t look that good.

Jack Dorsey is also the CEO of Square. I’ve found that shareholders are willing to overlook a lot, as long as the stock is going up. Just look at Elon Musk. Yes, he says silly things, but the stock has done well over the years. That’s not the case with Twitter, so that added additional pressure on Dorsey to choose one of his companies to lead.

Twitter went public seven years ago and the shares are now below where they were after the first day of trading. The IPO was priced at $26 per share. On the first day of trading, it zoomed over $50 and eventually closed at $44.90. Today, Twitter closed 96 cents below that. In seven years, Twitter has basically gone nowhere.

At the end of this year, Twitter will have brought in about $5 billion in revenue. Their gross profit will be around $3 billion while the operating profit will probably be about $300 million, give or take. That’s probably around 35 to 40 cents per share, and we still haven’t gotten down to taxes and other non-operating expenses.

Are investors willing to pay at least 100 times earnings for a company that seems to have little direction? Clearly, Agrawal has his work cut out for him.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– EddyP.S. Don’t forget to sign up for our premium newsletter.

-

Morning News: November 30, 2021

Posted by Eddy Elfenbein on November 30th, 2021 at 7:03 amEurozone Inflation Hits a Record High of 4.9%

China’s Manufacturing Rebounds With Signs Inflation Easing

Tiger Global Helps Make Credit-Card Startup Newest India Unicorn

Powell, Yellen Head to Congress as Inflation, Variant Risks Rise

FTC Asks Amazon, Walmart for Information About Supply-Chain Issues

Supply Chain Problems Have Small Retailers Gambling on Hoarding

Covid-19 Antibody Drugs Are Challenged by Omicron, Preliminary Testing Indicates

Moderna’s Concerns About Omicron Outlook Spark Market Slump

America’s Power Plants Are Low on Coal

Gas Prices Pressure Drivers’ Finances

In China, Tesla Is a Catfish, and Turns Auto Companies Into Sharks

Auto Executives Expect EVs Will Own Half of U.S., China Markets by 2030

A Secretive Robot Is Helping Investment Firm Stripes Pick Winning Bets

China’s Biggest Crypto Exchange Picks Singapore as Asia Base

How Crypto Vigilantes Are Hunting Scams in a $100 Billion Market

Twitter’s Agrawal Is Youngest CEO in S&P 500, Nudging Out Zuckerberg

Be sure to follow me on Twitter.

-

Stocks Rebound After Friday’s Drop

Posted by Eddy Elfenbein on November 29th, 2021 at 10:31 amThe stock market is making back some ground it lost after Friday’s big drop. The S&P 500 is currently up about 1% while the Dow is up just 0.34%. Many of the high-flying high-beta stocks are leading the charge. The Nasdaq Composite is up about 1.5%.

Shares of Twitter have been up as much as 11% this morning on news that Jack Dorsey will be stepping down as CEO.

It’s unclear who’s set to succeed Dorsey or the timing of a potential announcement. It’s also unknown why Dorsey would take a step back. But if he steps down, the next CEO will have to meet Twitter’s aggressive internal goals. The company said earlier this year it aims to have 315 million monetizable daily active users by the end of 2023 and to at least double its annual revenue in that year.

That has to be rough when your company adds $4 billion in market value on the news that you’re leaving.

This morning’s report on pending home sales rose by 7.5% in October. That comes after a drop in September. This can often be a leading indicator of the housing market. Wall Street had been expecting an increase of just 0.8%. It looks like this year will be the best for existing-home sales in 15 years.

This Friday is Jobs Day. Wall Street expects that the economy added 581,000 new jobs last month and that the jobless rate fell to 4.5%.

-

Morning News: November 29, 2021

Posted by Eddy Elfenbein on November 29th, 2021 at 7:05 amEconomists Game Out How Omicron Will Hurt the Global Recovery

Markets Aren’t That Spooked by Omicron

As U.K. Beckons Truck Drivers, Many in Poland Say ‘No Thanks’

Swiss Franc Rises to Six-Year High as Central Bank Stands Back

El-Erian Says Fed Should Recognize Inflation Isn’t Transitory

Cyber Monday Sales Expected to Slow as Shoppers See Fewer Deals

Rental Assistance to Be Redirected Based on Demand

Is India Banning Cryptocurrency? How Can It Do That?

Binance Reopens Dogecoin Withdrawals After Musk Spat With CEO

Crypto Firms Pay Massive Price Tags to Name Arenas as Sports Teams Weigh Risks

Apple’s Car and VR Headset Are Poised to Alter the Typical Product Rollout Strategy

Hunt for the ‘Blood Diamond of Batteries’ Impedes Green Energy Push

Nissan Unveils $18 Billion Electrification Push in Bid to Draw Level with Rivals

Uber Survived the Spying Scandal. Their Careers Didn’t

Disney’s Missing ‘Simpsons’ Episode in Hong Kong Raises Censorship Fears

‘Pension Poachers’ Are Targeting America’s Elderly Veterans

Be sure to follow me on Twitter.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His