-

The S&P 500 Drops More than 1%

Posted by Eddy Elfenbein on July 8th, 2021 at 12:07 pmEven though the stock market had its seven-day win streak snapped on Tuesday, the S&P 500 rallied to yet another new high yesterday. Today, however, is the first time in a long time that stocks are down sharply. This morning’s jobless claims report rose to 373,000. The S&P 500 is currently off by about 1%. At its low earlier today, the index was down by 1.6%.

As you might guess, it’s the cyclicals that are down the most. Specifically, the financials and the materials are lagging. The defensive sectors are down but not as much. When in doubt, just look at shares of Hershey (HSY). You can’t get much more defensive than chocolate. HSY is currently down 0.04%.

-

Morning News: July 8, 2021

Posted by Eddy Elfenbein on July 8th, 2021 at 7:05 amQuest to Define Post-Crisis Global Economic Order Gathers Pace

China’s Dovish Switch Ignites Fears Over Global Recovery Trade

A $9 Trillion Binge Turns Central Banks Into the Market’s Biggest Whales

European Central Bank Sets Its Inflation Target at 2% in New Policy Review

Ireland Fights For Its Tax Breaks

Post-Fed Taper Tantrum? Not This Time, Market Strategists Say

Falling U.S. Bond Yields May Signal Death Knell for ‘Reflation’ Stock Trade

U.S. Banks to See Big Jump in 2Q Profits Before Results Return to Normal

Cryptocurrency Seeks the Spotlight, With Spike Lee’s Help

Crypto Scammers Rip Off Billions as Pump-and-Dump Schemes Go Digital

Didi’s Regulatory Troubles Might Just Be Getting Started

Crackdown on Chinese Tech Giants is ‘Backfiring’ on Beijing

Dozens of States Sue Google Over App Store Fees

Volkswagen, BMW Fined $1 Billion by EU for Pollution Cartel

The Parking Garage of the Future

No, Billionaires Won’t “Escape” to Space While the World Burns

Be sure to follow me on Twitter.

-

The Fed’s Economic Outlook

Posted by Eddy Elfenbein on July 7th, 2021 at 2:25 pmThe federal Reserve just released the minutes from its last meeting. Here’s a look at their economic outlook.

The U.S. economic projection prepared by the staff for the June FOMC meeting was stronger than the April forecast. Real GDP growth was projected to increase substantially this year, with a correspondingly rapid decline in the unemployment rate. Further reductions in social distancing and favorable financial conditions were expected to support output growth, even though the effects of fiscal stimulus on economic growth were starting to unwind. With the boost to growth from continued reductions in social distancing assumed to fade after 2021 and the further unwinding of fiscal stimulus, GDP growth was expected to step down in 2022 and 2023. Nevertheless, with monetary policy assumed to remain highly accommodative, the staff continued to anticipate that real GDP growth would outpace that of potential over most of this period, leading to a decline in the unemployment rate to historically low levels.

The staff’s near-term outlook for inflation was revised up markedly, but the staff continued to expect the rise in inflation this year to be transitory. The 12 month change in total and core PCE prices had moved well above 2 percent in April, and incoming CPI data suggested that PCE price inflation would remain high in May. The recent 12-month measures of inflation were being boosted significantly by the base effects of the drop in prices from the spring of 2020 rolling out of the calculation. In addition, the surge in demand as the economy reopened further, combined with production bottlenecks and supply constraints, contributed to the large recent monthly price increases. The staff expected the 12-month change in PCE prices to gradually move down in coming months, reflecting, importantly, the fading of base effects along with smaller expected monthly price increases, but PCE price inflation was forecast to still be well above 2 percent at the end of this year. Over the next year, the transitory price increases caused by bottlenecks and supply constraints were expected to largely reverse, and the growth in demand was forecast to ease. As a result, inflation was projected to slow to slightly below 2 percent in 2022 before moving back up to a bit above 2 percent in 2023, supported by high levels of resource utilization.

The staff continued to see the uncertainty surrounding the economic outlook as elevated, although increasingly widespread vaccinations, along with ongoing policy support, were viewed as helping to diminish some of these uncertainties. Nevertheless, the staff judged that the risks around their strong baseline projection for economic activity were still tilted somewhat to the downside, as adverse alternative courses of the pandemic—including the possibility of the spread of more-contagious, more-vaccine-resistant COVID-19 variants—seemed more likely than outcomes that would be more favorable than in the baseline forecast. The staff continued to view the risks around the inflation projection as roughly balanced. On the upside, bottlenecks, supply disruptions, and historically high rates of resource utilization were seen as potential sources of greater-than-expected inflationary pressures, particularly if there were a significant rise in inflation expectations that altered inflation dynamics. On the downside, if the effects of supply constraints proved to be transitory, as expected, then the inflation record from the past 25 years suggested the possibility that low underlying trend inflation and a flat Phillips curve could cause inflation to revert to relatively low levels despite a strengthening economy.

-

9.2 Million Unfilled Jobs

Posted by Eddy Elfenbein on July 7th, 2021 at 11:16 amYesterday, the S&P 500 snapped its seven-day winning streak. The market is mostly flat so far this morning.

Later today, the Fed will release the minutes from its last meeting. There was a disconnect at the meeting. The economic forecasts from the Fed officials were much more hawkish than the comments by the Fed. Hopefully, the minutes will clarify the issue.

This morning’s job openings report was little changed at 9.2 million. That’s the number for May. (Technically, it rose a little bit to a new all-time high.)

Middleby looks to lose its battle to buy Welbilt (which is fine by me). Italy’s Ali Group raised its offer to buy Welbilt to $24 per share. Welbilt looks to go ahead with Ali Group. This will earn MIDD a new break-up fee.

Middleby stayed in the news by releasing updates for guidance for this quarter and full year. The company was sure to mention that this guidance is above current estimates.

For Q2, MIDD sees revenue of $808 million and adjusted EBITDA of $186 million. Wall Street had been expecting $794 million and $174 million respectively.

For all of 2021, MIDD now sees revenue of $3.244 billion and adjusted EBITDA of $730 million. That’s above consensus of $3.167 billion and $704 million.

-

Morning News: July 7, 2021

Posted by Eddy Elfenbein on July 7th, 2021 at 7:05 amOil Rises as OPEC+ Clash Over Supply Boost Keeps Prices Volatile

Saudi Arabia and the UAE Can’t Afford Not to Be Friends Despite Their OPEC Tiff

European Commission Sees the Economy Recovering Faster Than Expected.

China Considers Closing Loophole Used by Tech Giants for U.S. IPOs

Didi Removed from China’s WeChat and Alipay Apps for New Users in Another Big Blow

IMF Chief Sees Risk of Sustained Rise in U.S. Inflation

A Planned Biden Order Aims to Tilt the Job Market Toward Workers

Yellen’s Next Test: Persuading G20 That U.S. Congress Will Not Block Tax Deal

Running for Safety When Market Corrections Occur Cn Be Costly

Amazon Notches Comeback Win in Years-Long Pentagon Cloud Battle

Revolt Against Bank Fees Mints a $3 Billion Fortune for Fintech Founders

Russia ‘Cozy Bear’ Breached GOP as Ransomware Attack Hit

Discovery’s David Zaslav Promises More Media Merger Mania at Sun Valley

Violence, Drugs And Fast Food: How Americans’ Risky Behavior Surged While Under A Covid Lockdown

Ever Given Container Ship Begins Exit from Suez Canal 106 Days After Getting Stuck

Be sure to follow me on Twitter.

-

Morning News: July 6, 2021

Posted by Eddy Elfenbein on July 6th, 2021 at 7:07 amOPEC+ Crisis Propels Oil to Six-Year High

Global Corporate Tax Overhaul Faces Rocky Road to Completion

Empathy Bootcamp? UK Banks Seek Payback on $105 Billion COVID Loans

When Will China Overtake the U.S. as the World’s Top Economy? Maybe Never

Quickening U.S. Recovery Puts Fed Taper Discussion in Focus

The Next Big Divide in Finance Takes Shape in Your Office

American Internet Giants Hit Back at Hong Kong Doxxing Law

China’s Crackdown on Didi Is a Reminder That Beijing Is in Charge

Big Ransomware Hack Highlights a Robust Software Business Model

No Soil. No Growing Seasons. Just Add Water and Technology.

Here’s What You Should Know About That Eye-Popping Sign-On Bonus

Airbnb’s Pandemic Party-Blocking Spree Rages On

SoftBank Pays $1.6 Billion for Yahoo Japan Rights

Amazon Transformed Seattle. Now, Its Workers Are Poised to Take It Back.

Be sure to follow me on Twitter.

-

Italy’s Ali Group Raises Offer for Welbilt to $3.41 Billion, Trumping Middleby Bid

Posted by Eddy Elfenbein on July 5th, 2021 at 11:45 pmFrom Reuters:

Italy’s Ali Group on Monday said it raised its offer to buy Welbilt Inc, valuing the U.S. food service equipment maker at $3.41 billion.

The deal trumps a $2.9 billion all-stock offer for Welbilt put forward by competitor Middleby in April to beef up its commercial foodservice platform.

Welbilt will receive $24 for each share, representing a premium of 3.53% to the closing price on Friday.

The offer is a raised bid from its previous $23 per share offer in May.

Ali Group said that it has obtained fully underwritten, binding commitment letters for debt financing from Goldman Sachs International and Mediobanca.

Based near Milan, Ali Group, with 80 brands, operates worldwide and supplies foodservice equipment to businesses ranging from hotels to schools and supermarkets.

-

Morning News: July 5, 2021

Posted by Eddy Elfenbein on July 5th, 2021 at 7:09 amOPEC+ Crisis Deepens as Saudi Arabia Refuses to Budge

Credit Suisse Strategist Sees $1 Trillion Problem for Money Markets

Why Is China Cracking Down on Didi After U.S. IPO?

Chinese Antitrust Regulator to Block Tencent’s Videogaming Merger

The Tech Cold War’s ‘Most Complicated Machine’ That’s Out of China’s Reach

Britain Proposes Tech Company Listing Reforms to Catch Up with New York

Stocks Are Expensive but that Doesn’t Mean the Bull Run is Ending

Pandemic Wave of Automation May Be Bad News for Workers

Investigating Amazon, the Employer

‘Absolutely a Sprint’: How Andy Jassy Raced to the Top of Amazon

After Pressuring Telecom Firms, Myanmar’s Junta Bans Executives from Leaving

The Charges Against the Trump Organization Are a Master Class in Tax Evasion

The US is a First-World Nation With a Third-World Rail System

Sun Valley’s Billionaire ‘Summer Camp’ Is Back After A Virus-Induced Break

Be sure to follow me on Twitter.

-

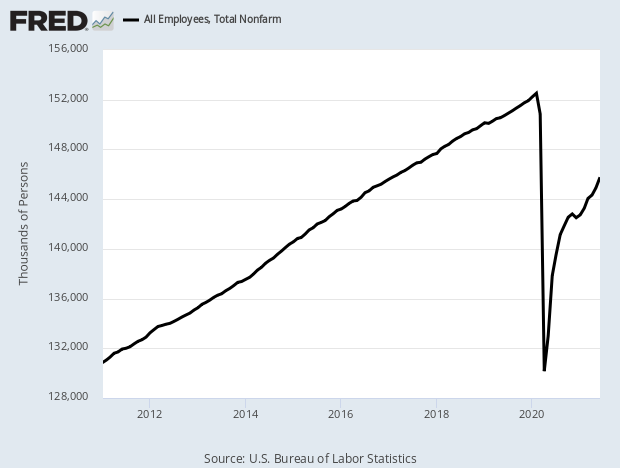

June Jobs Report

Posted by Eddy Elfenbein on July 2nd, 2021 at 8:33 amThe jobs report is out. Last month, the U.S. economy created 850,000 new jobs. The consensus was for 706,000.

The private sector added 762,000 jobs. The unemployment ticked up to 5.9%.

Average hourly earnings rose 0.3%. In the last year, average hourly earnings are up 3.6%.

Underemployment is 9.8% and the labor force participation rate was 61.6%. The latter figure has barely budged.

Hospitality continued to be the prime beneficiary of the reopening as workers returned to jobs at bars, restaurants, hotels and the like.

The industry notched a gain of 340,000 amid easing restrictions across the country. That total included 194,000 in bars and restaurants, but still left the sector 2.2 million shy of where it was in February 2020 before the pandemic began.

Other notable gains came in education, which totaled 269,000 across state, local and private hiring, while professional and business services increased by 72,000 and retail added 67,000.

The other services industry added 56,000 jobs, including a gain of 29,000 in personal and laundry services, a subsector that has been seen as a proxy for the resumption of normal business activity. Social assistance added 32,000, while wholesale trade contributed 21,000 to the total and mining grew by 10,000.

Manufacturing edged up 15,000 for the month, though construction lost 7,000 positions despite a sizzling housing industry where new building has been held back by supply shortages and what had been soaring lumber prices before the recent plunge.

Here’s the updated chart of nonfarm payrolls.

We’ve created a lot of jobs but we still have a long way to go.

-

Morning News: July 2, 2021

Posted by Eddy Elfenbein on July 2nd, 2021 at 7:01 amOil Holds Near $75 as Brinkmanship at OPEC+ Threatens Deal

U.S. Proposal for 15% Global Minimum Tax Wins Support From 130 Countries

Budget Deficit Projected to Hit $3 Trillion as Pandemic Spending Buoys Economy

Halfway Through 2021, the Hot Stocks Are Old-Fashioned

World’s Top Pension Fund Books ‘Historic’ $339 Billion Gain

China and Hong Kong Stocks Tumble After ‘Broken Heads and Bloodshed’ Speech from Xi

U.S. Toymaker Doubles Down in China Despite Rising Costs, Political Tensions

Didi Opens Door for More Tech IPOs Beyond China. Where Emerging Market Investors Should Look.

Dogecoin Whale? Robinhood IPO Filing Reveals Dogecoin as One of its Biggest Risk Factors

Rumors of the Demise of Cars Have Been Greatly Exaggerated

‘Shocked’ Mitsubishi Electric CEO to Quit Over Data Deceit

New Saudi Airline Plan Takes Aim at Emirates, Qatar Airways

The FTC Just Took a Step That Could Make It Easier to Go After Amazon

Amazon Revises Corporate Values Days Before Bezos Steps Down

Bezos’ Exit Is One of Many Among Amazon’s Top Ranks

Jeff Bezos Is Headed To Space. Richard Branson Decided To Beat Him There

Be sure to follow me on Twitter.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His