-

Trex and Our Track Record

Posted by Eddy Elfenbein on September 15th, 2020 at 8:18 amFor track record purposes, I assume our Buy List is a $1 million portfolio that’s equally weighted at the start of each year.

For 2020, we had 445.03783 shares of Trex (TREX) at $89.88 per share.

Due to the 2-for-1 split, that now becomes 890.07566 shares at $44.94.

The Buy Below is now $75 per share.

-

Morning News: September 15, 2020

Posted by Eddy Elfenbein on September 15th, 2020 at 7:07 amBig Investors Are Dying to Know What Amateur Traders Are Doing

The Fed and the Future of America’s Debt

U.S. Restricts Chinese Apparel and Tech Products, Citing Forced Labor

TikTok’s Proposed Deal Seeks to Mollify U.S. and China

How ByteDance’s CEO Balked At Selling TikTok’s U.S. Business

Banks Balk at Fed’s $600 Billion Lifeline for Main Street Firms

Pandemic-Proof Apple To Kick Off Lineup For Critical Holiday Season

Verizon to Buy Prepaid Wireless Provider Tracfone for $6.25 Billion

For Ray Dalio, a Year of Losses, Withdrawals and Uneasy Staff

Daimler to Pay $1.5 Billion to Settle Emissions Cheating Probes

With Nissan’s Carlos Ghosn Gone, Greg Kelly Faces Trial Alone

Ben Carlson: 4 Questions I’m Pondering At the Moment

Howard Lindzon: The FinTAM Explosion

Be sure to follow me on Twitter.

-

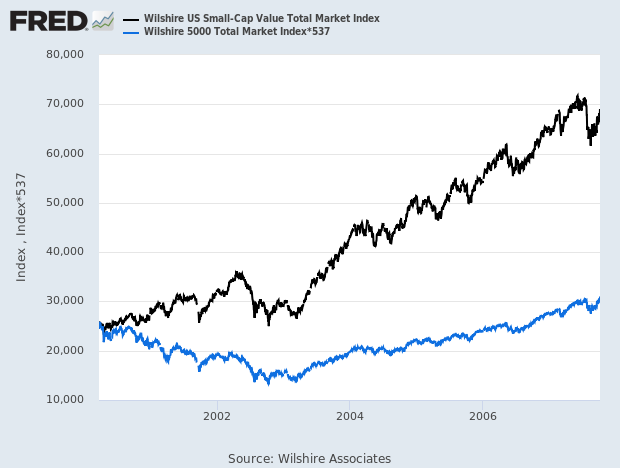

20 Years Ago, Small-Cap Value Bucked the Bear

Posted by Eddy Elfenbein on September 14th, 2020 at 11:45 amHere’s an interesting chart. The blue line is the broad market and the black line is small-cap value.

March 2000 was the start of a terrible bear market as the tech bubble popped, but small-cap value almost completely ignored the selling. Of course, value stocks had a rough time before that.

Looking for a single index to represent the entire market ignores many important trends happening beneath the surface.

-

Investment Talk By Peter Lynch

Posted by Eddy Elfenbein on September 14th, 2020 at 10:00 amIf you have the time, here’s a good talk about investing by Peter Lynch.

-

Reminder: Trex to Split 2-for-1

Posted by Eddy Elfenbein on September 14th, 2020 at 9:31 amShares of Trex (TREX) will split 2-for-1 today. That means shareholders will get twice as many shares and the share price will fall in half. Our Buy Below price will drop to $75 per share.

The split goes into effect after today’s closing bell and you’ll see the impact in tomorrow’s trading.

-

Morning News: September 14, 2020

Posted by Eddy Elfenbein on September 14th, 2020 at 7:00 amOracle Chosen as TikTok’s Tech Partner, as Microsoft’s Bid Is Rejected & The Woman Taking Over TikTok at the Toughest Time

Nvidia to Buy Chip Designer Arm for $40 Billion as SoftBank Exits

Immunomedics Shares Double After Gilead Agrees to Buy the Cancer Drugmaker in $21 Billion Deal

Amazon Hiring 100,000 New Employees in U.S. and Canada

AstraZeneca Shows the Risk of Investing in Coronavirus Vaccine Stocks

Feds Can’t Scapegoat Google and Big Tech As Anti-Trust Targets Forever

Condo Butler Service Demand in China Sparks 400% Stock Gain

How GE Has Become a Shadow Of Its Formerly Great Self

Exxon Used to Be America’s Most Valuable Company. What Happened?

BP Says the Era of Oil-Demand Growth Is Over

How to Stop CEOs From Laying Off Workers While Earning Fortunes

Greed Is Good. Except When It’s Bad.

Michael Batnick: What’s Driving Inflation?

Ben Carlson: The Work From Home Backlash is Upon Us & Investing Experts on an Earlier Version of the World

Joshua Brown: The Whole Story, Why Markets Crash in the Fall, A Tale of Two Semis

Be sure to follow me on Twitter.

-

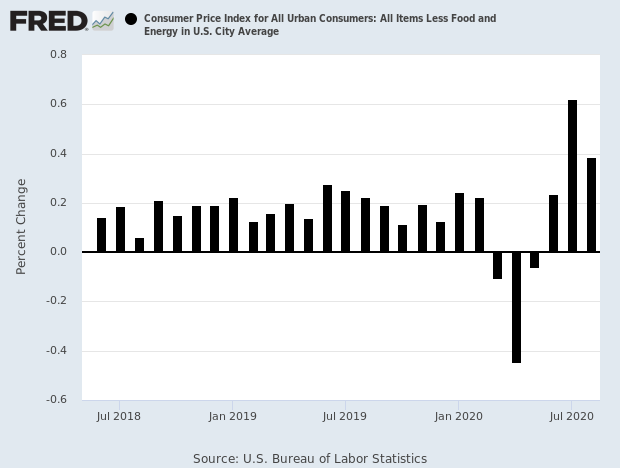

Inflation Runs Hot in August

Posted by Eddy Elfenbein on September 11th, 2020 at 10:40 amThis morning’s inflation report was surprisingly strong. For August, the CPI rose by 0.4% (or 0.37% to be more precise). That beat Wall Street’s forecast for a rise of 0.3%. Some of this could be a bounce back effect from the lockdowns earlier this year. We had deflation in March, April and May.

Nearly 30 million people are on unemployment benefits. The Fed’s preferred inflation measure, the core personal consumption expenditures (PCE) price index, rose 1.3% in the 12 months through July. August’s core PCE price index data is scheduled to be released at the end of this month.

Gasoline prices rose 2.0% in August after increasing 5.6% in July. Food prices edged up 0.1% after declining 0.4% in July, the first decrease since April 2019. The cost of food consumed at home fell 0.1% after dropping 1.1% in the prior month.

One interesting detail from the report: the cost of used cars and trucks rose by the most in 51 years.

The core rate of inflation also rose by 0.4% (or 0.385%).

Over the last three months, inflation has been running at more than 6.2% annualized while core inflation has been at 5.1%.

Here’s a look at monthly core inflation:

-

CWS Market Review – September 11, 2020

Posted by Eddy Elfenbein on September 11th, 2020 at 7:08 am“It is not the crook in modern business that we fear, but the honest man who doesn’t know what he is doing.” – Owen D. Young

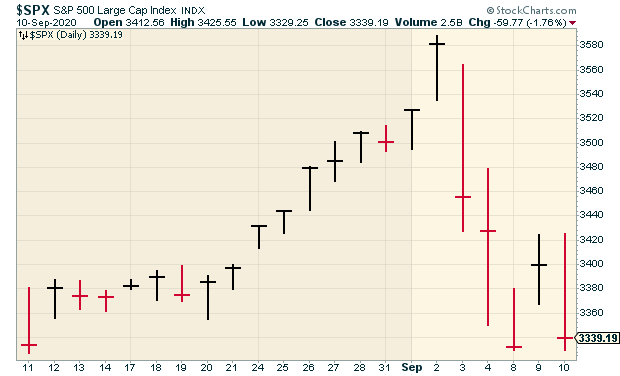

Summer is slowly retreating, and there’s a new mood on Wall Street. After a very bullish summer and the best August in 36 years, the S&P 500 has lost ground over four of the last five days. Could this be the start of a downward trend?

That’s hard to say, but the calendar is definitely not on the bulls’ side. September, I’m afraid to say, has historically been a terrible month for stocks. In fact, it’s been the single worst month for stocks over the last 20 years. Not only that, but it’s also been the worst over the last 50 and 100 years.

I crunched the numbers for the entire 124-year history of the Dow and found that the worst stretch of the year has come between September 6 and September 30. Over that time, the Dow has lost an average of 2%. That may not sound like a lot, but for a 124-year average, it’s pretty big.

Of course, none of this means that this September will be a bad one. While the market has been soggy lately, it’s been the hi-flying tech names that have felt the most pain. For example, shares of Telsa got hammered because—are you ready for this—it wasn’t selected for addition to the S&P 500. Within one week, the shares dropped by one-third. (Don’t cry for Elon. Tesla’s still up 337% this year.)

In this week’s issue, I want to take a closer look at some of the key underlying trends in the market and how they affect our Buy List. For the first time in a long time, value stocks are popular and growth stocks are not. I’ll explain what it all means. I’ll also cover some recent economic news. Plus, I have a few Buy List updates for you. But first, is the market finally ready to rotate towards value?

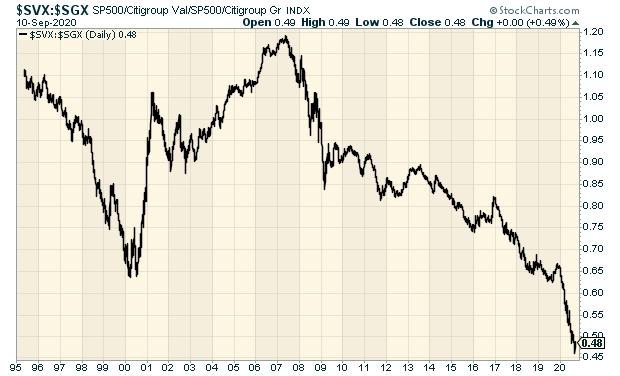

Value Gets Its Day In The Sun, But Will It Last?

In recent issues, I’ve talked about the how the market has soared and a small group of stocks has enjoyed the lion’s share of the gains. Lately, however, the bears have pushed back, and it’s been the former darlings of Wall Street that have gotten knocked down. Amazon, Google, Facebook and the others have all gotten dinged hard this month.

For the first time in a long time, value stocks are popular. I have to explain that growth stocks have been beating value stocks consistently for more than 13 years. Not only that, but the rate of the divergence has sped up noticeably this year.

Let me quickly explain what I mean by these terms and why the growth-value cycle is so important. A value investor is someone who looks for a large gap between the actual share price and the true underlying value. Of course, calculating the correct value is the hard part. The value investor then hopes the gap closes.

By contrast, the growth investor isn’t so concerned with price. She sees a stock’s value not in its share price but in its ability for future growth.

So which is better? Neither. They’re simply different ways to go about selecting stocks. Academic studies have shown that value stocks have, over the long term, been the better bet. We don’t follow either dogma around here, although our Buy List is slightly biased towards value. Or if you want to sound Wall Streety, we have a value “tilt.” Not a big one, but it’s there. I think this is less about value and more that we steer clear of the most speculative names in the growth universe.

Value stocks tend to be more stable, and they often have higher dividend yields. Value tends to outperform growth when the market tanks. The reason we watch the growth-value cycle is that it tells us about the market’s risk-tolerance level. Once a cycle gets started, it usually lasts for a few years.

Here’s a 25-year look at the S&P 500 Value Index divided by the S&P 500 Growth Index:

This one is unusual because it’s run on so long. Every few months, some guru will proclaim that the cycle has finally ended. So far, they’ve all been wrong.

One problem with growth-value analysis is that the most popular way to categorize growth and value is by a stock’s price/book value, meaning its market price compared with its accounting value. This has caused many banks and energy stocks to be classified as value stocks.

Just about every major bank has a price/book ratio near 1. The same goes for most of the big energy companies. This is simply due to the accounting realities of operating in those businesses.

Ideally, the growth and value indexes should tell us about the market’s risk-tolerance level. In the near term, it does that well enough. But the 13-year drought isn’t so much about value and growth. Instead, if reflects the long-term structural problems faced by oil and banking companies.

I was surprised by how violently the market shifted to value in the past week. Wednesday was a brief counter-attack from growth, but that was quickly halted on Thursday. I’ll cautiously say that this could be a real turning point for the cycle.

This means that investors should be cautious of stocks with unusually high valuations. Investors should also make sure they have plenty of dividend-paying stocks in their portfolios. Some value names on our Buy List would be financial stocks like AFLAC (AFL) or Globe Life (GL). Silgan (SLGN) and Middleby (MIDD) are also going for reasonable valuations.

The Economy Is Getting Better—Slowly

Last Friday, the government released the August jobs report, and it was pretty good. Make no mistake, the U.S. economy is still in rough shape, but we’re gradually improving. During August, the economy created 1.371 million net new jobs, and the unemployment rate fell to 8.4%.

It’s odd that 8.4% is now considered good news when that would have been the peak during previous recessions. Over the last four months, the economy has created 10.61 million jobs. That’s good news, but the problem is that in the two months before that, we shed 22.16 million jobs.

The labor-force participation rate is up to 61.73%, which is still very low. Before the pandemic, it was running around 63%. The jobs-to-population ratio is now at 56.5%. It was over 61% at the start of this year.

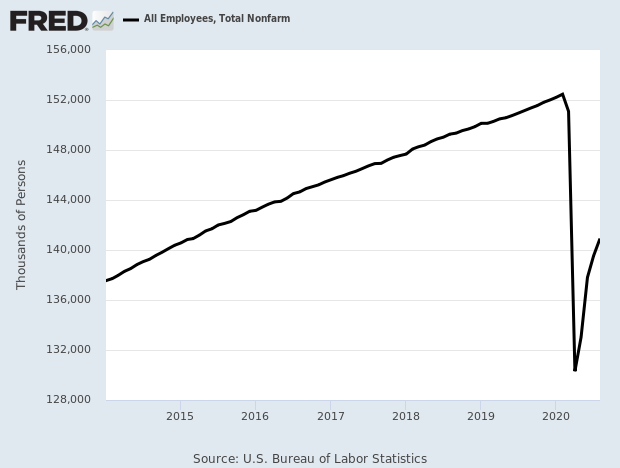

Here’s a look at non-farm payrolls:

The overall message on the economy is that things are rough, but they’re gradually getting back to normal. It will still take several more months, but there is optimistic news out there. This week, for example, Amazon said it’s hiring 33,000 workers and that it’ll have an average compensation package of $150,000 per year. Demand for mortgages is up 40% in the last year.

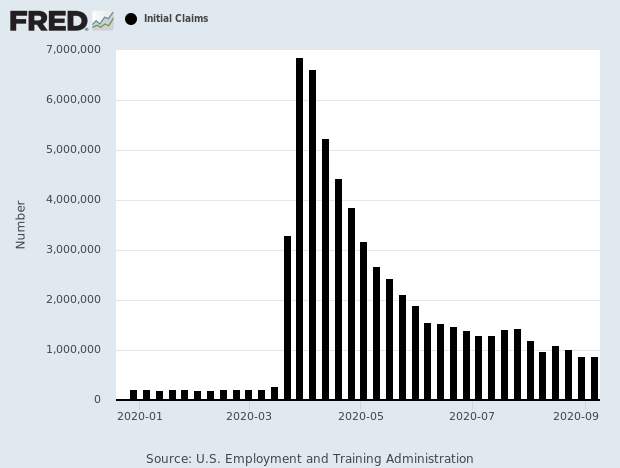

Thursday’s initial-claims report came in at 884,000. That was above Wall Street’s estimate of 850,000. Remarkably, that’s the exact same number as last week’s report, after it was revised. The good news is that these are the lowest reports since the crisis started six months ago.

We’re actually not far from the worst jobless-claims reports of the Great Recession. In early 2009, the reports peaked at 665,000. In 1982, jobless claims got to 695,000.

The four-week moving average for claims through the week of Sept. 5, a number which helps smooth out volatility in weekly numbers, declined 21,750 to 970,750. The moving average for continuing claims fell 523,750 to 13.982 million.

Claims under the Pandemic Unemployment Assistance program continued to climb, rising more than 90,000 last week to 838,916. The total of those claiming benefits through all programs, though Aug. 22, also rose to just over 29.6 million.

At the state level, California showed the biggest increase at 17,953, while Florida reported a decline in claims of 9,049, according to unadjusted numbers.

Continuing claims are now at 13.385 million. That’s after peaking at close to 25 million in May. This week’s continuing claims report is slightly higher than last week’s. The Labor Department said that it changed the way it does seasonal adjustments, so the numbers aren’t precisely comparable.

The trade deficit is now at a 12-year high. The government also said this week that the budget deficit hit $3 trillion in August. September is the final month in the Federal government’s fiscal year. When the fiscal year is up, the deficit will be about $3.3 trillion, give or take. This will be the first time since World War II that the deficit was larger than the economy.

Buy List Updates

Intercontinental Exchange (ICE) has completed its $11 billion acquisition of mortgage-services company Ellie Mae. ICE’s CEO Jeffrey C. Sprecher said, “Ellie Mae’s industry leadership and best-of-breed technology will better enable us to further accelerate the automation of the mortgage-origination workflow, which will benefit stakeholders across the production chain, including consumers.”

RPM International (RPM) said it will report its fiscal Q1 results before the market opens on Wednesday, October 7. This is for the quarter that ended on August 31. For Q1, RPM expects net sales growth “in low single digits and adjusted EBIT growth of 20% or more.” RPM hasn’t provided any full-year guidance.

Hershey (HSY) said it’s partnering with Google to target ads towards people are who less likely to go outside for trick-or-treating. The companies claim they can spot a consumer’s willingness to go outside based on their search history. Honestly, it sounds a little creepy, but I understand they need to spend marketing budgets wisely. For Hershey, Halloween represents 10% of its annual sales. It’s not holding back. Hershey plans to spend 160% more than it did last year on digital ads.

Shares of Disney (DIS) have been performing well lately. Or rather, not falling like everyone else. The movie Mulan is a bona-fide hit. However, Disney is facing backlash because it filmed parts of the movie in areas of China where the government has committed gross human-rights violations.

Mulan was to be released in March, but it had to be delayed due to the coronavirus. Disney opted to release the movie on its streaming service. For now, Disney is facing a PR nightmare, and it’s their own fault. Even worse, in the credits, Disney thanks the local government. The company should have known better. It’s 2020 and companies need to be more aware of such issues.

That’s all for now. There are some important economic news and events coming our way next week. On Tuesday, we’ll get the report on industrial production. The retail-sales report comes out on Wednesday. The Federal Reserve meets on Tuesday and Wednesday. The Fed’s policy statement will come out on Wednesday afternoon. Chairman Powell will also hold a post-meeting press conference. Thursday is another jobless-claims report. We’ll also get reports on housing starts and building permits. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: September 11, 2020

Posted by Eddy Elfenbein on September 11th, 2020 at 7:04 amChina’s Expanded Export Controls Pose Fresh Challenge to Global Tech Industry

Fear And Frustration: Europe’s Wealthy Keep Wallets Closed

Hedge the U.S. Election in Currency Markets

The Dangers of the Fed Aiding Fiscal Policy

Has Business Left Milton Friedman Behind?

A Deflationary Mindset That Isn’t In Our Minds

Rio Shakeout Shows How Powerful Investor Advocacy Has Become

Citigroup’s Fraser to Be First Woman to Lead a Big Wall Street Bank

The New ‘Blank Check’ Barons Are Coming for Wall Street

Tesla Plans to Start Shipping Out Cars Made at Shanghai Gigafactory

Netflix CEO Says Company Won’t Buy Movie Theater Chain

Michael Batnick: Most Stocks Suck

Ben Carlson: The Emotional and Financial Costs of Infertility

Howard Lindzon: Mental Health – Give Yourself A Break

Joshua Brown: An Endless Responsibility & The Stupendous Luck Of Bill Gates And Other Money Psychology Fables – With Morgan Housel

Be sure to follow me on Twitter.

-

Jobless Claims Unchanged

Posted by Eddy Elfenbein on September 10th, 2020 at 10:21 amThis morning’s initial claims report came in at 884,000. That was above Wall Street’s estimate of 850,000. Remarkably, that’s the exact same number as last week’s report, after it was revised. The good news is that these are the lowest reports since the crisis started six months ago.

We’re actually not far from the worst jobless-claims reports of the Great Recession. In early 2009, the reports peaked at 665,000. In 1982, jobless claims got to 695,000.

The four-week moving average for claims through the week of Sept. 5, a number which helps smooth out volatility in weekly numbers, declined 21,750 to 970,750. The moving average for continuing claims fell 523,750 to 13.982 million.

Claims under the Pandemic Unemployment Assistance program continued to climb, rising more than 90,000 last week to 838,916. The total of those claiming benefits through all programs, though Aug. 22, also rose to just over 29.6 million.

At the state level, California showed the biggest increase at 17,953 while Florida reported a decline in claims of 9,049, according to unadjusted numbers.

Continuing claims are now at 13.385 million. That’s after peaking at close to 25 million in May. This week’s continuing claims report is slightly higher than last week’s. The Labor Department said that it changed the way it does seasonal adjustments, so the numbers aren’t precisely comparable.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His