-

Ingredion Earns $1.89 per Share

Posted by Eddy Elfenbein on August 1st, 2017 at 8:38 amThis morning, Ingredion (INGR) reported Q2 earnings of $1.89 per share. Wall Street had been expecting $1.85 per share. They earned $1.73 per share in last year’s Q2.

“We continue to deliver shareholder value with another strong quarter, including solid operating income and earnings per share growth. Good operating efficiency, the impact of acquisitions, and higher specialty volumes more than offset headwinds in South America,” said Ilene Gordon, chairman, president and chief executive officer. “Operating income in North America reached record levels, but was lower in South America due to macroeconomic headwinds and the temporary interruption of manufacturing activities in Argentina associated with the implementation of a new labor agreement.”

“As in the past, our growth strategy and continuous improvement programs drove margin expansion. The integrations of TIC Gums, Shandong Huanong Specialty Corn, and the Sun Flour Industry rice business are progressing as planned. We have completed an important organizational restructuring of our Argentina business and we will continue our disciplined approach to cost management. As we continue to execute our strategy, we expect another strong year and reiterate our anticipated 2017 adjusted EPS guidance in the range of $7.50 to $7.80,” Gordon added.

Ingredion reiterated their full-year guidance of $7.50 to $7.80 per share. For the first half of this year, the company has made $3.77 per share. The shares gapped down at the open but are now down about 2%.

-

Morning News: August 1, 2017

Posted by Eddy Elfenbein on August 1st, 2017 at 7:03 amIndonesia Lifts Threat to Ban Encrypted App Telegram

U.S. Nuclear Comeback Stalls as Two Reactors Are Abandoned

No Bubble in Stocks But Look Out When Bonds Pop, Greenspan Says

Discovery to Buy Scripps, Owner of Food Network, in $11.9 Billion Deal

BP Breaks Even in `Tough Environment’ After Debt Hits Record

Honda Posts Strong First Quarter, Sees Higher Annual Profit on Favorable Forex

Coinbase Faces Backlash, Legal Risk Over Bitcoin Cash

Apple, Google Drop Trading Apps After Australian Intervention

Gilead’s Unique Philanthropic Act Will Pay Off

Lessons From An Altria Flash Crash

Debt-Ridden Chinese Giant Now a Shadow of Its Former Size

Amid His Most Important Tesla Milestone, Elon Musk Says He May Be Bipolar

Howard Lindzon: Momentum Monday – Let Ideas Come to You

Ben Carlson: When Risk Is Not Rewarded

Joshua Brown: Chart o’ the Day: August Sucks Sometimes

Be sure to follow me on Twitter.

-

Pending Home Sales Rise 5%

Posted by Eddy Elfenbein on July 31st, 2017 at 11:14 amThe National Association of Realtors reports that pending home sales rose 1.5% in June.

After falling throughout the usually busy spring season, a monthly index of signed contracts to purchase existing homes increased 1.5 percent in June compared with May, and May’s figure was revised slightly higher, according to the National Association of Realtors.

The index was 0.5 percent higher compared with June 2016, the first annual increase since March. So-called pending home sales are a forward indicator of closed sales two to three months later.

“The first half of 2017 ended with a nearly identical number of contract signings as one year ago, even as the economy added 2.2 million net new jobs,” said Lawrence Yun, chief economist for the Realtors. “Market conditions in many areas continue to be fast paced, with few properties to choose from, which is forcing buyers to act almost immediately on an available home that fits their criteria.”

Here’s my preview from CNBC:

This one report out on Monday is a key indicator for the economy from CNBC.

-

Morning News: July 31, 2017

Posted by Eddy Elfenbein on July 31st, 2017 at 6:58 amOPEC’s Existential Sucker Punch

Inflation Hits Low Bar Draghi Set as Stimulus Debate Gets Closer

Spain’s Long Economic Nightmare Is Finally Over

The Biggest Worry for British Bankers Isn’t Brexit

China July Factory Growth Cools But Construction Boom Fortifies Economy

Alphabet Wants to Fix Renewable Energy’s Storage Problem — With Salt

Model 3’s Buzz Belies U.S. Market Barely Getting a Lift From EVs

HSBC to Buy Back Up to $2 Billion in Shares

Discovery Communications To Acquire Scripps Networks Interactive For $14.6 Billion

SoftBank Is Said to Plan Making Direct Offer for Charter

Raytheon’s Troubled GPS III Ground Control Network Slips Again

Uber’s Search for New C.E.O. Hampered by Deep Split on Board

Jeff Carter: Decentralization Vs. Centralization

Jeff Miller: Weighing the Week Ahead: A Congressional Vacation?

Cullen Roche: Indexing Isn’t Just For Quitters and Three Things I Think I Think – Weekend Edition

Be sure to follow me on Twitter.

-

Update: Wabtec Misses Earnings and Guides Lower

Posted by Eddy Elfenbein on July 29th, 2017 at 1:14 pmI neglected to update you on Wabtec (WAB) in Friday’s newsletter. My apologies for the delay.

On Tuesday, the freight services company released a disappointing earnings report. For Q2, WAB earned 75 cents per share. That includes a charge of five cents per share due to “net effect of the restructuring and transaction expenses and the interest expense benefit.” Wall Street had been expecting Q2 earnings of 94 cents per share. Not good.

Wabtec had quarterly revenue of $932.3 million, which was also below Wall Street’s estimate of $1 billion. For all of 2017, Wabtec now expects sales of $3.85 billion and EPS between $3.55 and $3.70. That’s a reduction from their April forecast of $3.95 to $4.15 per share.

This is the fourth time in the last five earnings reports where Wabtec has missed Wall Street’s consensus. So what went wrong? Basically, the environment for their business is pretty bad right now. Wabtec said there was $250 million in sales, which they had expected during Q2, but it never showed. It’s important for us to distinguish what’s bad due to them from what’s bad for everyone in the sector. This is more of a lousy environment story.

On the positive side, Wabtec said their backlog is up 10%. They also just completed the merger with Faiveley.

This is Raymond T. Betler, the CEO, on the earnings call:

The main reason for our shortfall in the second quarter and our reduction in full year guidance is that we’ve seen about $250 million of revenues, roughly 5% of our full year total pushed out due mainly to revised timing of sales and projects already in the backlog, and to the market conditions, which we’ve discussed previously rebounding slower than we anticipated.

These factors are more than offsetting the expected ramp up of synergies from the Faiveley integration during the year. Some of the revenue slippage occurred in the second quarter, including projects for signal, design and construction work, locomotive overhauls, which both have — did not materialize, so we removed them from our 2017 forecast.

Also, we are not yet seeing the expected recovery in the freight aftermarket spending, and the OEM freight markets remained sluggish. As a result, we revised our 2017 guidance as follows: Compared to the first 2 quarters of the year, we expect some modest improvement in our third quarter results due to seasonality, with the strong fourth quarter and an adjusted operating margin target in the fourth quarter of about 15%. With more of our revenues coming from Europe, the seasonality in the third quarter will be more of a factor than it’s been in the past.

The shares dropped nearly 10% on Tuesday, plus another 6% on Wednesday. The stock eventually bottomed at an 11-month low on Thursday. The shares are now going for 20 to 21 times this year’s guidance range. That’s a rich valuation but it may be quite reasonable based on an expected pickup in 2018. We’ll have to see.

I don’t like these numbers but I’m willing to give WAB more time to show us some improvement. For now, I’m lowering my Buy Below price on WAB to $81 per share.

-

These 5 Stocks Could See Big Moves

Posted by Eddy Elfenbein on July 28th, 2017 at 6:43 pm -

Buy Apple Ahead of Earnings?

Posted by Eddy Elfenbein on July 28th, 2017 at 4:12 pm -

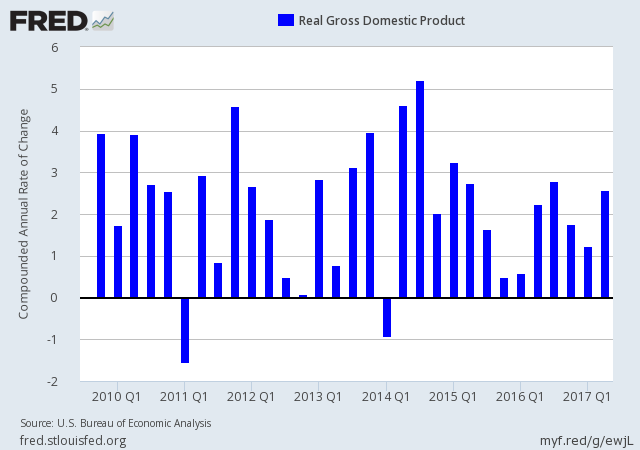

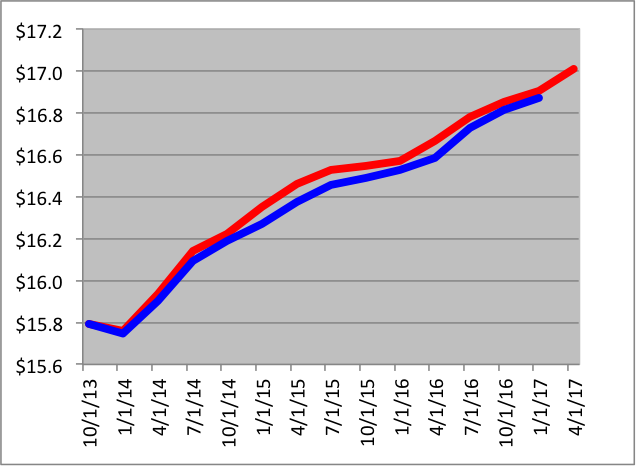

Q2 GDP +2.6

Posted by Eddy Elfenbein on July 28th, 2017 at 11:22 amThe government gave its first report on second-quarter GDP this morning. The U.S. economy grew, in real annualized terms, by 2.6% during April, May and June.

This is slightly above the trend of the expansion. The economy has grown roughly at a 2.1% to 2.2% rate over the last eight years. While the expansion has been long, it’s been unusually weak.

The government will update this figure next month and again in September. In fact, the government will probably update these figures several years from now. This morning, they updated all the GDP figures over the past three years. The old is in blue, the new is in red (real annualized and in trillions).

-

CWS Market Review – July 28, 2017

Posted by Eddy Elfenbein on July 28th, 2017 at 7:08 am“99% of the troubles that threaten our civilization come from too optimistic accounting.” – Charlie Munger

This was another big week for Buy List earnings reports. We also had a Federal Reserve meeting. As expected, the central bank decided against raising interest rates. The stock market seemed pleased as the major indexes rose to more all-time highs. At the same time, the Volatility Index dropped to its lowest levels in more than 20 years.

For the overall market, this is shaping up to be a very good earnings season. About 80% of companies in the S&P 500 have beaten their earnings expectations. The typical “beat rate” usually runs around 65%. Some of the results are being aided by the weak U.S. dollar.

In this week’s CWS Market Review, I’ll go over all our recent earnings news. Moody’s, Express Scripts and Stryker all beat and raised guidance. I love seeing that! At the other end, RPM International had a lousy report. They missed expectations by a mile. I’ll go into more details on that in a bit. I’ll also preview the final batch of Buy List earnings coming our way next week. First, though, let’s look at last week’s excellent earnings report from Moody’s.

Good Earnings from Moody’s, Bad Earnings from RPM

Last Friday, shortly after I sent you last week’s newsletter, Moody’s (MCO) reported very good earnings, plus they raised guidance. For Q2, the ratings company earned $1.51 per share, which is a 16% increase over last year. That beat expectations by 17 cents per share. Quarterly revenues were up 8% to $1 billion, and operating income rose 12% to $457.5 million. These are very good results.

More importantly, Moody’s raised its full-year guidance range to $5.35 to $5.50 per share. The previous range was $5.15 to $5.30 per share. Things are going very well for Moody’s. This week, I’m raising my Buy Below on Moody’s to $141 per share.

On Monday, RPM International (RPM) had a complete dud of an earnings report. The company made $1.02 per share for its fiscal Q4 which was 16 cents below Wall Street’s consensus. Quarterly net sales rose 4.6% to $1.49 billion.

The company’s explanation:

“We took additional cost reduction measures in the fourth quarter to position RPM to a return to double-digit earnings growth in fiscal 2018. We were pleased with solid organic growth in both our industrial and specialty segments during the fourth quarter, which we expect to continue as we enter into fiscal 2018. Organic growth across our consumer businesses was down 1.0%, principally due to lower results at our Kirker nail enamel business, the negative impact of a very rainy start to the spring season for home improvement sales and a difficult comparison to our prior-year quarter in which organic growth across RPM’s core consumer product lines increased 9.9%,” stated Frank C. Sullivan, RPM chairman and chief executive officer.

“The consolidated revenue increase, particularly in a growth-challenged economic environment, was mitigated somewhat on leverage to the bottom line as a result of higher raw material costs during the quarter, including shortages and availability issues in a couple of key product lines. Also, a significantly higher tax rate in the fourth quarter this year versus last year reduced earnings per share on a comparative basis by $0.12.

I’m always a little suspicious when companies blame the weather for their business woes. Now for guidance. RPM sees fiscal 2018 earnings ranging between $2.85 and $2.95 per share. For fiscal Q1, which ends in August, RPM projects earnings between 83 and 85 cents per share. Wall Street had been expecting $3 per share for the year and 89 cents per share for Q1.

In Monday’s trading, RPM dropped 7%. I’m not pleased with RPM’s progress so far. For now, I’m going to keep my Buy Below at $55 per share.

Express Beats and Raises Guidance

After the closing bell on Tuesday, Express Scripts (ESRX) reported Q2 earnings of $1.73 per share. That’s up 10% from last year’s Q2, and it topped Wall Street’s consensus by two cents per share. Earlier Express told us to expect Q2 results to range between $1.70 and $1.74 per share.

Here are some highlights:

-Adjusted claims of 350.0 million, flat

-GAAP net income of $801.8 million, up 11%

-GAAP earnings per diluted share of $1.37, up 21%

-EBITDA of $1,824.1 million, up 1%

-EBITDA per adjusted claim of $5.21, up 1%

-Adjusted net income of $1,011.6 million, up 1%

-Adjusted earnings per diluted share of $1.73, up 10%

-Net cash flow provided by operating activities of $1,081.2 million, up 146%The best news is that Express raised its guidance. The company now sees full-year earnings of $6.95 to $7.05 per share. The earlier guidance was $6.90 to $7.04 per share. Wall Street had been expecting $6.97 per share. The new range represents growth of 10% over last year.

For Q3, Express expects total adjusted claims of 340 million to 350 million, and they see earnings of $1.88 to $1.92 per share. Wall Street had been expecting $1.89 per share.

Express didn’t have much more to say about the ongoing battle with Anthem. They did say that if they continued to do business with Anthem it would be on terms significantly less favorable for Express Scripts. I will say that I feel more confident about ESRX than I did a few weeks ago, but I want to see more improvement. Express Scripts is a buy up to $69 per share.

Earnings from AFLAC, Cerner, CR Bard and Stryker

There were four Buy List reports on Thursday, all of which came after the close. First up was AFLAC (AFL). For Q2, the duck stock’s operating earnings rose 10.9% to $1.83 per share. That easily beat the range they had given us of $1.55 to $1.70 per share. There are two notes to add. First, the exchange rate knocked off two cents per share. Also, the company got a tax benefit of five cents per share during the quarter. For Q2, AFLAC’s annualized ROE was 13.6%.

Dan Amos, AFLAC’s CEO, stood by the company’s full-year range for operating earnings of $6.40 to $6.65 per share. That assumes that the yen averages 108.70. I’m a little surprised he didn’t raise that range. For Q3, Amos expects AFLAC to earn $1.51 to $1.69 if the yen averages between 105 and 115.

I like these numbers. AFLAC is a buy up to $80 per share.

Cerner (CERN) reported Q2 earnings of 61 cents per share which matched expectations. The healthcare IT company had previously announced an earnings range of 60 to 62 cents per share. Quarterly revenue rose 6% to $1.292 billion which exceeded Cerner’s guidance.

For Q2, operating cash flow was $292.2 million and free cash flow was $119.1 million. Days sales outstanding fell to 73 days from 74 days last year. Total backlog rose 11% to $16.648 billion.

For Q3, Cerner expects revenue between $1.265 billion and $1.325 billion, and EPS between 61 cents and 63 cents. For all of 2017, Cerner sees revenue between $5.15 billion and $5.25 billion. Cerner is narrowing its full-year EPS guidance from $2.44 to $2.56, to $2.46 to $2.54. Cerner remains a buy up to $68 per share.

CR Bard (BCR) reported Q2 earnings of $2.92 per share. That beat their guidance of $2.75 to $2.85 per share. Quarterly sales rose 5% to $979.7 million.

Timothy M. Ring, chairman and chief executive officer, commented, “We continue to see strong, balanced growth across our portfolio and geographies. Half-way through 2017, each of our businesses has performed at or above the top of our forecasted constant currency revenue growth ranges for the full year. In the second quarter we reached a new milestone, with revenue from emerging markets now representing 12 percent of total company revenues. We are pleased with the continued momentum of our global business as we prepare to merge with Becton, Dickinson and Company in the fourth quarter of 2017.”

Bard also raised the low end of its 2017 range by five cents per share. They now expect full-year earnings to range between $11.70 and $11.90 per share. I’m pleased to hear they expect to complete the merger with Becton, Dickinson (BDX) sometime in the fourth quarter.

Our final one this week is Stryker (SYK). For Q2, earnings rose 10.1% to $1.53 per share, two cents more than consensus. Quarterly net sales rose 6.1% to $3.0 billion. In constant currency, that’s an increase of 6.9%.

Kevin A. Lobo, Stryker’s CEO, said “Our growth momentum continued in the second quarter as we continue to drive share gains through new products and strong commercial execution.” Looking at Stryker’s three divisions, Orthopaedics sales rose by 5.5%, MedSurg’s sales increased by 6.2%, and the Neurotechnology and Spine unit saw a sales increase of 6.9%.

Stryker now expects organic sales growth for this year of 6.5% to 7%. For full-year EPS, they expect $6.45 to $6.55. That’s an increase of 10 cents per share at both ends. For Q3, Stryker sees a range of $1.50 to $1.55 per share. This is very good news. I’m raising my Buy Below on Stryker to $149 per share.

Several More Buy List Earnings Next Week

Next week will be another very busy week for earnings. On Tuesday, Fiserv and Ingredion are scheduled to report. Fiserv (FISV) just reached another all-time high. In April, Fiserv reiterated its full-year outlook for $5.03 to $5.17 per share. They didn’t give a range for Q2, but the consensus among analysts is for Q2 earnings of $1.23 per share.

Ingredion (INGR), the plant food people, had a very good report for Q1. They now see 2017 EPS ranging between $7.50 and $7.80. Wall Street is looking for $1.85 per share.

Next Thursday will be crowded with four earnings reports.

Axalta Coating Systems (AXTA) recently helped out another one of our Buy List stocks. Valspar needed to sell its North American Industrial Wood Coatings unit in order to complete its merger with Sherwin-Williams (SHW). Axalta bought it for $400 million in cash. Wall Street expects Q2 earnings of 39 cents per share.

Cognizant Technology Solutions (CTSH) has rebounded quite nicely over the past several months. For Q2, Cognizant expects revenue ranging between $3.63 billion and $3.68 billion and EPS of at least 89 cents per share. That’s quite good. For the full year, CTSH sees revenue between $14.56 billion and $14.84 billion and EPS of at least $3.64.

Continental Building Products (CBPX) has been sliding downward for the last several weeks. I think the wallboard maker is a good buy here. Wall Street expects earnings of 35 cents per share.

Intercontinental Exchange (ICE) is turning into a nice winner for us this year. ICE is up 17.2% for us YTD. The consensus is for Q2 earnings of 76 cents per share. ICE should beat that.

Cinemark (CNK) is due to report next Friday. The movie theater chain had a decent Q1 earnings report but the stock has pulled back. Cinemark theater chain now runs 525 theaters with 5,894 screens. Wall Street expects earnings of 45 cents per share. I expect Cinemark to beat that.

With the turn of the month, we’ll get some key economic reports next week. On Tuesday, we’ll get the latest ISM report. We’ll also get a look at personal income and spending. Wednesday is the ADP payroll report. Then on Friday is the big July jobs report. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: July 28, 2017

Posted by Eddy Elfenbein on July 28th, 2017 at 7:04 amOil Prices May Stay Low ‘Forever’

Speaker Ryan Admits Defeat, Giving Up on Border Adjustment Tax

Amazon Profits Fall Far Short of Expectations, But Investors Shrug

Get Ready For The Less-Profitable Amazon That You Used to Know

Starbucks Doubles Down On China, Targets 5,000 Stores By 2021

Elon Musk Takes The Stage Tonight to Deliver the First Tesla Model 3s

SpaceX Is Now One of the World’s Most Valuable Privately Held Companies

Wisconsin and Foxconn Sign $3 Billion Assistance Agreement

Twitter: Testing Investors’ Patience

Barclays Reports ‘Pretty Good Progress,’ and a $1.8 Billion Loss

R.I.P., Coke Zero: The Five Stages of Ice-Cold Grief

Wells Fargo Broadsided Anew With an Auto Insurance Sales Scandal

Jeff Miller: Stock Exchange: Reading Into Retail Moves

Roger Nusbaum: There’s a Storm Comin’

Michael Batnick: A Few Charts and a Few Thoughts

Be sure to follow me on Twitter.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His