-

The Trump Trade Is Dead—What Now?

Posted by Eddy Elfenbein on March 28th, 2017 at 1:33 pmMy latest from The Observer:

Yesterday, the Dow Jones Industrial Average dropped for the eighth day in a row. For the venerable index, this is its longest losing streak since 2011. The Dow is currently on pace for its worst month since January 2016.

So does this portend bad times? Has President Trump finally pushed the economy off the cliff?

Doubtful. Instead of witnessing a new bear market, what we’re really seeing is the implosion of the “Trump Trade.” This was the furious—and largely unexpected—rally that took hold of the U.S. market after President Trump’s surprise victory. It was the unexpected outcome of a still-less expected event.

Turn back the clocks to election night where, at one point, the Dow futures were down 862 points. That’s how much global markets freaked out over a Trump administration. But Doomsday Day, alas, was a no-show. Cooler heads prevailed and in the following day’s trading, stocks rallied. The Dow closed higher by 257 points. From there, the Dow went on to add more than 2,500 points in less than four months.

Read the rest at The Observer.

-

Morning News: March 28, 2017

Posted by Eddy Elfenbein on March 28th, 2017 at 7:05 amTrump’s Take on Corporate Tax Rate Could Look Very Much Like Obama’s

The Biggest Risk From the Dollar’s Drop May Not Be What You Would Guess

Supreme Court Considers Why Patent Trolls Love Texas

Amazon Clinches Deal To Buy Middle East Online Retailer Souq.com

Elon Musk Launches Neuralink to Connect Brains With Computers

American Airlines Takes $200 Million Stake in China Southern

Jack Dorsey Rings in Square’s Debut in the U.K.

Uber to End Services in Denmark After Three Years

Akzo Nobel to Detail New Strategic Plan on April 19

Virgin Atlantic Braces for a Loss and Blames the Pound

YouTube Ad Boycott May Cost Google $750 Million

Record 220-pound Gold Coin Stolen From German Museum in Mysterious Heist

Bond King Bill Gross Agrees to Settlement in Lawsuit Against Pimco, Ending Nasty Dispute

Josh Brown: Investors Underperforming Their Own Investments

Be sure to follow me on Twitter.

-

Morning News: March 27, 2017

Posted by Eddy Elfenbein on March 27th, 2017 at 7:05 amGerman Business Confidence Increases to Strongest Since 2011

Dollar Hits Four-Month Low as Trump Trade Deflates

Oil Slips Towards $50 On Doubts Over Output-Cut Extension

These Charts Show Alarm Bells Ringing on the Trump Trade

California’s Vow to Reduce Auto Pollution May Be Setting Up a Full-Out War With Trump

Push For Internet Privacy Rules Moves to Statehouses

EU Antitrust Regulators Clear $130 Billion Dow, DuPont Merger

Publishers Retreat From the Risks of Google-YouTube Advertising

Can GameStop Stock Bounce Back After Last Week’s 16% Drop?

BT Shares Extend Losses As Regulatory Headwinds Mount

Walmart Moving Upmarket Does Not Presage The Death Of The American Middle Class

Tesla Model 3 Ramp Up Aims to Crush BMW and Mercedes

Icahn Raises Ethics Flags With Dual Roles as Investor and Trump Adviser

Jeff Miller: What Does the Health Care Decision Mean for Stocks?

Roger Nusbaum: It Doesn’t Have To Be Doom & Gloom

Be sure to follow me on Twitter.

-

CWS Market Review – March 24, 2017

Posted by Eddy Elfenbein on March 24th, 2017 at 7:09 am“If you have trouble imagining a 20% loss in the stock market, you shouldn’t be in stocks.” – Jack Bogle

The streak finally came to an end. On Tuesday, the stock market did something it hadn’t done in the previous 109 trading days. It closed down by more than 1%.

This was the longest such hot streak in more than 20 years, and it was close to becoming the longest in over 50 years. If we look more closely, the recent streak was even more impressive because there were only two days in which the S&P 500 fell more than 0.7%. Of course, we have to remember that not that long ago, a 1% drop was barely a scratch. In 2008, it happened 75 times.

As we know well, Wall Street has a notoriously poor memory.

So, is this the beginning of the end? Have the walls come crashing down? Eh…probably not. Bear in mind that the Trump Rally has endured four North Korean missile launches, two Fed rate hikes, and of course, President Trump himself. Through all that, it’s quietly powered ahead.

But this may be the end of the Trump Trade. It’s a little more complicated than has often been portrayed. I’ll explain what it all means. I’ll also cover some of the recent stories impacting our Buy List stocks. But first, let’s look at the fading Trump Trade.

The Death of the Trump Trade

While there’s been a lot of talk of the Trump Trade, properly speaking, there were two separate trades in recent months.

The first Trump Trade came immediately after the election. That’s when stocks soared. The stock rally was matched by a big downturn for bonds. Within a few days, the yield on the 10-year Treasury jumped from around 1.8% to close to 2.3%. That’s an unusually large move for such a short period of time. Combine that with the fact that the 10-year yield had been creeping higher since the summer, and you can see how dramatically the interest-rate outlook had changed.

Within the stock sectors, the small-caps saw the biggest gains. On November 3, the Thursday before the election, the Russell 2000 stood at 1,156.89 (see below). By November 25, the index had risen to 1,347.20. That’s a jump of more than 16% in just over three weeks. That’s a huge leap for an entire size category.

Among stock sectors, the big winners were Industrials and Financials. The move in the latter was astounding. On our Buy List, shares of Signature Bank (SBNY) soared 21% in four days. Prior to the election, Goldman Sachs warned of dire consequences if Trump were to be elected. That outcome, apparently, didn’t include a massive rally in shares of Goldman. Shares of GS gained more than 60% in the second half of 2016. (The bank’s former COO, Gary Cohn, is now President Trump’s top economic advisor.)

Here’s what was happening. This first stage of the Trump Rally was based on the idea of a markedly improving economy. Traders thought policies in Washington would shift towards fiscal stimulus. That’s why the Cyclicals stocks led the way. The yield curve widened, and defensive areas like Utilities and Staples didn’t fare so well.

But by early December, that stage of the rally had petered out. By December 13, the S&P 500 had reached a near-term peak of 2,271.72. The stock market was pretty flat for a few weeks after that. By Inauguration Day, the S&P 500 closed at 2,271.31.

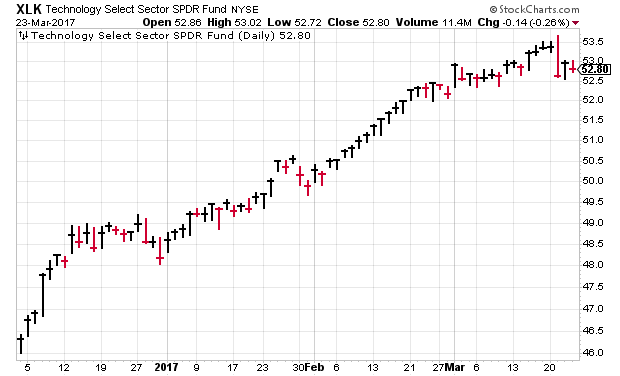

Stage Two of the Trump rally really got going in February. This second stage was led by large-cap tech stocks. Unlike stage one, this time the long end of the bond market was relatively stable. The yield on the 10-year bond peaked around mid-December and has mostly been in a trading range since then (between 2.3 and 2.6%).

Instead, the interest-rate action has been at the short end. The second stage of the Trump Rally happened at the same time there was a perceived need for higher interest rates. This is when we saw yields at the short end of the yield curve touch levels they hadn’t seen in seven or eight years. This move in the market foreshadowed last week’s Fed rate hike. In fact, it also caused traders to think more hikes were on the way.

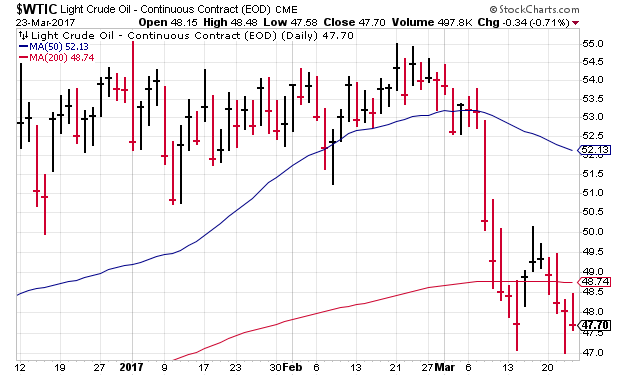

But now, that thesis is starting to show holes. For one, we can’t help noticing the price of oil. One month ago, West Texas Crude got as high as $54.45 per barrel. Everything was going right for OPEC. The production cuts were holding. Finally! But the latest numbers show that there’s still an oil glut. In fact, it’s a big one, and the oil markets are taking notice. At one point, the price of oil fell ten times in eleven days. This week, West Texas Crude came close to falling below $47 per barrel.

Goldman Sachs noted that OPEC’s production cut has had an unintentional side effect—it has spurred the biggest productions in history. It’s hard to say that the Fed needs to raise interest rates to combat inflation when the price of oil is dropping.

Both parts of the Trump Rally have seen rising share prices and low volatility. If I had to pinpoint a single day when the Trump Rally peaked, it would probably be the day after President Trump’s congressional address. Traders loved the speech. The Dow shot up 300 points the following day.

Since then, however, the market has had a tough time getting its footing, and some cracks are starting to show. For example, 217 stocks in the S&P 500 are currently below their 50-day moving average. The overall index is just 0.72% above its 50-DMA. There are now 171 stocks in the index that are more than 10% below their 52-week high, which is the traditional definition of a market correction. In other words, more than one-third of the index is effectively in a correction already.

On Tuesday, the S&P 500 lost 1.24%. Ryan Detrick notes that the average worst day of the year is three times worse than Tuesday’s loss, which is our current worst day of the year. It wasn’t bad, but it was different from the trend, and that’s what catches our attention. The Nasdaq Composite, actually, hit a new all-time high on Tuesday, which shows the impact of large-cap tech.

So stage one of the Trump Rally (November and December) was about a resurgent economy. Stage two (February) was about taking on more risk due to higher rates.

What to do now: I’m still holding onto my view that stocks are due for a modest pullback. It may have already started, since the S&P 500 has now gone three weeks without making a new high. But let me caution you not to worry. I’m not expecting a major decline.

Make sure that you’re well diversified and look for decent dividends. Microsoft (MSFT), for example, currently yields 2.4%. Cinemark (CNK) yields close to 2.7%. I think there’s a very good chance that we’ll be looking at a lot of bargains in the spring. Now let’s look at some news affecting our Buy List stocks.

Buy List Updates

Sherwin-Williams (SHW) said the acquisition of Valspar will take longer than expected. It doesn’t seem to be a major problem. They have to work through some divestitures. Originally, Sherwin thought the deal would close by April. Now they’re thinking it will be June. Going into the deal, SHW knew they were going to have to sell off some units to appease regulators. They just didn’t know what. Don’t let this news worry you. Sherwin-Williams is doing fine.

HEICO (HEI) announced a 5-for-4 stock split. This means investors will get an extra share for every four they currently own. The share price will be expected to fall about 20%. The semi-annual dividend will stay at nine cents per share, so that’s effectively a 25% increase.

I’m never sure why companies like to do small splits like this. If I had my way, only 2-for-1 splits or higher would be allowed, and the share price needs to be over $100. This will be HEICO’s 15th stock split since 1995. The split is payable on April 18 to shareholders of record as of April 7. Cash will be paid in lieu of fractional shares. If you had invested $100,000 in HEICO in 1990, today it would be worth $18.7 million.

That’s all for now. Next week is the final week of the first quarter. On Thursday, the government will update the Q4 GDP report for a second time. Before that, on Tuesday, we’ll get the report on consumer confidence for March. Then on Friday, we’ll get the reports on personal income and spending for February. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: March 24, 2017

Posted by Eddy Elfenbein on March 24th, 2017 at 4:39 amChina Bets on Sensitive U.S. Start-Ups, Worrying the Pentagon

Venezuela’s Fuel Shortage Is Getting Worse

Oil Set for Weekly Drop on U.S. Supply Before OPEC Meet on Cuts

Scrapping TPP a Mistake as China Fills Void, Ex-USTR Froman Says

Planning for a Low-Tax, High-Deficit World

Senate Panel Presses SEC Nominee on Conflicts

The Senate Just Voted To Undo Landmark Rules Covering Your Internet Privacy

YouTube Advertiser Exodus Highlights Perils of Online Ads

Lessons From Richard Branson’s Goodbye Letter to Virgin America

Why Morgan Stanley Is So Bullish on Tesla and the Model 3

Micron’s Earnings Reveal Cloud and SSD Demand Have Joined Rising Prices as Growth Engines

Samsung Elec Rejects Calls For Holding Company Structure, For Now

Credit Bureau Experian Fined $3 Million Over Misleading Credit Scores

Jeff Miller: Stock Exchange: Trading in a Time of High, News-Driven Risk

Cullen Roche: The Biggest Myths in Investing, Part 9 – Risk Is Something We Can Quantify

Be sure to follow me on Twitter.

-

Morning News: March 23, 2017

Posted by Eddy Elfenbein on March 23rd, 2017 at 6:45 amWorld’s Biggest Meat Producer Struggles With Bad Beef Allegations

North Korea Said to Be Target of Inquiry Over $81 Million Cyberheist

Big Oil Replaces Rigs With Wind Turbines

China Bets on Sensitive U.S. Start-Ups, Worrying the Pentagon

Virgin America Will Disappear Into Alaska Airlines in 2019

Nike Suffering Its Own Brand of March Madness

Tencent-led Funding Said to Value Video App at $3 Billion

Wells Fargo Banks on New Ad Campaign to Regain Customer Trust

Why Airbnb’s New China Push Could Actually Work

AT&T and Johnson and Johnson Pull Ads From YouTube

With Sears’ Future In Doubt, Vendors Begin Pulling Back

Where De Beers Hid Its $5 Billion Diamond Stash

Bebe Plans to Shut Its Stores and Focus on Web Sales

Jeff Carter: The Blockchain, Cryptocurrency and Trust

Joshua Brown: QOTD: The WSJ Unloads on “Fake President”

Be sure to follow me on Twitter.

-

Morning News: March 22, 2017

Posted by Eddy Elfenbein on March 22nd, 2017 at 7:08 amDublin Is Best EU City for Bankers Fleeing Brexit, Study Says

Chinese Supermarkets Pull Brazil Meat From Shelves As Food Safety Fears Grow

Devices Banned on Flights From 10 Countries Over ISIS Fears

Stocks Retreat, Havens Gain as Trump Trade Wobbles

What to Expect When You’re Expecting Acosta as Labor Secretary

Airbnb Adopts New Name, Doubles Investment to Woo China

Li Ka-Shing’s Main Companies to Increase Dividend Payments

Amazon Has a New Tactic to Fight Counterfeits

FedEx Earnings Are Worth a Second Look

Akzo Nobel, Maker of Dulux Paint, Rejects 2nd Offer From American Rival

Parent of Sears and Kmart Issues Warning as Its Losses Mount

Acushnet: Looks Like An Amazing Short At $18

A.I. Expert at Baidu, Andrew Ng, Resigns From Chinese Search Giant

Howard Lindzon: Pepsi Can Buy Russia and Make America Smoke Again

Be sure to follow me on Twitter.

-

The 1% Streak Comes to an End

Posted by Eddy Elfenbein on March 22nd, 2017 at 12:55 amThe S&P 500 fell over 1% today for the first time since October 11. The index amassed an impressive run of 110-straight days without a 1% loss. In fact, there were only two losses that exceeded 0.7%. This is the longest such streak since 1993.

Today, however, the index dropped 1.24%. From a larger context, that’s hardly a terrible loss. Not that long ago, losses like that happened all the time. But in our placid market of recent months, it’s an outlier.

The losses were not evenly spread out. The banks, for example, took it hard. Bank of America was down 5.8%. Morgan Stanley dropped 4.3%. Our own Signature Bank lost 4.2%. BAC usually has the highest volume of any stock but today it had its highest volume in four months. Interestingly, there was no news today specific to BAC.

Outside the banks, it really wasn’t that bad a day. The staples were down slightly and the utes were up. Whenever you see the financials and utes move in opposite directions like that, you know the market is debating short-term rates. Today was a strong move in favor of those thinking short-term rates will stay low for longer. I don’t know if they’re right, but they had control of the markets today.

In the futures market, the odds of a June rate hike declined from 58.3% to 54.0%.

I saw plenty of commentary saying the market fell for this or that reason (Trump, taxes, healthcare, North Korea). Call me skeptical. The healthcare stocks didn’t move that much.

-

RIP: David Rockefeller

Posted by Eddy Elfenbein on March 21st, 2017 at 5:36 pmHere’s my piece in The Observer.

Here’s Where Rockefeller Was Different

We’ve lost something larger than a man.

David Rockefeller passed away Monday, aged 101. He was the last surviving grandchild of the great oil tycoon, John D. Rockefeller, Sr. Born into great wealth and opulence—he grew up in the largest private residence in New York City—Rockefeller also inherited his famous family’s sense of noblesse oblige. The New York Times estimates that, over the course of his life, he donated $900 million to charity.

Rockefeller was part of a vanishing and perhaps extinct breed of men—the Establishment Men. Serious and sober-minded gentlemen, well-born and from the East Coast elite, who left the Ivy League to serve their fellow men. They started foundations, served on boards, built skyscrapers, collected art, preserved nature and promoted high culture.

Yet it was all done with an air of calm reserve. Rockefeller was a gentleman who embodied the great Yankee virtues of thrift and hard work. Well into his nineties, he would work from his office in, naturally, Rockefeller Center, the complex built by his father during the Depression.

David Rockefeller was also a visionary who refused to accept the staid conventions of banking. In the 1970s, as chairman of Chase Manhattan, Rockefeller led a bold strategy of international expansion. He traveled the world and became a de facto global ambassador for American-style capitalism. In 1973, he even managed to open a branch office in the Soviet Union.

Read the rest at The Observer…

-

Keep Your Eye on Real Rates

Posted by Eddy Elfenbein on March 21st, 2017 at 12:28 pmFrom John Melloy at CNBC:

The bears believe that low interest rates have been the primary driver of this bull, allowing companies to borrow cheaply to buy back their own stock and making ballooning multiples acceptable on a relative basis. Now that the Fed is in an interest rate hiking cycle, with moves to shrink its balance sheet likely on the horizon, the bears believe the run fueled by cheap money is over.

But Eddy Elfenbein, manager of the AdvisorShares Focused Equity ETF, points out that real rates (interest rates minus inflation) are still low.

The “median Fed member sees the range for fed funds rates to be 2 percent to 2.25 percent by the end of 2018,” said Elfenbein citing the latest Fed “dot plot” data. “They also see inflation at 2 percent. That means real rates will remain negative (and next to negative) for nearly two more years.”

“That’s the strongest point in the bulls favor,” he said.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His