-

Good Earnings for Medtronic

Posted by Eddy Elfenbein on May 21st, 2013 at 10:43 amThis morning, Medtronic ($MDT) reported its fiscal fourth-quarter earnings. Excluding special items, MDT made $1.10 per share which beat Wall Street’s consensus by seven cents per share. Frankly, this was a bit of a shock to me. I knew business was going well for Medtronic but this number was better than I was expecting.

Digging into the numbers, the big surprise was that sales of pacemakers and defibrillators rose. Pretty much everyone was expecting continued declines. Sales of defibrillators rose by 1.5%, and pacemakers were up by 2.6%. Company-wide, revenues were up by 3.8% last quarter. Medtronic’s CEO, Omar Ishrak, said that for the first time in 4-and-a-half-years, sales of defibrillators and spinal products rose in the U.S. in the same quarter.

For the year, Medtronic made $3.75 per share. That’s up from $3.46 per share in 2012. Some history: Last May, MDT originally saw earnings for this year coming in between $3.62 and $3.70 per share. In January, they raised the range to $3.66 — $3.70 per share.

For fiscal 2014, Medtronic projects earnings between $3.80 and $3.85 per share. Wall Street had been expecting $3.84 per share. Traders are very pleased with today’s news. Shares of MDT are up more than 6.5% this morning. The shares are at their highest point since September 2008.

Sometime next month, MDT will raise its dividend for the 36th year in a row.

-

Morning News: May 21, 2013

Posted by Eddy Elfenbein on May 21st, 2013 at 7:16 amBundesbank Says German Recovery to Gather Pace in Second Quarter

Yen Slips as Amari Backtracks While Europe Shares Decline/a>

Fed’s Evans Says Economy Has Been ‘Improving Quite a Lot’

But Wait. Didn’t Yahoo Try a Deal Like This Before?

Good News For Boeing: 787 Dreamliner Deliveries Resume And United Takes Off

Seamless And GrubHub, 2 Nearly Identical Food Websites, Are Now Officially The Same Thing

Clearwire Investors Anticipate Higher Bid as Sprint Vote Looms

Campbell Soup Beats Street Estimate, Raises Outlook

JA Solar Rallies on Narrower-Than-Expected 1Q Loss

Dell Renews Call For Details On Carl Icahn’s Takeover Bid

Before Tumblr, Founder Made Mom Proud. He Quit School.

Edward Harrison: Germany Is Willing To Accept A Higher Inflation Target But Does It Matter?

Be sure to follow me on Twitter.

-

The Garbage Stock Rally

Posted by Eddy Elfenbein on May 20th, 2013 at 2:55 pmYou know what’s rallying? Crap!

The most-indebted U.S. companies are rallying more than any time in almost four years compared with the rest of the stock market amid the broadest rally since at least 1995.

Federal Reserve interest rates near zero and the expanding economy are allowing Standard & Poor’s 500 Index companies with the lowest working capital, smallest earnings and highest debt ratios to reduce borrowing costs and avoid default. The stocks surged 27 percent this year, almost double the gains for businesses with the most cash and least borrowing, according to data compiled by Bloomberg and Goldman Sachs Group Inc.

Bulls say the spread shows the futility of fighting the Fed at a time when more than 90 percent of the companies in the Russell 1000 Index have risen in 2013, the most in at least 18 years. Bears say loose monetary policy has inflated prices and owners of the riskiest stocks will suffer the biggest losses when the Fed curtails bond purchases.

“The rally is so broad that the weakest companies that hadn’t been participating have finally caught fire and roared ahead,” said Anthony Lawler, a fund manager who helps oversee about $53 billion at GAM Holding AG in London. “A rally can stay broad-based for a period of time. It’s not an indication that it’s toppy.”

(…)

Industries most reliant on economic growth have led gains since the S&P 500 reached a six-week low on April 18, data compiled by Bloomberg show. Banks, mining companies, technology producers and material shares climbed more than 9 percent in the period. A total of 914 companies in the Russell 1000 have risen this year, the most since Bloomberg data starts in 1995.

Indebted companies beat those with stronger finances by about 1 percentage point since April 28 after outperforming by 9 points in the first three months of the year, the most since the third quarter of 2009, the data show.

“The catch-up is greater in stocks with weak balance sheets,” Hayes Miller, who helps oversee about $48 billion as the Boston-based head of asset allocation in North America at Baring Asset Management Inc., said in a phone interview on May 17. “Investors by and large feel they have to gain greater exposure to equities.”

-

Yahoo’s $1.1 Billion Mistake

Posted by Eddy Elfenbein on May 20th, 2013 at 11:12 amYahoo ($YHOO) is buying Tumblr for $1.1 billion which, in my opinion, is a big mistake. I’ve long been a critic of Yahoo, or more specifically, Yahoo’s valuation. It’s a fine company but it’s not an especially fast-growing company.

I think Yahoo is basically similar to a newspaper and it should be valued the same way. For many years, I said that Yahoo should be valued around $15 per share, and I was usually right in that the stock failed to perform.

The advent of Marissa Mayer, however, has changed that and the stock has jumped over the last few months to $27 per share. Yahoo is still over-priced but not as egregiously as before.

The good news for Yahoo is they got a pile of cash from selling off their stake in Alibaba. This brings us to the “Bladder Theory” of corporate finance — oftentimes too much cash is not a good thing. Management feels they have to do SOMETHING BIG. Too much cash over-inflates the role of management, and they feel they have to do something dramatic. As I’ve often said, there’s nothing wrong with a special dividend.

Yahoo clearly feels the need to stay hip and cool so buying Tumblr seems like an easy choice. From the New York Times:

The blogging site has been trying to create new ad efforts like interactive campaigns, rather than using standard clickable ads, with mixed success. It has set a revenue goal of $100 million for this year; the company reported only $13 million for the first quarter and reported $13 million for 2012.

Despite its ranking as the 24th most viewed Web site on the Internet, according to Quantcast, Tumblr has yet to translate that into success on mobile devices, something Yahoo needs.

Tumblr also bears a fair amount of unsavory content that may unsettle advertisers. Pornography represents a fraction of content on the site, but not a trivial amount for a site with 100 million blogs.

The search for profits isn’t unique to Tumblr, as free apps and services struggle to wring money from their users. Instagram famously generated no money when Facebook bought it.

A good indicator of a bad merger is when it’s done out of fear, and that’s what this is. Ideally, a merger should appear to be an obvious extension of both parties’ business. Yahoo is paying more than 10 times revenue for a company that might not hit its revenue target. I don’t see the need for that.

At Fortune, John Saroff has a better idea:

Instead of Tumblr, I propose that Yahoo focus its cash not on bulk of pageviews, but on acquisitions and R&D that erect barriers to entry (Buffett’s famous moat) around its already robust display business. Those likely take the form of deep investments in the product and engineering corps and strategic acquisitions of adtech businesses. Those maneuvers will be less sexy, but they have the potential to reinvigorate Yahoo for the next 20 years. It is hard to see how, with all of the strategic risks inherent in the deal, acquiring Tumblr builds the moat for Yahoo that I believe it needs

-

Aaron’s (AAN) Is a Good Buy Here

Posted by Eddy Elfenbein on May 20th, 2013 at 10:48 amOne stock that I’ve been watching closely is Aaron’s ($AAN), the lease-to-own retailer. The company came in below expectations on their last two earnings reports and I think that has unduly hurt the shares. The stock closed on Friday at $28.72 but I think the shares are worth close to $35.

A few weeks ago, with the first-quarter earnings report, Aaron’s lowered their full-year forecast. The old range was $2.25 to $2.41 per share, and the new range is $2.11 to $2.23 per share. Make no mistake, that’s quite a hit. For Q2, AAN expects earnings to range between 45 and 49 cents per share. The Street’s consensus was for 54 cents per share.

The company has had some short-term problems but nothing it can’t fix. The stock is a good value here.

-

An Economist Gives Investing Advice

Posted by Eddy Elfenbein on May 20th, 2013 at 10:19 amHarvard professor Greg Mankiw writes in the New York Times on how economists look at the stock market. He makes several good points except I’m afraid he includes the Efficient Market Hypothesis which only seems to be believed in academia.

The other points Mankiw makes are that the stock market’s moves are often inexplicable. This is absolute true. I recently pointed out that the standard deviation of the Dow’s daily change is more than 40 times its average change. That means there’s a lot of noise in there. Mankiw writes that holding stocks is a good bet. I’d add that it depends on which stocks you hold.

In 1985, Rajnish Mehra and Edward C. Prescott, both now at Arizona State University, published a paper in the Journal of Monetary Economics called “The Equity Premium: A Puzzle.” They pointed out that over a long time span, stocks have earned, on average, about 6 percent more per year than safe assets like Treasury bills. This large premium, they said, is hard to explain with standard economic models. Sure, stocks are risky, so you can never be certain you’ll earn the premium, but they are not risky enough to justify such a large expected return.

Since the paper was published, economists have made some limited progress in explaining the equity premium. In any event, the large premium has convinced most of us that stocks should be part of everyone’s financial plan. I allocate 60 percent of my financial assets to equities.

The buy-and-hold philosophy is widely mocked nowadays even though it’s been a huge winner for the last three years. Mankiw also stresses the importance of diversity and investing outside the United States.

-

The S&P 500 Has Gained 1,000.58 Points

Posted by Eddy Elfenbein on May 20th, 2013 at 10:02 amI’m back in the office today. I was out traveling last week so there was no newsletter. I’m happy to report that the market had a very good day on Friday. The S&P 500 closed at its intra-day high of 1,667.47 which is a remarkable gain of 1,000.58 points since the intra-day low from March 6, 2009. One point in the S&P 500 is currently worth about $8.9 billion. I was happy to see that Ford finally broke $15 per share. The auto stock closed at $15.08 on Friday.

The stock market is down a bit this morning. Bed Bath & Beyond ($BBBY) is taking a little hit after it was downgraded to Hold from Buy at Jefferies. I’m not at all worried.

Even though Cognizant ($CTSH) disproved its critics by reporting good earnings, the shares have been shaken up by the recent debate on the immigration bill. I’m not yet able to say how this will impact Cognizant but the company is the largest recipient of visas bringing H-1B temporary workers to the United States. CTSH hires these folks then sends them around the country to work at clients’ sites. Whatever bill emerges will probably make it tougher for outsourcing firms, but we don’t know how tough the rules will be. Until then, expect some volatility in CTSH.

Medtronic ($MDT) is due to report its earnings tomorrow and Ross Stores ($ROST) will follow on Thursday. These are the only two Buy List stocks on the January-April-July-October reporting period.

The other big story for our Buy List is tomorrow’s shareholder vote on the fate of Jamie Dimon. JPMorgan Chase ($JPM) shareholders will decide whether to split the roles of Chairman of the Board and CEO. The vote is non-binding and only advisory. Still, I hope they vote yes, or at least enough people do so that Mr. Dimon makes the right decision.

-

Morning News: May 20, 2013

Posted by Eddy Elfenbein on May 20th, 2013 at 6:40 amEU Leaders Struggling With Economic Growth to Turn to Tax Policy

Goldman Sachs To Exit ICBC With $1.1 Billion Stake Selldown

Enron No Lesson to Traders as EU Probes Oil-Price Manipulation

Can Yahoo Buy Its Way Back To Relevance?

Elan Makes Two Acquisitions for $380 Million

Vodafone $100 Billion Stirs Payout, Deal Dreams

H-1B Models Strut Into U.S. as Programmers Pray for Help

Tech Industry Pushes to Amend Immigration Bill

US Senator Proposes Student Loan Refinance Plan

Hedge Fund Owner Gets Subpoena to Testify

JPMorgan Chase Vote Tests Stockholders’ Power

Epicurean Dealmaker: Mr. Indespensable

Jeff Miller: Weighing The Week Ahead: Are You Ready For Some Fedspeak?

Be sure to follow me on Twitter.

-

Morning News: May 17, 2013

Posted by Eddy Elfenbein on May 17th, 2013 at 7:29 amJapan Most Favored Nation in Poll Showing Abe Optimism

China Cuts Red Tape as Premier Li Shows Stimulus Reluctance

Fisher Urges Cutting Mortgage Bond Buying to Avoid Disorder

Initial Jobless Claims Jump To 360,000, Most Since March

CREDIT SUISSE: ‘Gold Is Going To Get Crushed’

Facebook’s Rocky Year As A Public Company

Musk Bulls Power Tesla Ahead of Offering: Mover

Wal-Mart’s U.K. Asda Chain Boosts Sales Growth Amid Lower Prices

Yahoo in Talks to Acquire Tumblr

Maersk Line Posts Profit as Capacity Control Lifts Pricing

Dell’s Profit Dives As Billionaire Battle Rages On

J.C. Penney’s New Plan Is to Reuse Its Old Plans

Bill Gates Retakes World’s Richest Title From Carlos Slim

Jeff Carter: A Solution to Obama’s IRS Problem

Howard Lindzon: Overvalued, Overvalued, Overvalued…NOT the Location, Location Location of Markets

Be sure to follow me on Twitter.

-

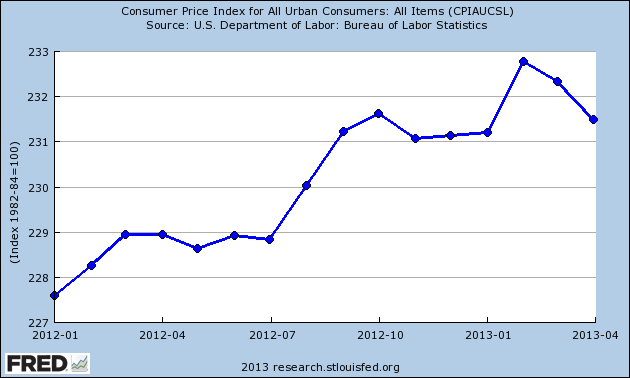

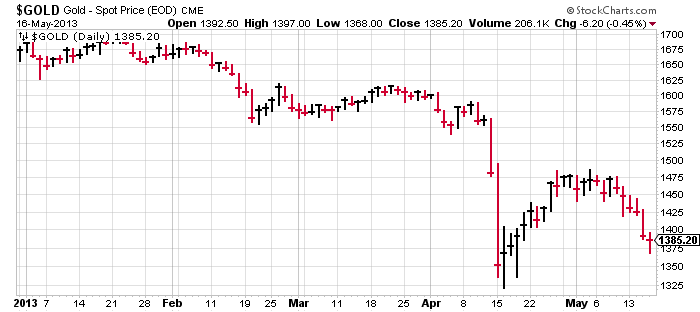

So I Guess Gold Was Right….

Posted by Eddy Elfenbein on May 16th, 2013 at 10:12 pmThe price of gold has been dropping pretty sharply recently. According to my gold model, that must mean the real interest rates have been on the rise. Since short-term rates are still close to 0%, that means that we’ve been experiencing deflation.

This morning, the government confirmed that’s exactly what’s been happening. Consumer prices fell 0.4% last month which is the biggest drop since 2008. It’s also the second-straight monthly drop. The annualized rate of deflation over the last two months was -3.27%. In effect, the Fed has raised interest rates.

Here’s a look at the price of gold. In September 2011, the yellow metal peaked at $1,923 per ounce. Now it’s at $1,385.

- Load More

*UNITEDHEALTH UNDER CRIMINAL PROBE FOR POSSIBLE FRAUD: WSJ

Crossing Wall Street is looking to hire a Director of Social Media. Qualified candidates will be vain, self-centered and argumentative. Relevant skills include missing the point, name-calling, GIFs and being offended.

185% Tariffs: How the Trade War Hit One Shipment of T-Shirts

-

-

Archives

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His