-

Morning News: October 11, 2023

Posted by Eddy Elfenbein on October 11th, 2023 at 7:05 amThis Country Won the Global Tax Game, and Is Swimming in Money

Yellen Says Nothing Is ‘Off the Table’ as U.S. Considers New Sanctions on Iran and Hamas

Higher Rates May Be Needed to Curb Inflation, Fed’s Bowman Says

Largest US Banks Grapple With Worst Write-Offs in Three Years

KKR and Carlyle Take No Carry on New Private Credit Funds

JPMorgan Has a Master Plan to Beat Competitors in Silicon Valley

Even Google Insiders Are Questioning Bard AI Chatbot’s Usefulness

U.S. Considers Dropping Sanctions Against Israeli Billionaire in Push for EV Metals

Exxon to Buy Pioneer for $60 Billion to Dominate Shale Oil

Fear and Anger Follow the Path of Joe Manchin’s Mountain Valley Pipeline

Birkenstock, the German Sandal Maker, Raises $1.48 Billion in Its I.P.O.

The Californization of the Texas Housing Market

Biden to Announce New Actions Slashing Junk Fees

Amazon Wants You to ‘Buy Again’

High UAW Wages Shrink Detroit’s Room to Maneuver

Boeing’s 737 MAX Output Falls to Lowest Level in Two Years

Walgreens Names Veteran Health-Care Executive Tim Wentworth as Next CEO

Claudia Goldin’s Nobel-Winning Research Shows ‘Why Women Won’

Only Question for Taylor Swift Film: How Big Will It Be?

Disneyland Lifts Prices Up to 9%; Florida Annual Passes Rise Too

Caroline Ellison, Adviser to Sam Bankman-Fried, Says He ‘Directed’ Her to Commit Crimes

Be sure to follow me on Twitter.

-

CWS Market Review – October 10, 2023

Posted by Eddy Elfenbein on October 10th, 2023 at 10:25 pm(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

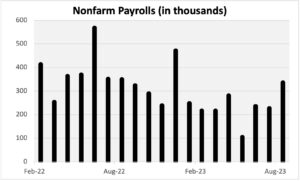

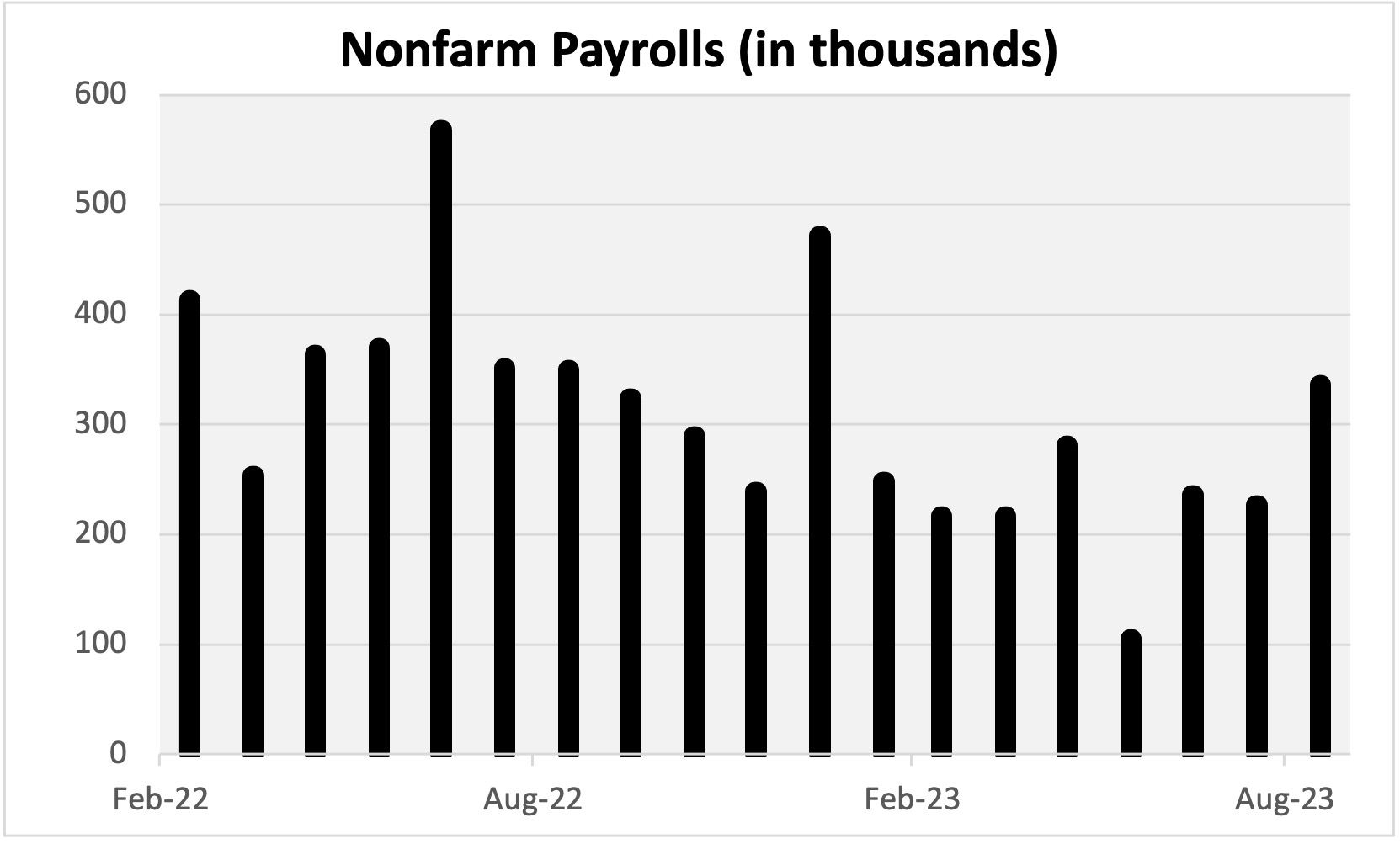

Wall Street Rallies on the September Jobs Report

On Friday, the government said that the U.S. economy created 336,000 net new jobs last month. That was well above expectations for a gain of 170,000. It was also an improvement of more than 100,000 jobs compared with August. September was the best month for job gains since January.

This report is very good news and it’s a sign that the economy may not be in as much trouble as the bears believe. While I’m pleased to see these numbers, I still think the economic cycle may be nearing its end.

Let me explain.

The labor market tends to be a lagging indicator. It usually tells us what just happened instead of what’s about to happen. After all, folks generally don’t lose their jobs until after business conditions weaken.

The jobs report also said that the unemployment rate was 3.8%. Wall Street had been expecting the jobless rate to fall to 3.7%.

I had been particularly interested to see the wage gains numbers. Unfortunately, they weren’t that good. For September, average hourly earnings rose by 0.2%. Wall Street had been expecting a gain of 0.3%. Over the last year, earnings are up by 4.2%. That’s above the rate of inflation but not by much. I disagree with the Fed about lots of things, but we’re on the same page on an important point. The recent bout of inflation was not caused by excess wages.

Here are some details from the jobs report:

From a sector perspective, leisure and hospitality led with 96,000 new jobs. Other gainers included government (73,000), health care (41,000) and professional, scientific and technical services (29,000). Motion picture and sound recording jobs fell by 5,000 and are down 45,000 since May amid a labor impasse in Hollywood.

Service-related industries contributed 234,000 to the total job growth, while goods-producing industries added just 29,000. Average hourly earnings in the leisure and hospitality industry were flat on the month, though up 4.7% from a year ago.

The private sector payrolls gain of 263,000 was well ahead of a report earlier this week from ADP, which indicated an increase of just 89,000.

The labor force participation rate stayed the same at 62.8%. That number has improved a lot but it’s still below the pre-Covid levels. I also like to look at the labor force participation rate for prime working-age adults. That was unchanged at 83.5%. The broader U-6 jobless rate rose to 7%.

The stock market was initially soft after the jobs report came out, but the bulls eventually got in control and the market closed higher. The rally was strong enough to continue into Monday and today. The bond market was closed yesterday for Columbus Day, but yields fell sharply today in a global desire for safety.

The problem with the economy right now isn’t jobs. The economy has created more than two million jobs this year, and there are nearly 10 million open positions. The problem is inflation.

Even if people are employed, they sense that the economy is not as good as it used to be. It’s often noted that if unemployment rises from 4% to 9%, that affects 5% of people. If inflation rises from 2% to 9%, that impacts 100% of people.

We’re at an odd point where jobs are plentiful but your money doesn’t go as far. For example, the cost of housing has been particularly hard on consumers. The median home price is up 27% since late 2019. The median age of a homebuyer is now 36. That’s the highest on record which goes back 40 years.

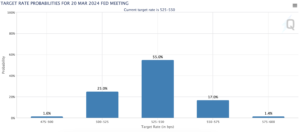

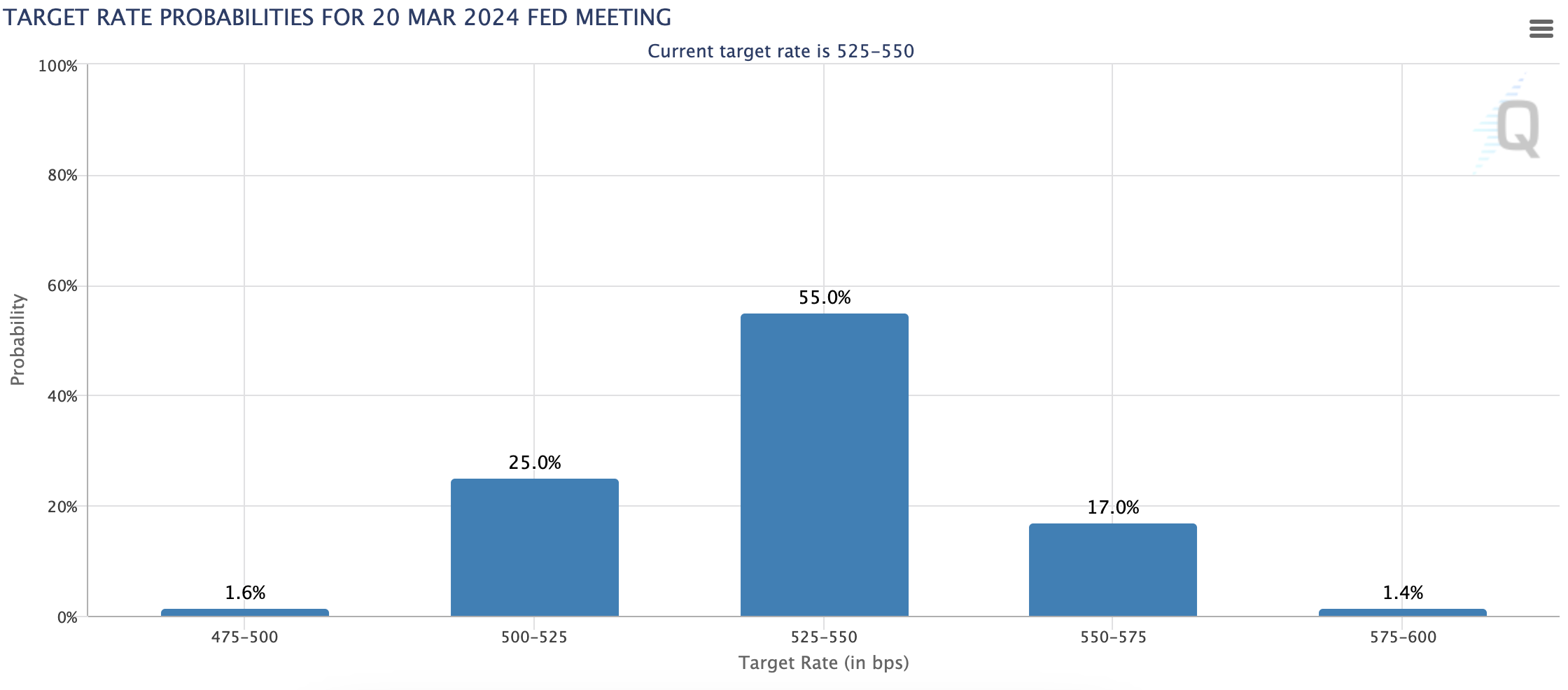

Wall Street seems to have reconciled itself to the fact that the Federal Reserve will pause once again at its next FOMC meeting. The Fed is scheduled to meet again on November 1.

The futures market currently places the odds of another pause decision at 86%. I was surprised to see traders place the odds of a Fed rate cut in March of next year at 25%. One week ago, those odds were at 7%. Those odds may get higher soon. The Fed doesn’t see a rate cut as probable until June 2024.

Here are the odds for the June FOMC meeting:

Raphael Bostic, the head of the Federal Reserve Bank of Atlanta, said he doesn’t see the need for more rate hikes. He’s been one of the more dovish members on the FOMC. It’s as if the recent rise in long-term bond yields has helped do some of the Fed’s work for it.

The market has a few hurdles to get through. Tomorrow, the Fed will release the minutes from its last meeting. This is when the Fed decided to pause on rates, but it tried to sound tough.

On Thursday, the government will release the CPI for September. Wall Street expects both core and headline inflation to have increased by 0.3% last month.

We’re also about to get some of the first earnings reports for the Q3 earnings season. The big banks usually go first. On Friday, Citigroup, JPMorgan and Wells Fargo are set to report.

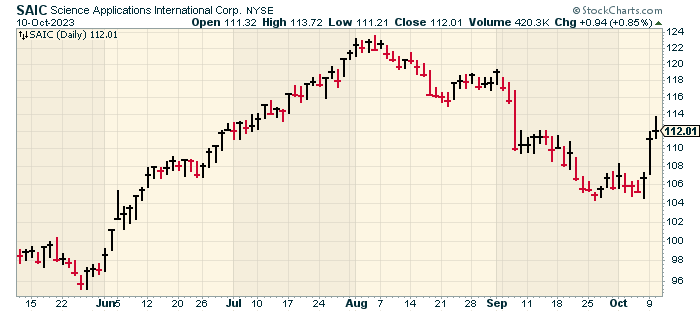

SAIC Is Worth a Look

Defense stocks got a nice boost yesterday for obvious reasons. On our Buy List, we have Science Applications International (SAIC), which is a very good company. SAIC gained more than 4% yesterday and another 2% today.

Last month, SAIC said that its fiscal-Q2 earnings increased by 17% to $2.05 per share. That was well ahead of Wall Street’s consensus for $1.62 per share. This is the third quarter in a row in which SAIC has beaten the Street by more than 17%.

SAIC’s CEO Nazzic Keene said, “I am proud of the financial performance we delivered in the quarter with both strong organic-revenue growth and margin expansion. We remain on track to achieve our three-year financial targets and are off to a strong start.”

SAIC’s operating income increased 7% to $134 million. Operating margin widened by 70 basis points to 7.5%. Q2 EBITDA increased by 5% to $174 million, and EBITDA margin was 9.8%. Free cash flow was $143 million. These are solid results.

One impressive stat is that SAIC reduced its number of outstanding shares. For Q2, SAIC’s number of shares decreased from 55.9 million to 53.9 million. During the quarter, SAIC used $100 million to buy back shares and paid out $20 million in dividends.

SAIC also raised its outlook for the rest of this year. The company now sees full-year earnings coming in between $7.20 and $7.40 per share. That’s an increase of 20 cents to both ends of the previous guidance. Wall Street had been expecting $7.16 per share.

This is the second time this fiscal year that SAIC has increased its full-year guidance. The previous increase was also by 20 cents per share at both ends.

Shares of SAIC had a very nice run earlier this summer, but they had been somewhat weak lately. That is, until this week. SAIC’s next earnings report will be due out in early December. Look for more good results.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

-

Morning News: October 10, 2023

Posted by Eddy Elfenbein on October 10th, 2023 at 7:04 amFragile Global Economy Faces New Crisis in Israel-Gaza War

Israel War: Military Builds Forces Near Gaza as US Sends Aid

Bank of Israel Interventions Reverse Shekel Selloff

Bank of England to Review How It Stress Tests Banks

China Mulls New Stimulus, Higher Deficit to Meet Growth Goal

Country Garden Caves to Debts as China’s Real Estate Crisis Worsens

IMF Warns of Stubborn Inflation and Weaker Global Growth in 2024

U.S. Dysfunction Clouds Economic Diplomacy Efforts

Treasuries Have Best Day Since March on Signs Fed May Be Done

Americans Have Saved Hundreds of Billions More Than Previously Thought

Tiny Homes Are the Hot New Homeowners’ Accessory

Binance Founder’s $1 Billion Plan to Save Crypto Quietly Fizzled Out

South Korean Chip Makers Get U.S. Waivers From China Export Rules

General Motors Workers in Canada Walk Out After Contract Talks Fail

Amazon Dangles Prime Day Deals With Shoppers in ‘Driver’s Seat’

PepsiCo’s Hefty Quarter Pokes a Hole in Idea of an Ozempic-Fueled Sell-Off

Consumers Are Less Interested in Brands Taking Stances on Sociopolitical Issues, Survey Finds

CNN Boss Mark Thompson to Staff: Network Is ‘Nowhere Near Ready for the Future’

Why Nelson Peltz Grew Impatient With Disney’s Turnaround Efforts

Be sure to follow me on Twitter.

-

Morning News: October 9, 2023

Posted by Eddy Elfenbein on October 9th, 2023 at 7:06 amOil Surges as Israel Conflict Reignites Middle East Volatility

Israel Shekel Slumps Despite $45 Billion Central Bank Pledge

Russia’s Economy Is Increasingly Structured Around Its War in Ukraine

U.S. Probe of Russia-Sanctions Busting Focuses on Major Oil Trader

BlackRock’s Hildebrand Wants IMF to Address New Economic Reality

Africa Is Front and Center at IMF as US-China Rivalry Heats Up

Burundi President Replaces Central Bank Governor After 14 Months

China’s Rich Entrust Total Strangers to Sneak Cash Out of the Country

The Free-Money Experiment Is Over

Harvard Professor Goldin Awarded Economics Nobel Prize for Pay-Gap Work

Amid Strikes, One Question: Are Employers Miscalculating?

10-Year Treasuries Aren’t An ‘Important’ Asset, They’re a Consequence

The Wager That Betting Can Change the World

Big-Company Bankruptcies Hang Over Economy

US Wealth, Income Concentration Resume Upwards Climb in Post-Pandemic Era

The U.S. Economy’s Secret Weapon: Seniors With Money to Spend

How Beyoncé and Taylor Swift Struck a New Kind of Movie Deal

Home Depot Tracked a Crime Ring and Found an Unusual Suspect

The Stunning Boom and Bust of a Tax-Refund King

Zombie Viruses Are Waking Up After 50,000 Years as Planet Warms

GSK Partners With Zhifei to Boost Shingles Vaccine Availability in China

Be sure to follow me on Twitter.

-

Morning News: October 6, 2023

Posted by Eddy Elfenbein on October 6th, 2023 at 7:04 amRussia Lifts Diesel-Export Ban That Battered Global Markets

Exxon in Talks to Buy Shale Driller Pioneer Natural in What Could Be 2023’s Biggest Deal

Chevron Labor Dispute Flares Up Again in Australia

New Shein Executive Aims to Expand Supply Chain Outside China

China Is Becoming a No-Go Zone for Executives

The IMF’s $43 Billion Argentina Problem Is About to Get Worse

Rates Are Jumping on Wall Street. What Will It Do to Housing and the Economy?

The 5% Bond Market Means Pain Is Heading Everyone’s Way

Corporate America Is Ignoring Jay Powell and Bingeing on Debt

Finance CEOs Who Have Stuck It Out for 11 Years Are Eyeing Exit

America Has a Bankruptcy Problem

September Jobs Report May Be Last Good One Before Sharp Slowdown

How to Protect Your Retirement From Nagging Inflation

Between a Rock and a ‘Hard’ Insurance Market

Tesla Cuts Model 3, Y Prices in US After Quarterly Sales Dip

The Birkenstock IPO Is Coming. Nobody Mention Crocs.

New This Holiday Season: Discounts on Shipping Packages

Philips Shares Fall 7% After U.S. Drug Regulator Deals Fresh Blow to Sleep Device Recall

PGA-LIV Deal Faces Delay Over Antitrust, Players Demand Stake

Down With Efficiency! (When We Get Around to It.)

Confessions of a Pop-Tarts Taste Tester

Be sure to follow me on Twitter.

-

Morning News: October 5, 2023

Posted by Eddy Elfenbein on October 5th, 2023 at 7:06 amPakistan Considers Long-Term LNG Deal as Domestic Output Slides

Oil Extends Plunge as Brent Falls Below $85 on Demand Worries

High Gas Prices Reek of Low Cigarette Sales

Diesel Prices Could Keep Inflation High

McCarthy’s Ouster Raises Likelihood of a Government Shutdown

Fed’s Bid to Avoid Recession Tested by Yields Nearing 20-Year Highs

Only an Equities Crash Can Rescue the Bond Market, Barclays Says

Traders from Moore Capital Are Spinning Out $3 Billion Hedge Fund to Wager on Inflation

Rising Interest Rates Mean Deficits Finally Matter

The Economics of ‘Free Stuff’ Is That There’s No Free Stuff

They Dredged the Mississippi River for Trade. Now a Water Crisis Looms

America’s Factory Boom Brings Billion-Dollar Projects to Tiny Towns

New U.A.W. Chief Has a Nonnegotiable Demand: Eat the Rich

In This City, the Right to Own a Car Starts at $76,000. And That Doesn’t Include the Car

China’s E.V. Threat: A Carmaker That Loses $35,000 a Car

A Start-Up’s Alternative to Uber: Employing Its Own Drivers

Relocation Concerns Slow Hiring of New Tech Leaders

‘This Is a False Advertisement’: X Ads Are Being Challenged by Reader Context

Ozempic Is Making People Buy Less Food, Walmart Says

French Train Maker Alstom Slumps After Cash Flow Warning

Caroline Ellison Is One of the Only People Who Knows ‘Truth’ Behind SBF’s Fall

Be sure to follow me on Twitter.

-

Morning News: October 4, 2023

Posted by Eddy Elfenbein on October 4th, 2023 at 7:07 amFraud Is Forcing Global Trade to Fix Its Paper Problem

Oil Prices Edge Lower Ahead of Supply Data as Saudis Affirm Extension of Production Cut

Japan Keeps Yen Traders Guessing Over Whether It Intervened

ECB Interest Rate Hikes May Be Over, Centeno Says

Bond Selloff Threatens Hopes for Soft Landing

Investors Eye Profit Rebound After Yearlong Earnings Recession

A ‘Shadow’ Lending Market in the U.S., Funded by Insurance Premiums

Every Generation Makes Money Mistakes. Here’s What They Are

Chaos in Washington Adds to Market Jitters

McCarthy Exit Means More Turmoil Before New US Shutdown Fight

Why 8% Mortgage Rates Aren’t Crazy

As Student Loan Payments Resume, Biden Cancels $9 Billion in Debt

Kaiser Workers Launch Largest Health Care Strike in US History

America’s High EV Costs Are Driving Buyers to Hybrids

Amazon Used Secret ‘Project Nessie’ Algorithm to Raise Prices

SAS Stock Dives 95% as Restructuring Announced

How Dodgy Spare Parts Got Into Jet Engines, Leaving Airlines Scrambling

F.C.C. Issues First Fine Over Space Junk Rule

Spotify Gave Subscribers Music and Podcasts. Next: Audiobooks

Netflix Plans to Raise Prices After Actors Strike Ends

Hollywood Ignored Tyler Perry, So He Built His Own Empire

Be sure to follow me on Twitter.

-

CWS Market Review – October 3, 2023

Posted by Eddy Elfenbein on October 3rd, 2023 at 7:41 pm(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

The Stock Market Continues to Drift Lower

Wall Street is still in a cranky mood, and the culprit is higher interest rates. There appears to be an emerging consensus that the Federal Reserve will hold interest rates “higher for longer.”

Wall Street doesn’t like that. Last week, the S&P 500 closed out its first losing quarter since Q3 of last year. The index continued to fall today. The S&P 500 closed at its lowest level since June. The Dow is now down for the year.

The S&P 500 has already dropped below its 50-day moving average and it’s not too far from breaking below its 200-day moving average. The index has traded above its 200-DMA without stopping for six straight months. Falling below moving averages is often an omen of bad things to come.

What’s next? All eyes are focused on Friday’s jobs report. So far, the labor market has remained calm, but any weakness could convince the bears that they’ve been right.

For August, the economy created 187,000 net new jobs. That was higher than both June and July, and the unemployment rate rose from 3.5% to 3.8%. For this Friday, Wall Street expects to see 170,000 net new jobs created for September and it expects the unemployment rate to fall to 3.7%.

However, the number I’ll be watching most closely is average hourly earnings. The consensus on Wall Street is for earnings to rise by 0.3%. Workers have been getting paid more but that’s mostly keeping with inflation. That’s probably part of the reason why we’ve seen organized labor activity recently.

I won’t make a prediction for Friday’s report, but I will note that other labor reports have been pretty good. For example, the initial jobless claims report is near a seven-month low. On Tuesday, the Bureau of Labor Statistics said that job openings increased in August from 8.9 million to 9.6 million.

I was also impressed by Monday’s ISM Manufacturing Index. This report comes out on the first business day of the month. Monday’s report came in at 49.0. Any number above 50 means the factory sector of the economy is growing, and any number below 50 means it’s contracting.

This was the 11th month in a row of contraction, but it wasn’t by much. Monday’s report was the highest in 10 months.

Despite those selected positive notes, Wall Street seems to be very worried.

As grumpy as the stock market has been, the bond market is even grumpier. On Tuesday, the yield on the 10-year Treasury reached its highest level since 2007.

The yield on the 10-year got as high as 4.781% while the 30-year reached 4.874%, also the highest since 2007. A little over three years ago, the 10-year yield was going for just 0.5%.

Rising interest rates are bad for stocks for two major reasons. One is that interest expense is an important part of a company’s income statement. If it costs more to borrow money, companies will do less of it. It also costs more to refinance existing debt.

The other reason is that higher yields provide stronger competition for investors’ money. The one-year Treasury is going for 5.5%. Sure, it’s not for me, but I certainly can understand investors who’d prefer to make an easy 5.5% for one year than deal with the frenzy of stock market volatility. That 5.5% works out to more than 1,800 Dow points over the coming year, and it’s basically risk-free. What we want to look at isn’t so much the absolute level of interest rates but rather, their direction. Lower yields are good for stocks and higher yields are dangerous.

What’s interesting is that “real” yields, meaning after inflation, are rising as well. Since May 11, the yield on the 10-year TIPs, the inflation-adjusted security, has increased by 1%. It’s not just an inflation story (but that is a big problem).

The two-year yield is often considered to be the maturity that is most sensitive to the Fed’s interest-rate policy. The two-year yield recently rose to 5.129%.

The Federal Reserve doesn’t meet for another month, but the interest rate “hawks” have gotten a little stronger. The futures market still indicates that the Fed will pause at its next meeting, but the dissenters are growing. One week ago, the odds of a 0.25% rate hike in November were just 16%. Now they’re at 30%.

This week, Raphael Bostic, head of the Atlanta Fed, said he can see interest rates at the current range of 5.25% to 5.5% well into next year.

He’s not alone. Loretta Mester, the president of the Cleveland Fed, said rates could be held higher “for some time.” The next CPI report will be out on Thursday, October 12.

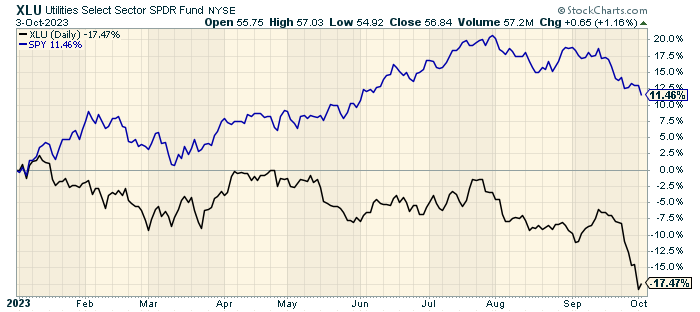

I’ve also been struck by how many conservative stocks have been getting squeezed by this market. For example, utility stocks are lagging badly. Check out this chart of the S&P 500 versus the S&P 500 Utility ETF:

Related to this is that growth stocks have been holding up much better than value stocks have this year. I’m not sure that can last for much longer. If the broader economy starts to get shaky, that will help the relative performance of many defensive stocks.

The Boring Stock Portfolio

In his book, One Up on Wall Street, Peter Lynch extolled the virtues of investing in boring stocks. There are many stocks that are very good businesses, but they really don’t do anything interesting. As such, investors tend to overlook them.

Just because the sector isn’t interesting doesn’t mean it’s not important, or unprofitable. These are companies that are rarely mentioned on TV.

There’s a group of boring stocks that I like to follow. Here’s a sample of some good but very dull stocks.

American Water Works (AWK) is a nice, dull stock. AWK is a public utility that provides water to 1,700 communities across 24 states. Water is a good business to be in. No town wants to be another Flint, Michigan water disaster.

American Water “owns 80 surface water treatment plants, 480 groundwater treatment plants, 160 wastewater treatment plants, 52,500 miles of pipes, 1,100 groundwater wells, 1,700 pumping stations, 1,300 water storage facilities, and 76 dams.”

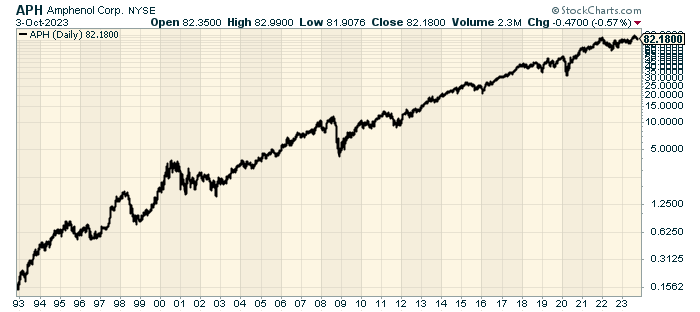

Amphenol (APH) is a former Buy List stock. The company makes electronic and fiber optic connectors. Bor-ing. Over the last 31 years, it’s up more than 42,000%.

Many people assume that Clorox (CLX) is a brand that’s owned by some larger multinational. No so. Clorox owns Clorox. The company also owns Pine-Sol and Liquid-Plumr. Clorox was founded in 1913.

Cummins (CMI) is an engine company but it’s so much more. The company makes diesel and natural gas engines, plus electric and hybrid powertrains. It’s also engaged in filtration and power generation. Cummins employs more than 70,000 people around the world.

Donaldson (DCI) is a filtration company. It makes air filters for several different sectors. Another former Buy List stock.

Eaton (ETN) is a power management company that’s based in Dublin, Ireland. The company has been listed on the NYSE for 100 years. Only 32 companies have been listed that long.

Graco (GGG) makes fluid-handling systems. Snore. Over the last 30 years, it’s only up 20,000%.

Illinois Tool Works (ITW) “produces engineered fasteners and components, equipment and consumable systems, and specialty products.” Yes, it’s based in Illinois.

Public Storage (PSA) is the largest self-storage real estate investment trust (REIT) in the United States. There are currently more than 2,600 Public Storage locations around the world. PSA has relatively few employees. The lots are automated so customers can access their units at any time.

The company does a lot more than just provide the space. They also provide a broad range of services for their clients. PSA offers insurance and packing products. The company also had a subsidiary that provides boxes and truck rentals.

Sysco (SYY) is a major supplier to restaurants and dining facilities. The company has 600,000 clients.

WD-40 (WDFC) is like Clorox. Many people assume it’s a brand owned by a larger company. Nope, WD-40 is owned by WD-40.

Most every homeowner is familiar with WD-40. The lubricant spray is instantly recognizable by its yellow and blue label. Some folks at the firm were working on a Water Displacement formula. The first 39 tries failed, but #40 worked and the name was born.

Did you know WD-40 can soften leather? It can also clean tile and erase crayon. It can even unstick Legos.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

-

Morning News: October 3, 2023

Posted by Eddy Elfenbein on October 3rd, 2023 at 7:06 amOPEC+ Shows No Sign of Easing Oil Squeeze as Ministers Meet

US Supreme Court to Hear Case Targeting Consumer Financial Watchdog

The Fed Seeks to Up Its Influencer Status

Fed’s Mester Says One More Rate Hike May Be Needed This Year

Wall Street Thinks America’s Homes Are Overvalued

Americans’ Growing Reluctance to Quit Their Jobs, in Five Charts

A Plot to Oust the House Speaker Hits Weary Investors

‘Dumb Money’ Exposes the Baffling Allure of Bad Investment Advice

Can AI Beat the Market? Wall Street Is Desperate to Try

J.P. Morgan Growth Equity and Index Ventures Back Logistics Payment Platform Loop

Brookfield Raises $12 Billion for Flagship Private Equity Fund

Zoom’s Ex-CMO Will Now Pitch Hybrid Work as CEO of Video-Tech Firm Neat

Meta Explores Charge for Ad-Free Instagram and Facebook. Its Model Is Under Threat

From $26 Billion to Bust: Sam Bankman Fried’s Astonishing Rise and Fall

U.S. Car Sales Expected to Increase Again in the Third Quarter

China Is Suffering a Brain Drain. The U.S. Isn’t Exploiting It

A Rural Michigan Town Is the Latest Battleground in the U.S.-China Fight

China Evergrande Shares Soar as Trade Resumes Amid Police Probe

Key Taiwan Tech Firms Helping Huawei With China Chip Plants

Rare Look Inside TikTok Parent’s Finances Shows Slowing Revenue Growth

Tiger Woods-Backed Golf League Signs Sponsorship Deal with SoFi

Be sure to follow me on Twitter.

-

Morning News: October 2, 2023

Posted by Eddy Elfenbein on October 2nd, 2023 at 7:06 amDoes China’s Property Bust Make a Financial Crisis Inevitable?

China’s Precarious Economy Signals More Support Is Needed

BOJ to Buy Additional Bonds to Curb Rise in Sovereign Yields

Kenya’s Stock Market Becomes World’s Worst Performer

Why a US Recession Is Still Likely — and Coming Soon

Will Companies Keep Their Pandemic-Era Gains? It Depends

Higher Rates Starting to Hit US Profits, Goldman Strategists Warn

Wall Street’s Most Hated Regulator Faces a Fundamental Threat

Severe Crash Is Coming for US Office Properties, Investors Say

With Banks Offering 5% Returns, Financial Advisers Fight Irrelevance

Americans Are Still Spending Like There’s No Tomorrow

Why Consumers Are Mad About Inflation Even Though It Has Fallen

Birkenstock Attracts Norwegian Wealth Fund to $1.6 Billion IPO

Vaccine Breakthrough Behind Pfizer, Moderna Shots Wins Nobel

Aging Trees Show a Crisis Looms for the World’s Everything Oil

The Secret Behind the First $1 Billion Green Hydrogen Startup

Rivian’s Quest to Build the Ultimate Truck Burns Through Billions

Crypto Goes on Trial, as Sam Bankman-Fried Faces His Reckoning

Who’s Rooting Hardest for a Sam Bankman-Fried Conviction? The Crypto Industry

Airbnb Is Fundamentally Broken, Its CEO Says. He Plans to Fix It.

Peak TV Is Over. A Different Hollywood Is Coming

Longtime Union Leader Steps Fully Into Hollywood’s Spotlight

Be sure to follow me on Twitter.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His