-

Morning News: August 31, 2022

Posted by Eddy Elfenbein on August 31st, 2022 at 7:08 amEurozone Inflation Reaches 9.1 Percent, Driven by Prices for Energy and Food

Russia Halts Natural Gas Flows to Germany Again

Biden Still Undecided on Chinese Tariffs, Commerce Secretary Says

Powell Abandons Soft Landing Goal as He Seeks ‘Growth Recession’

Mortgage Demand Falls Even Further, as Rates Shoot Back Up to July Highs

US Life Expectancy Sees Biggest Two-Year Decline in a Century

This Remote Mine Could Foretell the Future of America’s Electric Car Industry

Some Carmakers Say Recycling Car Parts Is the Future. But Is It Realistic?

Choosing Your Own Hours Isn’t Just for Remote Workers Anymore

To Meet a New Generation, Legacy Black-Owned Businesses Get a Reboot

Fast-Food Operators Mobilize Against California Wage Bill

Bed Bath & Beyond Sinks After Saying It May Sell Shares

HP Warns of Slowing Business Spending as PC Sales Sag

Frustrations Mount at Washington Post as Its Business Struggles

Japan Declares ‘War’ on the Floppy Disk

Be sure to follow me on Twitter.

-

CWS Market Review – August 30, 2022

Posted by Eddy Elfenbein on August 30th, 2022 at 6:57 pm(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Holy Jackson!

In last week’s issue, I talked about how the impressive summer rally had finally faced some pushback. Until very recently, the bulls had been having a great summer.

We first got a little hiccup after the Federal Reserve released the minutes of its last meeting. Things got a lot worse on Friday when Fed Chairman Jerome Powell said we’re in for “more pain.”

Yikes! One must understand that central bankers simply don’t speak that way. Obfuscation is part of the job description. Alan Greenspan famously said, “I know you think you understand what you thought I said but I’m not sure you realize that what you heard is not what I meant.”

Powell’s words had an immediate impact, and the market gods were displeased. During the trading day on Friday, the Dow lost more than 1,000 points and the Nasdaq Composite dropped 4%. The market fell again on Monday and Tuesday. Since August 16, the S&P 500 has lost over 7%.

It’s about time the Fed acted boldly. To be perfectly honest, the central bank helped cause the inflation, and its predictions consistently understated the threat of higher prices.

Here’s the trend of the Fed’s projection for inflation in 2022:

Sep 2019: 2.0%

Dec 2019: 2.0%

Jun 2020: 1.7%

Sep 2020: 1.8%

Dec 2020: 1.9%

Mar 2021: 2.0%

Jun 2021: 2.1%

Sep 2021: 2.2%

Dec 2021: 2.6%

Mar 2022: 4.3%

Jun 2022: 5.2%The emergence of inflation was clearly visible one year ago, yet the Fed did nothing. The Fed currently projects inflation of 2.2% in 2024. Yeah, right.

“They Will Also Bring Some Pain”

Let me explain what Powell said and why it was so jarring to the market. First off, this wasn’t just any address. Powell was speaking at the Fed’s annual end-of-summer conference in Jackson Hole, Wyoming.

Since there’s no Fed meeting this month, the conference gets a lot of attention. In previous years, the Fed has used that Jackson Hole conference to announce major changes in policy.

The backdrop of this year’s meeting was a very impressive summer rally. In fact, as I mentioned in last week’s issue, the bulls finally faced some resistance only after the Fed released the minutes of its most recent meeting.

There’s also the all-important issue of persistent inflation. While there has been some improvement, mostly with energy, Americans are still facing rising costs for nearly everything.

Furthermore, there’s concern that the Fed may not realize the enormity of the job before them. I have to count myself among this group. It’s easy for the Fed to talk tough, but it’s quite another to act tough.

Here’s the broader text of what Powell said. I’ve added the boldface.

Restoring price stability will take some time and requires using our tools forcefully to bring demand and supply into better balance. Reducing inflation is likely to require a sustained period of below-tren growth. Moreover, there will very likely be some softening of labor market conditions. While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses. These are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain.

Powell was unambiguous that the Fed intends to defeat inflation. Powell said, “We will keep at it until we are confident the job is done.” That’s unusually blunt language for a central banker. The remarks were also unusually brief.

The Fed has already raised short-term interest rates by 0.75% at its last two meetings. Recently, however, some Fed members have expressed concern about the damage the economy has experienced. Just ask anyone you know who works in the housing sector.

There was some concern that the Fed might announce a “pivot” in Jackson Hole and plan on a softer interest-rate policy. Alas, the pivot never came.

Some Possible Softening of Inflation

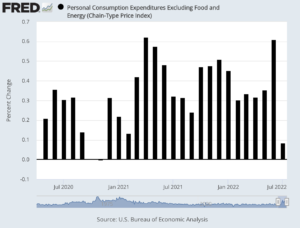

As it turns out, Friday was also the day that the government released its PCE inflation report. This is the Fed’s preferred measure of inflation. According to the PCE, inflation rose by 6.3% in the 12 months ending in July. That’s down from 6.8% for the 12 months ending in June. While inflation may be decelerating, it’s still high. The goal of 2% inflation is based on the PCE.

The core PCE rate, which excludes food and energy, is up 4.6% over the last year. During July, the core PCE rate increased by 0.1%. That’s a very big drop from the 0.6% increase we had in June. Powell said, “restoring price stability will likely require maintaining a restrictive policy stance for some time.”

Much of inflation is really an expectations game. If the public expects more inflation, then there will be more inflation. If the public expects inflation to wane, then it will wane. The problem is that once expectations become embedded in the public’s perception, then it’s very hard to undo that. That’s part of the reason why Powell is sounding so tough.

On Friday, Powell said, “The longer the current bout of high inflation continues, the greater the chance that expectations of higher inflation will become entrenched.” He also noted that the economy “continues to show strong underlying momentum” despite some mixed signals on growth.

This Friday, the government will release the official jobs report for the month of August. The last report showed the lowest unemployment rate in 53 years. Some folks had been expecting to see a drop off in the jobs market. So far, that hasn’t happened.

For Friday, the consensus on Wall Street is that the economy created 318,00 net new jobs last month and that the unemployment rate will hold steady at 3.5%. That sounds about right.

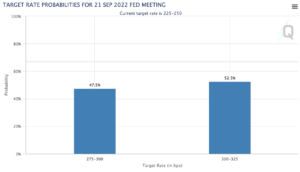

The Federal Reserve’s next meeting is on September 20-21. Previously, it had been a tossup in the market’s mind as to whether the Fed would raise interest rates by 50 basis points or by 75 basis points. However, after Powell’s comments, the 75-basis-point camp now has a solid majority among futures traders.

On Tuesday, we learned that jobs openings reached 11.24 million. That was much higher than expectations. That’s nearly two openings for every unemployed person. Economists also like to track the number of people who quit their jobs, and that’s still high. This probably suggests that workers have the upper hand in being able to demand higher wages since it’s relatively easy to find work elsewhere.

That’s all for now. The stock market will be closed on Monday for Labor Day. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want to learn more about the stocks on our Buy List, please sign up for our premium service. It’s $20 per month, or $200 per an entire year.

-

Morning News: August 30, 2022

Posted by Eddy Elfenbein on August 30th, 2022 at 7:06 amGermany’s Energy Bill Spirals as Uniper Seeks More Cash

China’s Biggest Developer Says Property Crisis Has Yet to Bottom

Lockdowns in China, and North Korea, Deal Double Blow to Bridge City

World Cup Fever Spreads From Qatar in Tourism Boom

Cryptoverse: Bleeding Bitcoin’s Holding Out for A Hero

Fed Plans 2023 Launch of Long-Anticipated Faster Payments System

Biden’s Student Loan Plan Sets Off Fierce Debate Among Economists

Bonds Are Sliding Toward the First Bear Market in a Generation

A Different Take on the U.S. Economy: Maybe It Isn’t Really Shrinking

The Bottom 50% of Americans Are Building Wealth Even as Inflation Bites

Would You Take Out a Loan to Buy This Week’s Groceries?

This Remote Mine Could Foretell the Future of America’s Electric Car Industry

FTC Sues Idaho Company for Selling Sensitive Tracking Data

Silicon Valley’s Elite Get Dragged Into Musk-Twitter Trial

Indian Billionaire Gautam Adani Is Now the World’s Third Richest Man

Be sure to follow me on Twitter.

-

Morning News: August 29, 2022

Posted by Eddy Elfenbein on August 29th, 2022 at 7:03 amXi Jinping’s Vision for Tech Self-Reliance in China Runs Into Reality

‘The Eye of the Storm’: Taiwan Is Caught in a Great Game Over Microchips

If Economists Fear Inflation, It’s a Sign You Should Not

‘Inflation Fever’ Is Finally Breaking — But Central Banks Won’t Stop Hiking Rates

Rally Hopes Crumble as Powell’s Rates Reality Hits Full Force

Dollar Zooms Higher as Markets Brace for Higher for Longer Rates

Some Companies Haven’t Paid a Dividend Since 2020. They Might Bring It Back as a Slowdown Looms

Asset Managers Renaming ESG Funds Told to Brace for Backlash

Revenge of the Founders: A Generational Struggle on Wall Street

Everyone’s a Landlord—Small-Time Investors Snap Up Out-of-State Properties

Everyone’s an Energy Trader as Power Bills Hit the Sky in the US

Honda, LG Set to Build $4.4 Billion EV Battery Plant in US

Ryan Cohen’s Bed Bath & Beyond Stock Sales Highlight Gray Area in Disclosure

NASA’s Artemis Launch Gives Boeing Chance to Restore Its Space Credibility

A Who’s Who of Silicon Valley Lawyers Up for the Musk-Twitter Trial

Be sure to follow me on Twitter.

-

Morning News: August 26, 2022

Posted by Eddy Elfenbein on August 26th, 2022 at 7:02 amThe World’s Rivers, Canals and Reservoirs Are Turning to Dust

China’s Record Drought Is Drying Rivers and Feeding Its Coal Habit

UK Energy Bills to Rise by 80% in October as Regulator Announces Hike

Underwhelming Iowa Corn Crop Sets Stage for More Food Inflation

The Crypto World Can’t Wait for ‘the Merge’

Crypto’s Real Value Was Never $3 Trillion

Fed Watchers Scrutinize Jackson Hole for Hints on Interest-Rate Outlook

Powell Is Not Likely to Tell Investors What They Want to Hear in Jackson Hole Speech

IRS Revenue Boost From Stronger Enforcement Is Scaled Back in CBO Estimate

Alibaba, JD.com, and Other China Stocks Rose on Potential Deal Ending U.S. Delisting Risk

How Elon Musk Plans to Kill Off Cellphone Dead Zones Across the US

California E.V. Mandate Finds a Receptive Auto Industry

Dollar Stores Report Higher Sales as Shoppers Seek Inflation Relief

Gap Posts Surprise Profit on Banana Republic Boost; Withdraws Forecasts

Peloton Slides as Bleak Forecast Douses Hopes of Quick Turnaround

Ford Trucks in $1.7 Billion Verdict Weren’t Subject to Tougher Safety Rules

Be sure to follow me on Twitter.

-

Morning News: August 25, 2022

Posted by Eddy Elfenbein on August 25th, 2022 at 7:03 amEnergy Crisis Squeezes Smaller Firms That Power Europe’s Economy

A Sick Economy Is Forcing Tehran’s Hand in Nuclear Deal Talks

US Shale Could Erase Debt by 2024, Freeing Up Cash for Gas Pivot

Pace of Climate Change Sends Economists Back to Drawing Board

At the Fed’s Big Conference, Investors Will Grasp for Hints About Rate Path

Jackson Hole Should Be a Mea Culpa for Central Bankers

Biden’s Student-Loan Relief Adds New Wrinkle to Inflation Debate

What You Need to Know About Biden’s Student Loan Forgiveness Plan

US Housing Market in ‘Much Worse Shape’ Than Fed Admits

The Rocky Road of Running an Ice Cream Truck This Summer

Tesla Split Will Struggle to Feed $280 Billion Rally

Amazon Is Shutting Down Its Telehealth Service, Amazon Care

Peloton’s Quarterly Loss Tops $1.2 Billion

The Slow Death of the Traditional Business Card

When Your Boss Is Crying, but You’re the One Being Laid Off

The Backlash Against Quiet Quitting Is Getting Loud

Be sure to follow me on Twitter.

-

Morning News: August 24, 2022

Posted by Eddy Elfenbein on August 24th, 2022 at 7:04 amBritain’s Labor Shortage Is Helping Drive Its Inflation Problem

Derby’s Take: Economists See Powell Quashing Hopes for Rate Cuts Over Long Term

Fed’s Kashkari Says No Time To Back Off On Inflation Struggle

Offshore Tax Loophole Helps Rich Americans Cheat IRS, Senate Says

I.R.S. Undertakes a Security Review Amid Threats to the Agency and Its Employees

Larry Summers Defends Stance That Student Loan Debt Relief Is Inflationary

The Surprise in a Faltering Economy: Laid-Off Workers Quickly Find Jobs

A ‘Tsunami of Shutoffs’: 20 Million US Homes Are Behind on Energy Bills

Goldman Says Hedge Funds Back Betting Big on Megacap Tech Stocks

First-Time Buyers Show More Demand for Mortgages, Even as Interest Rates Rise

Twitter’s Former Security Chief Accuses It of ‘Misleading’ Public on Security Practices

Federal Trade Commission Drops Mark Zuckerberg From Antitrust Lawsuit

Bed Bath & Beyond Clinches Loan Deal

Indian Billionaire Makes Hostile Bid for High-Profile NDTV News Channel

We Need to Talk About How Good A.I. Is Getting

Be sure to follow me on Twitter.

-

CWS Market Review – August 23, 2022

Posted by Eddy Elfenbein on August 23rd, 2022 at 6:07 pm(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

The Great Summer Rally Stalls

The Great Summer Rally of 2022 has finally faced some pushback. On Friday, the S&P 500 fell by 1.29%. Under normal circumstances, that’s not much of a big drop, but considering this summer, it’s noticeable. That was the index’s largest drop since late June.

For more than two months, the bulls were partying, and no bears were in sight. The market increased in value by a cool $7 trillion. The S&P 500 was on pace for one of its best quarters in decades. At one point, the S&P 500 had its best start to a Q3 in 90 years!

Until this point, the market treated every minor dip as a chance to buy. Not this time. The selling pressure continued into Monday as the S&P 500 fell 2.14%. Again, that’s nothing huge, but it stands out in a market that had been so placid. The Nasdaq Composite fell by 2.55% on Monday. The market closed lower on Tuesday as well. In the last week, the S&P 500 has lost a little over 4%.

By the way, that can be a key sign of a change in the market, when a downside move is followed by an even larger downside move. The stock market tends to be very trend sensitive. In other words, whatever the market’s doing, the odds are that it will continue doing it. These trends often play out larger than you think possible.

That means the keys are the turning points. Unfortunately, you can never know the difference between some minor pushback and a true change in sentiment. The same holds true for now. I’ll note in passing that the market got the willies at nearly the precise point that it bumped up against its 200-day moving average (the bluish line in the chart above). I tend to be a skeptic on these technical indicators, but a lot of people think they’re very important, which in turn, makes them important.

What led the summer rally to stall? That’s hard to say, but I’d say it’s a round of the usual suspects. The top of which is the Federal Reserve. The market may be treating last week’s Fed minutes with some new-found respect.

In the minutes, the Fed made it clear that it intends to keep raising rates until inflation is soundly put back in its box, but there had been some doubters. It’s easy and cheap for the Fed to sound tough, but it’s quite another thing to deliver. We even saw in the futures market some expectations that the Fed might start cutting rates during the first half of next year.

The event looming over the market is Fed Chairman Jerome Powell’s speech at Jackson Hole scheduled for this Friday. At the moment, the market is in a tug of war over what will happen with interest rates next month. One moment, expectations are for a 0.50% hike. Then they’re for a 0.75% hike. Then they’re back to 0.50%. Right now, 0.75% has a slight lead. Powell’s speech may clear things up.

The National Association for Business Economists recently ran a survey of business economists. It found that 52% of respondents said they were “not very confident” in the Fed’s efforts to fight inflation.

I doubt the recent downtick had anything to do with earnings. We have nearly the final numbers for Q2 and it was a decent earnings season. Earnings are up a little over 9% compared with a year ago, which is basically in line with inflation. As of today, 76.1% of companies beat on earnings, 71.3% beat on sales and 59.5% beat on both.

Apple Goes to the Bond Market

There’s some interesting news this week from Apple (AAPL). In a filing with the SEC, the computer giant said it’s going to issue long-term bonds and use the proceeds to pay out dividends and buy back its own stock.

In plainer terms, Apple is borrowing money to invest in itself. That’s not a bad idea if you can borrow for less than what you’re investing in. Right now, Apple pays a tiny dividend yield of 0.55%.

However, I think this move by Apple raises some important questions. The first is, should a company be involved in financial engineering? Some investors, including myself, believe a company should be solely focused on making money. What to do with that money should be left to the owners—the shareholders. I see moves like this as management encroaching on an area that’s not their concern. Unfortunately the government’s shifting tax policy has played a role in determining what companies do with their profits.

This isn’t just a buyback; Apple is borrowing money to fund the buyback. That raises another issue, what if Apple is paying too much for itself? Cisco famously lost billions of dollars investing in its inflated stock. A cash dividend to shareholders gives them the option to buy more or to invest their funds elsewhere.

What’s also interesting about this offering is that the bonds have a maturity of 7 to 40 years. According to Bloomberg, the offering is for $5.5 billion, and the bonds yield 118 points over similarly-dated Treasuries. The initial discussions were for a premium of 150 basis points, meaning there was unexpected demand for the bonds.

In December, Moody’s (MCO), a Buy List favorite, raised its long-term rating on Apple to AAA. That’s a huge deal. That’s roughly Wall Street’s equivalent of being a “made man” in the mafia. No one can touch you. Microsoft (MSFT) and Johnson & Johnson (JNJ) are the only other current members of the AAA club. If Wall Street thinks you’re on the same level as a sovereign government, perhaps you should have a similar debt load? Eh, I’m not so sure.

Apple is sitting on nearly $180 billion in cash. Four years ago, Apple had a cash position of $285 billion. There was a time when Apple had enough cash to buy every single team in the NFL, NBA, NHL and MLB.

Apple could also be taking advantage of lower interest rates. There’s been a surprising recovery in the bond market. During July, the yield on the 10-year Treasury fell by 33 basis points. That was the largest decline in yields in over two years.

Perhaps Apple sees inflation continuing to be a problem. One of the major issues with inflation is that it benefits borrowers at the expense of lenders. If the Fed is going to continue hiking rates, this offering could be quite remunerative for Apple.

This move also sends a positive message from Apple to the market that it plans to buy its stock for many years to come. Also, if Apple does something, then it gives cover for other boards of directors to do the same thing.

Barron’s Features Broadridge Financial Solutions

In our premium service, we’ve been doing well lately with Broadridge Financial Solutions (BR). The shares are up 30% in a little over two months. This is an interesting stock that should be better known.

We recently got a nice bump in Broadridge after the company released a very good earnings report. I was especially pleased to see that Barron’s recently featured the stock: “Broadridge Notches Steady Growth in Uncertain Times.” I won’t give away the whole thing, but here’s a sample:

Broadridge has been a steady stock for rocky times. That is thanks to a model heavy on recurring-revenue businesses and exposure to long-term trends that should remain in place no matter the near-term path of the economy or interest rates. Broadridge stock’s recent rally could cap gains in the near term, but the company’s long-term positive trajectory remains intact.

The company has a near monopoly in the business of managing and distributing investor communications for practically every public company in the U.S., plus mutual funds, exchange-traded funds, and more. That includes proxies, regulatory disclosures, and other reports and filings required of all U.S. securities issuers. Those are non-discretionary communications that companies and funds need to distribute no matter what the world is doing. That segment tends to grow at the pace of overall stockholdings in the U.S., with Broadridge able to eke out higher profit margins thanks to a continuing shift from printed documents delivered by mail to digital investor communications.

Broadridge also has a smaller but faster-growing segment focused on back-office functions for asset managers, investment banks and broker-dealers. Those include trade processing and settlement, record-keeping, and a variety of other compliance or regulatory functions. That is a software-as-a-service business that has expanded through a combination of organic growth and Broadridge buying companies with adjacent or complementary software and services.

For the fiscal year that ended in June, Broadridge earned $6.46 per share. That’s up 14% from last year. The company said it sees further growth of 7% to 11% for the current fiscal year. That works out to an earnings range of $6.91 to $7.17 per share.

The company also hiked its dividend for the 16th year in a row. For nine of the last 10 years, BR has increased its dividend by 10% or more.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want to learn more about stocks like Broadridge, please sign up for our premium service. It’s $20 per month, or $200 per an entire year.

-

Morning News: August 23, 2022

Posted by Eddy Elfenbein on August 23rd, 2022 at 7:03 amUS Life Expectancy Dropped in 2020 by Most Since WWII, CDC Says

Oil Climbs as Tight Supply Moves Back Into Focus

Expansion of Clean Energy Loans Is ‘Sleeping Giant’ of Climate Bill

Supply-Chain Bottlenecks Shift to East and Gulf Coast Ports

Wall Street CEOs Warn Recession Is Likely — Even As Their Own Economists Waffle

Stocks Can Rally Out of Jackson Hole, Strategists Say

SoftBank’s Epic Losses Reveal Masayoshi Son’s Broken Business Model

Companies Face Challenges Determining Impact of New Minimum Tax

Credit Suisse Is Reassigning Bankers as Part of Focus on Wealth

Apple’s New iPhone 14 to Show India Closing Tech Gap With China

Phone Companies Want to Be Your Home-Internet Provider—and Vice Versa

Zoom Is Struggling to Convince Consumers to Pay, and the Stock Is Sliding

Quiet Quitting is the Latest Workplace Trend, but it Doesn’t Mean What You Think

Harvard’s Status as Wealthiest School Faces Oil-Rich Contender in the University of Texas

Musk’s Lawyers Seek Documents From Former Twitter Chief Dorsey

Be sure to follow me on Twitter.

-

Morning News: August 22, 2022

Posted by Eddy Elfenbein on August 22nd, 2022 at 7:04 amDrought Hurts China’s Economy as Central Bank Cuts Rates

China Plans $29 Billion in Special Loans to Troubled Developers

Pandemic Bolsters China’s Position as the World’s Manufacturer

A Supplier of Rare Earth Metals Turns to Greenland in Bid to Cut Reliance on Russia

Europe’s Natural-Gas Crunch Sparks Global Battle for Tankers

Expansion of Clean Energy Loans Is ‘Sleeping Giant’ of Climate Bill

Wall Street Bears Take Revenge After a $7 Trillion Rally

The $80 Billion IRS Infusion Means More Audits—in 2026 or 2027

Credit Suisse Investment Bankers Are Bracing for Brutal Cutbacks

Big Banks Expected to Rack Up More Than $1 Billion in Fines for WhatsApp Use

Despite What You’re Told, Banks Do Not ‘Create Money’

You Can Get a $7,500 Tax Credit to Buy an Electric Car, but It’s Really Complicated

Big Five Airline? How a Combined JetBlue and Spirit Could Compete

Amazon Among Bidders for Signify Health

How Pharmacy Work Stopped Being So Great

Some Colleges Don’t Produce Big Earners. Are They Worth It?

Be sure to follow me on Twitter.

- Load More

Gotta hear both sides.

"Model from California killed, castrated, cooked and then ate her husband"I apologize for my last tweet. I should not have said Alderaan "had it coming" and they "got what they deserved." Some of my best friends are Alderaanian. I'm learning. I'm growing.

You can do very well by betting on the big winners before they became the big winners.

-

-

Archives

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His