Archive for December, 2013

-

Morning News: December 18, 2013

Eddy Elfenbein, December 18th, 2013 at 7:13 amU.K. Unemployment Unexpectedly Falls to Four-Year Low

Bitcoin Price Halves as China Clampdown Escalates

Merkel Urges EU Treaty Change in First Speech of New Term

Fed Said to Delay Bank Leverage Cap Until Basel Completed

Fed Faces Tough Call on Bond Buying as Economy Strengthens

Gold Climbs in London Before Fed’s Decision: Palladium Advances

Consumer Prices Stay Nearly Flat

Insurers Wary of New Obamacare Fix for January Health Plans

Herbalife Investors Win Battle

BP Flags Gulf of Mexico Find, $1.08 Billion Brazil Writedown

William Morris Said to Have Won Auction for IMG, Sports and Talent Agency

Shopping Marathons Coming: Stores Open 100+ Hours in a Row Before Christmas

Credit Writedowns: Are Equity Markets in a Massive Bubble?

Cullen Roche: Updating Warren Buffett’s Favorite Valuation Metric

Be sure to follow me on Twitter.

-

Fiserv Splits 2 for 1

Eddy Elfenbein, December 17th, 2013 at 9:06 amFiserv ($FISV) split its stock 2 for 1 this morning. The new Buy Below is $56 per share.

For tracking purposes, I assume our Buy List is a $1 million portfolio that’s equally weighted at the start of the year. For this year’s Buy List, the “buy price,” meaning the price as of the close of 2012, on Fiserv drops from $79.03 per share to $39.515 per share. The number of shares in our tracking portfolio doubles from 632.6711 to 1,265.3422 (hence to give us a $50,000 position at the beginning of the year).

-

Technological Miracles Will Keep Generating Profits and Jobs

Eddy Elfenbein, December 17th, 2013 at 7:24 amOver the weekend, I booked a pair of airline tickets from Seattle to south Florida – over 3,300 miles – for under $330, round trip, or just five cents per mile. I used the Internet to shop among competing airlines, dates, times and warm-weather transfer points. It’s tempting to complain about TSA delays, bad food and tight seating, but I appreciate these cheap, long flights – fruits of our reasonably free market in air travel.

This brings to mind an event 110 years ago this morning. At 10:30 am on December 17, 1903, two Dayton bicycle mechanics flipped a coin to see who got the first chance to fly like a bird on the beach of Kitty Hawk, North Carolina. Shortly thereafter, Orville Wright took a short (and VERY slow) flight, for a man, while creating a giant leap for mankind. He “flew” (a few feet above the sand) 40 yards in 12 seconds. That works out to 10 feet per second, or less than seven miles per hour – slower than your average jogger.

Wilbur and Orville made a total of four flights that day in 1903. The longest jaunt covered 852 feet in 60 seconds, ending in a nose dive. That’s less than 10 miles per hour. Even the lightest of today’s planes would stall at under 10 miles per hour, but the Wrights’ 605-pound bird was not much heavier than air.

For nearly five years, few believed the Wrights, because nearly everyone else failed in flight and the Wrights kept their invention under wraps, fearing patent infringement. Finally, in the summer of 1908, in France, Wilbur flew his plane 40 miles in 90 minutes, or 27 miles per hour. This flight was astounding to its viewers, but no more astounding than a half dozen other technological innovations from 1901 to 1905.

Planes, Cars, Radio and Other Innovations Took Time to Mature

America is particularly suited to invention, especially at that time in our history. In 1900, most guys had access to a shop or a tool barn, and most loved to tinker, looking for better, easier and cheaper ways to get a job done. America had a system of patents that encouraged innovation. The Wright brothers were bicycle makers first, tinkerers second. Henry Ford was a mechanic with Edison Electric in the 1890s, but he was also a nocturnal tinkerer. He spent nights reading manuals about the new internal combustion engine. Ford asked for a loan in 1903, but the president of the Michigan Savings Bank told him that “the horse is here to stay, but the automobile is a novelty.” Ford failed often, but Ford Motor finally opened.

When Ford started making cars, Detroit had a speed limit of 8 miles per hour, and fines of $100 – two months’ wages – for a first infraction, so Ford’s cars and Wright’s planes were incredibly slow at first.

Innovation does not directly lead to profitable commercial applications, but innovation is vital for the continuation of long-term economic growth. Airplanes didn’t become useful or profitable until World War I forced plane makers to develop a series of technological innovations, improving speed and safety.

You can see the same delayed payoff in other early 20th Century technologies. Ford Motor incorporated in 1903, but Ford’s continuous assembly line did not emerge until 1913. Guglielmo Marconi sent the first transatlantic radio broadcast on December 12, 1901, but radio did not captivate the public until the 1920s.

In 1904, the diesel engine debuted in St. Louis. In 1905, Einstein developed the theory of relativity and several other insights, but they were not proven true until 1919 or later. For the most part, the major inventions of 1901 to 1905 did not reach the consciousness of the general public until the 1920s.

Likewise, many of the greatest breakthroughs of the 1950s and 1960s – like Xeroxing, faxing or color TV transmission – were developed in the late 1930s, but it took decades to reach commercial viability.

Ben Bernanke’s Most Important 2013 Speech was Not about QE or Tapering

Federal Reserve Chairman Ben Bernanke has taken a lot of heat for his expansive policies over the last eight years, but last May he said something far more important than anything he said before Congress or during some FOMC meeting. Four days before he introduced “tapering” last May 22, Bernanke give a commencement address at Bard College. His subject was technology, and he referred back to the time of the Wright Brothers and Henry Ford, saying that innovation didn’t die with Edison, Ford or the Wrights.

Bernanke told Bard graduates and their families that “the modern industrial era, which lasted from the mid-1800s well into the years after World War II….featured multiple innovations that radically changed everyday life, such as indoor plumbing, the harnessing of electricity for use in homes and factories, the internal combustion engine, antibiotics, powered flight, telephones, radio, television, and many more.” The result, he said, is that our output per person increased by about 30 times between 1700 and 1970.

Bernanke concluded his talk by saying that “pessimists may be paying too little attention to the strength of the underlying economic and social forces that generate innovation in the modern world…. Moreover, because of the Internet and other advances in communications, collaboration and the exchange of ideas take place at high speed and with little regard for geographic distance…. [T]he economic rewards for being first with an innovative product or process are growing rapidly. In short, both humanity’s capacity to innovate and the incentives to innovate are greater today than at any other time in history.”

Other academic experts echo Bernanke’s optimism. In a September BusinessWeek survey (“Is Innovation Leading to a New Age of Productivity in the U.S.?”), we hear from Chad Syverson, an economics professor at the University of Chicago, who has charted the cycle of productivity in the development of technology, citing the many “lags between the introduction of new technologies and productivity gains.” MIT Management Professor Erik Brynjolfsson agrees, saying: “In my papers, we found that companies that installed big, new enterprise information systems didn’t get the full benefits for five to seven years.”

Technology is vital to create future profits, but any new technology may take several years to generate profits. A Bloomberg BusinessWeek chart shows that productivity gains run in cycles. From this 50-year chart, we can see sharp declines in 1972, 1982 and 1992, followed by significant productivity booms.

Here’s a safe prediction: We don’t know what the world will look like in 50 years, but the most important innovations are probably taking shape now, in the form of the 50th or 100th failure in some university or corporate laboratory, or in some tinkerer’s garage. Creativity did not die with Steve Jobs. What we once considered wildly innovative – like phones with cameras or a talking GPS in your car – are considered normal now. What’s next? Bitcoins you can trust? 3-D imaging for something more beautiful than guns (violins, perhaps), delivered in 30 minutes by an Amazon drone? Or how about a hyper-loop bullet car taking you 300 miles in 30 minutes? Or a trip to space, orbiting the earth or shooting off to the moon?

We have no idea what tomorrow will bring, but somebody, somewhere, is inventing tomorrow today.

– Gary Alexander

-

FactSet Research Earns $1.22 Per Share

Eddy Elfenbein, December 17th, 2013 at 7:19 amFactSet Research Systems ($FDS) just reported fiscal Q1 earnings of $1.22 per share. That’s an increase of 10% over last year’s Q1. Three months ago, FDS gave us an earnings range of $1.21 – $1.24 per share, so they’re hitting their internal objectives. Technically, this was below Wall Street’s estimate of $1.24 per share.

“Our investment discipline and proven business model continues to generate shareholder value as illustrated by our 10% adjusted EPS growth. Our buy-side client base is experiencing a healthy business cycle, but we are facing a challenging sell-side environment, which reduced organic ASV,” says Philip Hadley, Chairman and CEO. “As we continue to generate record levels of quarterly free cash flow, I’m pleased to announce a $300 million expansion to our existing share repurchase program. We also completed the acquisition of Revere Data in September and acquired a 60% ownership interest in Matrix Data Limited in December 2013.“

Here are some details: Cash flow for the quarter rose 18% to $53 million. The key number to watch in FactSet’s earnings is Annual Subscription Value, or ASV. Last quarter, ASV rose 5% to $890 million. Of that $890 million, $609 million was domestic and $281 million was foreign. FactSet bought back 530,000 shares last quarter for $57.8 million. These are good numbers.

Now for Q2 guidance. FactSet revenues ranging between $225 million and $228 million. They see earnings coming in between $1.20 and $1.23. FactSet added that the ending of a tax credit for R&D should take a three-cent bite out of earnings. Wall Street’s consensus was for $1.25 per share. Overall, this was a solid quarter for FDS.

-

Morning News: December 17, 2013

Eddy Elfenbein, December 17th, 2013 at 7:03 amGermany to Propose Bundesbank Deputy for ECB Board Seat

German Investor Sentiment Hits Seven-year High in December

Turkish Police Detain High-Profile Figures in Probe Into Alleged Bribery

The Luxembourg Tax Break That Helps Firms Profit From Loss

Should Investors Trim Positions in Banks as Rate Hike Looks Imminent?

Dollar 1% From 5-Year High Versus Yen on Taper Bets; Krona Falls

Fed’s $4 Trillion Assets Draw Lawmaker Ire Amid Bubble Concern

S.E.C. Calls for Stiff Penalties Against Tourre

First Volcker Victim? Zions Dumping Its Hedge Funds

Will AIG’s $5.4 Billion ILFC Sale Lift Shares?

GlaxoSmithKline to Spend $1 Billion to Raise Stake in Indian Pharma Unit

Boeing Will Shovel Billions Of Dollars In Cash Back To Its Investors

Herbalife Clean Audit a Setback for Ackman’s Pyramid Case

Howard Lindzon: How to Move a Stock – by Carl Icahn

Joshua Brown: Sundown at the Permabear Alamo/a>

Be sure to follow me on Twitter.

-

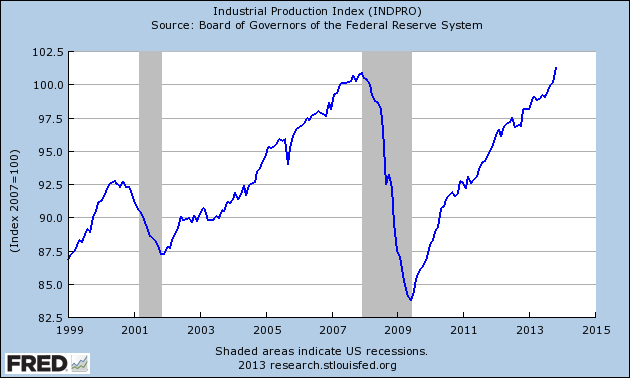

Industrial Prodcution Hits All-Time High

Eddy Elfenbein, December 16th, 2013 at 9:31 amStill more good economic news. The Industrial Production data series had been one of the major series that had failed to top its pre-Recession high. That came to an end today.

Industrial Production for November jumped 1.1% which is the largest rise in a year. It also edged out the reading from December 2007 to hit a new all-time high.

-

Morning News: December 16, 2013

Eddy Elfenbein, December 16th, 2013 at 6:58 amEuro-Area Manufacturing Grows More Than Forecast on Germany

Germany Will Decide Quickly on New ECB Executive

‘Abenomics’ Gets Thumbs Up: Japan Business Mood at Six-year High

China Manufacturing Index Unexpectedly Drops on Output

November WPI at 14-Month High: Case For RBI Rate Hike Strengthened, Say Analysts

Global Bitcoin Conference Calls for Reserve Bank of India Recognition

Fed Taper Message Succeeds With Bonds Adjusting to Economic Data

Inflation Still Low as Wholesale Prices Fall for 3rd-straight Month

Amazon’s German Workers to Protest in Seattle

AIG Plans to Sell Aircraft Leasing Unit to AerCap for $5 Billion

Carrefour to Buy Shopping Malls in $2.8 Billion Deal

NPR Gets $17 Million in Grants to Expand Coverage and Develop Digital Platform

Beyonce Rejects Tradition for Social Media’s Power

Roger Nusbaum: Why Doesn’t the Dividend Growth ETF Grow Its Dividends?

Jeff Miller: Weighing the Week Ahead: A Turning Point for the Fed?

Be sure to follow me on Twitter.

-

Peter Lynch Talks With Charlie Rose

Eddy Elfenbein, December 14th, 2013 at 2:55 pm -

How the Financial System Works

Eddy Elfenbein, December 13th, 2013 at 4:04 pm -

CWS Market Review – December 13, 2013

Eddy Elfenbein, December 13th, 2013 at 7:06 am“You don’t have to be brilliant, only a little bit wiser than the

other guys, on average, for a long, long time.” – Charlie MungerDespite a strong 2013, the stock market seems to be limping into the end of the year. On Thursday, the S&P 500 dipped down to its lowest level in nearly a month. The index has lost ground on eight of the last ten days, and we’re on track for our worst weekly performance in the last 15 weeks.

Of course, since volatility is so low, the overall loss ain’t that much (see the chart below). This is a minor pullback at best. The S&P 500 is currently less than 1.8% below its all-time high close. That’s right folks, we’ve dropped all the way back to those grim and hopeless days of early November. Naturally, some folks are already calling this the beginning of a new bear market. Please: We’re trading at less than 14.5 times next year’s earnings, and estimates have been moving higher.

Before we get into this week’s issue, I want to remind you that I’ll be unveiling the 2014 Buy List in next week’s issue. As usual, I’m adding five new names to the Buy List, and I’m deleting five names. The Buy List always stays at 20 stocks.

The new Buy List takes effect on January 2nd, the first day of trading of the new year, and it’s locked and sealed for the entire year. I can’t make any changes. For tracking purposes, I assume the Buy List is a $1 million portfolio, equally divided among the 20 stocks. Whenever I mention how well (or poorly) our Buy List is doing, that’s what I’m referring to. And don’t forget that you can always see how well we’re doing by visiting the Buy List page of our website.

In this week’s issue, I want to look at more encouraging economic signs. There’s a very good chance that 2014 will be the strongest year for economic growth in quite some time. Will stocks follow? Well, that’s another matter. We’ll also take a look at upcoming earnings reports from FactSet Research Systems and Oracle. I also want to update a few other Buy List stocks. But first, let’s take a closer look at why the economy is looking up.

The Balance Sheet Recession Is Finally Over

One of the big turning points we’ve seen recently is that economic news has improved considerably. I still wouldn’t say that the economy is strong, but we’re a lot better than where we were. The key is that many of the risks that plagued us have slowly melted away. Even our hopelessly dysfunctional Congress seems to have gotten its act together and reached a deal to avert yet another government shutdown. I’ve also been pleased to see things look better in Europe. It was the euro crisis that weighed heavily on U.S. stocks in 2011 and 2012.

While a lot of people have been calling the stock market a bubble, I think we’ve witnessed very much the opposite. Namely, the tremendous fear bubble has deflated. It was only two years ago that the S&P 500 hit its lowest P/E Ratio in over two decades.

Another area where we can see the dissipation of fear is in the credit markets. Bond traders are paid to worry about things, and they’re having a harder time of it. Bespoke Investment Group pointed out that high-yield spreads are at a six-year low, which is a clear sign of optimism. When lenders are afraid, they pull back, and when credit markets freeze up, the whole economy is in trouble. That’s not what’s going on right now.

Things are also looking good for consumers. David Rosenberg, who’s been a long-time bear, has defected to Camp Bull. He noted that the Fed’s recent Beige Book referred to wage pressures 26 times. Folks are also hitting the stores. Retail sales for November rose 0.7%, and the October figure was revised upward to 0.6%. That’s good news for Buy List retailers like Ross Stores ($ROST) and Bed Bath & Beyond ($BBBY).

Consumers have also been getting their finances in order. Cullen Roche, who’s one of the most astute writers on the economy today, recently declared an end to the “balance sheet recession.” For the first time in several years, households are adding on debt. I realize that may sound like something bad, but in econo-speak, it’s actually good news. More household debt is what needs to happen during an expansion. The long trend of paying down debt was a necessary and painful obstacle for the economy. It’s come to an end.

Even Uncle Sam’s finances are getting better. The U.S. budget deficit, while still massive, is much less massive than it was a few years ago. The deficit for this year will probably be about 3% of GDP, which is down from 10% in 2009. Also, cost-cutting at the local government level (what some people call “austerity”) is largely over.

I’ve also noted that the spread between the 2- and 10-year Treasuries is widening, which is a classic forward-looking indicator for the economy. In fact, it’s one of the most reliable macro indicators around. What’s particularly interesting is that the yield on the two-year has been fairly stable, while the 10-year has been rising. The 2-10 spread is near the highest it’s been in more than two years. This is a particularly good omen for Buy List financial stocks like Wells Fargo ($WFC) and JPMorgan Chase ($JPM). Remember that a bank is basically the yield curve with incorporation papers. Now let’s take a look at some upcoming earnings reports.

FactSet Research Systems Is a Steady Winner

Three of our Buy List stocks have reporting quarters that end in November, and two of them, Oracle and FactSet Research Systems, will report earnings next week. FactSet ($FDS) is due to release its fiscal Q1 earnings report on Tuesday, December 17th, and Oracle follows the next day with its fiscal Q2 earnings report. The third stock, Bed Bath & Beyond, won’t report its earnings until January 8.

Let’s start with FactSet, which has been a solid performer for us this year. The stock, which makes software that tracks all the geeky financial data that Wall Street loves to play around with, is up 30% this year. Six months ago, FactSet merely “met” Wall Street’s consensus, and you can probably guess what happened. Traders panicked. The stock dropped. We sat and watched. After a bit, the stock quietly rallied to a new high. That’s our game, and we play it well.

Then three months ago, FactSet had an earnings “miss.” Well, technically it was a miss, since it was one whole penny below Wall Street’s consensus—never mind that it was well within FactSet’s own guidance for the quarter. But because it was a miss, the shares dropped. Like clockwork, the stock settled down and again quietly rallied to another all-time high. FDS came close to making another new high yesterday, even though the broader market was retreating.

Now let’s get into some numbers. When looking at FactSet, the important metric to watch is ASV, which is annual subscription value. The ASV for last quarter rose by 6%, which is a good number. For the upcoming earnings report, FactSet said they expect to see revenues between $222 and $225 million and earnings between $1.21 and $1.24 per share. That’s strong growth. For comparison, FDS earned $1.11 in last year’s fiscal Q1.

Here’s the bottom line: Business is going well for FactSet. It’s still early, but I think the company can churn out $5 per share this fiscal year (which ends in August). This is a steady winner. FactSet remains a very good buy up to $119 per share.

Oracle Is a Buy up to $36 per Share

Oracle ($ORCL) is due to report its earnings on Wednesday, December 18. On Monday, ORCL hit a nine-month high, but it suddenly got chopped down later this week. On Thursday, two Wall Street firms, Morgan Stanley and RBC, downgraded Oracle. Both analysts think the valuation is too high, which I think is nuts. But one of the analysts cited concerns about cloud computing, which I think is a valid concern but probably overstated.

I have to admit that Oracle had been frustrating us for much of this year. It’s by far our worst-performing stock on the Buy List. Their new software sales, in particular, have been disappointing. But I’ve learned to never count Larry Ellison out. If there’s one lesson I’ve learned in life, it’s that businessmen who own their own Hawaiian island probably know what they’re doing. Just a rule of thumb there.

Oracle’s last earnings report was pretty good. Whenever I look at an earnings report, I like to dig into see the numbers below the surface. One key metric is free cash flow, and for Oracle that was a cool $6 billion last quarter, and about half of that went to share buybacks. Actually, the earnings would have been even better this time if it weren’t for those meddling currency effects. I was also pleased to see Oracle double its dividend in June. That’s always a strong sign of confidence from management.

Three months ago, Oracle told us to expect Q2 earnings to range between 64 and 69 cents per share. They should be able to top that, but I’m curious to see what guidance they’ll offer for fiscal Q3. I suspect Oracle enjoys low-balling Wall Street. For this fiscal year, I think Oracle has a chance to earn as much as $3 per share, which means the stock is going for about 11 times forward earnings. That’s a good deal. Don’t let this week’s downdraft rattle you. Oracle is a good buy up to $36 per share.

Buy List Updates

Now here are a few updates to some of our other Buy List stocks. This week, AFLAC ($AFL), our favorite duck stock, gave a presentation at a Goldman Sachs conference. One of things I like about AFLAC, besides its being very well run, is that it’s a fairly transparent company. They’re up front about what’s going on, which is frustratingly rare. Supplemental health insurance can be rather opaque, but AFLAC tries to bring some clarity. If you remember, when the stock dropped over concerns about its European investments, management kept investors in the loop.

While I like AFLAC a lot, it’s no secret what one of their major problems is: Bond yields around the world are pitifully low, and that’s not fun if you’re running a $100 billion fixed-income portfolio. At the Goldman conference, the company explained that they want to diversify their portfolio outside of Japanese government bonds. They even hired a top manager away from Goldman to run their portfolio. AFLAC said they want to start buying other assets, including more U.S. corporate debt. I think this is a smart move. The company has strong cash flow, so they have to keep plowing that coin back into suitable fixed income. Right now, AFLAC is going for about 10 times next year’s earnings. My take: It’s a solid buy up to $70 per share.

A few months ago, there was some mindless chatter that Google ($GOOG) was about to buy the very lucrative NFL Sunday ticket away from DirecTV. Suddenly, everybody thought that football was going to be broadcast over YouTube. Oh brother. At the time, I said this was complete nonsense. The truth is that the NFL is very happy with DTV, and vice versa. Of course whenever a contract is up, you want to hear offers from other parties. What’s the word for that? Oh right, business.

Sure enough, the latest word is that DTV and the NFL are close to reaching a deal to keep the NFL Sunday Ticket at DirecTV. The Sunday Ticket has two million subscribers, and the package starts at $49.99 per month. On Thursday, shares of DirecTV gapped up to a new all-time high. DirecTV is a buy up to $70 per share.

Ford Motor ($F) continues to be a bargain hidden in plain sight. The company has impressive plans for the future. Ford said they’re hiring 11,000 new people next year, 5,000 in the U.S. and 6,000 in Asia. This will be the most people they’ve hired since 2000. Ford plans to introduce 23 new vehicles next year, 16 of which will be in the U.S. The stock is now going for less than nine times next year’s estimate. I rate Ford a buy up to $18 per share.

Finally Fiserv ($FISV) splits 2 for 1 next Tuesday. Don’t be surprised when you see the lower share price. The stock remains a buy up to $112 per share, and post-split, the Buy Below will be $56 per share. This is a good stock.

That’s all for now. Next week is the last full trading week of the year. We’ll get earnings reports from FactSet on Tuesday and Oracle on Wednesday. The Fed meets on Tuesday and Wednesday, and Bernanke will hold his last post-meeting press conference, but I doubt we’ll see a taper announcement. Next week, we’ll also get an important report on Industrial Production, plus we’ll see another revision to Q3 GDP. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

P.S. Here’s a segment I did earlier this week on CNBC’s “Fast Money.”

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His