Archive for December, 2013

-

Morning News: December 13, 2013

Eddy Elfenbein, December 13th, 2013 at 7:03 amIreland’s Tough Economic Policies ‘To Continue’, Says Finance Minister

Goldman Sachs Goes Against Consensus in Dollar Call

Ukraine Riots Flash Buy Signal to Foreigners as Bonds Scooped Up

Indian Court Lifts Obstacle to Microsoft-Nokia Merger

Stronger U.S. Retail Sales Point to Spending Rebound

Retailers Extending Black Friday Deals Amid Lukewarm Demand

With $25 Million Bet, Silicon Valley Officially Claims Bitcoin as Its Own

A Surprise From Hilton: Big Profit for Blackstone

Peugeot Shares Fall as General Motors Sells Its Shareholding

Dan Akerson: The CEO Who Took GM From the Wake of Bankruptcy to Profitability

Instagram Introduces Private Messaging

JPMorgan Said to Near $2 Billion Settlement of Madoff Probes

Cisco Cuts Long-term Revenue, Earnings Targets

Credit Writedowns: What Do Negative Interest Rates Do?

Why Buyouts Are Stalled in the Middle Market

Be sure to follow me on Twitter.

-

Rosenberg: “a better U.S. economy is at hand”

Eddy Elfenbein, December 12th, 2013 at 10:10 amDavid Rosenberg, who has been a long-time bear, has shifted his stance and now sees reasons for optimism:

With this in mind, the most fascinating statistic this past week was not ISM or nonfarm payrolls, but the number of times the Beige Book commented on wage pressures: 26. That’s not insignificant. Again, when I talked about this at the Thursday night dinner, eyeballs rolled.

There was much discussion about the lacklustre holiday shopping season thus far, with November sales below plan. There was little talk, however, about auto sales hitting a seven-year high in November even with lower incentives. And what’s a greater commitment to the economy — a car or a cardigan?

As I sifted through the Beige Book to see which areas of the economy were posting upward wage pressure and growing skilled labour shortages, I could see it cut a large swath: technology, construction, transportation services, restaurants, durable goods manufacturing.

Of the 115 million people currently working in the private sector, roughly 40 million of them are going to be reaping some benefits in the form of a higher stipend and that is 35% of the jobs pie right there.

That isn’t everyone, but it is certainly enough of a critical mass to spin the dial for higher income growth (and spending) in the coming year. Macro surprises are destined to be on the high side — take it from a former bear who knows how to identify stormy clouds.

-

The Santa Claus Rally Season Is About To Begin

Eddy Elfenbein, December 12th, 2013 at 8:23 amWe’re getting close to what is historically the best time of the year for stocks.

I took all of the historical data for the Dow Jones from 1896 through 2010 and found that the streak from December 22nd to January 6th is the best time of the year for stocks. (December 21st and January 7th have also been positive days for the market but only by a tiny bit.)

Over the 16-day run from December 22nd to January 6th, the Dow has gained an average of 3.23%. That’s 41% of the Dow’s average annual gain of 7.87% occurring over less than 5% of the year. (It’s really even less than 5% since the market is always closed on December 25th and January 1st. The Santa Claus Stretch has made up just 3.8% of all trading days.)

Here’s a look at the Dow’s average performance in December and January (December 21st is based at 100):

You should note how small the vertical axis is. Ultimately, we’re not talking about a very large move.

-

Morning News: December 12, 2013

Eddy Elfenbein, December 12th, 2013 at 6:57 amEuro Zone Industrial Output Unexpectedly Falls in October

Draghi Builds Stress-Test Credibility in ECB Bank Review

Hardships Linger for a Mending Ireland

Mexico Lower House Passes Oil Overhaul to End State Monopoly

Fischer Seen Bringing Crisis-Fighting Skills to No. 2 Fed Post

Foreclosures Drop to Eight-Year Low as Crisis Wanes

IATA Boosts Profit Forecast 10% But Warns Returns Still Weak

Blackstone’s Hilton Raises $2.35 Billion in Record Hotel IPO

Korea Aerospace Seals $1.1 Billion Jet Deal

Peugeot Shares Sink 10% on Capital Hike Worries

Snapchat Confirms $50 Million Investment

Criminal Action Is Expected for JPMorgan in Madoff Case

Cullen Roche: Some Thoughts on Economic and Market Forecasting

Howard Lindzon: Google and Goldman Sachs…The Enteroctopus and The Vampire Squid

Be sure to follow me on Twitter.

-

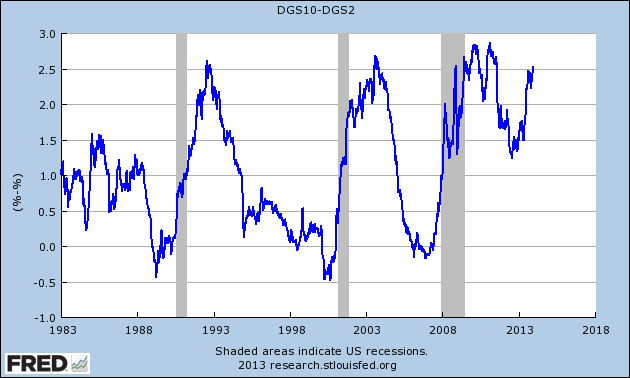

Some Guy on TV

Eddy Elfenbein, December 11th, 2013 at 6:53 pmYep, that was me on CNBC’s Fast Money talking about the 2-10 spread. Here’s the 2-10 Spread going back 30 years. Notice how it turns negative before each recession (the shaded parts). It’s got a great track record, and it’s been more bullish lately.

Eddy: It’s looking good for the economy. A lot of people on Wall Street are paid a lot of money to predict the economy and a lot of them don’t have very good track records. One of the best is one of the cheapest, and that is the difference between the 2 and the 10. And it’s been going up over the last few weeks and it’s now at a two-year high.

Josh Brown: Eddy, I see in the chart that you’re showing that we kind of had a false start toward the end of 2010, and we actually know how that’s worked out for momentum stocks and cyclicals ever since then. Is there anything in your reading of this or elsewhere that could tell you that “this time is different” from the false start in 2010 when we were all faked out?

Eddy: Absolutely. I think there are two good confirmations. One is the ISM report for November which was also a two-year high. It is the exact same time frame as the 2-10 spread. Another one is that if we look at the relative strength of the Cyclical Index, the CYC, that is also at a two-year high. It’s confirming these trends almost perfectly.

Melissa Lee: Were you surprised, actually, that you had these other two indicators also confirm this trend given that the Fed has essentially been manipulating the yield curve for so long?

Eddy: The difference is what we saw earlier in this year when the 2-10 spread got wider, but it was a different underlying trend driving it: the middle part of the yield curve is what was driving it, and that was the fear of taper. This time it’s very different because the middle part really hasn’t moved much at all. In fact, the two-year part is lower than where it was on Labor Day. The real driver of the growing steepness of the spread has been on the ten-year. And that’s driven up so that we’re about 260 basis points wide right now.

-

Morning News: December 11, 2013

Eddy Elfenbein, December 11th, 2013 at 7:34 amEU States Move Toward Clash With Parliament on Bank Plan

Yen Rises From Six-Month Low as Asian Stocks Fall; Aussie Slides

The Volcker Rule Is Tough. It’s Complicated. Will It Be Effective?

Time to Take the Bitcoin Bubble Seriously

Costco Profit Misses Estimates

Advice for GM’s CEO Mary Barra

Lloyds Fined £28 Million For ‘Serious Failings’ in Sales Practices

GE Capital to Pay $34 Million to Credit Card Customers

Zara Parent Inditex’s Profit Edges Higher

Twitter Rises Most Since IPO on Advertising Product Optimism

What Exactly is Imgur, and Why is Yahoo Trying to Buy It?

Joshua Brown: The Wizard of Oz Was About the Gold Standard

Roger Nusbaum: Yahoo Finance: Could You Be Oversaving for Retirement?

Be sure to follow me on Twitter.

-

Investing Isn’t Rocket Science

– No, It’s Harder than That!

Eddy Elfenbein, December 10th, 2013 at 5:23 pmOn December 10, 1896, Alfred Nobel died. He left a lot of money for scientific prizes named after him. In honor of his death date, the Nobel Prize ceremony is usually held on this day, December 10. The first ceremony was in 1901 when the first Nobel Peace Prize was awarded to the Swiss founder of the Red Cross, Jean Henri Durant. The 1901 Physics prize went to Wilhelm Roentgen for the “remarkable rays” named after him. The 1903 Physics prize went to Pierre Curie and Marie Curie – the first female winner.

Three “hard” sciences have been awarded Nobel Prizes since 1901, namely physics, chemistry and physiology or medicine. The softer, more subjective awards are for Literature and Peace. Since 1968, the Nobel commission has added the “Nobel Memorial Prize in Economic Sciences,” but the question facing us today is whether economics is more of a hard science, like Physics, or a creative art, like Literature.

Since the days of John Maynard Keynes, economists have tried to turn their profession into a science, using calculus to create complex mathematical models, which they call “econometrics.” Alas, in the end, as Alan Greenspan unburdened himself in his recent tome, “The Map and the Territory,” economics is more about our “animal spirits” – greed, fear and mob behavior – than bloodless mathematical models.

That brings us to the three winners of the 2013 Nobel Prize for Economics. Each won the big prize for his work in how to apply mathematical models to asset values – like stock prices. The problem is that all three came to strikingly different conclusions. In Physics, this would be like Albert Einstein and Neils Bohr (the 1921 and 1922 winners) having divergent opinions about how gravity works, or the speed of light.

Meet the 2013 Nobel Prize Winners – Eugene Fama, Robert Shiller and Lars Hansen

Here are the Nobel Prize winners and their divergent views.

Eugene Francis Fama, age 74, is Professor of Finance at the University of Chicago. He is often called the father of the “efficient market” hypothesis which stemmed from his doctoral thesis. He is best known for using exhaustive market databases to formulate theoretical and empirical (real life) portfolio decisions.

Robert James Shiller, 67, often appears on CNBC in connection with his famous housing index, as well as his market predictions. He is currently Professor of Economics at Yale, after holding key positions in the National Bureau of Economic Research and the American Economic Association. He is also co-founder and chief economist for an investment management firm, MacroMarkets LLC. Unlike Fama, Shiller is noted for pointing out market inefficiencies and price anomalies within the major markets.

Lars Peter Hansen, 61, is perhaps lesser known to investors than the other two. Like Fama, he teaches at the University of Chicago as the David Rockefeller Distinguished Service Professor of Economics. He is best known for his studies on the interface between the financial and the “real” sectors of the economy.

All three plow the same field – asset valuation – but they emerge with different answers. Fama says that most markets are “informationally efficient,” since most investors revalue prices almost instantaneously to reflect any new information. In shorthand, the news is rapidly reflected, or baked into, the market price.

Shiller doesn’t think investors are that smart or rational. Investors are subject to animal spirits, prisoners of their human nature and subject to mob psychology. Shiller proved in the 1980s that stock prices move in much wider swings than their underlying dividends, which are far more predictable than stock prices.

A famous case in point is Shiller’s book, “Irrational Exuberance,” which was first published in March of 2000, the exact month of the peak in NASDAQ and S&P 500. In his 2005 update to that book, Shiller added a section on how overvalued the U.S. housing market had become. He showed that housing was a case of greed fueled by unrealistic previous price increases. His predictions were once again right on the money, as real estate prices soon peaked and began to fall precipitously over the next few years, as reflected in the housing index that Shiller pioneered – now called the S&P Case-Shiller home price index.

The tie-breaker in this argument comes from Lars Hansen, who studies the causes of market volatility. He seems to lean more toward Shiller’s view, that the wide variations in asset prices within a short time cannot be caused by slight changes in valuation measures. Such swings are not explainable by normal valuation models, so Hansen focuses on those “moments” of change, when investors vacillate from manic to depressive. This seems to be the origin of the recent fixation with the terms “risk on” and “risk off.”

While Shiller and Hansen seem to dispute Fama’s conclusions, Fama has won the allegiance of armies of index fund managers, who deny the value of individual stock selection in favor of exchange-traded funds (ETFs) and various index funds, which try to reflect the movement of indexes by constantly rejiggering the funds’ contents to reflect the market capitalization of each stock in the index, thereby exacerbating the size of the market’s swings, as index fund managers are forced to chase the “hottest” stocks in the index.

Successful Investing Differs from Econometric Modelling

My father was a rocket scientist, of sorts. During my college years (1963-67), he was a Boeing engineer and project manager in Huntsville, Alabama, and New Orleans, helping build the Saturn booster rockets. In retirement, dad applied his scientific skills to the stock market. He kept elaborate graphs of each stock he followed – by price, dividend, P/E and other ratios. It was all very mathematical, but his track record was unsatisfactory, so he asked for my advice. Looking at all his charts, I said, “Dad, investing isn’t like rocket science. It’s harder than that.” He wasn’t sure if had lost my marbles, so I explained: “Investing involves real people making emotional decisions, usually bad decisions. In rocket science, you can project a missile into space with known variables, with almost exact precision. With investing, you have to work with human beings. The numbers have some limited value, but they won’t be able to predict stock prices.”

Justin Fox’s 2009 book, “The Myth of the Rational Market” covered how physicists from the Los Alamos National Laboratory launched the Santa Fe Institute, which attempted to apply chaos theory to markets. Fox wrote: “Physicists struggled with the reality that sentient beings are harder to work with than, say, subatomic particles.” One physicist, J. Doyne Farmer, said economics is “a harder field than physics.”

In my 30+ years of working with financial newsletter editors, I’ve run into many former engineers who became investment advisors, lured by the fascination of seeking scientific formulas for profits. These advisors became successful, but only by accounting for investor sentiment and other emotional elements.

Prices will always swing in wide arcs – due to human excesses, not just logic. That fact will always give investors a chance to beat the markets. After all, it’s almost un-American to strive to be just “average.”

– Gary Alexander

Navellier Market Mail -

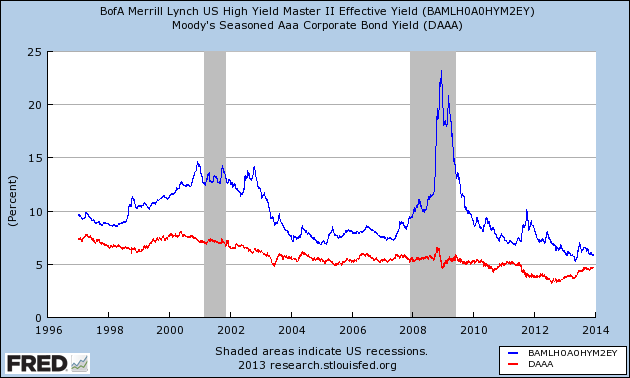

The Amazing Decline of Risk

Eddy Elfenbein, December 10th, 2013 at 3:10 pmOne of the points I’ve tried to make this year is that financial markets are up, not so much due to a bubble in expectations, but rather it’s been the result of a tremendous fear bubble deflating. Valuations aren’t extreme. They’ve gone from low to somewhat moderate.

We can see another good example by looking at credit spreads. Here’s the yield of a Junk Bond Index (the blue line) compared with AAA Bonds (the red line).

Notice how the spread between the two has narrowed considerably. When markets get nervous, the marginal borrower gets elbowed aside. Well, in 2008, he didn’t just get elbowed — he got a super-atomic wedgie. The world was collapsing and no one wanted to make any junk loans.

The problem is that wider credit yields, in turn, hurt the economy. But as credit markets chill out, those spreads narrow. This reflects the fact that lenders now have more confidence in lending. The downside of this is the lenders can become sloppy and gradually ignore real risks, like we saw during the credit bubble. I’m not saying we’re there yet, but that’s the conventional undoing of tight spreads.

Notice how the problems in Europe caused a big spike in Junk Yields in late 2011. That was an unusual time for investors because financial markets greatly over-reacted to the actual risks at hand. Of course, their skittishness was understandable given what happen only three years before. It’s the unwinding of this fear bubble that’s driven a lot of our gains this year.

-

Banks Rally on the Volcker Rule

Eddy Elfenbein, December 10th, 2013 at 11:15 amAs many of you know, I live in Washington, DC and as much as I love this city, it’s notoriously ill-prepared to deal with snow. Even a little sends us into a panic. If the Soviets had only known! We’re getting a modest dusting of snow, and the place is almost completely shutdown.

The S&P 500 closed at an all-time high yesterday and we’re down just a tad so far this morning. One area of strength is big banks. The government unveiled the “Volcker Rule” today, named after the former Fed chairman. The rule limits what banks are allowed to trade under their own accounts.

The belief behind the rule is that it’s highly unstable for the economy if banks can take depositors money, which is insured, and start gambling with it. It’s taken a long time for regulators to come up with the precise wording of the rule. The rally in bank stocks is because the regulations aren’t as onerous as feared.

Shares of JPMorgan ($JPM) got above $57 earlier today, and Wells Fargo ($WFC) is over $44, and close to a new 52-week high.

Investor’s Business Daily profiles DirecTV ($DTV) ahead of their investor day on Thursday. What’s impressed me about DTV is how they’ve been able to reduce share count with their buybacks. Over the last seven years, the number of outstanding shares is down 57%.

While the company has certainly done well, there are concerns about its subscriber growth in Latin America, especially in Brazil. While any business issues may impact the bottom line, it seems that DTV will plow ahead with their generous stock repurchase plan. The company has also been able to raise prices to offset slower subscriber growth.

-

Morning News: December 10, 2013

Eddy Elfenbein, December 10th, 2013 at 7:07 amCarney Pushes Guidance Message as He Warns Against Early Exit

Pakistan to Push Forward on Gas Project With Iran

Narendra Modi could be India’s Shinzo Abe

General Motors Sees China-like Take-off in Indonesian Car Market

Regulators Expected to Vote on Volcker Rule Despite Snowstorm

Fannie (FNMA) and Freddie (FMCC) Tip Into the Red

GM Bailout Ends as U.S. Sells Last of ‘Government Motors’

U.S. Household Worth Rose by $1.92 Trillion in Third Quarter

For Natural Adversary of the Bargaining Table, Labor Holds a Banquet

Sysco and US Foods Agree to Merge, Creating a World-Class Foodservice Company

Cerberus May Offer Divestment in Firearms

Lululemon Founder Steps Down as Chairman

Paul Krugman: Bitcoin’s Value Is Driven By The Fact That It Sounds Impressive

Cullen Roche: The Balance Sheet Recession is Over

John Hempton: Interoil: Both Longs and Shorts Look Like Fools

Be sure to follow me on Twitter.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His