Archive for September, 2015

-

Relative Strength of Tobacco Stocks

Eddy Elfenbein, September 14th, 2015 at 1:02 pmHere’s a fascinating chart I made this morning. This shows the S&P tobacco stocks divided by the S&P 500. In other words, when the line is rising, tobacco stocks are outperforming. When it’s falling, they’re trailing.

First, notice how well tobacco stocks have done. They’ve outperformed the market over the last 25 years. In fact, this chart may understate their performance since the dividend yields of tobacco stocks tend to be higher than the overall market.

As we know, boring stocks in boring industries can be wonderful investments. If there’s any stock to avoid, it’s the hottest stock in the hottest sector.

Also, notice the periods of tobacco underperformance. Tobacco badly lagged the market from late-1998 until early 2000 (the Tobacco Master Settlement Agreement was signed in November 1998). This was an echo of the market’s tremendous bubble. Tech stocks gained so much that other stocks were forced to underperform.

Remember: A bubble isn’t stocks going from 15 times to 18 times earnings. It’s stocks going way, way, WAY out of proportion to everything and thereby distorting all valuations. That’s what happened during the tech bubble. Once the bubble deflated, tobacco stocks returned to normal.

Tobacco again outperformed in 2008. That was investors running to safety as the world was falling apart. Defensive stocks are great for rough economic times. This sector has been great for buy-and-hold investors.

-

The Fed Countdown Begins

Eddy Elfenbein, September 14th, 2015 at 10:54 amWelcome to Fed week! This week’s trading will naturally be dominated by news of whatever the Fed decides to do this Thursday. There seems to be a consensus that the Fed will stand pat. I was surprised to see that Bill McBride, the talent behind Calculated Risk, say that he thinks the Fed will raise rates. So the consensus isn’t universal.

One difference with this rate hike is that it probably won’t be the start of a rate hike cycle like we saw before the crisis when the Fed hiked rates at 17 consecutive meetings. In recent years, several central banks have raised rates only to cut them again. In fact, just about the only central banks that haven’t raised rates at all are the Fed and the Bank of England, and we’ve both had some of the best recoveries. I think there’s a very good chance that we’ll get one or two rate hikes followed by a long pause.

In the WSJ, Harriet Torry and Jon Hilsenrath point out that there’s still a gap between the Fed’s long-run view and that of investors. In June, the Fed’s “blue dots” saw rates at 1.625% at the end of next year, and at 2.875% by the end of 2017. But the futures market for Fed funds sees those rates at 1% and 1.5%. When in doubt, I side with the market’s view. This week, we’ll get another view of the Fed’s projections.

-

Morning News: September 14, 2015

Eddy Elfenbein, September 14th, 2015 at 7:11 amChina Stocks’ Worst Day in Nearly Three Weeks After Punishments

China Seizes Up to $157 Billion of Unspent Local Government Budgets

OPEC Cuts Forecast of Oil Supplies From Nonmembers in 2015

Fed to Dominate Week of Central Bank Meetings

Solera to Be Acquired by Vista Equity Affiliate in $6.5 Billion Deal Including Debt

Alibaba Disputes Barron’s Bearish Cover

Baidu’s Li Says Investors Don’t Get China’s Coming Internet Boom

TV Bundles Challenge Apple to Make a Deal

Fiat Chrysler CEO Cancels Auto Show Appearance to Assist With Labor Talks

Airbus Guns for Boeing With New Factory in Its Home Market

DuPont to Face First Trial Over C-8 Exposure

Was Tom Hayes Running the Biggest Financial Conspiracy in History?

Which Fed Leaders Fear Inflation? Look at When They Grew Up

Jeff Miller: To Hike or Not to Hike?

Joshua Brown: The 2.5 Million Year Bull Market in Humanity

Be sure to follow me on Twitter.

-

Down, Up, Down, Up, Down, Up, Down, Up, Down, Up

Eddy Elfenbein, September 13th, 2015 at 2:05 amFor the last ten weeks, the S&P 500 has alternated between down and up weeks.

According to Ryan Detrick, if we’re down next week, that would tie a record.

-

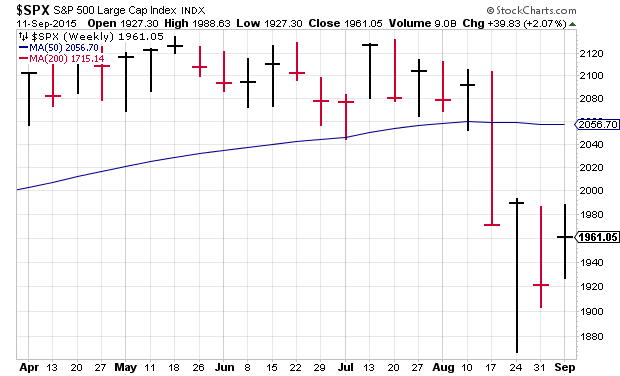

CWS Market Review – September 11, 2015

Eddy Elfenbein, September 11th, 2015 at 7:08 am“Preventing liquidation of an unbalanced market will leave you in tears.”

– Ben BernankeNext week is the big FOMC meeting, and there’s a chance that the Federal Reserve will raise interest rates for the first time in nine years.

Wall Street is completely obsessed with this issue. Frankly, I’m conflicted on even discussing it with you. Whatever the Fed does next week is truly not very important to us as investors. Yet I feel the need to at least touch on the subject since it’s dominating the news on Wall Street. Plus, as the decision day gets closer, we still don’t know exactly what the Fed will do.

In this week’s CWS Market Review, I’ll take a closer look at the issues confronting the Federal Reserve. For now, Wall Street seems to doubt that a rate hike is coming, but not by much. The more important issue is that the bond market is still calm, and the broader economy is improving. Later on, I’ll preview one of our Buy List earnings reports coming next week. Our Buy List has outpaced the market in five of the last six days. I’ll also update you on some of our other Buy List stocks. But first, let’s see what’s in store for the Fed as they get together next week in Washington.

The Fed Will Probably Do Nothing Next Week

We have a slight clue as to what the Federal Reserve will do from keeping an eye on the futures pits. Traders there buy and sell contracts on just about everything, and that includes the Fed funds rate. By looking at the prices on those futures, we can make out what the market thinks the Federal Reserve will do. (You can see for yourself at this page run by the CME.)

One month ago, China shocked the financial world by devaluing its yuan. That was their biggest deval in two decades. It’s not exactly a secret that the PRC keeps its currency artificially low in order to make its exports cheaper on the world market. Naturally, the Communists love money just like everybody else. It’s not that your currency needs to be cheap; it’s that it needs to be cheaper than everybody else’s. So the fear was that this devaluation could set off a deval frenzy as other countries raced to the bottom.

Scary, but not likely. Still, that devaluation was the first domino to fall. Soon, the mighty Kazakh tenge plunged by 22%. Other currencies followed. Then Asian equity markets buckled, and soon enough, our markets dropped as well.

Are those fears overblown? Sure. As big as China is, all the revenues from that country account for a rounding error for the S&P 500. In fact, the figure is probably less than the 2% number you often hear once you exclude semiconductors and other tech products which are sent to China to be re-exported elsewhere. China, I’m afraid to say, just isn’t that important to us yet.

Before China’s surprise devaluation, futures traders thought there was a 60% chance the Fed would start raising rates at its meeting scheduled for September 16-17. Since then, that figure has dropped to about 26%.

Jon Hilsenrath, the WSJ reporter who’s often considered to be the Fed’s major media conduit, recently said that the central bank is not in agreement on what to do. I would think that the Fed would want to show a unified front, considering it’s the first rate increase since 2006. When Hilsenrath writes “senior Fed officials” in one of his stories, you can be sure they’re very senior Fed officials. It’s his story from Wednesday that has me thinking the Fed will hold off on any rate increase.

The monetary doves, those who are against raising rates, say that inflation is nowhere to be seen. Commodity prices are down. This Labor Day weekend, a gallon of gas was 99 cents lower than it was last year. While the jobs numbers are good, workers haven’t seen much in the way of higher wages. It’s hard to make an argument that the economy is overheating. If I were on the Fed (and I have not been asked, at least not yet), I would vote against raising interest rates. I’m not ardent in this belief. It just seems too early.

The hawks, those who want higher rates, have points to make as well. The jobs situation has improved dramatically from a few years ago. The last jobs report has the unemployment rate at 5.1%. That’s the lowest in more than seven years. The unemployment rate is lower now than it was at any time from May 1974 to March 1997, except for one month in 1989. The initial jobless claims report has been below 300,000 for 27 weeks in a row.

The hawks also say that you can’t wait for inflation to show up before you raise rates—you need to strike before inflation appears. So far this year, core inflation, which excludes food and energy, is running at 2.2%. Next week, we’ll get the CPI report for August. The headline inflation, which includes everything, hasn’t hit the Fed’s target of 2% in more than three years.

The other problem for the Fed is that the world is heading in one direction (lower rates, more stimulus) while the Fed is paring back. In Europe, Mario Draghi is trying to run Ben Bernanke’s playbook. So far, it’s been a flop. In China, the government is going out of its way to prop up its delicately-managed financial markets. The mismatch between the U.S. and the rest of the world is part of the reason for the recent turbulence.

The good news is that the stock market has started to relax a bit. Still, I’ve said I won’t give the “all clear” sign until the VIX closes below 20. On Thursday, the VIX closed at 24.37 which is a three-week low.

Remember how calm things were? Less than two months ago, the WSJ said, “It’s Official: This Is the Most Boring Stock Market in Decades.” Or as I wrote so eloquently in June, “This market’s just dull, dull, dull.” Through this past Tuesday, the S&P 500 had seven 2% moves in just 13 days. In the 167 days prior to that, we only had one 2% move.

Looking past the September meeting, futures traders think there’s a 60% chance of a rate hike in December. In fact, that may be the compromise reached at next week’s meeting. Here’s the point I think many investors are missing: interest rates will still be low after a Fed hike. In fact, real short-term rates will most likely be negative for another 18 months, and probably longer.

There’s no guarantee, but low real rates has been one of the backdrops for bull markets. One rate hike is not a killer for stocks or the economy. The problem comes when rates get too high. Until that happens, the broad outlook for stocks is quite good.

Oracle’s Fiscal Q1 Earnings Preview

Next week, Oracle (ORCL) is due to report fiscal Q1 earnings on Wednesday, September 18, after the closing bell. This is one of our two Buy List stocks with August-ending quarters. The other is Bed, Bath & Beyond (BBBY), which isn’t scheduled to report until September 24.

Three months ago, Oracle had a lousy earnings report. The company was clearly a victim of the strong dollar. Oracle’s quarterly revenues fell by 5%, but they said that if it hadn’t been for the strong dollar, quarterly revenues would have risen by 3%. The company told us to expect Q4 earnings to range between 90 and 96 cents per share. As it turned out, Oracle wasn’t even close—they earned just 78 cents per share. While the strong dollar caused a lot of damage, that wasn’t all. Oracle’s software sales fell 6%. The company loves to tell us how well its cloud business is doing but that’s not very big.

For Q1, Oracle said it expects earnings between 56 and 59 cents per share. That’s pretty weak, and Wall Street expects even worse. The current consensus is at 52 cents per share. It’s interesting that the Street is going below the company’s public guidance. That’s not a sign of faith.

Since the last earnings report, the stock has been a disaster. Shares of Oracle nearly broke below $35 a few weeks ago. Oracle is now going for 13.6 times last fiscal year’s earnings. By most conventional metrics, Oracle is a good bargain, but there needs to be some good news to get investors excited again. I’m also curious how long Oracle will continue with two CEOs. With a lower share price, the company may want to prove that it’s moving forward with greater direction. I’m still a fan of Oracle, and I’m sure the dollar headwinds are tough, but I want to see better numbers here soon. This week, I’m lowering my Buy Below on Oracle to $40 per share.

Buy List Updates

Since the stock market broke down in August, I’ve been hesitant to lower our Buy Below prices. The market is still in flux, and I don’t want investors to be swung back and forth. As always, our strategy is to be patient and wait for bargains.

This week, I want to lower the Buy Belows for eBay (EBAY) and PayPal (PYPL). I gave both somewhat elevated Buy Below prices because I knew there would be heavy demand going into the spinoff. Unfortunately, both stocks have been punished recently. Just this week, eBay was downgraded by Cantor Fitzgerald from buy to hold. I’m going to lower the Buy Below by $2 per share for both stocks. eBay is now a buy up to $28 per share, and PayPal is a buy up to $38 per share.

Express Scripts (ESRX) announced this week that its CEO, George Paz, will be retiring in May. He’s been a great leader for the company and I’m sad to see him go. ESRX’s current president, Tim Wentworth, will succeed Paz as CEO. Wentworth came on board three years ago when ESRX bought Medco Health Solutions. I expect another good earnings report next month. Express Scripts is a buy up to $92 per share.

That’s all for now. The big news next week will be the FOMC meeting. The Fed will meet on Wednesday and Thursday, September 16-17. The meeting will be accompanied by an update on the Fed’s economic projections. I should warn you that the Fed has a pretty bad track record at this. The meeting will be followed by a press conference from Fed Chairwoman Janet Yellen. The rate decision should come at 2 p.m. on Thursday. On Tuesday, we’ll get reports on retail sales and industrial products. Then on Wednesday, the CPI report for August comes out. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: September 11, 2015

Eddy Elfenbein, September 11th, 2015 at 7:03 amPork Prices Drive Up Inflation in China

As a Boom Fades, Brazilians Wonder How It All Went Wrong

Oil Production in US, Russia Seen Tumbling Due to Price Drop

How Low Can Oil Go? Goldman Says $20 a Barrel Is a Possibility

U.S. 10-Year Bond Yield Closes at One-Month High

Risk Reversal in Stocks as S&P 500 Volatility Passes Small Caps

Treasury’s Lew Says U.S. Can Still Borrow Through Late October

U.S. Jobless Claims Drop; Imported Inflation Remains Weak

Krispy Kreme’s Signature Sweet Treats Coming to Peru

Aerojet Bids About $2 Billion for Boeing-Lockheed Rocket Venture

GE Seeks Sale of Asset Management Arm Amid Industrial Push

Wal-Mart’s Suppliers Are Finally Fighting Back

Inquiry’s Trail: From George Washington Bridge to United’s Executive Offices

Joshua Brown: Rates Traders Unconvinced of September Liftoff

Howard Lindzon: Investing is Hard…And Why Everyone Should Invest… The Definitive Post

Be sure to follow me on Twitter.

-

Torchmark Since 1988

Eddy Elfenbein, September 10th, 2015 at 12:06 pmHere’s another in my long-run series, “boring stocks that have done amazingly well yet no one knows about.” This time, I’m featuring Torchmark (TMK). Here’s a description from Hoover’s:

Torchmark aims to be a beacon in the world of insurance. It is the holding company for a family of firms; its member companies specialize in lower-end individual life insurance and supplemental health insurance. Torchmark subsidiaries, which include flagship Liberty National Life, offer whole and term life insurance, supplemental health insurance, accidental death insurance, Medicare supplements, and long-term care health policies for the elderly. Its American Income Life sells life insurance policies to labor union and credit union members in the US, Canada, and New Zealand. Torchmark sells its products through direct marketing, as well as a network of exclusive and independent agents.

Sexy, right? Now check out the chart:

That’s a stellar record. Let me add that while I like Stockcharts, I’m not sure if their long-term charts are 100% accurate. Still, this seems to be reasonably close. In 1998, Torchmark spun-off Waddell & Reed Financial (WDR) which has also beaten the market.

Despite their great growth, Torchmark still isn’t terribly large. Their market cap is about $7 billion. They’re in the S&P 500, but their market cap is around 440th. I also like that Torchmark has an incredibly stable earnings line.

-

Express Scripts CEO George Paz to Retire

Eddy Elfenbein, September 10th, 2015 at 10:28 amYesterday, Express Scripts (ESRX) announced that its CEO, George Paz, will retire in May. The company’s president, Tim Wentworth, will replace him.

Wall Street is familiar with Wentworth, and the executive is “well positioned” for the industry’s challenges due to his experience with both specialty drugs and in sales, BMO Capital Markets analyst Jennifer Lynch said in a research note.

Leerink analyst David Larsen said in a separate note that Paz’s retirement announcement came earlier than expected, but Wentworth is “well suited” to lead the company.

“In our view the CEO change increases the likelihood that (Express Scripts) will consider a large strategic deal, and we believe investors will view this leadership change announcement favorably,” Larsen wrote.

Paz has done an excellent job running ESRX. He’ll still be there as non-exec Chairman. The stock initially rose but has now slipped back into the red. I assume traders are guessing whether the company has a greater likelihood of being bought out under Wentworth.

-

Morning News: September 10, 2015

Eddy Elfenbein, September 10th, 2015 at 7:07 amBOE Unruffled by China, Markets Turmoil

What’s Behind The Big Declines In China’s PPI

China’s Response to Stock Plunge Rattles Traders

Justice Department Sets Sights on Wall Street Executives

Even Harvard B-School Alums Are Fretting Over Income Inequality

Dell Says To Invest $125 Billion in China Over Five Years

Netflix to Launch in Singapore, South Korea, Hong Kong and Taiwan

Alibaba Plays Down Worries of Hit on Consumer Spending as China Slows

The U.S. Economy Is Just Starting to Tap Into a Big Source of Dry Powder

Mondelez to Boost Ad Spending, Healthier Offerings

The Rail Executive United Airlines Tapped to Lift Its Fortunes

Tesla P90D Review: Elon Musk Wants Your Sedan to Be Ludicrously Fun

Joshua Brown: Rates Traders Unconvinced of September Liftoff

Jeff Carter: Credentials, Who Needs ‘Em?

Be sure to follow me on Twitter.

-

Hilsenrath: Fed Not In Agreement on Rates

Eddy Elfenbein, September 9th, 2015 at 10:50 pmJon Hilsenrath has a piece in the WSJ saying that the members of the FOMC are not yet in agreement on the need to raise rates next week. The Fed meets again next week, on Wednesday and Thursday.

Investors see the hesitance. In futures markets, where traders make bets on the outlook for Fed policy, the market places a 74% probability on the Fed leaving its benchmark rate unchanged this month, according to the Chicago Mercantile Exchange. Futures market prices show traders see the probability of a move by December at greater than 60%.

Still, the case isn’t closed. Internal deliberations could move the Fed toward action next week. New twists in markets or economic data will shape discussions.

I’m not going to make a guess on what the Fed will do, but I would think the central bank would want a broad majority for its first rate increase in nine years.

Fed Vice Chairman Stanley Fischer sought during a central-bank conference in Jackson Hole, Wyo., late last month to push against the market’s view that a September increase had become much less likely. He and other officials have sought to keep their options open, and some advocate a move.

“I will not, and indeed cannot, tell you what decision the Fed will reach by Sept. 17,” Mr. Fischer said.

The market’s perception of what the Fed will do has changed since China devalued last month. But I strongly doubt that influenced Fed members.

If I were a voting member, I’d vote against a rate hike. As of yet, President Obama has not called for my advice.

The Fed’s decision isn’t a binary one—to act or not to act. Before every policy meeting Fed staff economists present officials with a variety of choices, typically three, including middle-ground options that navigate between Fed “hawks” who lean away from low interest-rate policies and “doves” who support easy money.

A middle-ground choice now could involve signaling more strongly the Fed’s intent to raise rates this year once officials become comfortable recent market moves aren’t a sign of deeper problems in the global economy.

“It would be reasonable, from my own perspective, to see interest rate increases sometime later this year—or an interest rate increase” if the U.S. outlook doesn’t deteriorate, Mr. Williams said.

I think the market doesn’t fully realize that the Fed could hike once or twice and then do nothing. The first increase will have the biggest impact on investor psychology. But in reality, 0.25% increases aren’t that much.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His