Archive for July, 2018

-

Stryker Earns $1.76 per Share for Q2

Eddy Elfenbein, July 24th, 2018 at 4:26 pmStryker (SYK) reported Q2 earnings of $1.76 per share. That’s above their guidance range of $1.70 to $1.75 per share. Net sales rose 10.3% to $3.3 billion.

“We continue to execute on our strategy and delivered another strong quarter of organic sales growth, adjusted operating margin expansion and adjusted net earnings per diluted share,” said Kevin A. Lobo, Chairman and Chief Executive Officer. “Our diversified and decentralized business unit model combined with strong talent and culture continue to serve us well. We have raised our guidance to reflect the strong results and positive outlook for the remainder of the year.”

For Q3, they’re looking for earnings between $1.65 and $1.70 per share. Wall Street had been expecting $1.69 per share.

For all of 2018, Stryker now expects earnings to range between $7.22 and $7.27 per share. That’s the second increase. SYK’s initial range was $7.07 to $7.17 per share. Then it went to $7.18 to $7.25 per share.

Business details:

Consolidated net sales of $3.3 billion increased 11.0% in the quarter and 9.9% in constant currency. Organic net sales increased 7.9% in the quarter including 9.0% from increased unit volume partially offset by 1.1% from lower prices.

Orthopaedics net sales of $1.2 billion increased 8.0% in the quarter and 6.6% in constant currency. Organic net sales increased 6.6% in the quarter including 8.9% from increased unit volume partially offset by 2.3% from lower prices.

MedSurg net sales of $1.5 billion increased 10.0% in the quarter and 9.2% in constant currency. Organic net sales increased 7.3% in the quarter including 7.6% from increased unit volume partially offset by 0.3% from lower prices.

Neurotechnology and Spine net sales of $0.6 billion increased 20.1% in the quarter and 18.5% in constant currency. Organic net sales increased 12.4% in the quarter including 13.3% from increased unit volume partially offset by 0.9% from lower prices.

Earnings Analysis

Reported net earnings of $452 million increased 15.6% in the quarter. Reported net earnings per diluted share of $1.19 increased 15.5% in the quarter. Reported net earnings include certain items, including charges for acquisition and integration-related activities, the amortization of purchased intangible assets, restructuring-related and other charges, compliance with European Medical Devices Regulation, Rejuvenate and other recall-related matters, regulatory and legal matters and tax matters. The effect of each of these matters on reported net earnings and net earnings per diluted share appear in the reconciliation of GAAP to non-GAAP financial measures. Excluding the aforementioned items increases gross profit margin from 65.9% to 66.1% in the quarter and increases operating income margin from 20.2% to 25.7%(1), including a 20 basis point favorable impact related to the adoption of the new revenue recognition standard(2). Excluding the impact of the items described above, adjusted net earnings(4) of $670 million increased 15.3% in the quarter. Adjusted net earnings per diluted share(3) of $1.76 increased 15.0% in the quarter.

-

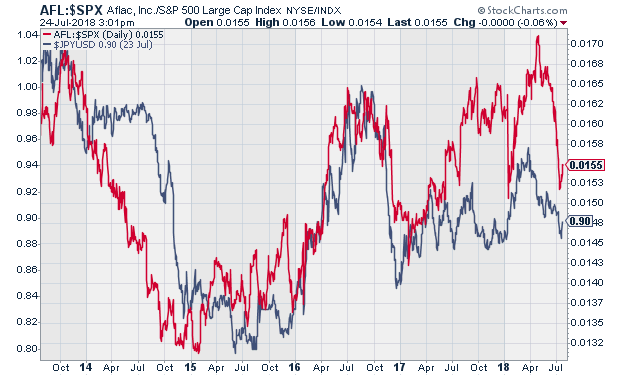

The Yen’s Impact on AFLAC

Eddy Elfenbein, July 24th, 2018 at 3:05 pmHere’s an interesting chart I wanted to show you. It shows AFLAC divided by the S&P 500 (in red) along with the yen/dollar (in blue).

The yen line is dollars per yen which is the inverse of how it’s normally discussed. I did this to show the correlation between the two.

Speaking of the correlation, the chart shows that they’re kind of related, but it’s not a very strong relationship.

In particular, the red line has dropped recently, meaning AFL has lagged. Some of this is probably due to the exchange rate, but I suspect that’s not all.

We’ll know more when AFLAC reports this week. I think the negative impact of the yen won’t dampen a solid earnings report.

-

Wabtec Earned 96 Cents per Share

Eddy Elfenbein, July 24th, 2018 at 9:27 amThe other earnings report this morning came from Wabtec (WAB). For Q2, the company made 96 cents per share. That beat estimates by three cents per share. They also increased full-year guidance.

Raymond T. Betler, Wabtec’s president and chief executive officer, said: “Our second-quarter results were on target, and with a strong backlog and the positive indicators we see in our markets we’re comfortable increasing our guidance for the year. Our freight business demonstrated strong growth in revenues and income from operations, and we expect demand to continue to improve. In transit, as expected we are managing through some lower-margin contracts in the short term while making long-term improvements in the core business. Overall, we’re pleased with our year-to-date performance, excited about the opportunities we see from our combination with GE Transportation and confident we can deliver improved earnings, margins and cash flow in the future.”

Wabtec increased its guidance for the year, with revenues now expected to be about $4.2 billion and EPS expected to be about $3.85 excluding estimated costs related to the proposed GE Transportation merger, expenses for restructuring and the effects of tax law changes. The company’s adjusted operating margin target for the full year is about 13.5 percent, and its effective tax rate for the full year is expected to be about 24 percent excluding the second quarter tax benefit.

-

Sherwin-Williams Earns $5.73 per Share

Eddy Elfenbein, July 24th, 2018 at 9:17 amThe second-quarter earnings report from Sherwin-Williams (SHW) is out. The company made $5.73 per share for Q2. That beat estimates by seven cents per share. The company is also increasing its guidance range for this year to $19.05 to $19.35 per share.

CEO John G. Morikis said, “The Company posted record results in net sales, gross profit, and profit before taxes in the second quarter, aided by the Valspar acquisition which continues to build momentum. Consolidated earnings per share expanded by 26.8% percent in the quarter, excluding acquisition-related costs and environmental expense provisions impacts in both years. Underlying demand remained solid across most of our end market segments during the quarter. At the same time, raw material costs continued to inflate during the quarter at a rate slightly higher than anticipated. We continue to focus on offsetting these escalating costs by controlling spending and implementing price increases.”

-

Morning News: July 24, 2018

Eddy Elfenbein, July 24th, 2018 at 5:07 amPortugal Dared to Cast Aside Austerity. It’s Having a Major Revival.

Trump Trade War Overshadowing Other Potentially Harmful Global Battle

Big Oil Is Raking In Cash and Investors Are Asking Now What?

Home Sales Extend Slump Despite Economic Strength

Trump Just Hijacked a Necessary Conversation About Amazon

Alphabet Gains as Google Ad Machine Powers Past Record Fine

Google Loses 2 More Cloud, AI Execs

Sergio Marchionne’s Exit Jolts Ferrari

Nike to Bump Up Pay for 7,400 Employees After Internal Review

Las Vegas Shooting Victims Speak Out Against MGM Lawsuit Against Them

GE Stock Sinks Again Despite Solid Results

Whirlpool Sinks With Raw Material Costs Climbing Around the World

Ben Carlson: How Hard is it to Become a 401(k) Millionaire?

Michael Batnick: Pick One Stock

Roger Nusbaum: Lifestyle, Investing and Gurus

Be sure to follow me on Twitter.

-

The Overrated Trade War

Eddy Elfenbein, July 23rd, 2018 at 12:51 pmGoldman Sachs said that a full-blown trade war could shave 15% off the earnings for the S&P 500.

That may be correct, but I have a few things to add. I would say that the odds of a full blown trade war are very low. The negative impact of anything that has a decent chance of happening are quite low.

“We consider adverse scenarios in which tariffs are placed on all imports from China or globally. For all US industry, roughly 15% of cost of goods sold (COGS) is imported. We assume that S&P 500 companies, which are more global in nature and have more complex supply chains, import roughly 30% of COGS. This is consistent with the 29% of S&P 500 sales is generated outside the US. Imports from China comprise 18% of total US imports. Conservatively assuming no substitution to other suppliers or pass-through of costs, and no boost to domestic revenues or change in economic activity, a 10% tariff on all imports from China would lower our 2019 S&P 500 EPS estimate by 3% to $165. If tensions spread and a 10% tariff were implemented on all US imports (highest rate since 1940s) our EPS estimate would fall by 15% to $145.”

Don’t get me wrong — a trade war is bad, but a minor skirmish won’t destroy us.

-

Morning News: July 23, 2018

Eddy Elfenbein, July 23rd, 2018 at 7:16 amBank of Japan Offers Unlimited Bond Buying After Yields Jump

Alphabet Bulls Looking for Earnings Spark From FANG Laggard

French IT Firm Expands in U.S. With $3.4 Billion Deal

Microsoft: Letting This Bull Rampage On

Sudden CEO Shift Jolts Fiat Chrysler

China Tower Seeks to Raise Up to $8.7 Billion in Hong Kong IPO

Ryanair Warns Labor Strife Is Starting to Bite as Profit Slides

Tesla Asks Suppliers for Cash Back to Help Turn a Profit

Papa John’s Board Votes to Adopt ‘Poison Pill’ Against Founder

Howard Lindzon: Another Open Letter to Twitter

Roger Nusbaum: What To Do If Sandinistas Ruin Your Retirement Plan

Jeff Miller: Weighing the Week Ahead: A Delicate (and Temporary) Balance

Be sure to follow me on Twitter.

-

CWS Market Review – July 20, 2018

Eddy Elfenbein, July 20th, 2018 at 7:08 am“Nothing so undermines your financial judgment as the sight of your neighbor getting rich.” – J.P. Morgan

Earnings season is underway, and the stock market is mostly in a pleasant mood. On Wednesday, the S&P 500 closed at its highest level in nearly six months. Then on Thursday, we got the lowest jobless-claims report since December 6, 1969. For context, that was the same day as Altamont. (Google it.)

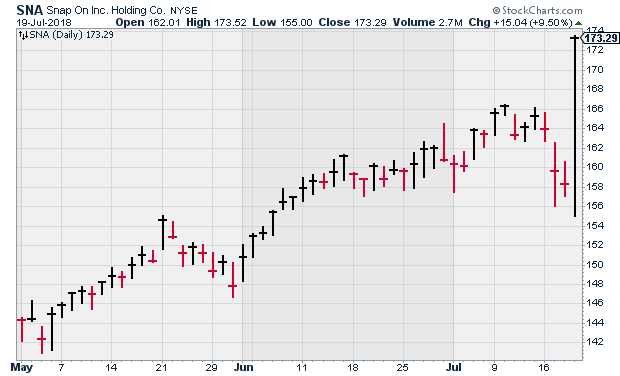

Spoiler Alert: This week’s issue is all about earnings. We had five Buy List reports on Thursday, and it was mostly quite good. Snap-on beat earnings, and the stock jumped 10%. Danaher also rallied on a nice earnings beat, and they announced they’re going to spin off their dental business next year. Signature Bank said they’re initiating a dividend. I’ll go through all the details in a bit.

This is only the beginning. We’re going to have seven more Buy List earnings reports next week, then another nine in the week after that. Without further ado, let’s look at this week’s earnings.

Five Buy List Earnings Reports

Thursday was a very busy day for us with five Buy List stocks reporting results. Here’s a look at our updated Q2 Earnings Calendar:

Company Ticker Date Estimate Result Alliance Data Systems ADS 19-Jul $4.66 $5.01 Danaher DHR 19-Jul $1.09 $1.15 RPM International RPM 19-Jul $1.18 $1.05 Signature Bank SBNY 19-Jul $2.80 $2.83 Snap-On SNA 19-Jul $2.95 $3.11 Sherwin-Williams SHW 24-Jul $5.66 Stryker SYK 24-Jul $1.73 Wabtec WAB 24-Jul $0.93 Check Point Software CHKP 25-Jul $1.30 Torchmark TMK 25-Jul $1.49 AFLAC AFL 26-Jul $0.99 Moody’s MCO 27-Jul $1.90 Carriage Services CSV 31-Jul $0.37 Fiserv FISV 31-Jul $0.74 Becton, Dickinson BDX 2-Aug $2.86 Cerner CERN 2-Aug $0.60 Church & Dwight CHD 2-Aug $0.47 Cognizant Technology Solutions CTSH 2-Aug $1.10 Continental Building Products CBPX 2-Aug $0.45 Ingredion INGR 2-Aug $1.65 Intercontinental Exchange ICE 2-Aug $0.89 Let’s start with our big winner. Shares of Snap-on (SNA) jumped nearly 10% on Thursday thanks to a very good earnings report. For Q2, earnings per share rose 20% to $3.11. That was well above Wall Street’s estimate of $2.95 per share. Net sales rose 3.6%, and organic sales increased 1.3%. I was especially pleased to see a 0.3% increase in operating margins. That’s often a good sign of fiscal health.

Snap-on was also our big winner during the Q1 earnings season, but it quickly gave back most of those gains. I’m still concerned by weakness in Snap-on’s tool division, but other areas are doing well. Overall, I’m pleased with this report. I suspect the sentiment for Snap-on is still pretty negative. That’s why an earnings beat translated into such a big gain for the stock. Our patience is paying off. This week, I’m lifting my Buy Below on Snap-on to $181 per share.

Our second-biggest winner was RPM International (RPM). Oddly enough, RPM looked like it was going to be a big loser. After the earnings report, the shares opened down 4%. This is why we eschew trading. It’s too irrational. Fortunately, the market came to its senses, and RPM closed higher by 5.3%. The difference between Thursday’s high and low prices was nearly 12%. (Dear day-traders: RPM isn’t that interesting!!!)

For fiscal Q4, RPM earned $1.05 per share which was 13 cents below Wall Street’s consensus. The company blamed “higher raw-material costs and extended winter weather.” Rust-Oleum had to shutter two manufacturing facilities. RPM’s consumer segment was especially weak while the industrial unit fared better.

As part of the deal with Elliott Management, RPM is going to unveil a comprehensive business plan later this year. I think that may involve major divestments. Because of this, the company will forgo any EPS guidance. Sales-wise, for 2019, RPM expects a mid-single-sales increase for its industrials unit. For the consumer unit, they see an increase of mid- to upper-single digits. I’m raising my Buy Below on RPM to $67 per share.

Danaher (DHR) not only beat earnings, but also said it’s going to spin off its dental business next year. For Q2, Danaher earned $1.15 per share. When the last earnings report came out, they told us to expect $1.07 to $1.10 per share. For the second time, Danaher raised its full-year guidance. The company now expects 2018 earnings to range between $4.43 and $4.50 per share.

The dental spinoff won’t happen until the second half of 2019. The business is currently responsible for about 20% of the company’s overall revenue, but growth has been tepid lately. According to The Wall Street Journal, “Danaher said it expects the dental spinoff to have an investment-grade credit rating and about 12,000 employees.” The spinoff will be tax-free.

Shares of DHR jumped to a new high on Thursday. I’m lifting my Buy Below on Danaher to $110 per share.

Alliance Data Systems (ADS) reported Q2 earnings of $5.01 per share. That beat estimates by 35 cents per share. Despite the impressive earnings beat, ADS gained about 0.5% on Thursday.

Ed Heffernan, the CEO, said, “The second quarter marked the beginning of the long-awaited acceleration in our business.” The company is standing by its full-year earnings forecast of $22.50 to $23 per share. That gives them a P/E Ratio of about 10.

On Monday, shares of ADS dropped 10% after a weak monthly business update. I didn’t think the numbers were that bad. Fortunately, the Q2 earnings report is reassuring. This report is basically what I had been expecting. The stock is still working through an impressive turnaround, but it’s not going to be in a straight line. Don’t give up on ADS. I’m dropping my Buy Below down to $245 per share.

Our only loser on Thursday was Signature Bank (SBNY), and even they beat the Street. For Q2, SBNY made $2.83 per share, three cents more than estimates.

But the biggest news is that Signature is initiating a dividend. That’s good to see. The New York bank will start paying a quarterly dividend of 56 cents per share. Based on Thursday’s close, that’s a yield of 1.89%. Not bad, and Signature can easily cover it. That’s a payout ratio of about 25%. The new dividend is payable on August 15 to shareholders of record on August 1.

Let’s look at some numbers for the quarter. Total deposits now stand at $34 billion. That’s an increase of 5.5% in the last year. Loans rose to $34.15 billion. That’s up 12.4% in the last year. Net interest margin, which is the key metric for banks, came in at 2.94%. Those are decent numbers.

Still, on Thursday, the shares lost more than 5%. At one point, the stock dropped to its lowest level in 10 months. The stock is lower than where it was 4 1/2 years ago. I’m puzzled by SBNY’s lackluster performance. Perhaps the narrowing yield curve is scaring investors off. In any event, I still like Signature. This week, I’m dropping my Buy Below to $131 per share.

Seven More Earnings Reports Next Week

Next week will be another busy week. Seven of our Buy List stocks are due to report. The parade starts on Tuesday, July 24, when Sherwin-Williams, Stryker and Wabtec are due to report.

Sherwin-Williams (SHW) started off the year poorly for us, but it’s gained ground since the spring. Business is going well for Sherwin, but they’ve had trouble digesting the Valspar acquisition. I was afraid that might happen.

Excluding any Valspar issues, Sherwin expects $18.35 to $18.95 per in earnings this year. For Q2, Wall Street expects $5.66 per share. They should be able to beat that.

In April, Stryker (SYK) topped estimates and raised its full-year forecast. SYK’s initial range was $7.07 to $7.17 per share. Now they see 2018 coming in between $7.18 and $7.25 per share. For Q2, Stryker expects $1.70 to $1.75 per share.

This is a good time to look at Stryker. The shares got clobbered in early May after news came out that Stryker made an offer to buy Boston Scientific. Since the deal fell apart, SYK has rallied some, but it’s still below its May high.

Who would have guessed that Wabtec (WAB) would have been a 29% winner by July? Not me, that’s for sure, and I’m a fan. Obviously, the big news for the freight-services company is the merger with GE’s rail business. This is a huge opportunity. I do have concerns similar to those with Sherwin-Williams and Valspar. Wabtec expects full-year revenues of $4.1 billion, and earnings of “about” $3.80 per share. Wall Street expects Q2 earnings of 93 cents per share.

On Wednesday, Check Point Software and Torchmark are due to report. Three months ago, shares of Check Point Software (CHKP) got dinged after their Q1 earnings report. The earnings were fine, but traders didn’t like guidance. For Q2, Check Point expects revenue to range between $445 and $475 million. Wall Street had been expecting $477 million. For Q2 EPS, their range is $1.25 to $1.35. Wall Street had been expecting $1.35 per share.

Check Point also cut its full-year earnings range. The previous guidance was $5.50 to $5.90 per share. The new range is $5.45 to $5.75 per share. The issue is that Check Point has been shifting its business towards a greater reliance on subscription revenue. The problem is that these subscriptions boost results in higher deferred revenue. The company shouldn’t have any major difficulties working these problems out. Since June 25, the shares are up over 15%.

Torchmark’s (TMK) earnings are about the steadiest you’ll find. The company gave 2018 guidance of $5.93 to $6.07 per share. That’s probably too low. I think TMK can hit $6.10 per share, but I won’t quibble with their guidance; we’re still early in the year. For Q2, Wall Street expects $1.49 per share.

AFLAC (AFL) reports on Thursday. The duck stock has been sliding lately, and the strong dollar is probably to blame. For Q2, AFLAC said they’re expecting earnings between 91 cents and $1.05 per share. That assumes the yen averages between ¥100 and ¥110 to the dollar. It’s currently at ¥112.57. AFLAC is standing by its earnings forecast for full-year earnings of $3.72 to $3.88 per share.

Moody’s (MCO) will report its Q2 earnings on Friday. The stock is up 23.5% for us this year, and it just reached another new high. Moody’s business seems to be moving along quite well. I also like their Moody’s Analytics business. The company reaffirmed its full-year earnings forecast of $7.65 to $7.85 per share. For Q1, Wall Street’s consensus is $1.90 per share.

Before I go, I wanted to mention that last Friday, Smucker (SJM) raised its dividend by 9%. The quarterly dividend will rise from 78 to 85 cents per share. The new dividend will be paid on Tuesday, September 4 to shareholders of record at the close of business on August 17. This is SJM’s 17th-straight annual dividend increase.

That’s all for now. There are more Buy List earnings reports next week, so expect some volatility. Next Friday, we’ll get our first look at Q2 GDP. This could be a big number. Maybe 4%. We’ll also get the existing-homes sales report on Monday. The new-homes sales report comes out on Wednesday. Then on Thursday, it’s the durable-goods report. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Syndication Partners

I’ve teamed up with Investors Alley to feature some of their content. I think they have really good stuff. Check it out!

Buy These 3 High-Yielders Profiting from the Permian Bottleneck

How to Profit from Trump’s Trade War

Morning News: July 20, 2018

Eddy Elfenbein, July 20th, 2018 at 7:05 amChina’s Rising Economic Pressure Prompts Talk of Policy Rethink

Google’s Loon Brings Internet-By-Balloon to Kenya

The $20 Billion Question for Guyana

Dollar Bulls Learn the Meaning of Complacency

Trump Says He’s ‘Ready To Go’ With $500 Billion in Tariffs on All China Imports

Trump Lays Into the Federal Reserve, Says He’s ‘Not Thrilled’ About Interest Rate Hikes

Microsoft Set for Record High Open as Cloud Sales Drive Earnings Blowout

GE Beats Profit Estimates as Aviation, Health Buoy Results

Amazon Reportedly Had a 300-Person Conference Call to Deal With the Prime Day Glitches

Merck to Lower Prices on Some Drugs, But Not Blockbusters

Domino’s Pizza Extends Its Growth Streak

Thieves Jump on Cobalt Craze With $10 Million Warehouse Heist

Blue Harbinger: What Do Winning Traders Have In Common?

Ben Carlson: Surrendering to the Charms of Magical Thinking

Joshua Brown: The Chart Heard ‘Round the World

Be sure to follow me on Twitter.

Trump Dings the Fed

Eddy Elfenbein, July 19th, 2018 at 1:50 pmEarlier today, President Trump mildly criticized the Federal Reserve. I think this is the first time he’s done this as president.

The president said, “I’m not thrilled because we go up and every time you go up they want to raise rates again. I don’t really — I am not happy about it. But at the same time I’m letting them do what they feel is best. But I don’t like all of this work that goes into doing what we’re doing.”

Looking at gold and the dollar, I can’t say he’s completely wrong.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His