CWS Market Review – March 22, 2019

“Capital isn’t scarce; vision is.” – Sam Walton

The Federal Reserve made news this week by finally recognizing reality. That’s an odd headline for a news story. The facts didn’t change in any meaningful way, nor did the economy. Rather, the only change was that a committee of economists agreed to admit what had been perfectly obvious to everyone: the economy doesn’t need higher interest rates, and probably won’t for some time.

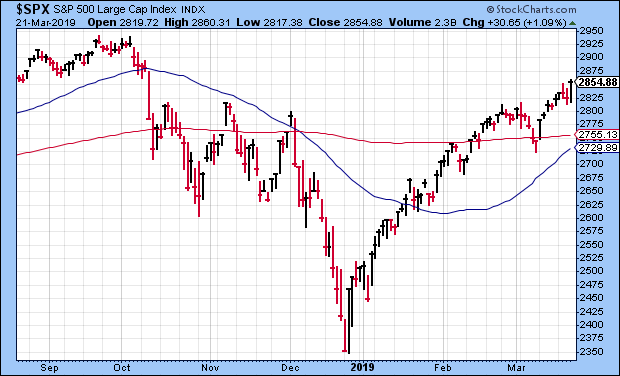

In 2019, that’s enough to rally on. On Thursday, the S&P 500 soared more than 1% to close at 2,854.88. That’s its highest close since October 9. Based on daily closes, the index has now made back 87% of what it lost during last year’s bout of unpleasantness.

In this week’s issue of CWS Market Review, I’ll go over what the Fed said and what it means for us. I also want to discuss Disney in some depth. The stock has gone nowhere recently, but I still like it. I’ll tell you why. Later on, I’ll preview the earnings report from FactSet. We also got a nice dividend boost from Raytheon. This is the 15th year in a row that Raytheon has sweetened its payout. But first, let’s look at this week’s Fed meeting and why we were right all along.

The Federal Reserve Catches up with Reality

Over the last few months, I’ve felt like a broken record. I’ve consistently said that the Federal Reserve has been vastly overestimating the need for more interest-rate increases. That’s why I’ve been so optimistic for our Buy List stocks.

This week, I’m happy to report that the Fed now agrees with us. In this week’s policy statement, the Fed said it’s not raising interest rates now. The central bank also kept the language that it “will be patient” in regard to further rate hikes. I think it’s clear that Chairman Powell has seen the need to alter course for a few months. The last rate hike was clearly not needed.

The important part of this week’s Fed news was the economic forecasts. The FOMC has 17 members. Though not all of them vote, all 17 members do get a chance to list their economic forecasts for the next few years. I’ll be honest – the Fed has a pretty bad record with its forecasts, but so does everyone else.

The FOMC members see the economy growing by 2.1% this year. That’s down from 2.3% when the last projections came out in December. They also lowered their inflation forecast (technically, the PCE index) by 0.1%. That’s not so important, but the big change came with interest rates. Of the 17 members, 11 see no need to change interest rates this year. Four members see the need for one hike, while two think two more are needed. In other words, the median vote wants to stand pat for the entire year. Hooray!

As for 2020, the FOMC sees the need for just one rate hike and no more changes in 2021. This is a remarkable turnaround. It wasn’t that long ago that the Fed thought it had to continue hiking rates this year and next. Why is this so important? The biggest factor impacting the direction of the market is real short-term interest rates. As long as those are low, then the math favors stocks. It’s not a guarantee of a bull, but it makes the bull feel a lot more comfortable.

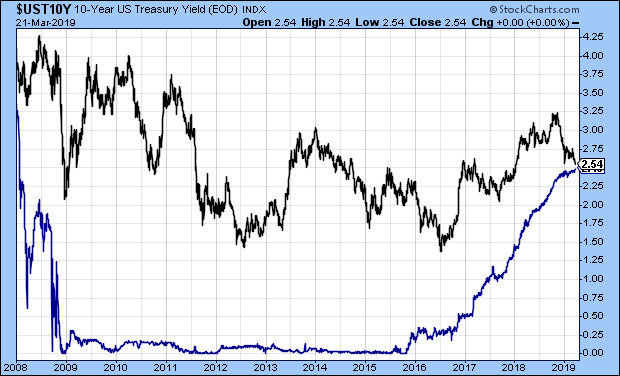

The futures market actually thinks there’s a 40% chance that the Fed will cut rates before the year is out. Hmmm. Call me a doubter. On Thursday, the yield on the three-month Treasury closed at a 10-year high. At the same time, the yield on the 10-year Treasury closed at a 14-month low. Since November, the yield on the 10-year has dropped by 70 basis points. That’s good news for mortgages and for housing in general. The chart above shows the 10-year yield (black) along with the three-month yield (blue). They’re nearly even. On Thursday, the two closed just five basis points apart.

This continues to be a favorable environment for investors. We’ll know a lot more once Q1 earnings season starts next month. Now let’s look at one of our stocks that seems to be stuck in a rut.

What’s Wrong with Disney?

I added Disney (DIS) to the Buy List at the start of this year and I’m not sorry I did. The stock, however, is down 1% for us. In fact, the stock is exactly where it was four years ago. I’m not concerned one bit.

Let’s back up a moment. The Mouse House had a great earnings report for Q4. The company made $1.84 per share which creamed estimates by 29 cents per share. Revenue fell to $15.30 billion, but that still beat expectations of $15.14 billion.

The big story here is that Disney is making a major push into streaming. Of course, Disney is into a lot of things. The parks are doing well. The movie business is down from last year, but that’s only because of some tough comparisons with some blockbusters in 2017.

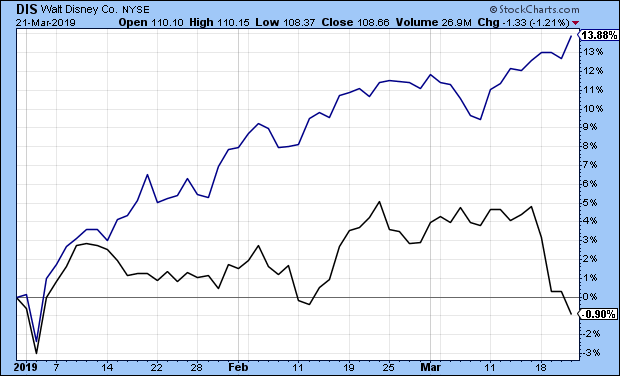

Here’s Disney YTD (in black) with the S&P 500 (in blue).

That brings us to this week and the big news that the mega-deal between Disney and Twenty-First Century Fox is now official. The deal is worth $71 billion. This is huge, and it will impact the entire entertainment industry. As I said, Disney is getting ready for the Streaming Wars.

Now that Disney owns Fox, they also own a boatload of movies and classic-movie franchises. (Just to be clear, Disney does not own Fox TV.) Disney also owns a 60% stake in Hulu. The deal also brings the X-Men and Fantastic Four characters back to Marvel, which is owned by Disney.

The backstory here is that Disney sees Netflix’s success and it’s not going to roll over. Disney is ready to take on Netflix, or anybody. There are still a lot of questions about the merger. There will be layoffs, but we don’t know yet how many.

It’s as if Disney and Netflix were two competing visions of the future. Disney is the old-line media company with tons of content. Netflix is a tech company that offers tons of choices.

I suspect the stock has been flat because there are simply a lot of concerns that Bob Iger can pull this off. There are worries that Disney will have to keep spending to stay competitive. As a result, some on Wall Street think Iger will have to lower earnings guidance for this year. That could be. The Investor Day webcast is coming up on April 11. The company plans to unveil its Disney+ streaming service.

I think it’s noteworthy that Netflix’s CEO thinks there’s plenty of room for competitors. Americans spend one billion hours a day watching video content. I think Disney is in great shape. The assets they now control are staggering, and the stock is going for a decent valuation. Disney is a buy up to $118 per share.

FactSet Earnings Preview

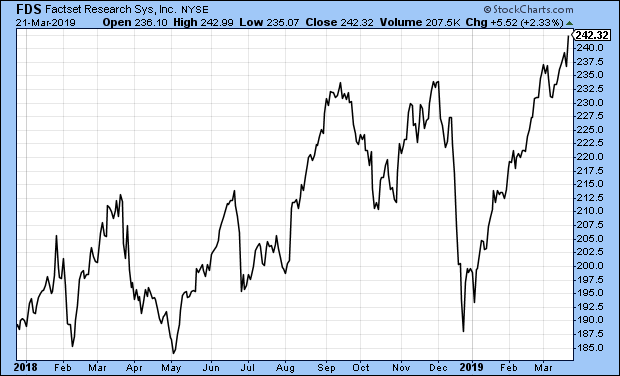

On Tuesday, March 26, FactSet (FDS) is due to report its fiscal Q2 earnings. This is for the quarter covering December, January and February. The stock has been a nice 21% winner this year for us.

In December, the fiscal-Q1 earnings report was quite a good one. Factset reported a 15% jump in earnings. That beat the Street by six cents per share. Also, organic revenue rose by 6.4%.

With FactSet, the key stat to watch is Annual Subscription Value, or ASV. At the end of Q1, ASV had increased to $1.42 billion. I was pleased to see that FactSet’s operating margin rose to 28.6%. FactSet’s client count stands at nearly 5,300, while user count is now over 115,000. Their annual retention rate is over 95%. People love their service.

In December, FactSet reiterated its 2019 guidance. FDS sees earnings ranging between $9.45 and $9.65 per share. That’s up from $8.53 per share last year. FactSet also sees organic ASV rising by $75 million to $90 million in 2019, and they see operating margins between 31.5% and 32.5%. That’s quite good.

The stock got dinged after the last earnings report. In December, I wrote, “I don’t see anything wrong with the earnings report. FactSet continues to be an excellent company. Now it has a cheaper share price. If you can buy FDS near $200 per share, then you got a good deal.” FDS closed Thursday at $242.32 per share.

FDS closed higher in 11 of the last 12 weeks. I’ll caution you that the shares are well above my Buy Below price. I’ll probably adjust that next week, but I want to see the earnings report first. Wall Street expects Q2 earnings of $2.33 per share.

Raytheon Hikes Its Dividend by 8.6%

On Wednesday of this week, Raytheon (RTN) announced an 8.6% increase to its dividend. This is the fifteenth year in a row that Raytheon has hiked its dividend. The quarterly payout will rise from 86.75 cents to 94.25 cents per share. That’s an increase of 8.6%.

“With today’s announcement, we have increased our annual dividend for 15 consecutive years,” said Thomas A. Kennedy, Raytheon Chairman and CEO. “The dividend increase is a key part of our capital deployment strategy, and reflects our confidence in the company’s growth outlook and our continued focus on creating value for shareholders.”

The new dividend will be paid on May 9 to shareholders of record as of the close of business on April 10. Raytheon is one of our new stocks for 2019, and it’s already up 18.6% for us this year. RTN is still 20% below its 52-week high. Based on Thursday’s closing price, Raytheon yields just over 2%. Raytheon is a buy up to $190 per share.

That’s all for now. Next week is the final week of March, and by extension, the final week of the first quarter. This looks to be one of the best quarters for the market in years. (True, last year’s Q4 was pretty ugly.) On Tuesday, we’ll get reports on housing starts and consumer confidence. On Thursday, the Q4 GDP report will be updated. The initial report showed growth of just 2.6% for the final three months of 2018. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

P.S. Happy birthday to the AdvisorShares Focused Equity (CWS). Our ETF just turned 2.5 years old. We’re celebrating with an after-market call this Wednesday, March 27 at 4 pm ET. Howard Lindzon will be our special guest. Please join us. You can register here.

Posted by Eddy Elfenbein on March 22nd, 2019 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

I want to remind everyone that investing isn't about making money. It's about making friends and having a good time.

Good run:

“Common Sense,” by Thomas Paine (published January 10, 1776)

“The Decline and Fall of the Roman Empire” (Vol. 1), by Edward Gibbon (February 17, 1776)

“An Inquiry into The Wealth of Nations,” by Adam Smith (March 9, 1776)

“The Declaration of Independence,” by… -

-

Archives

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His