CWS Market Review – June 27, 2023

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

UBS Takes the Axe to Credit Suisse

Spare a kind thought for your friendly neighborhood investment banker. This is a tough time for him or her. All over Wall Street, bankers are being laid off, and it’s not over.

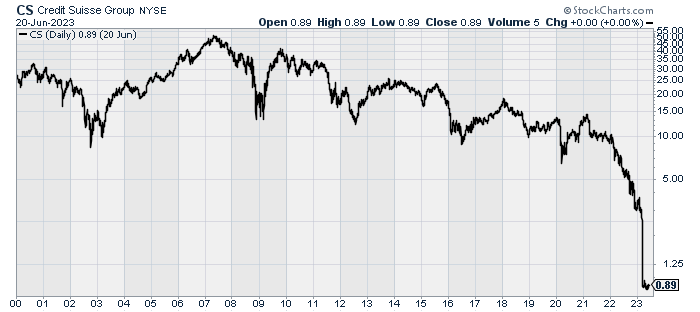

Things are especially bad for Credit Suisse. Earlier this year, the legendary Swiss bank, Credit Suisse, came to an ugly end. UBS, its longtime rival, bought it for $3.2 billion.

The plunge was epic. At the end of last year, Credit Suisse had a balance sheet of half a trillion dollars and 50,000 employees globally. Within weeks, it was a total trainwreck.

In March, I wrote:

To say this was a fire sale badly understates the events. The Swiss government essentially forced this deal to happen. They aimed to stop the banking crisis cold. To give you an idea of how far they went, the settled price for Credit Suisse was less than half of Friday’s closing price. It works out to 7% of CS’s tangible book value.

CS shareholders will get one share of UBS for every 22.48 shares of CS they own. That values a share of CS at 0.76 Swiss francs which is 99% below its high.

Yikes!

Today UBS said that it’s going to cut more than half of Credit Suisse’s workforce. Most of the cuts will be among traders, support staff and investment bankers. Bear in mind that this deal was done to prevent as many job losses as possible.

UBS looks to do three rounds of cuts before the end of the year. By the time they’re done, UBS will have cut their total workforce by 30% or about 35,000.

UBS isn’t alone. Goldman Sachs is also feeling the squeeze. Simply put, nobody is doing any deals this year. In dollar terms, the amount of Wall Street deals is down 40% this year.

Goldman is going to cut 125 managing directors. I’m sure that’s a lot of money. To be a managing director at Goldman is almost like Wall Street’s version of being a “made man.”

This is Goldman’s third round of layoffs in less than a year. In January, Goldman cut a bunch of jobs and the employees didn’t get their year-end bonuses.

JPMorgan Chase is cutting about 40 investment banking jobs. Citigroup will cut 30 investment-banking jobs. Last month, Morgan Stanley said it’s cutting another 3,000 jobs. A few years ago, many of these same banks went on a hiring binge. Now that’s over.

I have to be frank: this doesn’t impact the direction of stocks so much. Stocks can do very well even when the amount of Wall Street wheeling and dealing dries up. Lately, however, the noticeable trend from stocks is the big drop in volatility. We’re not seeing the kind of daily gyrations that characterized recent years.

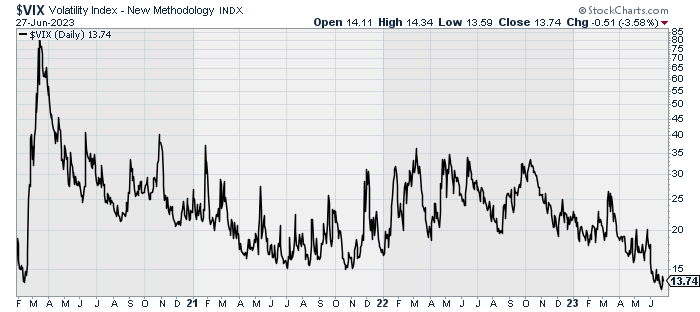

The Volatility Index Hits a Three-Year Low

Today was a good day for stocks. The S&P 500 closed higher by more than 1.15%. The tech-heavy Nasdaq was up by 1.65%. The cyclical-skewed Russell 2000 also did well as it gained 1.46%. The S&P 500 ended a run of five down days in six sessions.

High beta stocks significantly outperformed low volatility stocks. The S&P 500 High Beta Index gained 2.59% today while the S&P 500 Low Vol Index gained just 0.34%. Interestingly, the growth/value divide wasn’t so large today.

I like to track the VIX which is the Volatility Index, or as some call it, the Fear Index. Last Thursday, the VIX closed at 12.91 which is a three-and-a-half year low. The last time the market was this calm was just before Covid hit.

Traders are gradually resigning themselves to the fact that the Federal Reserve isn’t done with its rate hikes. The Fed won’t meet for another month, but the mood on Wall Street has definitely changed. Traders now realize that the Fed won’t let up until inflation is gone.

The mood change is also apparent in the stock market. For much of this year, growth stocks were leading value stocks. Lately, however, value stocks have struck back. This is likely due to the changing outlook for Fed policy. When rates go higher, investors become more conservative. We can’t say if it’s a meaningful turn, but it’s good to see.

I think too many investors thought that lower rates would bring us back to the free-and-easy investing of the Covid years. When rates are near 0%, P/E Ratios don’t mean much. Now that rates are over 5%, investors have become a lot more discerning.

My concern is that too many growth stocks have been allowed to get rich valuation without any market pressure. A good example, in fact maybe the ideal example, is Tesla (TSLA). I need to preface by stressing that I’m in no way anti-Tesla, but the stock has had a remarkable run this year. At one point, shares of Tesla were up 120% this year. The stock was trading at nearly 100 times this year’s estimated earnings.

I certainly understand that Tesla is a remarkable company, and it’s leading a major change in the automotive sector, but it can’t escape the simple question: how much is too much? In the last week, Tesla has lost more than 10%.

We may be in an odd spot where more good economic news is bad for growth stocks. I’ve been impressed by how resilient the economy has been.

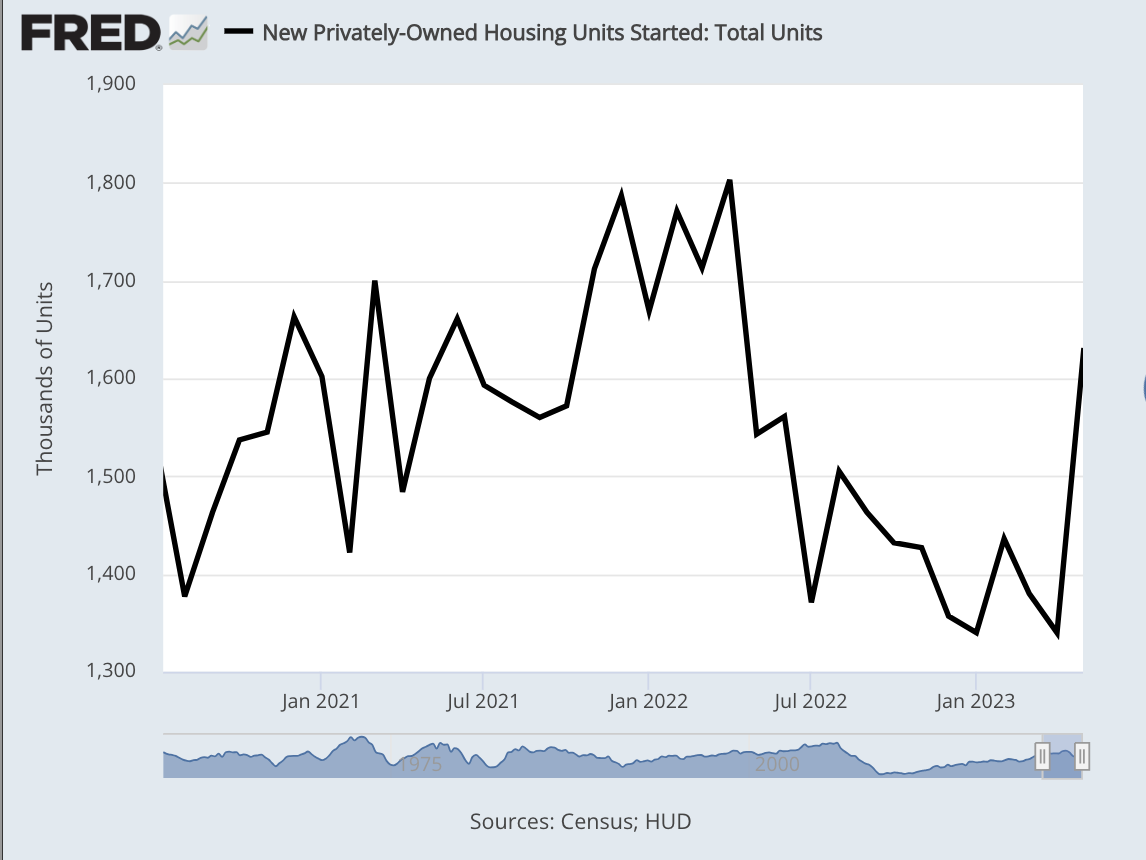

One bright spot for the economy is that the housing market may be on a rebound. This comes after a long, difficult stretch. This morning, the government reported that new home sales surged last month.

Let me take a step back to explain. What happened is that as the Fed raised interest rates, not many new homes were made. As a result, the inventory of new homes dropped very low relative to sales. At the end of May, total housing inventory was 1.08 million units. That’s down 6.1% from last year.

So many people locked in mortgages at low rates that they had little incentive to sell. At some point, you need greater inventory and that means more building. That’s exactly what’s happening.

From April to May, new home sales jumped 12.2%. In the last year, new home sales are up 20%. Sales of single-family homes came in at 763,000 (that’s an annualized figure). That’s up from 680,000 in April. I’m also impressed to see that the quality of mortgage loans is much higher than it was during the financial crisis.

It’s difficult for the broad economy to slip into a recession if the housing market is healthy. This is because housing touches so many different sectors. Median home prices are now down 16% from their peak. The Homebuilders ETF (XHB) touched a new 52-week high today.

It’s not just housing. We also learned this morning that orders for durable goods increased by 1.7% last month. That’s very good. This tells us that companies are probably making more long-term investments.

For durable goods, the key is to watch core capital goods orders. That’s a good proxy for business investment. Core capital goods excludes aircraft and military sales. For May, core capital goods rose by 0.7%. That compares with an increase of 0.6% in April.

Not only is the economy growing, but it may be accelerating. On Thursday, the government will release its second revision to Q1 GDP growth. The last report said that the U.S. economy expanded at a real annualized rate of 1.3% during Q1.

In late July, the government will release its first estimate for Q2 GDP. Most economists expect slightly higher growth for Q2 compared with Q1. According to the latest, Bank of America expects Q2 growth of 1.4%. Goldman is at 1.8% and the Atlanta Fed’s GDP Now model is at 1.9%.

The most widely-expected recession in recent history continues to be a stubborn no-show. Now traders don’t expect the Fed to cut rates until March 2024. That’s a big change from just a few weeks ago.

Until a few years ago, setting the Fed’s interest rate policy was pretty simple. When the economy entered a recession, all you had to do was bring short-term interest rates down to the same level of inflation. That meant that the “real” interest rate was 0%.

During an economic recovery, all you had to do was gradually raise interest rates until they were 3% above the rate of inflation. In other words, the Fed would simply oscillate between real Fed funds rates of 0% to 3%.

I’m exaggerating but not by much. That’s largely what the Fed did for a few decades. Then came the financial crisis and all of that went out the window. Since then, the Fed has kept interest rates well below the rate of inflation. Now it seems that the Fed is willing to raise interest rates much higher than expected. That’s good news for value-oriented portfolios.

Stock Focus: Graco (GGG)

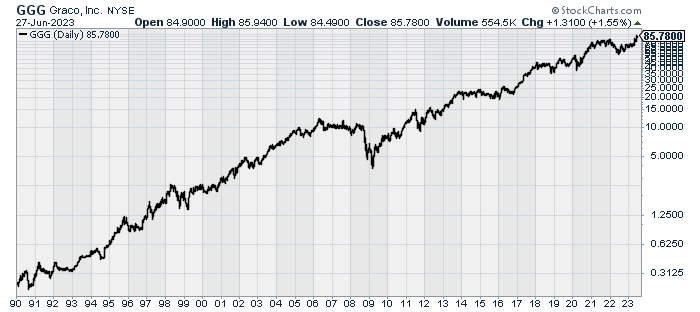

Speaking of which, here’s the latest in our series of great stocks that no one knows about. Graco (GGG) of Minneapolis specializes in fluid-handling systems and products. The company has been in business since 1926.

Graco’s business covers several different areas such painting, anti-corrosion, fluid transfer, gluing and sanitary applications, automotive, aeronautic, body refinish, wood, construction and marine.

I know it sounds boring, but it’s a very good business to be in. Many boring-sounding businesses can be wonderful investments. Last year, Graco did $2.14 billion in sales and net income was $460 million, or $2.63 per share.

Graco has been a big winner for decades. Ten years ago, it made $1.12 per share for the year. Ten years before that, it made 41 cents per share for the year. The company’s earnings don’t rise every year, but it’s a strong upward trend.

Thirty years ago, you could have picked up one share of Graco for $31.50. Adjusted for several stock splits, that works out to less than $1 per share in today’s terms. Meanwhile, the stock is at $85 per share today. That means that Graco has gained more than 90-fold over the last 30 years. If we include dividends, then Graco is up more than 18,500% over the last three decades.

Despite all its success, Graco doesn’t get much attention. Only about ten analysts bother following it. The market cap is about $14 billion.

In April, Graco reported Q1 earnings of 74 cents per share. That beat estimates by 12 cents per share. The stock jumped over 12% on its earnings report. Wall Street expects earnings for this year of $3.04 per share and of $3.19 per share for 2024. The stock is a little pricey but nothing outrageous.

The Q2 earnings report will be out in about a month. Wall Street expects 79 cents per share. Look for another earnings beat.

That’s all for now. There will be no free issue next week. The stock market will close early on Monday, July 3, and it will be closed all day on July 4 for Independence Day. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

Posted by Eddy Elfenbein on June 27th, 2023 at 6:39 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His