Author Archive

-

Irrational Exuberance Turns 18

Eddy Elfenbein, December 5th, 2014 at 10:04 amIt was 18 years ago today that Alan Greenspan gave his famous

“Irrational Exuberance” speech.Clearly, sustained low inflation implies less uncertainty about the future, and lower risk premiums imply higher prices of stocks and other earning assets. We can see that in the inverse relationship exhibited by price/earnings ratios and the rate of inflation in the past. But how do we know when irrational exuberance has unduly escalated asset values, which then become subject to unexpected and prolonged contractions as they have in Japan over the past decade?

The next day the Dow fell 55 points, and the S&P 500 lost 0.64%. By that point, the market has rallied more than 64% in two years, so some people were clearly nervous.

The bull market, however, was just getting started.

Greenspan’s speech got a lot of attention, but didn’t have much of an impact on the market. The Wilshire 5000 Total Return Index, which includes dividends and just about every stock, climbed another 114% to the March 2000 peak.

Since that day 18 years ago, the Wilshire 5000 Total Return Index has returned 307%. Annualized, that’s 8.11%.

-

Huge Jobs Report for November

Eddy Elfenbein, December 5th, 2014 at 9:22 amThe government reported that the U.S. economy created 321,000 net new jobs last month. This was our 50th-straight month of jobs gains.

On top of that, the number for September was revised higher by 15,000, and October was increased by 44,000. In the last 10 months, the economy created 2.5 million new jobs. The unemployment rate stayed the same at 5.8%.

This is a very strong report. Wall Street had been expecting an increase of 230,000 jobs. Average hourly earnings rose nine cents to $24.66 per hour.

-

CWS Market Review – December 5, 2014

Eddy Elfenbein, December 5th, 2014 at 7:09 am“I rest perplexed with a thousand cares.” – Henry VI, Pt 1

So does the stock market. Share prices continue to march higher, yet in very measured steps. On Wednesday, the S&P 500 closed at yet another all-time high, although we gave some of that back on Thursday. Still, the indexes are holding on to solid year-to-date gains. The S&P 500 is up more than 12% this year.

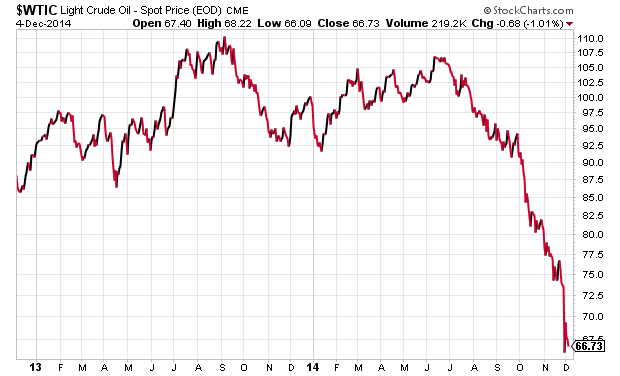

On Monday, the S&P 500 had its worst drop in six weeks. Of course, I have to laugh at this because the worst drop in six weeks is a measly -0.68%. Historically, that ain’t nothing. It’s especially small compared with the hyper-volatility of a few years ago. The fact is, the equity markets have chilled out in a major way.

The recent drama hasn’t been in stocks but in the commodity pits. The price of oil has been sliding since the spring (see above). Then, last Friday, the bottom fell out. Oil plunged 10% in one day. Bear in mind that this drop came after black gold had fallen by 27% in five months. Prices at the pump are the lowest they’ve been in four years!

Just about every major commodity has been feeling the pain. In this week’s CWS Market Review, we’ll take a closer look at what the commodities bear means for us. I’ll also run down some of the latest news for our Buy List stocks. Stryker ($SYK), one of our healthcare stalwarts, just gave us a nice 13% dividend increase. Express Scripts ($ESRX) just snapped a streak of 12-straight daily rallies. Before we get to that, though, let’s take a look at the slide in oil and the still-kicking Strong Dollar Trade.

The Global Fallout of the Rising Dollar

Earlier this year, I started telling you about the Strong Dollar Trade. I argued that this was emerging as a dominant investing theme and that it was impacting the economy and financial markets in different ways. All investors need to understand the effects of the rising greenback.

Put simply, the Strong Dollar Trade refers to the efforts of policymakers in Europe and Asia to weaken their currencies. Those economies are in rough shape, so they hope to spark a recovery by bringing down their currencies. That means the U.S. dollar appreciates. In turn, a rising dollar puts the squeeze on commodities like gold, silver and oil. This hurts energy stocks, but on the other hand, cheaper gasoline frees up money for consumers to shop more, and that’s good for retail stocks.

The Strong Dollar Trade is still on, but the ripple effects have spread further out. The most startling consequence is the effect on the Russian economy. Vladimir Putin’s soft autocracy has been aided by a long-term rise in energy prices. To the average Russian, his bluster delivered peace and prosperity. Then he annexed Crimea and began his ongoing shadow war in Ukraine. Now energy prices are no longer rising. The U.S. and our allies have responded with sanctions against Russia, and they’ve started to hurt. Even worse than any sanctions we’ve imposed against Russia is the collapsing price of oil. The Russian government estimates that the impact of cheap oil is more than twice that of the sanctions.

As a result of all this, the Russian currency, the ruble, has been getting crushed on the forex market. In July, a ruble was worth 2.9 cents. Today it’s down to 1.8 cents. In 2008, the ruble was going for 4.3 cents. The decline has been stunning. President Putin has responded by taking full responsibility. No, I’m kidding. He’s blamed “speculators.” Since July, the Russia ETF ($RSX) is down by 30%. (But stay away! Down isn’t the same thing as cheap.)

It’s important to keep in mind that Russia has an extraction-based economy. Their adventurism in the 1970s was funded by a bull market in gold and oil (ending in a hostile takeover of Afghanistan). The long commodity slide of the 1980s probably helped speed up the dissolution of the Soviet Union. The Russian economy is in much better shape than it was during the 1998 financial crisis, when the Russians devalued the ruble and defaulted on their debt. Russia isn’t as heavily indebted; plus they have foreign currency reserves standing by to defend the ruble—though for how long is another matter. Their economy is slowing down, and inflation is on the rise. I don’t see things getting better soon.

The outlook for oil continues to be bleak. What happened last week was fascinating as OPEC got together in Vienna. With oil dropping, some observers though OPEC would respond by cutting back on production. They didn’t, and that led to the oil crash last Friday.

Why did OPEC balk? There are a lot of theories. Some say the Saudis want to hurt the Russians, and possibly the Iranians. I can see that. Others think it’s a swipe at the U.S. shale market. The Shale Revolution has upended the world energy market, since we’re no longer so dependent on foreign oil.

The problem is that Saudi Arabia has a very low breakeven point ($5 to $6 per barrel), while American shale’s is fairly high. Perhaps the Saudis want to bring oil down low enough to make shale uneconomical. In any case, many major energy stocks are well off their highs. Apache ($APA) is down 39%; Haliburton ($HAL) is off by 45%. Airlines, which are major energy consumers, have been some of the strongest stocks around. The Airline Index is up 35% since mid-October.

Another wrinkle is that a lot of energy companies are over-represented in the junk-bond market. That was the way they could get funding to extract shale. As a result, the spread between junk-bond yields and higher-grade debt has widened. It’s still somewhat tame, but it’s interesting to see the connections in financial markets. We had a real-estate bust, and we had little idea of exactly who was exposed. I’m reminded of the little towns in Norway that were nearly ruined after they invested in complex instruments tied to the American mortgage market. Sometimes finance is like a giant game of dominos where you don’t know which domino is next to which—that is, until they fall.

There’s concern that a worsening market for low-grade debt could hurt the stock market since so much of the bull market has been funded by debt-fueled share buybacks. I doubt that will be a major factor, but undoubtedly, it will impact marginal borrowers.

Another impact of cheaper oil is that it helps the consumer sector. Prices at the pump are the lowest they’ve been since 2010. For many Americans, any savings there goes right into more shopping. Just look at Walmart ($WMT). The stock jumped 20% in six weeks. Nike ($NKE) seems to rise every day. On our Buy List, Ross Stores ($ROST) and Bed Bath & Beyond ($BBBY) have rebounded nicely (I’ll have more on them in the next section). Consumer staples have been leading the market since the summer. While consumer-discretionary stocks have been weak most of the year, they’ve picked up strongly in the last month. The recovery is beginning to filter down to the level of consumers.

The stronger dollar also acts to hold down inflation. There’s been absolutely no evidence of inflation, so that may give the Federal Reserve more breathing room to help the economy. If inflation is still holding between 1.5% and 2.0%, there will be little demand to raise rates. As a result, the 30-year yield is back under 3%, while mortgage rates are at their lowest levels in 18 months. That will certainly help housing. Mid-curve yields haven’t budged, so the spread between the 5-year and 30-year Treasuries has narrowed to 135 basis points. The spread hasn’t been that narrow since the bull market began.

For now, we should continue to focus on high-quality stocks like the ones on our Buy List. Earnings season doesn’t start for several more weeks, but we want to watch out for more signs of happy consumers. This could be a very good holiday season for businesses. Now let’s take a look at some recent news affecting our stocks.

Buy List Updates

Through Thursday, our Buy List is up 9.97% for the year, trailing the S&P 500’s YTD gain of 12.10% (that doesn’t include dividends). We’ve beaten the market for the last seven years, and sadly, it looks like that streak will come to and end.

While I’m disappointed, I have absolutely no plans to alter our long-term high-quality strategy. It may lose to the market here and there, but it works. Actually, most of our underperformance came earlier this year, during the spring. The good news is that we’ve been doing very well this quarter. Since September 30, our Buy List is up 8.00% compared with 5.05% for the S&P 500. Yes, we’re losing to the market YTD, but not by much (a deficit of about 2.1%), and we’re still making a solid profit. I’ll have the complete stats on our Buy List at the end of year. Now let’s look at some recent news impacting our stocks.

Express Scripts ($ESRX) has been on fire lately. The pharmacy-benefits manager tends to be quiet, but don’t let that fool you: they’re quite profitable. The stock closed higher on 12-straight trading sessions from November 17 to December 3. The shares are now up more than 22% from their October low.

So what’s the catalyst for the surge? Beats me. The only new story is that Warren Buffett recently started a position in ESRX. That’s certainly comforting. This was his only new position during Q3. In earning news, ESRX met expectations for Q3, and their guidance for Q4 was also within expectations. Personally, I’m fine with meeting expectations. It’s more important to me that a company hits the marks they state publicly rather than consistently low-balling us. ESRX is a classic slow-and-steady stock. This week, I’m raising our Buy Below on Express Scripts to $87 per share.

In the CWS Market Review from November 14, I told you to expect a dividend increase soon from Stryker ($SYK). I said I expected the quarterly payout to rise from 31.5 cents per share to 33 or 34 cents per share. I was close. This week, Stryker announced they’re raising their quarterly dividend to 34.5 cents per share. That’s a 13% increase. Given the new dividend, SYK now yields 1.46%.

Six months ago, after Medtronic ($MDT) announced their tax-inversion deal with Covidien, I said to keep an eye on Stryker and Smith & Nephew ($SNN). Sure enough, SYK is now said to be considering a tax inversion with SNN. I think a deal could come soon. It makes a lot of sense. I’m raising our Buy Below on Stryker to $98 per share.

As always, let me remind you: don’t chase after good stocks. Be patient and wait for good prices. Warren Buffett described investing as being like a batter standing at the plate who can wait for an endless number of pitches before swinging at a nice fat one coming down the middle. Keep that in mind.

CR Bard ($BCR) keeps on charging! It’s now our third-best performer this year. Shares of BCR are up nearly 29% this year. I’m raising the Buy Below to $175 per share, which is fairly tight. I’m expecting another good earnings report next month.

I also want to raise the Buy Below of our big bank, Wells Fargo ($WFC). I think Wells will raise its dividend again this spring. The stock is good for conservative investors. It tends not to move around so much. Wells is going for less than 13 times next year’s estimate. That’s a good deal. I’m bumping up my Buy Below on Wells to $57 per share.

Last month, for the first time in nearly 15 years, shares of Microsoft ($MSFT) pierced $50 per share. The stock reached its all-time high of $59.97 on December 30, 1999. We’re actually not that far from topping that. MSFT been a great stock for us this year. For now, I’m keeping our Buy Below at $50 per share.

Our two retailers, Bed Bath & Beyond ($BBBY) and Ross Stores ($ROST), have been performing quite well lately. The drop in oil prices certainly helps shoppers. I also think investors expect a strong holiday season for retail (we’ll get an important report on retail sales next week). This week, I’m raising my Buy Below on BBBY to $74 per share, and on Ross Stores to $93 per share. Both are excellent stocks.

One quick note: Even though BBBY’s fiscal third quarter ended last week, the company won’t report earnings until January 8. Our other Buy List stock on the November reporting cycle is Oracle ($ORCL). They’ll report earnings on December 17. That’s the only Buy List earnings report we’ll have this month.

I also wanted to touch on Ford Motor ($F). The stock recently traded over $16 per share for the first time since September. This year has been a rough one for Ford, but the payoff isn’t far away. Don’t expect much from the Q4 earnings report next month, but the fiscal Q1 report this spring will reflect Ford’s new business strategy. A lot of investors aren’t believers. Ford currently trades at less than 10 times next year’s earnings. I think Ford has made a lot of smart moves. Ford Motor remains a buy up to $17 per share.

That’s all for now. The big jobs report will be later this morning. We’ve had a nice run of good jobs reports, and I expect the trend to continue. The weak spot has been wage growth, so hopefully we’ll see better news there. Next week, we’ll get important reports on retail sales. It will be interesting to see how strong the consumer is heading into the holiday season. Also, don’t forget that I’ll unveil the 2015 Buy List in two weeks. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: December 5, 2014

Eddy Elfenbein, December 5th, 2014 at 6:47 amECB’s Wiedmann Says Monetary Policy Too Expansive for Germany

Yen’s Plunge Risks Haven Status as Bonds Are Worst

Natural Gas Stocks Are ‘Strong Buys’ As Seasonal Demand Is Due To Spike

U.S. Jobless Claims Fall, Unwind Prior Week’s Increase

Starbucks Aims to Double U.S. Food Sales

Uber Raises $1.2 Billion, Putting Its Value at $40 Billion

Amazon Now Serves Takeout – And Diapers

Cadillac to Build 95% Cars Locally by 2018 for China Push

Low-Wage Workers Stage Strikes and Protests Over Pay

Sears Reports Wider Loss But Better LIquidity

Barnes & Noble and Microsoft End Nook Partnership

Time Is on AT&T’s Side in Wait for Slim’s Mexico Assets

Jeff Miller: Keeping Investors Scared Witless

Cullen Roche: The Cure Depends On The Disease

Be sure to follow me on Twitter.

-

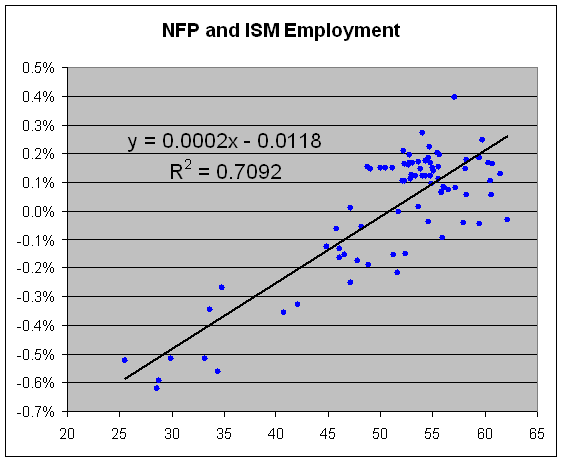

Predicting NFP

Eddy Elfenbein, December 4th, 2014 at 2:52 pmTomorrow is the big November jobs report. Yesterday we got the ISM Employment report which came in at 54.9.

Since the beginning of 2008, the ISM Employment numbers have been decently correlated with monthly NFP growth (R-squared of about 0.71).

Going by the recent regression, 54.9 translates to a gain of 131,000 payroll jobs. That’s well below expectations. Bear in mind that there’s a sizeable error spread is this analysis.

-

Morning News: December 4, 2014

Eddy Elfenbein, December 4th, 2014 at 7:08 amBank of England Keeps Rates on Hold at Record Low

British Government Proposes a ‘Google Tax’

Putin Vows to Punish Speculators Pushing Down Ruble’s Value

Fed’s Beige Book: Hiring Picks Up Broadly, but Wage Growth Is Muted

Obama Offers Candor, Insights in Q&A With Top CEOs

ADP Says Companies in U.S. Added 208,000 Workers in November

Shareholders Meeting Spotlights the New Microsoft

Intel to Invest $1.6 Billion in China Factory

Executives at Samsung Unit Relieved From Posts

Sears 3Q Loss Widens as Retailer Reshapes Itself

SoftBank Invests $250 Million in Uber Competitor GrabTaxi

Best Buy to Sell China Business, Focus on North America

Booyah! Activist Investor Hurls Purple Prose at Jim Cramer

Credit Writedowns: How Might a China Slowdown Affect the World?

Yes, the American Consumer is Back, Epilogue

Be sure to follow me on Twitter.

-

Stryker Raises Dividend 13%

Eddy Elfenbein, December 3rd, 2014 at 4:34 pmStryker ($SYK) announced today that they’re raising their quarterly dividend by 13%. The payout will rise from 30.5 to 34.5 cents per share. The dividend is payable on January 30, 2015, to shareholders of record at the close of business on December 31, 2014. Based on today’s close and the new dividend, shares of SYK now yield 1.46%.

-

Morning News: December 3, 2014

Eddy Elfenbein, December 3rd, 2014 at 6:53 amAnother Chart Piling Pressure on ECB: Producer Prices Slide Most in a Year

Rouble Sinks to New Lows as Russia’s Problems Mount

Australia Enters Income Recession, Dollar Dives as Economy Stalls

Oil-Price Drop Adds New Element to Middle East Tensions

Income Gap Shrinks in Chile, for Better or Worse

US Federal Reserve’s Dudley Says Oil Price Drop a Net Benefit For U.S.

Business Chiefs to Press Obama Over Tax Stalemate

GM, Chrysler, Honda U.S. Sales Rise in November

Bezos H’app’y With Washington Post Purchase

IBM Signs $1.25 Billion WPP Cloud Deal and Says More Coming

Hershey Explores Removing High-Fructose Corn Syrup

Takata Rejects U.S. Demand for Nationwide Air-Bag Recall

Hackers Pirate Sony Films and Leak Studio Salaries

Epicurean Dealmaker: Show Me the Money

Howard Lindzon: Predictions for 2015 …Continued…Web Video and Financial Web

Be sure to follow me on Twitter.

-

There’s No Such Thing as Being Market Neutral

Eddy Elfenbein, December 2nd, 2014 at 1:07 pmOne of the important truths about investing is that there’s no such thing as truly being “market neutral.” Any investment takes some sort of angle on the market. Even doing nothing and having your money sit in the bank is, ironically, playing some market.

This year, actively managed funds are having their worst year against the market in 30 years. Lipper reports that 85% of actively managed large-cap funds are lagging their benchmark.

But that’s not due to managers being bad at their jobs. At least, that’s not the only reason. What we don’t often hear is that the relative performance of active managers is very strongly correlated with the relative performance of small-cap stocks (yes, even among large-cap funds). Actively managed funds tend to be over-weighted with small-cap stocks. When small-caps soar, active managers look smart. But when they break down, they don’t look so good.

But it doesn’t end there. The relative performance of small-caps is semi-strongly correlated with the U.S. dollar. When the dollar rises, small-caps lag. Putting it all together, actively managed funds are having a bad year partially related to the dollar’s rally. That, in turn, is related to efforts in Japan and Europe to weaken their currencies.

Everything’s related to everything else.

-

10 Straight Rallies for ESRX

Eddy Elfenbein, December 2nd, 2014 at 12:26 pmThe stock market is gaining ground today after yesterday’s plunge. Of course, by plunge, I mean a very modest decline. But given this market’s hyper-low volatility, yesterday’s drop of 0.68% was the S&P 500’s worst daily decline since October 22.

Stryker (SYK) has been in the news lately as it seems they’re ready to strike for Smith & Nephew (SNN). I knew some kind of deal was coming, but I wasn’t sure what it would be. Shares of SNN gapped up to $37 per share last week, but have since slid back. Meanwhile, SYK is up to a new 52-week high. Expect to see a dividend increase soon.

Ford (F) reported another blah month for sales for November. Again, I’m not worried since consumers are holding back waiting for the new line of trucks to hit. The stock is holding up well and is closing in on $16 per share.

Shares of Express Scripts (ESRX) have closed higher for ten straight days, and they’re up again today.

This morning, the Census Bureau reported that October construction spending rose 1.1%. Despite the increase, this is one data series that’s not even close to its pre-crash high.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His