Author Archive

-

Apple’s IPO: 34 Years Ago Today

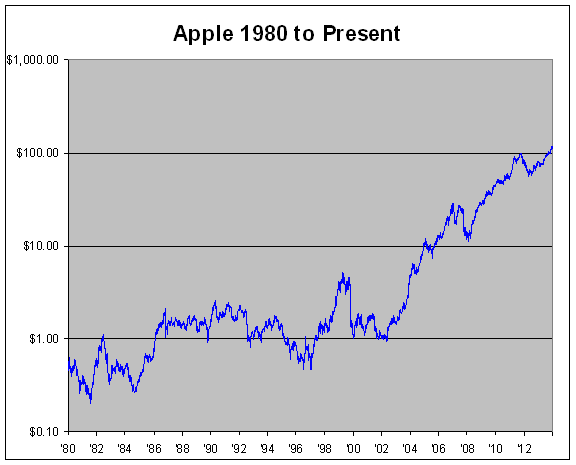

Eddy Elfenbein, December 12th, 2014 at 9:52 amThirty four years ago today, Apple Computer ($AAPL) went public. Today, the company is officially just Apple Inc. The offering was for $22 per share. Since then, Apple has split four times; three times 2-for-1 and once 7-for-1. That adds up to 56-for-1 which means the $22 offering is 39.3 cents split adjusted.

This may sound surprising, but Apple wasn’t a hit. By mid-1982, the shares were going for half the offering price. The stock did have its moment in the sun: In the 26 months prior to the 1987 crash, shares of Apple rose eight-fold.

But overall, Apple was not a hot stock. At its low point in 2003, Apple was lower than where it had been in 1983. Think about that! Twenty years of no gain, and this was well after Steve Jobs had returned.

But in 2003, Apple started one of the most amazing rallies in Wall Street history. In less than ten years, the stock jumped more than 100-fold. To be precise, Apple rose 107-fold (10,603%) in nine years and five months. That includes a brutal 60% drop during the Financial Crisis.

Apple gained back what it lost but suffered another painful correction. From September 2012 to April 2013, Apple shed 44%. That was when we heard the refrain, “Apple doesn’t know how to innovate anymore.” Once again, Apple made back everything it had lost.

Now here are some numbers. Measuring from the offering price 34 years ago, Apple has gained 28,412%. Annualized, that’s 18.1%.

Apple’s single-worst day came on September 29, 2000 when the stock plunged 51.9%. The catalyst was that Apple said they were going to miss earnings. That was also Apple’s highest volume day. It traded over 1.8 billion shares that day.

Apple has suffered other big drops. On the day of the 1987 crash, Apple fell 24.4%. The stock has fallen more than 10% in a single day 26 times, which is nearly once per year.

Apple’s single-best day came on August 6, 1997 when it soared 33.2%. That was the day Steve Jobs announced at a MacWorld trade show that Microsoft was investing $150 million in Apple preferred stock. That moved saved Apple. At the time, people in the crowd booed. Here’s a story from the Seattle Times about the announcement.

A lot of people forget that Apple used to pay a dividend many years ago. They introduced a small quarterly dividend in 1987. Apple raised it four times, and then kept it the same for five years until it expired in 1995. Two years ago, Apple resumed paying a dividend. The current quarterly dividend is 47 cents per share which is a 120% return on the IPO price.

When Apple was founded on April 1, 1976, there were three founders; Steve Wozniak, Steve Jobs and Ronald Wayne. On April 11, Wayne sold his 10% back to the Steves for $800. Apple’s current market value is $655 billion making it the most valuable company in the world.

-

CWS Market Review – December 12, 2014

Eddy Elfenbein, December 12th, 2014 at 7:09 am“Successful investing is anticipating the anticipations of others.” – J.M. Keynes

Before I get into this week’s issue, I want to remind you that I’ll be unveiling the 2015 Buy List in next week’s CWS Market Review. As always, I’ll be adding five new stocks and removing five current ones.

For tracking purposes, the “buy prices” of each stock will be the closing prices on December 31, 2014. The exchanges will be closed on New Year’s Day, so the new Buy List will go into effect on Friday, January 2. Once the Buy List is set, it’s locked and sealed. I won’t be able to make any changes until next December.

Now let’s look at the market’s latest doings. Last Friday, the Dow came within inches of cracking 18,000 for the first time in history. But the market followed up by dropping the next three days. It could have been a fourth as the indexes dropped quickly going into Thursday’s close, but we held on to modest gains.

The major development continues to be the remarkable decline in the price of oil. What started out as a modest pullback has turned into a full-fledged rout. I’m ready to say it out loud: “OPEC is dead!” On Thursday, oil dropped below $60 per barrel for the first time in five years. I don’t think people are surprised that oil has fallen, but nobody expected it to fall this much this quickly. Less than six months ago, oil was going for $107 per barrel.

What makes the falloff in crude so important is that much of the world economy had been based on oil’s being worth around 80% more than it currently is. I’m not exaggerating when I say that the math of the entire world economy has shifted. In this week’s issue, we’ll look at what the fallout is. We’ll also take a look at the recent news from eBay ($EBAY), and we’ll preview next week’s earnings report from Oracle ($ORCL). But first, let’s take a closer look at last week’s jobs report and what it means for investors.

The Economy Created 321,000 Jobs Last Month

Last Friday, the Labor Department reported that the U.S. economy created 321,000 net new jobs last month. That was well above expectations, and it was one of the best jobs reports in years. The unemployment rate is now down to 5.8%. I was pleased to finally see some real improvements in “discouraged workers” (folks who had left the workforce entirely). There’s also some evidence to indicate that wages might be growing as well.

What’s the impact of an improving jobs market on the stock market? There are several factors at work. For one, it helps consumer stocks. More people with more jobs being paid higher wages means more shoppers. Since the beginning of August, retail stocks have done twice as well as the rest of the market. On Thursday, the Commerce Department reported that retail sales rose 0.7% in November. That’s the best report in eight months. (By the way, ignore any discussion of the impact of Black Friday. It’s really not that important.)

The retail sales report for October was good as well. Clearly, cheaper fuel prices are helping the gains here, and this portends a strong holiday shopping season. On our Buy List, Ross Stores ($ROST) hit another new high on Thursday.

An improving jobs market is also good for financial stocks. Obviously, more people working means a lower default rate. On a relative-strength basis, financial stocks have been doing very well this month. Wells Fargo ($WFC), our favorite big bank, is close to a new 52-week high. The better jobs market also has a major impact on homebuilding stocks. The homebuilders had been lagging the broader market since early 2013. Only in the last two months have they resumed leading the market. I think this trend will continue. Mortgage rates are still holding below 4%.

Speaking of mortgage rates, the recent behavior of the bond market has been interesting. Bond traders were largely unimpressed with last week’s jobs report. Yields ticked up for a bit, but the yield on the 10-year is back below 2.2%. Interestingly, the yield on shorter-ranging debt is starting to creep higher. The yield on the one-year Treasury has doubled in the past few weeks. Of course, by doubling, I mean going from 0.1% to 0.2%. Still, the one-, two- and three-year Treasuries are all near three-year highs, while longer-term yields have trended lower. This means that the yield curve is getting narrower.

One of my favorite economic indicators to watch is the spread between the two- and ten-year Treasuries. Whenever the 2/10 spread turns flat or negative, the odds that a recession will soon follow are quite high. Since the beginning of this year, the 2/10 spread has narrowed by more than 100 basis points. (One basis point is bond-nerd shorthand for 0.01%.) The 2/10 spread is now down to 157 basis points, which is still quite wide, so I doubt we’re in immediate danger of a recession. The 2/10 spread hasn’t dipped below 120 basis points in nearly seven years.

To me, this indicates that bond traders truly expect the Fed to raise interest rates sometime next year. This is also why the dollar has been rallying. As long as the yield curve remains relatively wide, stocks are the best place to be. But this won’t last forever. To borrow from Churchill, the narrowing of the spread isn’t the beginning of the end for stocks, but it is the end of the beginning. Now let’s look at the stunning drop in oil.

OPEC is Dead

On Thursday, the price of West Texas Intermediate Crude dropped below $60 per barrel for the first time since July 2009. This is the biggest fall since the financial crisis. The difference this time is that it’s not about demand—it’s about supply and demand.

Of course, the tremendous growth of U.S. shale has roiled oil. President Rouhani of Iran said that the drop in oil is a conspiracy against the Muslim world. (I’m not making that up. He really said that.) Apparently no one told the Saudis, because they seem perfectly willing to stand by and watch oil fall.

The fact is that OPEC, for all intents and purposes, is dead. Killed by shale. OPEC simply doesn’t have the pricing power they used to. If a cartel can’t do that, what’s the point? The U.S is rapidly becoming energy-independent. Plus, the U.S. economy is much more efficient than it used to be. Twenty years ago, the U.S. consumed 1,760 barrels of oil for every $1 billion in GDP. Today that’s down to 1,178 barrels. On top of that, China’s economy appears to be slowing, so that’s pinching demand as well. There’s talk that oil could fall as low as $40 per barrel. Wow!

Naturally, the strong dollar is playing a major role as well. The greenback just backed off a two-year high against the euro and a seven-year high against the yen. Bond yields in Europe aren’t just low—they’re absurdly low. The yield on the German 10-year bond got down to 0.68%. With falling oil, there’s now fear that Europe might experience deflation. That would be more ammo for Mario Draghi to start his own QE program. The euro might be headed a lot lower.

The oil bear is weighing heavily on Russia. The ruble is looking more like rubble. Russia estimates that inflation will hit 10% next year. The Russian Fed raised interest rates again this week, but the forex market just laughed at them. I don’t blame them. Despite a lot of talk, the Bank of Russia simply isn’t serious about defending the ruble. The BOR raised rates by 1% to 10.5%. Please. If they’re serious, they would have raised rates by 2% or 3%. That’s what needs to be done.

The impact of lower oil can be seen in so many different areas. Tesla ($TSLA), the headline-grabbing electric-car stock, is 28% off its high from September. Energy stocks as a whole have been getting clobbered. The Energy Sector ETF ($XLE) was over $100 per share in July. This week, the XLE dipped below $75 per share.

My advice: Don’t be fooled into thinking energy stocks are cheap. A lower stock simply means it’s cheaper than where it was, not that it’s cheap in an absolute sense. I’m still leery of most energy stocks. I expect oil to continue to fall. The forces working against oil are just too strong. This is good news for many consumer stocks. Now let’s look at one of our favorite consumer stocks, eBay.

eBay is a Buy up to $60 per Share

Shares of eBay ($EBAY) got a nice bounce on Thursday. Unfortunately, the good news was rather unpleasant news. The Wall Street Journal reported that eBay is considering laying off thousands of workers next year in preparation for their spin-off of PayPal. According to the WSJ, the online-auction house is looking to shed 3,000 positions, which is about 10% of their workforce. The cuts will mainly impact eBay’s marketplace division, which runs eBay.com and StubHub.

Personally, I’m conflicted about news items such as this. I can’t help but think of the employees who are laid off. However, I have to concede the reality of the situation; eBay is planning to be a stand-alone company, and they need to keep overhead as low as possible. I also realize that the market very much approves of this kind of news. Shares of EBAY jumped 2.7% on Thursday to reach a nine-month high. This week, I’m raising my Buy Below on eBay to $60 per share.

Oracle Earnings Preview

Oracle ($ORCL) is due to report fiscal Q2 earnings on Wednesday, December 17 after the closing bell. I wasn’t exactly thrilled with Oracle’s last earnings report. The company missed earnings by two cents per share (62 cents versus a 64-cent estimate). This was the third quarter in a row in which Oracle missed estimates. But not everything in the report was bad; Oracle’s cloud business is doing quite well. The hardware business, however, continues to be a weak spot.

The biggest news in the last earnings report wasn’t earnings—it was that Larry Ellison said he’s stepping down as CEO. In his place, Mark Hurd and Safra Catz are now co-CEOs. In my opinion, that’s a big mistake. These things sound good on paper, but I’m convinced that any dual CEO scheme is a bad idea. I predict that within two years, there will only be one CEO, and it will probably be Mark Hurd.

Oracle told us to expect Q2 earnings to range between 66 and 70 cents per share. Wall Street expects 69 cents. According to my numbers, that’s about right. Oracle is coming through a difficult period for them, but I think things are turning around. The company should earn at least $3 per share for this fiscal year, which ends in May. That means that Oracle is going for about 13.6 times this year’s earnings. That’s not bad. Plus, I think Oracle may raise its dividend soon. Oracle remains a buy up to $42 per share.

That’s all for now. The Federal Reserve meets again next week. The policy statement will be out on Wednesday afternoon. It will be interesting to hear of any changes in their thinking. We’re also going to get key reports on inflation, industrial production and housing starts. Also, Oracle will report earnings after the close on Wednesday. Don’t forget: Next week, I’ll unveil the Buy List for 2015. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: December 12, 2014

Eddy Elfenbein, December 12th, 2014 at 6:55 amTrillion Dollar IT Trade Deal on a Knife Edge at the WTO

China’s Slowdown Deepens as Factory Output Growth Wanes

Greek Borrowing Costs at Most Since 2012 Amid Political Turmoil

Solar Rises in Malaysia During Trade Wars Over Panels

Global Oil Demand to Slow Despite Plunging Prices

How America Is Kicking Its Oil Habit

U.S. Authorities Face New Fallout From Insider Trading Ruling

U.S. Spending Fight Moves to Senate After Narrow House Passage

Delta Expects Profit Boost From Lower Fuel Prices

Chinese Search Engine Baidu to Invest in Uber

Ten Banks Broke Analyst Rules in Rush to Win Work With Toys R Us

SeaWorld Dumps Its CEO: Don’t Just Blame Blackfish

Cullen Roche: Is Technology Making Us Worse Investors?

Joshua Brown: Get to Know Lending Club

Be sure to follow me on Twitter.

-

Morning News: December 11, 2014

Eddy Elfenbein, December 11th, 2014 at 6:55 amCheap Loans From E.C.B. Get Tepid Response Among Eurozone Banks

Russia Inflation to Hit 10% By 2015, Growth Flat

Carney Wants Fed-Style Schedule as Part of BOE Decision Revamp

Central Banks’ Decisions Support FX Direction

Fed Proposes Extra Capital Cushion For Eight Big U.S. Banks

Fed Bubble Bursts in $550 Billion of Energy Debt: Credit Markets

Oil Trades Near 5-Year Low as Saudis Question Need to Cut Output

FAA’s Treatment Of Amazon Proves Congress Must Act Or Companies Will Take Drone Research Abroad

The Mergers and Acquisitions Cycle: Buy. Divide. Conquer.

Lending Club Set to Debut, And Industry Is Watching

Airbus Management Seek to Halt Share Price Slide

Wal-Mart Says Found China Pricing Discrepancies in 2011

Walgreen CEO Wasson To Step Down

Jeff Carter: Why Is There A Bubble?

Jeff Miller: Some Crucial Facts About Energy

Be sure to follow me on Twitter.

-

Oil Hits Five-Year Low

Eddy Elfenbein, December 10th, 2014 at 10:43 pmThe stock market had a terrible day today. The S&P 500 lost 1.64%. That’s the worst day in nearly two months. In fact, the loss is more than twice as much as the second-biggest loss over that time.

The worst damage was among energy stocks. The Energy Sector of the S&P 500 was down more than 3%. Small-caps were also hit hard. Outside of energy, it was a rough day but not too bad. Defensive stocks like staples and utes were down the least. Of course, that’s why they’re defensives.

All 20 stocks on our Buy List were down for the day, but thanks to not having any energy stocks, we outperformed the S&P 500 by 0.11% today. The selling in oil continues. Oil dropped more than $2 a barrel today to close at $61.22. At one point, it got as low at $60.43 per barrel. This is the lowest oil has been since July 2009. It’s interesting to see that Tesla (TSLA) has been falling as well since lower gas means less demand for alternatives.

eBay ($EBAY) made some news today when they said they’re planning on cutting 3,000 jobs next year to prepare for the PayPal spinoff. That’s about 10% of their workforce.

-

Morning News: December 10, 2014

Eddy Elfenbein, December 10th, 2014 at 7:08 amAsian Stocks Mixed on Greece Anxiety

Chinese Inflation Slows to Five-Year Low

China Seeking Foreigners to Tame Stock Market Swings

HK Blue Chips Overlooked in Shanghai Stampede

KFC Calls on Chinese Diners to Inspect Its Kitchen

Feds Propose Taxing Marijuana, True Cash Crop

Citigroup Is Catching Up To Its Peers

Uber Sued by San Francisco, Los Angeles Prosecutors

Airlines Profit Records Seen Prolonged on Oil Price Drop

BP Expects $1 Billion Job Cuts Charge

Costco Quarterly Profit Tops Estimates

Can Cutting Subscriber Bills In Half Solve Sprint’s Problems?

Earnings Miss Hammers Krispy Kreme: Should You Be A Long-Term Buyer?

Joshua Brown: Long Bonds: Still Uncorrelated After All These Years

Cullen Roche: Prediction Penance

Be sure to follow me on Twitter.

-

Morning News: December 9, 2014

Eddy Elfenbein, December 9th, 2014 at 7:09 amWhy This Equity Investor is Backing Japan

U.K. Manufacturing Unexpectedly Posts First Drop Since May

Crisis Returns to Greece as PM Gambles on Bailout Endgame

Putin Plan to Ship Gas to Europe Via Turkey Seen as Unrealistic

Treasury Three-Year Yield Holds Above 1% Before $25 Billion Sale

How The Bankruptcy Code Should Treat All Derivatives

Crude Rebounds From Five-Year Low Amid Shale-Oil Spending Curbs

Supreme Court Rejects BP Appeal of Spill Settlement

Amazon Debuts ‘Make an Offer’ Haggling Option

Will Merck & Co. Still Celebrate Cubist Pharmaceuticals Acquisition After Hospira’s Court Win?

Change.org Gets $25 Million From Big Names

American Airlines Luring High-Flying Passengers With $2 Billion Upgrade of Planes, Clubs

U.S. Sues Deutsche Bank, Banks for $190 Million

Roger Nusbaum: The All Everything Portfolio? No Such Thing

Jeff Carter: So You Want to Start Angel Investing?

Be sure to follow me on Twitter.

-

More on Stocks on the Yield Spread

Eddy Elfenbein, December 8th, 2014 at 3:54 pmA few weeks ago, I wrote about how stocks have performed much better when the spread between the three-month Treasury yield and the 10-year Treasury yield is 121 or more basis points.

Denis Ouellet of Bear No Bull has delved further into this relationship. Check it out.

-

The Late-’90s Rally Started 20 Years Ago Today

Eddy Elfenbein, December 8th, 2014 at 3:20 pmTwenty years ago today, the S&P 500 closed at 445.45. From there, the index started a five-year rally that saw it jump by more than 240%. Even after the two major crashes of the 2000s, the market has still given investors a nice return over the last 20 years.

Some people may quibble with my choice of December 8 because that wasn’t the low point of 1994. However, it was after December 8 that the market started on a nearly uninterrupted tear.

From December 9, 1994 to last Friday, the Wilshire 5000 Total Return Index is up 600.4%. That’s 10.2% annualized. Inflation over the last 20 years is up 59.1%, or 2.3% annualized.

-

Morning News: December 8, 2014

Eddy Elfenbein, December 8th, 2014 at 6:55 amUK Rate Rise in 2015 to Test High-Debt Households

Bank for International Settlements Warns of Market Fragility Despite Bullish Mood

China Announces Record Trade Surplus of $54.47 Billion, Helped By Weak Oil Price

Japan’s Early Elections Are All About the Economy

NATO Seeks Weapons to Counter Russia’s Information War

Ruble’s Rout Is Tale of Failed Threats, Missteps

Crude Oil: A Bounce Is On The Horizon

As Gas Prices Go Down, Likelihood of Higher Gas Taxes Goes Up

Saint-Gobain to Buy Controlling Stake in Swiss Chemical Maker

The Founding Families of Infosys Just Offloaded $1 Billion of Their Shares

Why Cubist Pharmaceuticals Inc. Shares Soared in After-Hours Trading on Friday

Madison Backs Qatari Bid for Canary Wharf Owner Songbird

Grappling With the ‘Culture of Free’ in Napster’s Aftermath

Howard Lindzon: Predictions for 2015, Part I Part II Part III

Jeff Miller: Weighing the Week Ahead: Time for a Santa Claus Rally?

Be sure to follow me on Twitter.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His