Posts Tagged ‘mdt’

-

CWS Market Review – November 21, 2014

Eddy Elfenbein, November 21st, 2014 at 7:08 am“Become more humble as the market goes your way.” – Bernard Baruch

Before I get into this week’s CWS Market Review, I have two announcements. The first is that there will be no newsletter next week. It’s Thanksgiving, and I’m taking a little break. The second is that I’ll be unveiling next year’s Buy List in the CWS Market Review on December 19, 2014, which is four weeks from today.

As always, I’ll be adding five stocks and deleting five stocks. The 2015 Buy List won’t take effect until the start of trading in January. I like to announce the names a few days ahead of time so no one can claim the positions are somehow manipulated. Later on in today’s newsletter, I’ll give you a list of some stocks I’m thinking about adding or deleting.

Now…about this lethargic stock market. The recent market hasn’t merely been slow; it’s been one of the sleepiest markets in history. Every day, it seems, the indexes climb higher, but only microscopically. The S&P 500 just closed out a five-day run where it didn’t close higher or lower by more than 0.1%. That hasn’t happened in 50 years.

The S&P 500 hasn’t had a meaningful down day in nearly a month. The last time the index dropped by more than 0.3% (which isn’t that much) was on October 22. The S&P 500 has closed higher 19 times in the last 26 sessions, but most of those were very small increases. The index has now closed above its five-day moving average for an amazing 25 straight days. That’s the longest streak since 1986. On Thursday, the market closed at yet another all-time high.

I’m pleased to note that our Buy List continues to do well. We had two very good earnings reports this week. Medtronic jumped nearly 5% on Tuesday after it reported good earnings. Then on Thursday, Ross Stores handily beat Wall Street’s earnings consensus, and the shares are poised to move much higher. I’ll give the details on those in just a bit, but first let’s look at some ideas I’m considering for the 2015 Crossing Wall Street Buy List.

Potential Changes for Next Year’s Buy List

According to the rules of our Buy List, I select 20 stocks each year. The portfolio is then locked and sealed, and I can’t make any changes for the next 12 months. (This set-and-forget rule has probably helped me more than I realize, since it’s prevented me from dumping good names at the first sign of trouble.) Each year, I swap out five names, which means my annual portfolio turnover is just 25%.

Right now, the five names I’m considering for deletion are CA Technologies ($CA), DirecTV ($DTV), IBM ($IBM), McDonald’s ($MCD) and Medtronic ($MDT). This is just a preliminary list: there’s no guarantee that these will be the ones to be cut when I make the big announcement next month.

Let me run through some thoughts on each of the names.

We did very well with DirecTV ($DTV), and I was happy to have it on our Buy List. But now it’s time to say goodbye. If all goes according to plan, the company will soon be bought out by AT&T. I like AT&T, but I’d rather not have it on our Buy List.

Medtronic ($MDT) is in a similar position. The medical-device stock has done very well for us, and particularly well lately (I’ll discuss this week’s earnings report in a bit). But Medtronic is about to become a very different company from the one we originally bought. The Covidien deal is a gigantic undertaking. They’re basically doubling in size, and there will need to be a lot of cost-cutting. If all goes well, Medtronic will soon take the name Medtronic PLC and will be incorporated in Ireland.

IBM ($IBM) and McDonald’s ($MCD) are also problematic. I simply made a mistake with both stocks. I thought both stocks were turning around, but the problems are more serious than I imagined. I think the prospects for McDonald’s could improve, but it’s too early to say. Their sales are flat, while competitors like Chipotle are cranking same-store-sales growth of 20%. IBM made a series of errors, and I think there need to be some changes at the top. Frankly, I think the two companies share a trait: they aren’t sure what kind of business they want to be.

CA Technologies ($CA) may be the weakest of the bunch. Their sales are in a tailspin. I should have pulled the plug a long time ago. As an investor, I always need to be frank about my mistakes, and I missed how serious the problems were at CA.

Ten Possible Additions for Next Year’s Buy List

Here are ten stocks I’m strongly considering for next year’s Buy List:

Alliance Data Systems ($ADS)

Babcock & Wilcox ($BWC)

Cardtronics ($CATM)

Colgate-Palmolive ($CL)

FactSet Research Systems ($FDS)

Howard Hughes Corporation ($HHC)

SEI Investments ($SEIC)

Signature Bank ($SBNY)

Tupperware Brands ($TUP)

Westinghouse Air Brake Technologies ($WAB)

I reserve the right to change my mind over the next four weeks, but I can say that these ten stocks are under serious consideration for next year’s Buy List. I don’t want to go into more detail, though, until I’ve made my final decision. Now let’s look at some recent earnings news.

Medtronic Is a Buy up to $76 per Share

In last week’s CWS Market Review, I said that I didn’t expect a big earnings beat from Medtronic ($MDT), and I was right. On Tuesday, the medical-device maker reported fiscal Q2 earnings of 96 cents per share. That met expectations right on the nose. For comparison, the company earned 91 cents per share for last year’s Q2.

The important news is that Medtronic continues to do well. The company also took the opportunity to reiterate that the Covidien ($COV) deal is on track. They hope to close the deal by the beginning of next year. At that time, Medtronic will reincorporate in Ireland, and its new name will be Medtronic PLC. The deal is up for a shareholder vote on January 6. I think it will pass easily.

For Q2, quarterly sales came in at $4.37 billion, which was a shade more than the consensus of $4.36 billion. Medtronic also reiterated its full-year earnings outlook of $4.00 to $4.10 per share. Their fiscal year ends in April, and Medtronic has already made $1.89 for the first two quarters of this year. That means they see earnings ranging between $2.11 and $2.21 per share for the last six months of this fiscal year. Medtronic earned $2.03 for the back-half of FY 2014.

Omar Ishrak, Medtronic’s CEO, said, “Revenue growth was at the upper end of our full-year revenue outlook and within our mid-single digit baseline goal, reflecting the strong execution of our global organization.”

The shares popped 4.7% on Tuesday and reached a new all-time high price. In the last three years, Medtronic has gained more than 116% for us, compared with 72% for the S&P 500. As I said before, there’s a good chance that Medtronic won’t be on next year’s Buy List, but that’s due to the deal, and not to any business failure. This week, I’m raising my Buy Below on Medtronic to $76 per share.

Ross Stores Beat Earnings

In last week’s CWS Market Review, I wrote, “For Q3, Ross said it expects earnings to range between 83 and 87 cents per share. Oh, please. That’s almost certainly too low.” I was right again. The deep discounter earned 93 cents per share for its fiscal third quarter.

I wish I could say this was due to my supernatural powers to divine the future. I’m sad to say that I was simply looking at the numbers, and the math said Ross is doing just fine. Quarterly sales rose 8% to $2.599 billion. Same-store sales, which is the key number for retailers, were up by 4%. Ross continues to deliver.

The CEO said, “We are pleased with the better-than-expected sales and earnings we achieved in the third quarter. These results were driven by our ongoing ability to deliver compelling bargains to our customers, which drove above-plan sales gains and strong merchandise gross margins. Operating margin for the quarter grew 55 basis points due to a 40-basis-point improvement in cost of goods sold and a 15-basis-point decline in selling, general and administrative expenses.”

Now let’s look at their guidance. For Q4, which is the all-important holiday shopping season, Ross forecasts earnings between $1.05 and $1.09 per share. Ross earned $1.02 for last year’s Q4. For the entire year, Ross sees earnings ranging between $4.28 and $4.32 per share. That’s an increase of 10% to 11% over last year.

Ross Stores is an excellent example of our style of investing. The stock had a miserable first half of 2014. By July, shares of ROST had dropped below $62. The shares were down more than 17% on the year. But the numbers still looked good, and we held on. ROST has rallied strongly ever since. The shares are now up more than 11% for the year, which is just ahead of the S&P 500.

The stock looks to open higher on Friday morning. This week, I’m raising our Buy Below on Ross Stores to $91 per share.

That’s all for now. The stock market will be closed next Thursday for Thanksgiving. The market will close at 1 pm on Friday. This is usually the slowest trading day of the year. There’s not much reason for the market to be open, but the NYSE hates to have the exchange closed four days in a row. The only interesting economic report will come on Tuesday when we get the first revision to Q3 GDP. The initial report said that the economy grew by 3.5% for Q3. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

CWS Market Review – November 14, 2014

Eddy Elfenbein, November 14th, 2014 at 7:17 am“Things are almost never clear on Wall Street, or when they

are, then it’s too late to profit from them.” – Peter LynchConsider this fact: In the last four weeks, the value of the global stock market has increased by a staggering $3.4 trillion. For some reason, we were terrible investors in September and early-October, but we’ve been brilliant investors ever since.

Or…perhaps, the mood of investors turned on a dime. It’s hard to believe that only a few days ago, investors were scared out of their wits about impeding elections, a deteriorating economy in Europe and truly scary news about the Ebola virus. How times have changed!

Investors shook these fears off and the stock market rallied to new highs again this week. Through Tuesday, the S&P 500 hit record closing highs for five straight days. The index has now made 40 record highs this year. That compares with 45 record highs last year. The S&P 500 has closed higher 16 times in the last 21 trading days, and three of those five declines were pretty measly (less than 0.2%). In the last month, we’ve experienced only one meaningful daily decline. This has been a golden time for investors, although trading volume has been very low (some chart watchers say that’s a bad sign).

In this week’s CWS Market Review, we’ll take a closer look at what’s driving this market. The simple explanation is that what’s been happening is still happening, only more so. Don’t worry; I’ll explain what it all means in a bit. I’ll also review this past earnings season. Except for a few duds, this was a solid earnings season for our Buy List. I’ll also preview two Buy List reports coming our way next week. Yes, the October reporting cycle is already upon us. We also had another good jobs report last week. But first, let’s look at what’s driving this market.

What’s Driving this Market

This has been a fascinating rally of late because we can see several factors at work. The most important factor continues to be the strength of the U.S. dollar. I’m afraid I might sound like I’m discussing the same phenomenon each week, but the dollar’s impact is crucial to what’s impacting our portfolios.

Since the economy in Europe and Japan are still quite weak, the governments there are purposely trying to weaken their currencies. It’s not so much that the dollar is truly strong; it’s that the greenback is the tallest Munchkin in Munchkin Land. Of course with forex, that’s all that matters. The yen just dropped to a seven-year low against the dollar. It looks like the government is about to call snap elections there. The British pound recently fell to a 14-month low against the dollar.

One impact of the rising dollar is that it puts the squeeze on commodity prices. The price of gold recently fell to a four-year low. Gold has been in a near non-stop plunge over the last three years. Since its 2011 peak, gold has lost close to $800 per ounce. That’s not all. Crude oil has been falling as well. On Thursday, oil fell below $75 per barrel. For the first time since 2010, prices at the pump are below $3 per gallon.

One of the reasons for the drop in oil is that Saudi Arabia has stepped up production. Normally, the Saudis would try to curtail their output in an attempt to prop up prices. This is probably evidence of OPEC’s declining influence. We can also see that Energy stocks have been quite weak (see the chart below). Many of the large oil stocks have mostly sat out this rally. The Energy Sector ETF ($XLE) is down slightly for the year, while most other sectors have done quite well. We currently don’t have any Energy stocks on the Buy List so that’s been a big help. I don’t see a broad rally for the Energy sector starting anytime soon.

Lower gas prices have been a welcome relief for many consumers. Despite the growth in payrolls, workers haven’t seen any real improvement in their wages. Since 2007, median income is down by 5%. About 10% of retail sales goes towards gasoline so lower prices at the pump frees up more money for other items. On Thursday, Walmart ($WMT) impressed Wall Street by reporting earnings that topped the consensus figure by three cents per share. The stock jumped 4.7% on the day. Business has been going well for WMT lately. Next year, Walmart has a good chance of clearing $500 billion in annual revenue.

Walmart’s strength has been good news for our favorite retailers. Shares of Bed Bath & Beyond ($BBBY) breached $71 this week. The stock hasn’t been that high since January. Our other big retailer, Ross Stores ($ROST), is due to report its fiscal Q3 earnings on Thursday, November 20. This is for the quarter that ended in October. Like BBBY, Ross has been rallying strongly lately. The shares topped $83 on Thursday for a fresh 52-week high. It was only four months ago that Ross was languishing at $62 per share.

For ROST’s last earnings report in August, the deep discounter beat estimates by six cents per share. The stock jumped more than 7% the next day, and it has continued to rally. For Q3, Ross said it expects earnings to range between 83 and 87 cents per share. Oh, please. That’s almost certainly too low. (Ross tends to be conservative with its estimates.)

For Q4 (November, December and January), Ross expects to see earnings between $1.05 and $1.09 per share. Naturally, the holiday season is very important for any retailer. For this year, Ross sees earnings coming in between $4.18 and $4.26 per share. Ross is getting pricier but it’s far from outrageous. For now, I’m keeping our Buy Below tight, at $83 per share. If the results are good, I’ll raise the Buy Below. Ross Stores continues to be a solid stock. Our patience has paid off.

Finance and Healthcare Have Been the Leaders

The two sectors of the market that have taken the lead for the Strong Dollar Trade are Healthcare and Finance, although Healthcare’s big run has preceded the emergence of the Strong Dollar Trade. The Healthcare Sector ETF ($XLV) has been a steady winner since February 2011. The recent election results also gave a boost to many Healthcare names.

The Healthcare stocks on our Buy List have also been doing quite well. Stryker ($SYK), Medtronic ($MDT) and CR Bard ($BCR) all hit new 52-week highs on Thursday. All three stocks are also handily beating the market this year. The Buy List is overweighted with Healthcare and that’s been good for us this year.

Medtronic is due to report earnings on Tuesday, November 18. This will be for their fiscal second quarter. Three months ago, the medical device stock topped earnings by a penny per share. For Q1, revenue rose 4.7% to $4.27 billion, which was $20 million better than expectations. Medtronic had its strongest growth for U.S. medical devices in five years.

The best news for Medtronic recently was the result of last week’s election. While I caution investors not to let their politics interfere with their investments, it appears that Congress will try to repeal the medical devices tax. I can’t say if this will happen, but it’s interesting to note that shares of MDT bounced nicely the day after the election.

Medtronic has stood by its intended acquisition of Covidien ($COV). The company plans to rework the specifics so it can clear any new regulations concerning tax inversions. This week, the company also offered concessions to please EU regulators. Medtronic will restructure the financing for the $43 billion deal which will allow the American company to reincorporate in Ireland and thereby lower its tax bill.

Medtronic has said they see full-year earnings (ending in April) ranging between $4.00 and $4.15 per share. Wall Street currently expects Q2 earnings of 96 cents per share. I don’t expect a big earnings beat from Medtronic. Rather, I expect to see more steady growth. This is an ideal stock for conservative investors. Medtronic is a buy up to $70 per share. Again, I’ll raise the Buy Below if earnings are strong, but I caution you not to chase it. Disciplined investors wait for good stocks to come to them.

Financial stocks have been more of a direct beneficiary of the Strong Dollar Trade. The Financial sector has led the market since August 20, although many financials got dinged hard in early October.

Our big banking stock is Wells Fargo ($WFC), and that’s ridden the recent wave quite nicely. Shares of WFC touched a new high a few days ago. The bank’s earnings have been very good lately, and they’ve navigated a difficult time for the industry. Wells is by far the best-run big bank in the country. (By the way, I’m so happy we got rid of JPMorgan this year.) Wells Fargo is a buy up to $54 per share.

Survey of Q3 Earnings Season

Earnings season is just about done, so let’s look at where we stand. Of the 445 companies in the S&P 500 that have reported so far, 332 beat expectations, 73 missed and 40 met.

For Q3, the S&P 500 is on track to report operating earnings of $29.83 per share. That’s an index-adjusted number, and it represents an increase of 10.8% over last year’s Q3. (These numbers are from S&P and they sometimes differ from other news sources.) At the start of the year, Wall Street had been expecting $30.89 for Q3. The estimates gradually fell as the year wore on. I should add that estimates generally start out too high, and it’s common to see them fall as earnings day approaches.

Over the last four quarters, the S&P 500 has earned $114.74 per share, so the index is going for 17.8 times that. Wall Street currently expects Q4 earnings to come in at $31.13 per share. That would be an increase of 10.2% over last year’s Q4. I like to see these steady 10% to 12% increases.

Interestingly, the estimates for Q4 had been fairly stable for much of the year. At the beginning of 2014, Wall Street was expecting $32.17 for Q4. On September 30, the estimate had increased by a tiny bit to $32.24. Only recently have the numbers come down.

If the current Q4 estimate is accurate, it would bring full-year earnings to $117.62. That would be an increase of 9.6% over last year. I’m fine with that. Going by Thursday’s close, the S&P 500 is now up 10.33% this year. In other words, the S&P 500 has largely kept pace with earnings this year. Despite some careless talk of bubbles, valuations haven’t changed. I should add that dividend growth has mostly tracked share prices as well.

In other words, there’s no bubble. The threat to the market isn’t excess valuations. Rather, it’s the potential for lack of growth. I don’t see difficulties in the immediate horizon, but that could change. As long as rates stay low, and the economy expands, stocks are the place to be.

Buy List Updates

This week, for the first time since September, shares of Ford ($F) topped $15 per share. The company finally started production on its aluminum-based F-150 trucks. This could be a game changer for the industry. (I hate that cliché so forgive me, but it’s true in this case.) Ford is currently going for less than 10 times next year’s earnings. The automaker just reported very good sales growth in Europe, especially in Britain and Italy. Ford remains a good buy up to $17 per share.

Earlier I mentioned that Stryker ($SYK) reached a new 52-week high. I also expect to see Stryker increase its dividend soon. Last year’s increase came on December 4. The company currently pays 30.5 cents per share. I think that will go up to 33 to 34 cents per share. Stryker is a buy up to $90 per share.

That’s all for now. Next week, we’ll get important reports on Industrial Production and Capacity Utilization. On Wednesday, the Fed will release the minutes from the last FOMC meeting. That’s when the Fed decided to end Quantitative Easing. On Thursday, we’ll get the latest report on Consumer Inflation. I expect to see more evidence that the strong dollar is holding back prices. We’ll also get earnings reports from Medtronic and Ross Stores. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

CWS Market Review – October 10, 2014

Eddy Elfenbein, October 10th, 2014 at 7:07 am“There is scarcely an instance of a man who has made a

fortune by speculation and kept it.” – Andrew CarnegieThe stock market decided to get a whole lot more interesting this week. On Thursday, the S&P 500 fell 2.09% for its worst day in six months. This was surprising, considering how calm the markets had been. Earlier this year, there was a three-month stretch when the index never had a 1% day. Now it’s happened four times in the last five days.

During Thursday’s trading, the Volatility Index ($VIX) spiked to over 19. Just a few days ago, it was less than 12. In the last few issues, I’ve talked about the distorting impact that the strong dollar has had on the markets. Now we’re seeing some of the negative fallout. On Thursday, the S&P 500 closed at 1,928.21. That’s a two-month low, and it’s a loss of 4.13% from the all-time high close of September 18. (Notice how the spread between the daily high and low has gradually increased.)

That’s not a big loss, but remember, we haven’t had a 10% correction in three years. I should remind all investors that every few years, stocks go down. It’s just the nature of the beast. But now we’re in earnings season, and this is when every stock is judged by the market. For disciplined investors, we also want to pay close attention to the earnings guidance from our stocks.

In this week’s issue, I’ll walk you through what’s been roiling the market. I’ll also highlight three of our Buy List stocks which have earnings reports coming next week. For the broader market, I’m expecting a mild earnings season. Nothing great, but not terrible either. I’ll also have some updates on our Buy List stocks, but first, let’s look at what has the market so rattled lately.

Volatility Makes a Comeback this Week

Last Friday, the government reported that the U.S. economy created 248,000 jobs last month. That’s a pretty strong number. The Feds also revised higher the figures for July and August, and the unemployment rate dropped down to 5.9%. This was the first time the jobless rate has dipped below 6% since July 2008.

The market briefly enjoyed the good news, and the S&P 500 rallied back over 1,970, but it wasn’t to last. Stocks sunk lower on Monday and Tuesday, but the heated action came on Wednesday and Thursday.

Stocks started out poorly on Wednesday, but that afternoon, the Federal Reserve released the minutes from their last meeting. We never know exactly what happens behind the scenes at these meetings, but three weeks after each one, the Fed releases the minutes. In them, the Fed expressed some concerns about the rising dollar. While a rising dollar carries benefits, it can also impinge on growth and keep inflation down. The Fed has tried desperately to keep the economy afloat, and we know that inflation is running below their target, so you can see their concern.

So does this mean there’s a growing chorus of doves at the Fed? Not exactly. I have to mention that reading the minutes from any Fed meeting is an arcane study in indefinite pronouns; “some participants say” this or “others” say that. In this week’s minutes, the concerns about the strong dollar were aired by “some” and “a couple.” Well, a few of us have a number of concerns some of the time about several of these minutes. What exactly are they saying?

In any case, traders were quite pleased, and the market staged an impressive turnaround on Wednesday afternoon. In fact, it was the best day for the S&P 500 all year. I think they’re correct that the Fed has a bias towards keeping rates low, but we simply can’t say how much they’re weighing the impact of the strong dollar.

Then on Thursday, concerns from Europe sent our stocks lower again. Mario Draghi, the head of the ECB, is clearly frustrated with the European economy. He’s particularly worried about the threat of deflation. The German economy is moving backward and there are concerns about its impact here. The sanctions against Russia aren’t helping either. So we followed the best day of the year with the fourth-worst day of the year. Market historians often tell us that weird things happen in October.

The Fed’s minutes caused a brief pullback from the greenback, but the effects on the strong dollar trade are still evident. Small-caps are doing poorly. The relative strength of the Russell 2000 has been terrible. Gold has been awful, although it got a little bounce this week. Conversely, the dollar fell a little bit, but commodity stocks have lagged badly. The Energy Sector ETF ($XLE) has dropped from over $100 on July 24 to just under $85 on Thursday. The yield on the 10-year Treasury dropped to 2.33%, which is its lowest yield in more than 15 months. At the start of the year, the yield was near 3%. It’s not just Treasuries; 30-year fixed-rated mortgages are back below 4%.

Several of our Buy List stocks got hit hard this week, including some of my favorites. AFLAC ($AFL), CA Technologies ($CA) and Ford Motor ($F) all touched new 52-week lows this week. I was really surprised by the falloff in Ford. The stock had already turned south after the lower guidance, but the selling has continued. A few weeks ago, Ford was closing in on $18 per share, and this week, it dropped below $14 per share. This week, an analyst at Morgan Stanley downgraded the automakers, not because of any weakness in their operations, but because of lower gas prices. The analysts said that cheaper gasoline won’t cause such a rush of buyers to snatch up Ford’s new aluminum trucks. Frankly, I think he’s missing the larger picture. What Ford is doing could be a massive change for the industry. I apologize for the volatility, but I haven’t altered my outlook on Ford. If their forecast for next year is correct, Ford is going for a great price here.

What to do now: Investors should focus on earnings instead of day-to-day volatility. For Q3 earnings season, analysts currently expect profit growth of 4.9%. Three months ago, the expectation was for growth of 7.8%. As I said, I expect mild growth this season. Some of the most attractive Buy List stocks at the moment are Ford Motor ($F), AFLAC ($AFL), eBay ($EBAY), Cognizant ($CTSH) and Microsoft ($MSFT). Now let’s take a look at some earnings reports coming our way next week.

Three Buy List Earnings Reports Next Week

Next week is the start of earnings season for our Buy List. On Tuesday, Wells Fargo ($WFC) will become our first Buy List stock to report. Three months ago, the big bank earned $1.01 per share, which matched expectations. I’ve been impressed by how Wells has managed itself during an important juncture in the industry (see the chart below). Mortgage revenue has plunged, but Wells is well ahead of the curve. The bank has broadened its footprint in credit cards, cars loans and investment banking.

Wells Fargo has managed to increase its earnings for 18 quarters in a row. Until last quarter, they beat expectations for 10 quarters in a row. The consensus on Wall Street is for Wells to earn $1.02 per share for Q3. My numbers say that’s about right. Frankly, the stock isn’t that exciting right now, but that’s a plus in this market. The stock is currently going for 12.4 times earnings, which is quite reasonable. This is a good stock for conservative investors. In a downturn, WFC probably won’t fall as much as other stocks and the dividend is secure. Wells Fargo is a buy up to $54 per share.

On Wednesday, eBay ($EBAY) is due to report. The online auction house has had a rough year, although it’s improved since the spring. The big news recently was the announcement that they’re going to spin off PayPal next year. I think that’s a smart move, and I expect to hear more details about this on the conference call.

For Q2, eBay beat by a penny per share. They said they expect Q3 earnings to range between 65 and 67 cents per share. Since that range is so narrow, I’m assuming that’s what it will be. Honestly, I’m surprised eBay is still below $55 per share. The business looks pretty good right now, and naturally, a stronger economy would help.

For the entire year, eBay sees earnings coming in between $2.95 and $3.00 per share. They see revenues ranging between $18.0 billion and $18.3 billion. I’ll be curious to hear what they have to say about Q4 guidance. Wall Street expects 91 cents per share, but there’s a chance it could be higher. I’m keeping a fairly tight Buy Below here; eBay is a buy up to $55 per share. I may raise it if earnings and guidance are strong.

On Thursday, it’s Stryker’s ($SYK) turn. The orthopedic company rarely surprises us, but they did last earnings season when they lowered the high end of their full-year guidance by ten cents per share. For Q3, they see earnings ranging between $1.12 and $1.16 per share. I think there’s a good chance SYK can top that. For the full year, Stryker projects earnings between $4.75 and 4.80 per share.

I don’t always trust guidance from companies, but in Stryker’s case, I‘m more inclined to believe them. I should also point out that Stryker may be in the works for a merger. I’m not predicting anything will happen, but merger mania seems to be spreading across their industry. If the price is right, a deal might come about. Stryker is a buy up to $87 per share.

Buy List Updates

Shares of Bed Bath & Beyond ($BBBY) spiked higher on Tuesday after rumors broke that Carl Icahn had taken a position in the stock. Let me stress that there’s absolutely zero confirmation that the story is true.

Traders naturally prefer to move first and wait for facts later. Sometimes that works for you, and sometimes it doesn’t. This week, it worked in BBBY’s advantage. Later on in the week, the shares kept their heads while the rest of the market got shaky. I doubt Carl made any move into BBBY, but you never know. Either way, we’re in this for the long term. Despite all the drama in this stock, the company hasn’t altered its long-term guidance. Bed Bath & Beyond remains a buy up to $70 per share.

Earlier this year, Medtronic ($MDT) announced its big “tax inversion” deal with Covidien ($COV), a company based in Ireland. Recently, however, shares of Medtronic pulled back after the Obama administration announced new rules regarding such inversions. Some investors thought that might cause the deal to be scrapped. Not so.

This week, Medtronic said they’re reworking the deal to be in compliance with the new rules. The combined entity will be domiciled on the Emerald Isle, and they’ll probably be able to cut their tax bill as well.

Not to get too technical, but Medtronic was going to use their cash held outside the U.S., and loan that to Covidien to complete the deal. Now Medtronic will use cash from another source. I’ve been impressed by Medtronic’s insistence that they’re doing this deal for operational reasons, not solely for a cheaper tax bill. You’d expect them to say that publicly, but now we have further proof that both companies are on board. Medtronic is a buy up to $67 per share.

That’s all for now. Next week will be about earnings. We’re also going to get important reports on retail sales and industrial production. You can see an earnings calendar for our Buy List stocks. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

CWS Market Review – September 26, 2014

Eddy Elfenbein, September 26th, 2014 at 7:05 am“The stock market is designed to transfer money from the active to the patient.”

– Warren BuffettThis market continues to be dominated by the strong U.S. dollar. This is a very important point that all investors need to understand. There’s barely a sector of the market that’s not being impacted by the rallying greenback. The difference is that lately, the market’s no longer going higher.

On Thursday, the stock market had its second-biggest drop in the last 24 weeks. The S&P 500 lost 1.62% to close at 1,965.99. That’s a five-week low. The Dow slipped below 17,000, and the Nasdaq Composite was especially hard hit. That index closed below 4,500 for the first time since mid-August.

It was only one week ago that the market reached its “Alibaba Peak.” Last Friday morning, the S&P 500 touched its all-time intra-day high of 2,019.26, and 122 minutes later, Alibaba made its market debut. That may not be a coincidence.

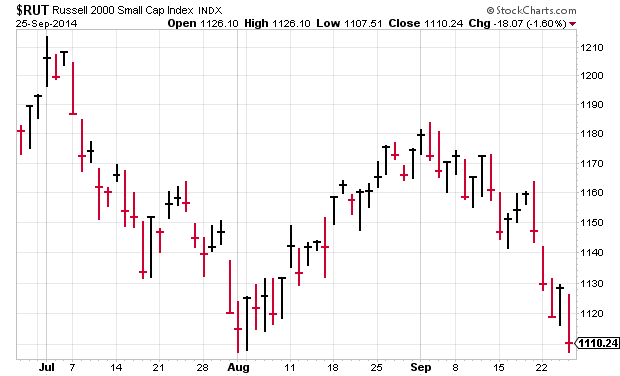

On Thursday, the dollar index broke out to a four-year high, and you can see the evidence everywhere. The yield spread between U.S. and German bonds reached a 15-year high. Gold dropped below $1,210 per ounce for the first time this year, and the small-cap Russell 2000 Index is now down 8.1% since July 3.

In this week’s CWS Market Review, I want to take a closer look at an important issue that has been driving the stock market: share buybacks. For years, Corporate America has been buying back its own shares at an impressive pace. Now, however, the buyback party looks to be coming to an end—and that might be good news. I’ll explain why in a bit.

Later on, we’ll take a look at the solid earnings report from Bed Bath & Beyond. The home-furnishings stores leaped more than 7% on Wednesday after they reported strong quarterly earnings. Speaking of buybacks, a few weeks ago, BBBY went to the bond market to borrow money so they could buy back gobs of their shares, and that’s what helped drive their earnings success. Or I should say their earnings-per-share success. We’ll also take a look at Medtronic’s tax inversion and the dividend increase from McDonald’s (their 38th in a row). But first, let’s look at what’s driving all these buybacks.

Why Share Buybacks Are Beginning to Fade

Anyone else remember when companies used to have lots of shares outstanding? Every quarter, the number of shares has slowly been getting smaller. More and more companies have been using their cash hordes to repurchase their own shares. The benefit for shareholders comes down to simple math. Having fewer shares helps your earnings-per-share, and investors like that. Howard Silverblatt, the main stat guy at S&P, notes that 295 companies in the S&P 500 reduced their share count last quarter.

On one hand, fewer shares is a good thing for investors, as it makes their holdings more valuable. But my take is that I’d prefer to see companies use their cash to expand their operations. That’s the best way to reinvest shareholder money: grow the business. But I can’t fault companies for buying back so much stock. What’s the point of keeping your cash in the bank, where you’d get 0.01%? After all, stocks are cheap and buyback announcements make for great PR.

I have two major complaints with share buybacks. One is that companies shouldn’t be in the stock market game. It’s a great idea to buy back a stock that’s cheap, assuming it rallies later on. But a lot of companies have tossed enormous sums of money at very expensive stocks, only to watch those assets fall. Cisco Systems is a perfect example. Remember a bank called Lehman Brothers? They used to be in the news a lot a few years ago. Anyway, Lehman spent $1 billion buying its own stock during the six months leading up to May 2008. I wince whenever I think about that. The Economist notes, “In all, America’s financial sector repurchased $207 billion of shares between 2006 and 2008. By 2009 taxpayers had had to inject $250 billion into the banks to save them.”

I’m also leery of companies sitting on too much cash. Peter Lynch has referred to this as the “Bladder Theory of Corporate Finance.” Even Apple got complaints from investors like Carl Icahn and David Einhorn for the size of its cash position, and it´s promised to return more money to shareholders. I also don’t like how many companies issue huge amounts of stock options for executive compensation, but they use share buybacks to mask how much they’re diluting their share base. There are exceptions like DirecTV which actually reduce their share count.

But we need to consider the fact that buybacks are popular with investors. Merrill Lynch found that companies with the largest buybacks crushed the market last year. But this year, the biggest repurchasers are performing nearly the same as the rest of the market. Actually, slightly worse. Perhaps, buybacks have lost their cool.

That could be the case. There are early indications that the buyback fever is fading. In Q2, companies in the S&P 500 bought back $116.2 billion worth of stock. That’s a decrease of 1.6% over last year, and a drop of 27.1% from Q1. Of course, stock prices are higher as well.

But that’s not all. Ironically, this could be an optimistic sign, because it means that companies are spending more money on growing their operations. Or, as crazy as this may sound, actually giving raises to their employees! When the financial crisis hit, buybacks were a no-brainer. Also, companies tend to be conservative with their dividend increases because it looks especially bad if you have to cut them later on. It’s generally assumed that a company will maintain its current dividend indefinitely.

There´s basic economics at work here. The U.S. economy has added close to nine million jobs in the last five years (we’ll get another jobs report next week). Those new jobs are an investment in a company’s future, and it’s encouraging to see firms take a more optimistic view of their future. A few days ago, Tesla said it’s building a new battery factory in Nevada. In response, the stock soared. In retrospect, the buyback craze was a result of low prices, low interest rates and a dragging economy. That’s coming to an end, and so, too, is the buyback frenzy. Now let’s take a look at a slumbering Buy List stock that’s taken full advantage of share buybacks.

Bed Buyback & Beyond

After the closing bell on Tuesday, Bed Bath & Beyond ($BBBY) reported earnings for its fiscal second quarter. Earnings announcements have been rather nerve-wracking for the home-furnishings chain; the stock has plunged after the last three earnings reports.

I’m pleased to say that that streak has come to an end. Shares of BBBY jumped more than 7.4% on Wednesday after Bed Bath & Beyond reported quarterly earnings of $1.17 per share. The company had previously said that earnings would range between $1.08 and $1.16 per share. Last week, I said that I expected earnings in the top end of that range, so the results were even better than I was expecting.

What’s interesting about BBBY’s earnings is the impact of buybacks. The company has been gobbling up its own shares at a furious pace. Net earnings fell 10.2% from the same quarter one year ago; however, there were 10.7% fewer shares. Presto! Earnings-per-share rose.

Bed Bath & Beyond recently floated a $1.5 billion bond offering to fund its share buybacks. Last quarter, BBBY spent $1 billion to buy back 16.9 million shares. Working out the math, that means they paid less than $60 per share on average, so they’re already in the money. Once again, it’s basic economics. The bond deal cost BBBY 4.38%, so it’s not exactly a back breaker. In fact, Standard & Poor raised their rating on Bed Bath & Beyond to AAA- from BBB+.

I’ve often said that I’m not a big fan of share buybacks, but I’ll give credit to BBBY for being another firm that´s actually reducing its share count. The company isn’t finished with buybacks either. There’s still another $1.8 billion remaining in the current buyback program. BBBY projects its share count will fall by another 13 million by the end of the fiscal year.

Bed Bath & Beyond gave us guidance for Q3 and Q4. For the third quarter, which ends in November, Bed Bath sees earnings ranging between $1.17 and $1.21 per share. For Q4, which is the all-important holiday season, they see earnings ranging between $1.78 and $1.83 per share. For the entire year, their earnings forecast is $5.00 to $5.08. BBBY sees comparable-store sales rising by 2% to 3% in Q3 and 4% to 5% in Q4.

The full-year forecast is the first time they’ve given us a specific EPS range, but it exactly comports with the “mid-single-digits” language they’ve used for several months. Not once have they budged from that forecast. Since the company made $4.79 per share last year, the current EPS guidance translates to annualized growth of 4.4% to 6.1%.

Adding up the two quarterly guidance ranges gives us a full-year range of $5.04 to $5.13. I’m probably reading too much into that, but it’s something to note. Overall, this was a solid quarter for BBBY. The stock remains a good buy up to $70 per share.

Medtronic Down on Tax-Inversion Rules

This week, Medtronic ($MDT) learned an important lesson that many of us have known for a long time—you simply can’t become Irish because you feel it. Shares of MDT dropped close to 3% on Tuesday, and still more on Wednesday and Thursday, after the government announced new rules for “tax inversions.” That’s what Medtronic is trying to do as it buys Ireland’s Covidien ($COV) and moves its HQ to the Emerald Isle. The move would cut their tax bill by a good amount.

I’ll be honest with you—I don’t know what impact the new rules will have on the MDT/COV deal, and it sounds like no one else knows at this point either. The lawyers are still looking it over. The key issue is a company’s holding of cash outside the United States. In Medtronic’s case, they hold close to $14 billion outside the country. Medtronic wants to loan some of that to their new parent, but the new rules might stop that.

Bloomberg reported that Medtronic released a statement saying, “We are studying the Treasury’s actions. We will release our perspective on any potential impact on our pending acquisition of Covidien following our complete review.” Don’t let the recent sell-off rattle you. Medtronic remains a buy up to $67 per share.

McDonald’s Raises Its Dividend for the 38th Year in a Row

I wanted to say a quick word about McDonald’s ($MCD), which has been a problem child this year. The company has been trying to right itself after several missteps. The results don’t yet reflect this, and the last sales report was truly terrible.

In the CWS Market Review from three weeks ago, I said I was concerned that Mickey D’s wouldn’t raise their dividend this year. I’m pleased to say that that wasn’t the case. Last week, McDonald’s announced that they’re raising their quarterly dividend from 81 to 85 cents per share. The burger giant aims to return $18 billion to $20 billion to shareholders from 2014 through 2016. The new dividend is payable on December 15 to shareholders of record as of December 1. Going by the new dividend and Thursday’s closing price, McDonald’s now yields 3.61%. McDonald’s remains a conservative buy up to $101 per share.

Two more things to mention. DirecTV ($DTV) shareholders approved the AT&T merger with 99% of the vote. Also, Cognizant Technology Solutions ($CTSH) is very cheap at the moment. The shares are at a seven-week low. If you can pick up CTSH below $45, that’s a very good purchase.

That’s all for now. The third quarter comes to a close next Tuesday. After that, we’ll get the important turn-of-the-month economic reports. The September ISM report comes out on Wednesday. There’s a chance it could hit a 10-year high. Also on Wednesday, we’ll get the ADP jobs report. Then on Friday will be the official jobs report from the government. The last report was on the weak side. I doubt that’s the start of a trend. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

CWS Market Review – August 22, 2014

Eddy Elfenbein, August 22nd, 2014 at 7:12 am“There is a danger of expecting the results of the future

to be predicted from the past.” – John Maynard KeynesLadies and gentlemen, I have a very important announcement to make: the Summer Swoon is officially over!

Yep, it’s true. From July 24 to August 7, the S&P 500 shed 3.94%. The market’s low came right as the Dow barely touched its 200-day moving average. But since then, the market has rallied impressively. In two weeks, U.S. equities have gained more than $900 billion in value. The S&P 500 has closed higher in eight of the last ten sessions. On Thursday, the index closed at 1,992.37, which is its highest all-time close. Believe it or not, we’re now within striking distance of 2,000.

Think about this: The stock market has nearly tripled in less than five and a half years. That’s simply amazing. As long-time followers know, our Buy List has done even better.

We’ve had more good news for our Buy List this week. Ross Stores, the deep discounter, just did our favorite two-step—the beat-and-raise polka. Medtronic, the large-cap medical devices company, beat earnings as well. Finally, on Thursday, eBay broke out with a 5% gain on news that it might spin off its PayPal unit. I’ll have full details later on.

We’ve also had some more promising general economic news. The Commerce Department said that housing starts were up sharply last month, and last week’s report on Industrial Production was also quite good. Some folks at the Fed are even talking about raising rates sooner than expected (I doubt it will happen). I want to be careful to put this in proper perspective, though. There are signs that the economy is improving, but we’re still far from healthy. I’ll run down the economic outlook in just a bit, and I’ll highlight what Buy List stocks look especially good right now. But first, let’s look at two big shifts that have been quietly underway on Wall Street.

The Shift Toward Large-Caps and Growth

The Summer Swoon caught a lot of folks off guard. Investors need to understand that summertime investing can be weirdly interesting because a lot of Wall Street bigwigs head off to the Hamptons or Martha’s Vineyard. As a result, trading volume drops off, and smaller events can have an outsized impact.

To boil it down, the market was tripped up by “headline risk,” which refers to political events not related to the market. Every night we’ve seen troubling stories about conflicts in places like Ukraine, Syria and Gaza. Naturally, this has scared investors, especially since volatility had been so low during the spring. I’ve mentioned this statistic before, but it bears repeating: The S&P 500 went 62 days in a row without a single close greater or less than 1%. The market hadn’t had a streak that long in nearly 20 years.

But what’s caught my eye now is that this rally has been a party for the big boys. Large-cap stocks are outperforming, and the smaller guys are lagging behind. While the large-cap S&P 500 finally topped its high from July 3, the small-cap Russell 2000 is still lagging at 4% below its July high. In fact, the Russell 2000 reached its all-time high close on March 4. On July 3, the Russell ran up to its previous high, falling short by just 0.5 points. Technical analysts are always on the lookout for “failures” like this, as they may portend more bad news. Since March 4, the S&P 500 is up more than 6%, while the Russell is down 4%. That’s a surprisingly wide gap between the two indexes.

Large-caps aren’t the only favored sector. Growth stocks are also doing well. This is a big change from the spring. In March and early April, the stock market turned sharply against Growth stocks in favor of Value. But since April 11, the Vanguard Growth ETF ($VUG) is up by 12.5%, and the relative performance of Growth has gotten even stronger lately.

What do these two market shifts, large-cap and growth, mean for the market? It’s hard to say exactly, but I think they reflect greater confidence in the economy. When people get scared, they turn to Value, so the newfound love for Growth probably reflects investor optimism. The last GDP report was certainly encouraging, and it bolsters the view that the economy is improving. Another bit of evidence was last Friday’s Industrial Production report. In July, Industrial Production rose by 4%. That’s twice the rate that economists were expecting. Industrial Production is up 5% in the last year.

The turn to large-caps is a bit more complicated. The big difference between large- and small-cap indexes is that large-cap stocks tend to get more of their revenue from overseas. The smaller stocks are skewed towards domestic manufactures. As a result, the large-cap surge could reflect more optimism about Europe and other foreign markets. For example, Ford Motor ($F) recently turned a profit from their European operations, which was earlier than expected.

The U.S. dollar is also improving against many currencies (bond yields in Europe are crazy low). A stronger dollar is typically correlated with large-caps outperforming small-caps. This makes sense since a stronger currency has a tendency to impede smaller domestic manufacturers.

The positive economic news is clearly influencing the Federal Reserve. On Wednesday, the Fed released the minutes from their July meeting. The minutes suggested that some Fed members are beginning to think that interest rates may have to go up sooner than expected. I’m skeptical. Of course, looking at the minutes from any Fed meeting is an extended exercise in indefinite adjectives; “some” members say this, while “many” members say that. We never know exactly how many members feel a certain way on a given issue.

I suspect the majority on the FOMC is in favor of letting short-term rates ride for several more months. Earlier this week, we learned that inflation continues to be very subdued. The CPI rose by just 0.1% in July. That’s the lowest rate in five months. There are few things that scare central bankers more than inflation, so this news gives the Fed a little more breathing room to keep rates low. For its part, the bond market is still holding up. The 10-year yield recently closed at its lowest level in 15 months. Until there’s more evidence of inflation, Janet Yellen and her friends at the Fed are quite content to keep rates near the floor. This is good for the economy, the stock market and Growth-oriented stocks. Now let’s turn to some of our recent earnings reports.

Medtronic Beats by a Penny

On Tuesday, Medtronic ($MDT) reported fiscal Q1 earnings of 93 cents per share. That was one penny better than expectations. Quarterly revenues rose 4.7% to $4.27 billion, which was $20 million better than expectations. Medtronic had its strongest growth for U.S. medical devices in five years.

I was pleased to hear the company reaffirm its commitment to the Covidien deal. Medtronic also stood by its full-year earnings guidance range of $4.00 to $4.15 per share. I like this company a lot, but I’m going to keep our Buy Below at $67 per share, which is fairly tight. At the current price, MDT is going for less than 16 times this year’s estimate. Medtronic is an ideal stock for conservative investors.

Ross Stores Is a Buy up to $77 per Share

After the closing bell on Thursday, Ross Stores ($ROST) reported very good numbers for their fiscal Q2. For May, June and July, the deep discounter earned $1.14 per share. That was six cents better than Wall Street’s consensus. It was also well above Ross’s own guidance of $1.05 to $1.09 per share. I should add that Ross tends to be fairly conservative with its guidance. Quarterly revenue rose by 7%, which was also better than expectations.

The results from Ross tell us that consumers are willing to spend money if they see good deals. I was very pleased to see the company’s operating margins rise to a company record. In the earnings report, Ross gave us earnings guidance for Q3 and Q4. For the current quarter, they see earnings ranging between 83 and 87 cents per share. The Street was at 86 cents. For Q4, they project earnings between $1.05 and $1.09 per share. Wall Street was at $1.12 per share. Bear in mind that Q4 is a biggie for a retailer like Ross.

Ross’s CEO said, “Our second-quarter sales performed at the high end of our expectations as today’s value-focused consumers continued to respond to our wide assortment of competitive name-brand bargains. Merchandise gross margin was above plan, which, coupled with strong expense controls, enabled us to deliver quarterly earnings per share that were above the high end of our guidance.”

Ross raised guidance for the entire year. Previously, they said they expected earnings to range between $4.09 and $4.21 per share. Now they see earnings coming in between $4.18 and $4.26 per share. Last week, I said that I wanted to see better guidance from Ross before I would touch the Buy Below price. Well, we got our evidence and business is going well. I’m raising our Buy Below on Ross Stores to $77 per share.

Will eBay Ditch PayPal?

Shares of eBay ($EBAY) spiked upward on Thursday on rumors that the company is considering spinning off its PayPal subsidiary. If you recall, Carl Icahn had been pressuring eBay earlier to make such a move. The company repeatedly shot down the idea, but PayPal makes a lot of money, and it could be very lucrative for eBay to let them go.

On Thursday, the online magazine “The Information” said that eBay has been telling prospective candidates for PayPal’s new CEO that a spinoff could be in the works. Honestly, that doesn’t strike me as that big of a deal. It seems quite natural that the spinoff topic would be addressed in a job interview. That doesn’t mean it will happen. Publicly, I expect eBay will still speak out against any spin-off.

What’s more interesting to me is how strongly the market reacted to the idea. The market clearly wants PayPal spun off, and that will cause shareholders to pressure the board to make a deal happen. I’ve been following stocks long enough to know that if a board of directors thought wearing clown shoes would help their stock, they’d do it before sunrise. Look for a deal to happen at some point, but it may take time. In the meantime, I’m raising our Buy Below on eBay to $58 per share.

Before I go, let me highlight a few Buy List stocks that look especially good right now. I really like Ford Motor ($F). I think the automaker will make another run at $18 very soon. Cognizant Technology Solutions ($CTSH) is also a very good buy if you’re able to get it below $47 per share. Shares of Qualcomm ($QCOM) pulled back sharply after the last earnings report. It’s coming back quickly, and I think that trend will continue. My Buy Below for QCOM is $79, but if you can pick up shares below $77, then you got a good deal.

That’s all for now. Next week is the final trading week for August. The year is nearly two-thirds over. The next big econ report will come on Thursday when the government revises the Q2 GDP report. The initial report came in at 4%, which surprised a lot of people. Not many folks had been expecting such a strong number. Now we have some more trade data, so the updated figure could be different. On Friday, we’ll get the report for Personal Income. This is usually a reliable metric for how well the overall economy us doing. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

CWS Market Review – June 20, 2014

Eddy Elfenbein, June 20th, 2014 at 7:06 am“In this game, the market has to keep pitching, but you don’t have to swing. You can stand there with the bat on your shoulder for six months until you get a fat pitch.” – Warren Buffett

The news got a lot more interesting this week. First, Medtronic ($MDT) announced a mega-merger deal with Ireland’s Covidien. The shares celebrated by jumping to an all-time high. MDT is a 13% winner on the year for us.

Also this week, the Federal Reserve decided on another taper, their fifth in a row. Investors liked what they saw, and the S&P 500 has now rallied for five days in a row. That’s our longest winning streak since April. The index just notched its 21st record high this year. The Nasdaq touched a 14-year high (see below), and the Volatility Index plunged to an 88-month low.

In this issue of CWS Market Review, I’ll walk you through the Medtronic-Covidien deal. Frankly, it’s not ideal, but I recognize that Medtronic had to make a move, and it’s probably the best deal they could get. I’ll also take a look at the recent earnings report from Oracle, and we’ll preview next week’s earnings report from Bed Bath & Beyond. BBBY has gotten beaten down this year, and I think it’s going for a very good price here. I’ll also discuss the Fed’s latest taper move and why the economy is finally looking better (no, really). But first, let’s take a closer look at the $42.9-billion deal Medtronic did with Covidien.

Medtronic Buys Covidien for $42.9 Billion

Two weeks ago, I told you that Medtronic ($MDT) was seriously considering a merger with Smith & Nephew ($SNN). This past weekend, however, the company announced that it’s buying Ireland’s Covidien ($COV) for $42.9 billion. In 2007, Covidien was spun off from Tyco International ($TYC).

What makes this deal interesting is that it’s an “inversion,” which means that Medtronic’s HQ will move from Minneapolis to Ireland, where corporate taxes are much lower. Americans are often surprised to learn that our corporate tax rate is higher than many European countries’ rates. The main corporate rate in Ireland is 12.5%, compared with 35% in the U.S. I think we can expect to see more of these inversion deals in the future. In Medtronic’s case, the tax savings won’t be that dramatic since they already have a modest tax bill thanks to R&D tax breaks.

The deal calls for Medtronic to pay $93.22 per share for Covidien ($35.19 in cash and 0.956 shares of MDT). That was a 29% premium to Covidien’s share price. As an interesting footnote, to qualify as an inversion, the deal has to be at least 20% in stock. With acquisitions, the rule of thumb is that the acquirer’s stock falls. Not this time. Shares of Medtronic initially stumbled, but then a rash of upgrades caused traders to push MDT as high as $65.50 per share on Thursday. That’s an all-time high.

Is this a good deal for Medtronic? It’s complicated. I’m not a fan of mega-mergers. Small rollups are fine, but trying to merge two large enterprises is often more difficult than the planners realize. Having said that, I realize that Medtronic had to make a move. All medical device companies need to. After all, their customers (hospitals and physician groups) have been merging for the last few years, and the device makers are facing those same economic pressures. You can be sure that many of these upcoming deals will be inversions, so expect to hear more talk about Stryker ($SYK) and Britain’s Smith & Nephew.

Ironically, by setting up in Ireland, Medtronic will be able to free up more cash, which they can reinvest in the United States. Medtronic said they plan to invest $10 billion in the U.S. over the next ten years. A lot of these inversions will be between companies that make strange bedfellows, but Medtronic and Covidien are a natural fit. For all the options Medtronic faced, this was the best deal for them to make, so I cautiously support this deal.

As if there’s not enough Medtronic news this week, the company also announced an 8.9% increase to its dividend. I love me a good dividend increase. The quarterly dividend will rise from 28 cents per share to 30.5 cents per share. For the year, that’s $1.22 per share. This is the 37th year in a row that Medtronic has increased its dividend. Going by Thursday’s close, Medtronic yields 1.9%. This week, I’m raising my Buy Below on Medtronic to $67 per share.

The Fed Tapers Again

The Federal Reserve held a two-day meeting this week, and as everyone expected, the central bank tapered its bond purchases again. Starting in July, the Fed will purchase $20 billion in Treasuries each month, plus $15 billion per month in mortgage-backed securities. This is the fifth-straight meeting in which the Fed has tapered.

Tapering by $10 billion at each meeting ($5 billion in Treasuries and $5 billion in MBS) has been the Fed’s game plan all year, and they’ve stuck to it, even when the economy got polar-vortexed earlier this year. In their post-meeting statement, the Fed said that the economy is slowly improving, although housing remains weak.

The Fed has four more meetings left this year. So if we assume they stay on course, they’ll be done with Quantitative Easing (QE) by the end of the year. (I’m assuming the final $5 billion in Treasuries will be tapered in December, but there could be a clear-the-decks move in October.) Janet Yellen has said to expect a rate increase about six months after the end of QE.

As part of this Fed meeting, they also updated their economic projections. You can see them here. Let me caution you that the Fed isn’t exactly known for its accuracy, but it’s interesting to see what its assumptions are. Here’s where it gets interesting. Check out Figure 2 on the PDF. The broad consensus is that the first rate hike will come next year. Twelve of the 16 members agree on that, and I think they’re right. But the consensus falls apart for year-end 2015. There’s a small clustering around 1% to 1.25%, which means that real rates are projected to be negative for at least another 18 months. As long as the lid stays on inflation, that’s very good for the stock market and our Buy List. One of the basic rules about finance is that the stock market loves cheap money.

This week’s inflation report shows that inflation continues to trend upward. Of course, we’re still far from it being a problem, but the rate of inflation is no longer falling. That’s key. The Bureau of Labor Statistics reported on Tuesday that core inflation rose at its fastest rate since October 2009, which is still quite modest. Only now is inflation finally moving into the Fed’s target area.

The Fed’s consensus for year-end 2016 is even more scattered. Their range for short-term interest rates goes from 0.5% to 4.25%, and there are never more than two members that agree on any one rate. I don’t expect a consensus, but I’m shocked to see so little agreement on where the economy will be in 30 months. In short, they see rates going up, but there’s no agreement on how high.

I should point out that two Fed regional surveys this week were quite optimistic. The Philly Fed Manufacturing Survey noticed a big increase in activity this month. Also, the Empire State survey showed that activity in New York is quite good. On Monday, the Fed reported that Industrial Production rose a healthy 0.6% last month. For the first time in a long time, we can say that things are looking up for the economy. Expect to see the economy average over 3% annualized growth for the next few quarters. After five years, the recovery is beginning to be felt on Main Street.

Oracle Misses Earnings by Three Cents per Share

After the closing bell on Thursday, Oracle ($ORCL) reported fiscal Q4 earnings of 92 cents per share. Frankly, that’s disappointing; it’s three cents below Wall Street’s consensus. Oracle said they lost two cents per share due to the currency loss in Venezuela. Shares of ORCL, which had rallied to a 14-year high during the day on Thursday, got smacked around for a 6% loss in the after-hours market.

Three months ago, Oracle said to expect Q4 earnings to range between 92 and 99 cents per share. As it turns out, they hit the low end of their guidance, and business was pretty sluggish in Q4. Quarterly revenue rose 3.4% to $11.32 billion, which was $160 million below expectations.

One of the keys for Oracle‘s business is sales of new software licenses. For Q4, that came in at $3.77 billion, which is flat. Their hardware revenue, now finally growing, rose only 2% to $1.5 billion. One bright spot is that Oracle’s cloud revenue jumped 23% to $327 million. There have also been rumors that Oracle is considering buying Micros Systems ($MCRS) for $5 billion, which would be their largest deal since they bought Sun Microsystems four years ago. Micros makes software for hotels, restaurants and retailers.

Now for guidance. On the earnings call, Oracle said they see Q1 earnings ranging between 62 and 66 cents per share. That’s not so bad. Wall Street had been expecting 64 cents per share. Oracle sees quarterly revenue growth between 4% and 6%. Breaking that down, they expect new software-license revenue to be up by 6% to 8%. Hardware will be between -1% and 3%, but cloud revenue is expected to be up by 25% to 35%. If this guidance is accurate, that tells us that last quarter’s weakness won’t last. Oracle remains a good buy up to $44 per share.

Stay Tuned for Bed Bath & Beyond’s Earnings Report

Our biggest dud this year, by far, has been Bed Bath & Beyond ($BBBY). The stock is off more than 24% YTD. Last week, the shares traded below $60 for the first time in 15 months.

I apologize for the rough ride with this one, but make no mistake, I haven’t given up on BBBY. In the CWS Market Review from May 9, I announced that I was ready to pound the tables for BBBY. This coming Wednesday, June 25, is our first big test. That’s when BBBY will report their fiscal Q1 earnings.

Let’s review where we stand. Three months ago, Bed Bath & Beyond reported terrible results for Q4 (December, January, February). The home-furnishings store earned $1.60 per share. That was eight cents lower than the year before. That was quite a shock, because BBBY delivered earnings increases like clockwork. They estimated that poor weather knocked six to seven cents off their bottom line.

For their Q1 outlook, BBBY had more bad news. They said to expect earnings to range between 92 and 97 cents per share. The consensus on Wall Street had been for $1.03 per share. They made $4.79 all of last year, and for this fiscal year, they expect earnings to rise by “mid-single digits.” If we take that to mean 4% to 6%, their guidance works out to a range of $4.98 to $5.08 per share. Wall Street had been expecting $5.27 per share.

Now let’s look at the items in BBBY’s favor. First is the low share price. The stock is going for about 12 times forward earnings. If we look at one of my favorite valuation metrics, Enterprise Value/EBITDA, BBBY’s is down to 6.15, which is quite low. The company also has a very clean balance sheet: no debt and lots of cash. Let’s remember that the store is well managed, and they’ve ridden through storms such as this before. As the Fed indicated this week, the housing market is still weak, but that won’t last, and stronger housing helps BBBY. You need to be patient with this one, but Bed Bath & Beyond remains a very good buy up to $66 per share.

That’s all for now. Next week is the last full week of Q2. On Wednesday, the government will revise its Q1 report for the second time. The initial report showed growth of 0.1%, but last month it was revised down to -1%. I’m curious to see what happens this time. Also on Wednesday, we’ll get a key report on orders for durable goods. On Thursday, we’ll get the report on personal income. Also on Wednesday, we’ll get the earnings report from Bed Bath & Beyond. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

CWS Market Review – June 6, 2014

Eddy Elfenbein, June 6th, 2014 at 7:12 am“I don’t expect the consensus to be right. I’m just surprised by how wrong it has been.” – Jim Bianco

This has been a remarkably efficient stock market. I say that because it’s effortlessly made fools of everyone.

Remember all that talk about “a bubble” and that we’re “due for a correction”? Well, apparently Mr. Market wasn’t cc’d on that. On Thursday, the S&P 500 rallied for the 14th time in the last 19 sessions. The index hit yet another all-time high. (I was particularly impressed when it blew past the historically significant 1,929 marker.)

As we look at this rally, we have to keep in mind all the negative news that could have tripped us up—like the lousy Q1 GDP report, or the ongoing tensions in Ukraine. None of that seems to matter. Everyone, it seemed, was expecting a mass rotation out of bonds. Didn’t happen. Instead, bond yields have plummeted this year.

Despite the market’s resiliency, what’s truly been remarkable is how little trading volume there’s been. In less-technical terms, where the heck did everybody go? Trading volume has plunged, and the bull just doesn’t care. In this week’s CWS Market Review, we’ll take a look at what this low-volume, low-volatility rally means for us and our Buy List.

I’ll also highlight some of the recent economic news. We had some interesting drama on our Buy List recently. Shares of Stryker spiked after the company denied a report that they were looking to buy Smith & Nephew. Then another one of our Buy List stocks, Medtronic, had the same rumor hit them! What’s going on? I’ll untangle it all in a bit. But first, let’s look at where the economy stands.

Finally, an All-Time High for Jobs

On the first business day of each month, the Institute for Supply Management releases its Manufacturing Index. I like to keep a close eye on the ISM report for a few reasons. One is that it comes out so quickly. A lot of economic reports come weeks after the fact. It’s also one of the econ reports that’s not endlessly revised.

The ISM also has a good track record of lining up with recessions and expansions. Here’s how it works: Any number above 50 means that the manufacturing sector is expanding, while readings below 50 mean it’s contracting. When the index is below 45, it usually corresponds to a recession. The ISM Index has been 49.0 or better for the last 59 months in a row, which lines up exactly with the current expansion.

On Monday, ISM had some problems. They had to revise their May report not once, but twice. It’s embarrassing, but they finally settled on a figure of 55.4, which was only 0.1 below what Wall Street had been expecting. That’s a decent number, and it suggests that the manufacturing sector is still healthy. For now, I don’t believe there’s a risk of an imminent recession.

On Monday, we also learned that construction spending rose by 0.2% in April. Frankly, that was a bit weak. Economists had been expecting an increase of 0.7%. Also on Monday, we learned that housing inventory is up 10.5% from a year ago. This is very important, since there was so much overbuilding during the expansion. All that excess inventory had to be burned off. Inventory is still quite low, and prices have been rising. Housing isn’t the biggest part of the economy, but it’s probably the biggest part in determining the direction of the economy.

Then on Tuesday, carmakers reported good sales for the month of May. Sales for GM rose 13%, and sales for Chrysler rose 17%. Sales at Ford ($F) rose only 3%, but that’s actually a decent performance. Ford’s been cutting back on its incentives in an attempt to manage its inventory. This was the best May for Ford in ten years. On Thursday, shares of Ford got as high as $16.89, which is a six-month high. I like this stock a lot. Ford remains a solid buy up to $18 per share.

Now about the jobs report. As usual, I’m writing this newsletter to you early on Friday morning, and the big jobs report will come out later this morning. In fact, it’s probably out by the time you’re reading this (check the blog for updates). It’s always a hazard guessing how many new jobs were created. The government is very clear that their estimates have a very wide error range (the standard deviation has been 236,000), but that doesn’t stop Wall Street from playing the guessing game. What’s more important to me, however, is the general trend of new jobs. Fortunately, that’s been rather good lately. Of course, there are still lots of unemployed folks out there, especially long-term unemployed.

On Wednesday, ADP, the private-payroll folks, said that 179,000 private-sector jobs were created last month. That was below expectations, but I should caution you that ADP doesn’t have a great track record as a bellwether for the government’s report. On Thursday, the Labor Department said that unemployment claims rose to 312,000 last week. That’s a good number. Since this number bounces around a lot, economists like to focus on the four-week moving average, which is now at a seven-year low.

It’s very likely that Friday’s jobs report will show that we finally surpassed the peak employment set in January 2008. In other words, it’s taken us six and a half years to create a few thousand jobs. As rough as that sounds, the economy lost 8.7 million jobs in 25 months. It then took another 51 months, more than twice as long, to make them all back. Wall Street has high expectations for this report. The current consensus is for 213,000 jobs. The economy added 288,000 jobs in April.

Also on Thursday, the Federal Reserve released the big “Flow of Funds” report. This is always an interesting report to see. According to the Fed, U.S. household net worth rose to $81.8 trillion at the end of Q1. In the last five years, our net wealth has risen by more than $26 trillion.

Overall, the broad economy appears to be doing well. More folks on the Street expect GDP for Q2 to be over 3%. It could be as high as 4%. One of the better economist reports is the Fed’s Beige Book. It’s a bit on the wonky side, but it has some good tidbits. The most recent Beige Book reported growth in all 12 of the Fed’s regions.

Another one of my favorite economic indicators is the yield spread between the two- and ten-year Treasuries. While the 10-year has rallied this year, it still yields 219 basis points more than the two-year. That’s a big gap. Whenever that spread turns negative, you can be sure the economy will soon hit a rough patch. The 2-10 spread has a much better track record than a lot of highly paid folks on Wall Street. The 2-10 has been over 200 basis points every day for nearly a year.

Hey, Where Did Everybody Go?

On Thursday, the S&P 500 closed at 1,940.46, which is another all-time high. But what’s interesting is that the market has rallied on very low volatility and low volume. The trading volume has declined remarkably. On Wednesday, trading in the S&P 500 ETF ($SPY) hit a new low for the year.

Last month, an average of 1.8 billion shares were traded in the S&P 500 companies. That’s the lowest volume in six years. During May, an average of $26 billion was traded each day in S&P 500 companies. That’s down from $32 billion in April.

Also, the market’s breadth continues to narrow. On May 23, the S&P 500 made a new high, but only 24 stocks in the index made a new 52-week high. I’ll warn you that these are traditionally negative signs; the problem is that you never know when the trouble will begin.

Earlier this week, the Volatility Index ($VIX) dropped down to 11.29, which is the lowest level in more than a year. (Warning: math stuff ahead.) If you’ve ever wondered what the VIX is, it’s the market’s estimate of the S&P 500’s standard deviation over the next month. The hitch is that it’s expressed in annualized terms. To turn it into a monthly figure, just divide the VIX by the square root of 12, which is 3.46. So the current VIX of 11.68 means that traders think the S&P 500 will move up or down by 3.37%, or about 65 points, over the coming month.

Only two years ago, the European bond market was ready to sink into the Adriatic. Now bond yields in the Old World are at their lowest point since the Battle of Waterloo. Mario Draghi just dropped the deposit rate from 0% to -0.1%. The European Central Bank is now the first major central bank in the world to go to negative interest rates. So much of the European economy is still in shambles. In 1914, Lord Grey famously said, “the lamps are going out all over Europe.” This time, it’s not a metaphor.

On this side of the pond, the market still seems reasonably priced despite the rally. Analysts on Wall Street currently expect earnings this year for the S&P 500 of $119.82. The estimate for next year is $137.38, but that’s probably too high. As long as yields stay low, the spreads are wide, and the economy is generating more than 150,000 new jobs each month, then the bull case is intact.

As always, investors should focus on high-quality stocks like the ones on our Buy List. As long as they’re below my Buy Below price, I think they’re good buys. Right now, I especially like AFLAC ($AFL), Bed Bath & Beyond ($BBBY), Ford ($F), Oracle ($ORCL) and Wells Fargo ($WFC).

Smith & Nephew & Stryker & Medtronic

Here’s a bit of an odd story. Last week, the Financial Times reported that Stryker ($SYK) was looking to bid on Smith & Nephew ($SNN), a British orthopedics company. But Stryker was all, “um…no, we’re not planning any bid.”

Here it gets a little confusing. Stryker had been interested in SNN, but they were only in the evaluating stage. Now that Stryker has said they’re not going to make a bid, according to British law, they can’t bid for six months. But SNN is allowed to go to them.