-

Humans prefer cockiness to expertise

Posted by Eddy Elfenbein on June 17th, 2009 at 1:48 pmNewScientist reports that Humans prefer cockiness to expertise (if you click through to the article, you won’t be surprised to see whose picture they’ve used):

EVER wondered why the pundits who failed to predict the current economic crisis are still being paid for their opinions? It’s a consequence of the way human psychology works in a free market, according to a study of how people’s self-confidence affects the way others respond to their advice.

The research, by Don Moore of Carnegie Mellon University in Pittsburgh, Pennsylvania, shows that we prefer advice from a confident source, even to the point that we are willing to forgive a poor track record. Moore argues that in competitive situations, this can drive those offering advice to increasingly exaggerate how sure they are. And it spells bad news for scientists who try to be honest about gaps in their knowledge.

In Moore’s experiment, volunteers were given cash for correctly guessing the weight of people from their photographs. In each of the eight rounds of the study, the guessers bought advice from one of four other volunteers. The guessers could see in advance how confident each of these advisers was (see table), but not which weights they had opted for.

From the start, the more confident advisers found more buyers for their advice, and this caused the advisers to give answers that were more and more precise as the game progressed. This escalation in precision disappeared when guessers simply had to choose whether or not to buy the advice of a single adviser. In the later rounds, guessers tended to avoid advisers who had been wrong previously, but this effect was more than outweighed by the bias towards confidence.

The findings add weight to the idea that if offering expert opinion is your stock-in-trade, it pays to appear confident. Describing his work at an Association for Psychological Science meeting in San Francisco last month, Moore said that following the advice of the most confident person often makes sense, as there is evidence that precision and expertise do tend to go hand in hand. For example, people give a narrower range of answers when asked about subjects with which they are more familiar (Organizational Behavior and Human Decision Processes, vol 107, p 179).

There are times, however, when this link breaks down. With complex but politicised subjects such as global warming, for example, scientific experts who stress uncertainties lose out to activists or lobbyists with a more emphatic message.

So if honest advice risks being ignored, what is a responsible scientific adviser to do? “It’s an excellent question, and I’m not sure that I have a great answer,” says Moore.(HT: TAR).

-

Obama’s Plan For Financial Regulation

Posted by Eddy Elfenbein on June 17th, 2009 at 1:27 pm -

Market Reaction to Unexpected Monetary Policy Announcement

Posted by Eddy Elfenbein on June 17th, 2009 at 1:23 pmA bit wonky but interesting:

This paper examines the daily response of euro area stock markets to unexpected ECB monetary policy announcements. We define ECB’s unexpected decisions in analyzing the consensus in the specialized press the days before the announcement. Our preliminary results show that very few ECB’s announcement’s are unexpected by ECB watchers, this is a sign that the ECB’s monetary policy is very predictable. We also find little responses of stock markets to unexpected monetary policy decisions. If Eurozone equity markets react homogeneously to unexpected monetary policy decisions, we can see that reactions are higher in France than in Germany. We find significant and heterogeneous responses from sectorial indexes which indicate that the financial channel of monetary policy is different following the sector. Finally, we find that markets are more sensitive to good news in bad times, but there is no evidence of the opposite.

-

AFL Under $30

Posted by Eddy Elfenbein on June 17th, 2009 at 1:02 pmIf you’re looking to put free cash to use, Aflac (AFL) is a good buy under $30. That’s about six times the guidance they’ve given (and reaffirmed) for this year.

-

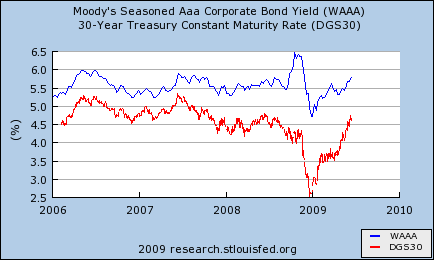

What’s Behind Soaring T-Bond Yields

Posted by Eddy Elfenbein on June 17th, 2009 at 10:48 amMany market observers have been alarmed by the surge in long-term bond yields. This has also sparked a debate on Wall Street: Are the higher yields due to an emergent recovery or fears of higher inflation?

For now, I don’t think it’s either. More than higher bond yields, we’re really seeing a closing of the gap between Treasury yields and corporate yields. In other word, investors are more willing to take on risk. To be even more precise, the level of risk-taking is backing off from its extremely scared level of about six months ago.

This chart shows the yield of the 30-year Treasury (red) along with an index of AAA bonds (blue).

Notice the closing of the gap between the two. Corporate yields are higher but the major change has come from Treasuries. This means that the price of risk is finally returning to normal. -

Ex-con tried to get $15 trillion tax return

Posted by Eddy Elfenbein on June 17th, 2009 at 9:35 amYou might as well go all the way:

Fresh out of prison on a money-laundering conviction, Marlon T. Moore tried to make a big score, federal prosecutors say.

The Miami man — aka ”X-Large Moore” — filed an income tax return seeking a refund of almost $15 trillion.

No joke. Now Moore is charged with filing false claims with the IRS and obstructing the agency’s laws.

After his release from a Florida prison in late 2007, Moore allegedly prepared bogus documents claiming that the feds owed him various amounts, including $5,950,000,000,000, $2,975,000,000,000 and $6,000,000,000,000.

“In fact, however, defendant Moore knew he was owed no such amounts,” according to a statement by the U.S. Attorney’s Office in Miami.

Moore, 38, has a bond hearing on Thursday. If convicted, he faces up to five years in prison for each false claim and up to three years for impeding IRS laws.This is completely unacceptable. Still, I’d like to see X-Large appointed to the Fed.

-

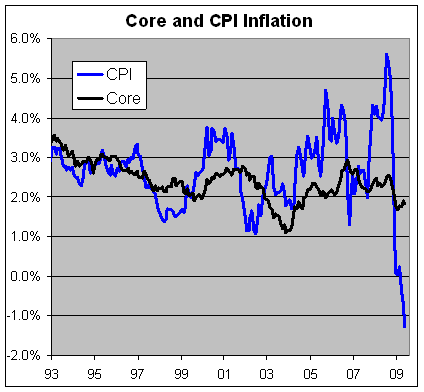

CPI Came in Below Forecast

Posted by Eddy Elfenbein on June 17th, 2009 at 9:19 amBoth headline and core were up 0.1%:

The cost of living in the U.S. rose less than forecast in May, culminating in the biggest 12-month drop in prices in almost 60 years.

The consumer price index increased 0.1 percent after no change a month earlier, the Labor Department said today in Washington. In the 12 months ended in May, costs dropped 1.3 percent, the biggest decline since 1950.

Higher commodity prices, including gasoline, will probably restrain Americans’ discretionary spending at a time when the economy is showing signs of stabilizing. The lack of sustained gains in sales is one reason companies are finding it difficult to pass increasing costs on to customers.

-

People With Way Too Much Time on Their Hands

Posted by Eddy Elfenbein on June 17th, 2009 at 8:55 am -

Swan Song

Posted by Eddy Elfenbein on June 16th, 2009 at 3:17 pmMark Gimein looks at Nassim Taleb:

But the failures of the Niederhoffers and AIGs do not translate to a validation of Taleb-style catastrophism because these two approaches turn out to be linked. They are mirror images. In noncatastrophic times, the Niederhoffers and AIGs make money consistently and quietly and then end up losing it conspicuously and painfully. The Talebs make money rarely, amaze everyone because they do it when everybody else is getting killed—and so make it easy to forget about years of steady losses. Over the long run, the anti-catastrophists often do fairly well (if they don’t get too greedy and make bets that cost them all their money in even a small market drop). But it is the catastrophists, a la Taleb, who look smarter. If you’re always planning for crisis, you look like a genius when it does come.

Arguing against Taleb is a little embarrassing; who among us wants to side with the plodders when for the price of a paperback you can join the elect? But the experience of the markets here is important because it shows that neither consistently discounting the chance of unforeseen risks, as AIG did with such gusto, nor betting day after day on unforeseen catastrophes is a reliable way to make money.

In his books Taleb presents a wealth of examples of how prone we are to discount the unexpected and unlikely, but what is notably missing from The Black Swan are examples of just how likely we are to overestimate the chances of unlikely events when they are presented to us under a spotlight. Taleb is, of course, right that we fail to anticipate what we are not looking for. But we also overanticipate when we are looking too hard for the outliers. Lottery players overvalue their chances of winning $10 million, and horse bettors put too much money on 100-1 long shots. People who watch the local news too avidly believe there is a child kidnapper around every corner, and followers of Taleb assume that every time they pass a dark alley, catastrophe is about to pop out with a bloody knife. -

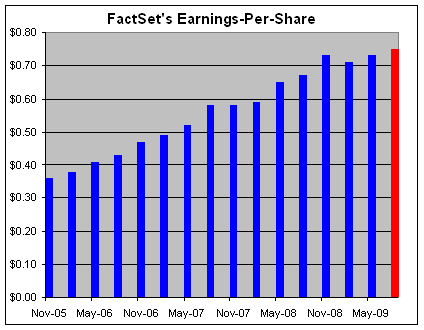

FactSet Beats the Street

Posted by Eddy Elfenbein on June 16th, 2009 at 12:01 pmOne of my Buy List stocks, FactSet Research Systems (FDS), just reported another strong quarter. For the May quarter, which is their fiscal third quarter, FactSet earned 73 cents a share which was a penny better than estimates. Revenues rose 4.7% to $154.4 million which was slightly below the Street’s consensus.

For Q4, FDS sees earnings coming in between 73 cents and 75 cents a share, and revenues between $152 and 157 million. The Street was expecting 72 cents on $155.45 million.

FactSet said its operating margins and free cash flow rose even though they lost 34 clients last quarter. Client count is now at 2,033. The company also recently raised its quarterly dividend to 20 cents a share from 18 cents. This is an excellent stock to own.

Here’s a look at FDS’ recent quarterly results with the red bar being my forecast for this quarter.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His