-

Gold Revisited

Posted by Eddy Elfenbein on April 8th, 2009 at 11:21 amThe other day, I asked how should one value gold. Specifically, what metrics should you follow to see if gold is overpriced or underpriced? My post was reposted at Seeking Alpha. As I expected, nearly all the comments were completely useless rants from gold bugs. Yes, I know why gold is used, but that doesn’t tell me anything about the current price.

One comment, however, stood out and I felt I should acknowledge this from silveraxis who blogs here.The proper way to value gold is based on its monetary qualities, or in other words what it could purchase. Many people use inflation rates such as CPI as a proxy for fair value of gold but this is not very sophisticated for several reasons, the most significant of which include accuracy issues as well as the fact that the aboveground stockpile of gold grows every year. I prefer to use a ratio of gold to the global economy, stock markets, U.S. Treasury debt and/or global asset base.

Global economy is reasonably estimated using global nominal GDP (currently around $55 trillion). There are also available figures for Treasuries and stock markets (an effective if rudimentary approach is simply to use the S&P 500 as it is already market cap weighted).

Global assets are much harder to estimate but this is probably the most relevant ratio because it reflects gold’s relative purchasing power. Clearly it wouldn’t make sense for all of the world’s gold to be worth more than every asset that could be purchased! Indeed, gold could only be realistically worth some fraction of total assets which throws some of the wilder (Jason Hommel, Ted Butler, etc.) gold price predictions right out the window. In any case, you basically add global stock market capitalization, real estate, private equity, debt collateral, fiat money in circulation, etc. but exclude all credit-based money, derivatives and other financial products that are zero sum (offsetting asset and liability). Let’s say the current number for the global asset base is $150 trillion (probably a bit high but not that far off).

Now calculate the global market cap of gold: 5 billion ounces times $900 = $4.5 trillion. Thus the gold to global economy ratio is roughly 12 ($55T/$4.5T) whereas the gold to global asset ratio is currently around 33. Similar ratios can be computed for stock markets and U.S. Treasuries.

To determine if these ratios and thus the gold price is fair, too high or too low, you need to come up with similar ratios for various points in time, such as the 1980 high in gold, the 2001 low, under Bretton Woods (pre-1971), etc. as well as an average over time. If you do the math it basically says that gold is currently comparable to where it stood in the mid-1970’s after the 1974 high and before the 1980 high. At the 1980 peak, the ratios were anywhere from 3 to 7 times lower. That implies if gold were to reach a similar extreme today, it could rise 3-7 times from current levels assuming the denominator (GDP, stocks markets, etc.) stays the same.

Alternatively, the average gold ratios over the past 40 years or so imply that fair value lies in the range between $500 and $1000. If we strip out most of the 1990’s when the novelty of gold mine hedging and central bank leasing were at their peaks, these fair values become $600 to $1200. I believe at least several of the analysts that predict $1200 gold are basing their numbers on a similar model to the one I am describing.

Finally, my own studies indicate that the historical ratio of global asset values to gold may have been approximately 5 under the gold standard. In other words, gold might have typically represented approx. 10-20% of the world’s material wealth in the past. Perhaps this could be viewed as the ultimate fair value of gold. If so, assuming a global asset base of $150 trillion would mean gold has a fair value of $3000 to $6000/oz. ($150T/5/5 billion ounces). Such a price assumes the adoption of a worldwide gold standard and no consequent deflation in asset prices, which may not be realistic. Perhaps $75T might be a better number given the already ongoing global asset meltdown in which case the fair value gold price under a gold standard could be $1500 to $3000.

Keep in mind all of the above gold prices are real and therefore don’t need to be further adjusted for inflation because the ratios’ denominators already account for changes in price over time.This is a thoughtful answer and he’s clearly given the topic serious consideration. My major objection is that the variables needed seem to be very hard to come by and there must be very large room for error.

My view is still the same. I think the safest way to look at gold is to consider its price to be wholly irrational. -

A Medical Marijuana Stock

Posted by Eddy Elfenbein on April 7th, 2009 at 3:10 pmOh dear lord. Check out Medical Marijuana, Inc. (CVIV.PK), formerly Club Vivanet:

Medical Marijuana, Inc. formerly Club Vivanet announced today that it filed a patent application for its invention, that potentially satisfies various governmental and the medical marijuana dispensaries’ needs for tax collection in the medical marijuana industry.

I think I know how this story ends. The middle part is still up in the air, but the ending isn’t.

(HT: Timbo) -

Not Buying Starbucks

Posted by Eddy Elfenbein on April 7th, 2009 at 2:39 pmI’m not buying this mini-rally for Starbucks (SBUX). The last three earnings reports have been AWFUL. Earnings come out on April 29 and 15 cents a share is looking pretty high. They might hit it since an earnings warning should have come out by now.

Earnings misses aren’t like athletes having a bad night. You can’t just shake it off. One earnings miss usually leads to another. It’s because companies have big problems with their business models. Starbucks has started cutting back on expenses, but it’s far too early to say things have turned around. -

RIP: Greg Newton

Posted by Eddy Elfenbein on April 7th, 2009 at 1:18 pmThis is awful news. I emailed Greg just a few days ago:

Our good friend and my personal confidant Greg Newton has passed away suddenly from a heart attack yesterday. He was driving to meet his fiancée Marsha where they were to begin a new life together in Florida.

I am devastated, and like many of you who listened to his wisdom and wit from our podcasts and his Naked Shorts blog, will miss him terribly.

Rest in peace my friend.

DaveNaked Shorts was a wonderful blog that looked at Wall Street with wit and insight. He will be missed.

-

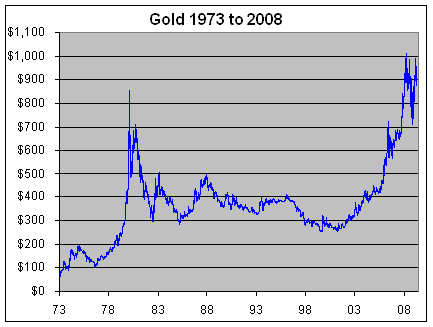

How Do You Value Gold?

Posted by Eddy Elfenbein on April 7th, 2009 at 12:09 pmI’d welcome any feedback on these questions since I have no idea of the answer: How should one determine the price of gold? What are the variables or ratios that someone ought to use?

I have to say that I have no idea how to make a judgment on the price of gold. It seems to me to completely irrational and that’s why I like to avoid it. With an asset like a bond, you can input a few variables and try to determine if the current yield is too high or too low. Of course, your assumptions may be wrong, but you can plainly see what went wrong.

With stocks, there are all sorts of models to determine value. These can also be wrong, and many are, but at least everyone knows what a P/E Ratio is. But for gold, I have no idea where to start.

Part of this I have to blame on gold bugs who seem to be overwhelmingly irrational and incoherent. I apologize to the more thoughtful gold bulls but your voices are drowned out by the mob.

The only argument I can make out is that gold will go higher because we’re bankrupt and the dollar is worthless. But does that justify any price? At what point could that argument still hold up, yet the price is simply too high? I get the feeling that few gold bugs have ever considered that question.

Are there metrics that you can point to that show how gold’s price should have plunged for over $800 in 1980 to around $250 in 2001, then to over $1,000 last March? My feeling is that a huge weighting to the price of gold is undefinable speculation. It just is and there’s no way to make sense of it.

Any ideas?

-

Population Growth and Wealth

Posted by Eddy Elfenbein on April 6th, 2009 at 1:52 pmMatthew Yglesias has an interesting post discussing the relationship between economic growth and population growth. He thinks that it’s possible to have long-term population decline alongside positive economic growth (though he says he’s not in favor of a declining population).

I’m not sure that’s correct. If a population is falling, then outside of war or disease, it must be due to either emigration or lower birth rates. That’s got to have a big impact on growth and innovation. In the other words, the size of GDP itself may boost per-capita GDP. If there’s heavy emigration, I would guess that would take a heavy toll on production since the émigrés would more likely be younger and more entrepreneurial.

If the falling population is due to declining birthrates, then that means the population is getting older. That would probably skew consumption away from innovative sectors. Not to mention that a falling population would place heavy pressure on a country’s social welfare obligations.

Yglesias posts a chart from Gregory Clark’s book, A Farewell to Alms: A Brief Economic History of the World which shows the lower population in pre-modern Britain led to higher wages. Sure, if all my neighbors are dropping dead from the plague my wages will rise, but that’s per-capita wealth which is very different from a growing economy.

The key part is the fitted line on Yglesias’s post that existed before Britain broke free from the Malthusian trap. I assume that the line would have to have a slope less than 0.5 (though it doesn’t appear that way). Either way, I think we can all agree that if another Great Plague comes along, wage growth won’t be a high priority. -

Doing Nothing Can Be Very Smart

Posted by Eddy Elfenbein on April 6th, 2009 at 11:11 amHere’s an interesting note on the Dow Jones Industrial Average (^DJI). Periodically, the gate keepers of the index add or delete stocks to keep things fresh. But if they had simply left the index alone, it would have done far better.

Since 1930, nine of the 30 stocks are still left. Twenty have been bought out or merged and only Bethlehem Steel has gone bust. The index would have finished 2008 at 14,600 instead of 8776. On top of that, the Dow’s weird weighting by price instead of market value also would have hurt you.

I don’t have the numbers on this but my guess is that a lot of the untouched Dow’s gain is due to one stock, IBM (IBM). The company was removed from the index in 1939 and put back in 1979. In those 40 years, IBM gained an astounding 22,000%.

Warren Buffett once said, “Lethargy bordering on sloth remains the cornerstone of our investment style.” Now you can see why. -

Shorting Reason

Posted by Eddy Elfenbein on April 5th, 2009 at 10:46 pmRichard Posner has a good review of Animal Spirits by George Akerlof and Robert Shiller. Here’s a snippet:

As one reads this book, one has the sense that deep down Akerlof and Shiller believe that being rational is the same as being right. That is a mistake. It prevents them from entertaining the possibility that what has now plunged the world into depression is a cascade of mistakes by rational businessmen, government officials, academic economists, consumers, and homebuyers, operating in an unexpectedly fragile economic environment, and that what is retarding recovery is not the “unreasoning fear” of which Franklin Roosevelt famously spoke but the rational fears–the reasoning fear, to use Roosevelt’s idiom–of businesspeople, consumers, and officials who confront economic uncertainties for which no one had prepared them.

I’ve often been critical of Robert Shiller’s work because I think he places too much emphasis on the short comings of investors. It’s true that folks often get carried away with things especially when prices get moving.

The truth is that many times it has been “different this time” or we did “enter a new era.” The speculation usually comes after a major change has taken place. Asset prices don’t easily confirm to a simple morality tale of people getting greedy and overpaying for stuff. If you scratch the surface, you’ll see that there are many concrete reasons (and government policies) that caused the animal spirits.

Just to give one example is that bubbles can often be confirmed by popular memes. The Nifty Fifty craze of the early 1970s specifically focused on companies that fostered social harmony (Xerox, McDonalds, Coke, Polaroid, Disney) which was a natural inclination after the turbulent 1960s.

The bubble of the 1990s seems to have been aided by the growth of the dubious first-mover-advantage theme. I remember being told countless times how some dot-com stock was “just like QWERTY.”

The story was that once a company became an industry standard, it would be the winner that took all. There was even a magazine called the Industry Standard. In 2000, the magazine sold more advertising than any magazine in America.

It didn’t last. -

Creditors Need to Take Some Risk

Posted by Eddy Elfenbein on April 4th, 2009 at 11:28 pmTyler Cowen has a good op-ed in the NYT pointing out a key factor in the bailouts—the true recipients are the creditors and that might cause future problems:

What the banking system needs is creditors who monitor risk and cut their exposure when that risk is too high. Unlike regulators, creditors and counterparties know the details of a deal and have their own money on the line.

But in both the bailouts and in the new proposals, the government is effectively neutralizing creditors as a force for financial safety. This suggests a scary possibility — that the next regulatory regime could end up even worse than the last.

The more closely a financial institution is regulated, the more it will be assumed that its creditors enjoy federal protection. We may be creating a class of institutions whose borrowing is, in effect, guaranteed by the government. -

Weekend Poll

Posted by Eddy Elfenbein on April 3rd, 2009 at 8:00 pm

Update: This question comes from the work of Daniel Kahneman and Amos Tversky, though I changed the amounts in order to experiment.

By pure rules of expected return, people should to take the 50-50 bet for $3000. Although that’s what most folks said, there’s still a significant percentage that chose the guaranteed $1,000. Incidentally, I don’t blame anyone for taking the $1,000. It really comes down to each individual’s risk tolerance.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His