-

The Jobless Rate Continues to Grow

Posted by Eddy Elfenbein on April 3rd, 2009 at 10:53 amI don’t have much to add about today’s awful jobs report. Let me say a few minor things. The official rate was reported as 8.5%. Technically, it was 8.543% which was only about 10,000 jobs away from 8.6%. At the present rate, that’s less than half-a-day’s job cuts. Over the last six months, the unemployment rate has ticked up 0.1% about every week.

Over the last nine years, the unadjusted adult population has grown by 23.3 million. The civilian labor force has grown by just 11.6 million which means that less than half of the increase in population is participating in the jobs market. The number of employed has grown by just 4.2 million. So even the increase that is participating in the job market, only 36% have jobs (bear in mind, I’m talking about the net increase). -

Cause Please Meet Effect

Posted by Eddy Elfenbein on April 3rd, 2009 at 9:58 amFebruary 23, 2004

May 16, 2007:

April 4, 2009

(HT: Joe W.)

-

Mark-to-Market Is More Realistic

Posted by Eddy Elfenbein on April 3rd, 2009 at 9:27 amIn honor of yesterday’s decision from FASB, we at Crossing Wall Street would like to review our legacy assets which include; three unicorns, eight hobbits (non-union), a half dozen minotaurs, two mermaids, a couple of CHUDs, several tic-tacs, true love and a smurf.

-

Forbes and the Flat Tax

Posted by Eddy Elfenbein on April 2nd, 2009 at 3:00 pmNow at his new perch at Reuters, Felix Salmon tweaks Steve Forbes for the news that Forbes magazine is cutting salaries by 10% for everything over $100,000:

This is taxing the rich! It’s class warfare! Why should those employees earning a six-figure salary be singled out for pay cuts? If you cut their pay, don’t you know that you’re going to reduce their incentive to work hard, and also the incentive for lower-earning employees to aspire to their position? And these are the most productive members of the firm! You’re punishing success! You should be giving the higher-paid employees a pay rise, instead — that will surely boost corporate revenues!

Come on Steve, walk the walk. If the rich can’t be treated equally with the poorer at Forbes, where is the hope for them in this world?I know he’s joking, but two things. Obviously, a cut in salary isn’t a tax. There’s a major difference between dealing with a private employer and government taxes. With the government, you have no choice.

Secondly, what Forbes is doing isn’t running away from the flat tax — it’s exactly how his flat tax works. Forbes has called for a 17% flat tax on income only above a specific level (that’s changed over the years). You may not like his principles, but in this care Forbes is walking the walk. -

What Caused Oil to Boom?

Posted by Eddy Elfenbein on April 2nd, 2009 at 1:29 pmA few months ago, I criticized the absurd 60 Minutes story which blamed speculators for the rise in oil prices. I said the story was “wretched, incoherent and it engages in the worst form of scapegoating.”

As is often the case, conspiracy theories sell. If you have a high tolerance for imbeciles, check out some of the comments when Seeking Alpha posted my piece.

Now James Hamilton has looked into the behavior of the oil boom and bust and he comes to the conclusion that oil was impacted by…are you ready…supply and demand.But while the question of the possible contribution of speculators and the Fed is a very interesting one, it should not distract us from the broader fact: some degree of significant oil price appreciation during 2007-08 was an inevitable consequence of booming demand and stagnant production.

(Via: Kedrosky.)

-

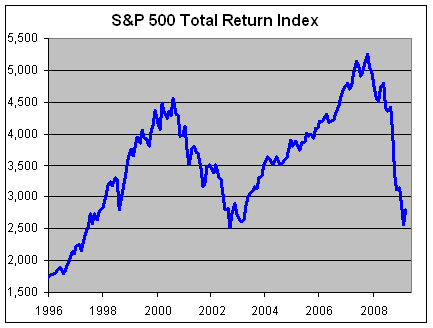

S&P 500 Total Return Index

Posted by Eddy Elfenbein on April 2nd, 2009 at 1:13 pmEven if we include dividends, the S&P 500 has lost money over the last 11 years.

And that’s not even adjusting for inflation. Ugh! -

Daniel Gross on Dumb Money in the Newspaper Industry

Posted by Eddy Elfenbein on April 2nd, 2009 at 8:30 amDaniel Gross points out that the failure of many newspapers isn’t always due to the decline of an industry, but to stupid moves from managers:

In 2007, legendary real estate investor Sam Zell decided that a talent for good timing in flipping office buildings made him an expert on the ailing newspaper industry. In December 2007, he closed on the $8.2 billion purchase of the Tribune Co., which owned the Los Angeles Times, the Chicago Tribune, and the Chicago Cubs. Zell put down just 4 percent of the purchase price—$315 million—and borrowed much of the rest, leaving the company with a $13 billion debt burden. This deal was the purest expression of the “dumb money” mentality. The only hope Zell had of making a dent in the debt load and keeping current on the $800-million-plus annual interest tab was to sell off trophy properties like the Cubs, office buildings, and big-city newspapers—assets that themselves don’t throw off lots of income but whose purchase requires tons of cheap credit. Tribune Co. filed for bankruptcy Dec. 8, 2008.

-

If There’s No Media, Is It Still a Protest?

Posted by Eddy Elfenbein on April 1st, 2009 at 11:42 amHere’s a truly post-modern photo I saw over at DealBreaker.

-

The Failure of the Junk Bond Market

Posted by Eddy Elfenbein on April 1st, 2009 at 9:52 amSteve Sailer writes on anti-usury laws and comments on the failure of the junk bond market:

Also, a generation freed from limits on interest rates is typically going to push them too far, with widespread damage. We saw that with Mike Milken’s junk bonds back in the 1980s, which worked pretty well at first, but generated so much profit that ever junkier junk bonds came out, culminating in the 1991 recession.

I have to disagree. Since junk bonds did so well during the 1980s, it suggests that credit had not been properly distributed and those who took the risk, were paid handsomely.

As with many cases, the junk bond market was simply pushed to far, though that was happening. The big problem was that the junk bond market got a very big push from the government. The Financial Institutions Reform, Recovery and Enforcement Act of 1989 (also known as Firrea) forced S&Ls to divest their junk bonds. That triggered an avalanche of selling which in led to the recession of 1990-91.

Research has shown that junk bond issuers outperformed the rest of the economy in terms of job growth, sales and productivity.

Incidentally, FIRREA also gave “both Freddie Mac and Fannie Mae additional responsibility to support mortgages for low- and moderate-income families.” -

It Can’t Possibly Go Any Lower

Posted by Eddy Elfenbein on April 1st, 2009 at 7:51 amAfter careful consideration, I’ve come to the conclusion that General Motors (GM) is a very strong buy.

For more details, read here.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His