-

The SEC takes on the First Amendment

Posted by Eddy Elfenbein on July 14th, 2008 at 9:51 amPhiladelphia, 1787:

Congress shall make no law respecting an establishment of religion, or prohibiting the free exercise thereof; or abridging the freedom of speech, or of the press; or the right of the people peaceably to assemble, and to petition the Government for a redress of grievances.

The Securities and Exchange Commission today announced that the SEC and other securities regulators will immediately conduct examinations aimed at the prevention of the intentional spread of false information intended to manipulate securities prices. The examinations will be conducted by the SEC’s Office of Compliance Inspections and Examinations, as well as the Financial Industry Regulatory Authority and New York Stock Exchange Regulation, Inc.

-

The Feds Step In

Posted by Eddy Elfenbein on July 14th, 2008 at 9:47 amThe government moves to help Fannie and Freddie:

Alarmed by the sharply eroding confidence in the nation’s two largest mortgage finance companies, the Bush administration on Sunday asked Congress to approve a sweeping rescue package that would give officials the power to inject billions of federal dollars into the beleaguered companies through investments and loans.

In a separate announcement, the Federal Reserve said it would make one of its short-term lending programs available to the two companies, Fannie Mae and Freddie Mac. The Fed said that it had made its decision “to promote the availability of home mortgage credit during a period of stress in financial markets.”

An official said that the Fed’s decision to permit the companies to borrow from its so-called discount window was approved at the request of the Treasury but that it was temporary and would probably end once Congress approved Treasury’s plan. Some officials briefed on the plan said Congress could be asked to extend the total line of credit to the institutions to $300 billion. -

After Hours: Mississippi John Hurt

Posted by Eddy Elfenbein on July 11th, 2008 at 3:43 pmDon’t let the market gives you the blues. Have a listen to the great Mississippi John Hurt.

-

Not Since 1982

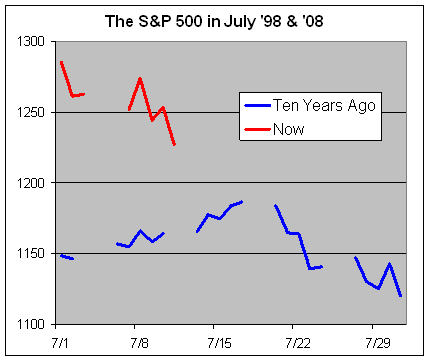

Posted by Eddy Elfenbein on July 11th, 2008 at 1:23 pmFor the first time since August 18, 1982, the S&P 500 might be lower than it was 10 years before.

The S&P 500 has been as low as 1,225.82 today. Today could be our lowest close since June 13, 2006. And if we go below 1,223.69, it will be our lowest close since November 9, 2005.

We’re already lower than where we were on the last day of trading in 1998. Here’s a look at how we’re doing this July (red line) compared with July 1998 (blue line):

Even if don’t break a 10-year trailing close this month, it will probably happen soon. The market is still over 19% below its March 2000 high. Are we going to be 24% higher 20 months from now? -

Jeremy Siegel on the Bear Market

Posted by Eddy Elfenbein on July 10th, 2008 at 9:39 am -

World’s Smallest Violin

Posted by Eddy Elfenbein on July 10th, 2008 at 8:48 amLouise Story sits down with a contrite John Devaney.

One by one, John Devaney sold his treasures, hoping to forestall what was in the end inevitable. He sold his Renoir and his Gulfstream, his home and his helicopter. Even his cherished yacht — gone.

But on Wednesday Mr. Devaney, who made and then lost a fortune trading mortgage investments, finally called it quits. He shut his hedge fund, and told his investors that all their money was gone too.

“I’m devastated, I’m totally devastated,” Mr. Devaney said by telephone from Aspen, Colo feel horrible that I’ve lost my own money and that so many people who saw the skills I have and trusted in us have now been hurt.” -

The Warren Buffett Rap

Posted by Eddy Elfenbein on July 9th, 2008 at 12:14 pm -

Correlation Doesn’t Mean Causation

Posted by Eddy Elfenbein on July 9th, 2008 at 9:59 amI’m not blaming anyone. I’m simply relaying the facts. In other words, I report, you decide.

-

Best Headline of the Day

Posted by Eddy Elfenbein on July 8th, 2008 at 5:22 pmThank you, Associated Press:

U.S. exports cigarettes, bras, bull semen to Iran

U.S. exports to Iran grew more than tenfold during President Bush’s years in office even as he accused it of nuclear ambitions and sponsoring terrorists.

America sent more cigarettes to Iran — at least $158 million worth under Bush — than any other product.

Other surprising shipments during the Bush administration: brassieres, bull semen, fur clothing, sculptures, perfume, musical instruments and military apparel.

Top states shipping goods to Iran include California, Florida, Georgia, Louisiana, Michigan, Mississippi, New Jersey, North Carolina, Ohio and Wisconsin, according to an analysis by The Associated Press of seven years of U.S. government trade data.

Despite increasingly tough rhetoric toward Iran, which Bush has called part of an “axis of evil,” U.S. trade in a range of goods survives on-again, off-again sanctions originally imposed nearly three decades ago. -

The S&P 500 Priced in Eggs

Posted by Eddy Elfenbein on July 8th, 2008 at 1:31 pmFelix Salmon links to a chart by DeForest McDuff of the S&P 500 priced in eggs. McDuff writes:

Investment returns matter only to the extent that you can buy more “stuff” in the future. The U.S. stock market has been slowly losing real purchasing power for almost a decade, with no signs yet of a trend reversal.

It’s true that the prices of hard assets like oil, gold, and omelettes have been increasing rapidly, but this is a direct consequence of decades of underinvestment in these asset classes. If you’re not thinking about investing in terms of purchasing power, then you’re playing the wrong game.This is correct, however, I caution against looking at the stock market in the price of some commodity. This is a subtle but important point. A lot of financial analysis involves developing a “feel” for the numbers.

The problem of pricing the market in terms of some commodity is that it often involves two data sets with very different characteristics. Equity prices are tied to corporate profits and therefore cyclical. At least in theory. Commodity prices, however, are often marked by price disruptions, meaning dramatic price spikes. If you look at the long-term chart of nearly every commodity, you’ll see a few large spikes followed by long periods of not much.

That’s why when you compare stock prices to a commodity, it often tells you less about equity prices and more about the commodity. From my experience, the most often used example is gold. For the last 35 years, the prices of gold has been a wild ride from around $30 to over $800 back to $250 and then up to $1,000. The stock market can be wild but nothing like that. Also, gold doesn’t pay dividends where the market does. It may not be much each quarter, but if you’re looking at a chart going back a few decades, it does add up.

Think of it this way. A commodity is a thing. In 1,000 years, gold will still be gold. But equity is what you do with the thing to make money. If you make enough money, you can buy more things. A stock can own a commodity, but a commodity can’t run a business.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His