-

Sir John Templeton Dead at 95

Posted by Eddy Elfenbein on July 8th, 2008 at 1:01 pm

One of the true giants has passed:Sir John Templeton, who has died aged 95, was a legend in the world of fund management and invested much of his multi-million pound fortune in promoting spiritual and religious progress.

Sir John Templeton

Templeton boasted one of the longest and most successful track records on Wall Street. From its foundation in 1954, his Templeton Growth Fund grew at an astonishing rate of nearly 16 per cent a year until Templeton’s retirement in 1992, making it the top performing growth fund in the second half of the 20th century.

A $100,000 stake invested in 1954 would, with distributions reinvested, would have grown to $55 million in 1999.

The Templeton formula was simple in theory, though not easily achieved in practice.

He looked for bargains — shares selling well below their asset values due to temporary circumstances — and would usually hold on to them for five years or more until they reached what he considered to be their true worth.

It was an approach that required rigorous research and determination not to be swayed by the fashions of the moment. -

Tom Gallagher on the Global Economy

Posted by Eddy Elfenbein on July 8th, 2008 at 12:49 pmI’ve embedded the whole video, but the key part is Tom Gallagher’s talk. I’d recommend watching 24:05 to 32:15.

-

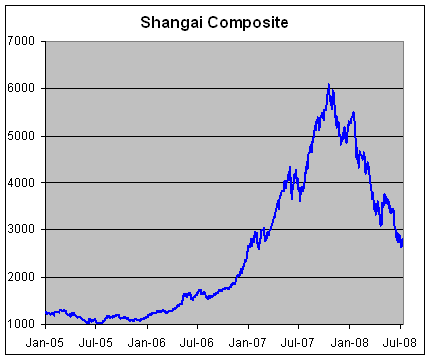

The Chinese Bubble Bursts

Posted by Eddy Elfenbein on July 8th, 2008 at 10:57 amIn early 2007, the Shanghai Composite made news all around the world when it plunged 8.8%. Let’s just say that the pullback was a buying opportunity. Eight months later, the index was 120% higher.

Nine months after that, which is today, we’re back where we started. Thanks for the wild ride!

-

The Pickens Plan

Posted by Eddy Elfenbein on July 8th, 2008 at 8:21 amT. Boone Pickens is launching an ad blitz on how to fix the energy crisis.

Today, Pickens will take the wraps off what he’s calling the Pickens Plan for cutting the USA’s demand for foreign oil by more than a third in less than a decade. To promote it, he is bankrolling what his aides say will be the biggest public policy ad campaign ever. The website, www.pickensplan.com, goes live today.

Jay Rosser, Pickens’ ever-present public relations man, promises that Pickens’ face will be seen on Americans’ televisions this fall almost as frequently as John McCain’s and Barack Obama’s.

“Neither presidential candidate is talking about solving the oil problem. So we’re going to make ’em talk about it,” Pickens says.

“Nixon said in 1970 that we were importing 20% of our oil and that by 1980 it would be 0%. That didn’t happen,” Pickens says. “It went to 42% in 1991 with the Gulf War. It’s just under 70% now. Where do you think we’re going to be in 10 years when our economy is busted and we’re importing 80% of our oil?”

Finding solutions to other major issues, including health care, are important, he concedes. But “If you don’t solve the energy problem, it’s going to break us before we even get to solving health care and some of these other important issues.” And it has to be done with the same sense of urgency that President Eisenhower had when he pushed the rapid development of the interstate highway system during the Cold War.

Of course, Pickens also has a particular solution in mind.

Wind. And natural gas. -

Top 10 Stocks Since the Last Recession

Posted by Eddy Elfenbein on July 8th, 2008 at 2:10 amThe Motley Fool lists the 10 best-performing stocks since the last recession (3/1/2001-7/6/2008):

Company……………………………..Return

Ultra Petroleum……………………..4,378%

Southwestern Energy…………….3,348%

Potash…………………………………2,070%

Walter Industries………………….1,860%

Apple…………………………………..1,715%

Canadian Natural Resources…..1,658%

Intuitive Surgical……………………1,627%

Research In Motion………………..1,548%

Range Resources…………………..1,515%

Terra Industries…………………….1,236% -

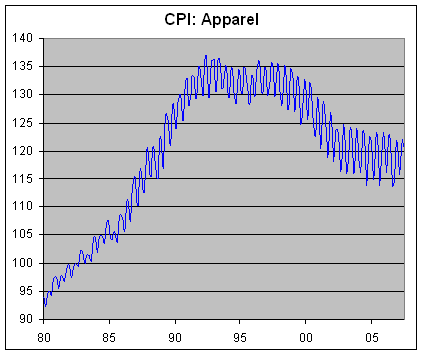

Inflation in Apparel

Posted by Eddy Elfenbein on July 7th, 2008 at 4:15 pmThere’s certainly lots of inflation in commodities, but there’s hardly any in other parts of the economy. Here’s a look at the CPI Apparel Index (not seasonally adjusted as the wiggles suggest). Prices are basically where they were 20 years ago.

-

Southwest Airlines on WallStip

Posted by Eddy Elfenbein on July 7th, 2008 at 1:31 pm

In 1974, you could have picked up shares of LUV for just a penny. That’s just adjusted for 14 stocks splits totaling 300-for-1 (two 2-for-1s, nine 3-for-2s, and three 5-for-4s). -

Who Killed the Economy

Posted by Eddy Elfenbein on July 7th, 2008 at 1:10 pmFill out your brackets today. Since “Morons Who Borrowed Way Too Much For a Ridiculously Overpriced House that They Couldn’t Afford Anyway” isn’t participating, I’m going with Greenspan.

-

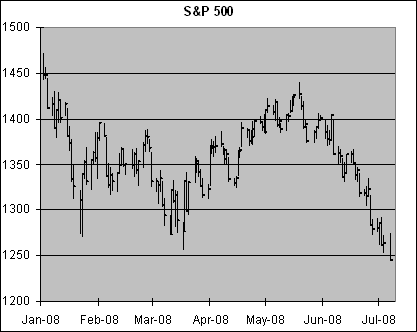

So Long SPX 1250

Posted by Eddy Elfenbein on July 7th, 2008 at 1:06 pm

-

Short Interest Is Up 55%

Posted by Eddy Elfenbein on July 7th, 2008 at 12:16 pmCould this be some sort of bubble?

Record bets against U.S. stocks may mean the market is on the verge of a rebound fueled by purchases of shares that were sold short, according to JPMorgan Chase & Co.

So-called short interest on the New York Stock Exchange has risen 55 percent this year to a record 3.6 percent of listed shares, JPMorgan Chief Equity Strategist Thomas J. Lee wrote in a report today. In a short sale, an investor sells borrowed shares in anticipation of being able to buy them back later, or “cover,” at a lower price.

Given the “extreme levels” of short interest, positive catalysts for the market “could trigger a substantial short- covering rally,” New York-based Lee wrote.The article notes that 36% of companies in the S&P 500 have at least 5% of their shares sold short.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His