-

Ryanair’s CEO Promises In-Flight Blow Jobs

Posted by Eddy Elfenbein on July 3rd, 2008 at 1:50 pm -

Looking at the Bear

Posted by Eddy Elfenbein on July 3rd, 2008 at 7:56 amThe S&P 500 closed today at 1,261.52 which is the lowest close since July 24, 2006. The index is now off 19.4% from its all-time high of October 9, 2007.

Since October 9, there have been 184 trading days. This is how the days of the week have panned out:

Monday………….-3.69% (35 data points)

Tuesday………….5.26% (36)

Wednesday…….-6.17% (39)

Thursday………..-1.93% (37)

Friday…………….-13.59% (37)

So the bear market is heavily, but not exclusively, a Friday phenomenon. The other four days of the week have lost a combined -6.72%.

The most surprising fact is that of the 184 days, 92 have been up, 91 were down and one was unchanged (January 3). -

Best Little Whorehouse in Wellesley

Posted by Eddy Elfenbein on July 2nd, 2008 at 3:47 pmProfessor Greg Mankiw notes that in his hometown of Wellesley police recently shut down a (ahem) massage business. This is the second time in the last six months that the police of busted such an enterprise.

But here’s the interesting fact. One of the people just arrested, William Eastwick, is the same guy who tipped off the police on the first arrest.Eastwick tipped Wellesley Police off to that operation, said [Wellesley Police Sgt. Marie] Cleary, although it is unclear why he did that.

Clearly, Cleary is unclear, but to Dr. Mankiw, it’s perfectly clear.

Like any businessman, Mr Eastwick prefers to have fewer competitors. Some businessmen lobby Congress for trade restrictions. Others alert the police to the brothel down the block. And when using the power of the state to thwart competition, they can both pretend to be acting in the public interest.

Sometime you need a small example to see the big picture. I wouldn’t say the state and Mr. Eastwick are in bed together, they just provide similar services.

-

CircuitBuster Now Officially Busted

Posted by Eddy Elfenbein on July 2nd, 2008 at 12:14 pmA three-act play:

April 14

Blockbuster offers $1 billion for Circuit City

May 10

Circuit City Opens Its Books to Blockbuster

July 2

Blockbuster Withdraws Offer for Circuit City

This was one the worst ideas to hit the Street in a long time. The good thing is that shareholders had far better judgment than management. Score one for the wisdom of crowds. -

Samuel Israel Surrenders

Posted by Eddy Elfenbein on July 2nd, 2008 at 11:53 am

Sam finally gives up:Samuel Israel, the fugitive hedge-fund firm founder convicted of directing a $400 million fraud at Bayou Group LLC, surrendered in Massachusetts, almost a month after fleeing instead of starting his 20-year prison sentence.

Israel, 48, turned himself in at 9:15 a.m. today, according to Sue Anderson, assistant to Southwick, Massachusetts, Police Chief Mark Krynicki. Southwick, near the Connecticut border, is about 117 miles from where Israel disappeared in New York the day he was to report to a federal prison northwest of Boston.

“He is in federal custody,” Rebekah Carmichael, a spokeswoman for U.S. Attorney Michael Garcia in Manhattan, said in an e-mailed statement.

Israel pleaded guilty in 2005 to securities fraud. His car was found June 9 on a bridge north of New York City with the message “suicide is painless” written in the dust on its windshield. Within a week, state and federal authorities in New York, where he pleaded guilty, ruled out suicide and launched an international manhunt. -

UnitedHealth Lowers Guidance

Posted by Eddy Elfenbein on July 2nd, 2008 at 9:49 amAs I expected, UnitedHealth (UNH) lowered its profit guidance for this year. The company now sees EPS coming in between $2.95 to $3.05.

Chief Executive Stephen J. Hemsley noted the quarter’s results were hurt by lower margins, adding that second-quarter weakness also stems from reduced margins at its risk-based businesses and Medicare operations. “We are continuing to take the aggressive specific steps necessary to improve our operating performance, as well as to better position our organization for sustained future growth,” he said. To stop weakness in the risk-based operations, the company has been letting go of some customers who didn’t generate enough profits.

The company is also paying about $900 million to settle two class-action lawsuits regarding the back-dating of stock options. Assuming the current forecast is correct, then UNH is a very cheap stock. The shares are up nicely today.

-

This Just In…

Posted by Eddy Elfenbein on July 1st, 2008 at 3:18 pm -

Worst First Halves Since 1971

Posted by Eddy Elfenbein on July 1st, 2008 at 3:05 pmHere are the ten worst first halves since 1971, going by the S&P 500’s total return:

Year…………………Gain

2002………………-13.16%

2008………………-11.91%

1973………………-10.38%

1974………………-10.17%

1982………………-7.83%

2001………………-6.70%

1984………………-4.90%

1977………………-4.38%

1994………………-3.39%

1981………………-0.95% -

Grasso Wins

Posted by Eddy Elfenbein on July 1st, 2008 at 2:51 pmIt’s hard to see multi-millionaire as victims, but Eliot Spitzer’s (aka Client #9) crusade against Dick Grasso was contemptible and an abuse of the legal system. The case against him was thrown out today. Last week, the court threw out four of the six claims against Grasso. The other two were dismissed today.

The New York Stock Exchange awarded Grasso a pay package worth $190 million. Is that too high? Probably. Is it illegal? Of course not.“My reaction is, I told you so,” Langone said today in a telephone interview. “There was never a case here. What more can we say? The enormous waste was a travesty.”

One final note on Mr. Spitzer. When he checked in the Mayflower Hotel for his meetings with Ms. Dupree, he used the nom de bork, George Fox. That’s one his friend’s names.

Classy guy. -

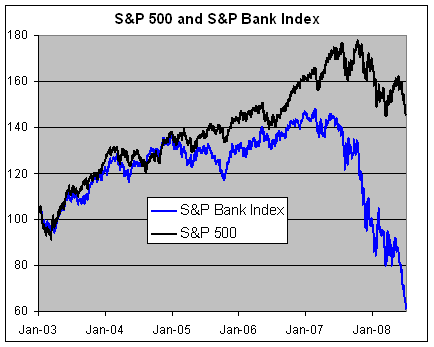

I Think this Chart Sums It Up Well

Posted by Eddy Elfenbein on July 1st, 2008 at 10:31 am

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His