-

Mahler’s Symphony 5: mvt. 4

Posted by Eddy Elfenbein on April 11th, 2008 at 7:34 pm -

So this Banker Walks Into a Bar

Posted by Eddy Elfenbein on April 11th, 2008 at 11:04 amWho knew the Fed was so darn funny.

Well OK, not that funny, but the central bank released its transcripts from 2002 and I’ve collected some highlights.

—

MR. STOCKTON. Thank you, Mr. Chairman. I was impressed at the last meeting with the creative language used by many members of the Committee to describe the economic outlook. So this morning I thought I’d try my hand at explaining the forecast using some of that language. To begin with the current quarter, I can report that—as the saying apparently goes—there has been about as much pumpkin as we had earlier anticipated though there is clearly less pumpkin now than in the third quarter.

CHAIRMAN GREENSPAN. It turned out to be seedy.

—

MR. MCTEER. Mr. Chairman, I’m going to miss Jerry Jordan’s anecdotes and vignettes, but I might note that in this case I think he’s behind the curve. We’ve already done the research and found that forklifts are indeed a leading indicator, but backhoes are a lagging indicator.

CHAIRMAN GREENSPAN. It’s still a very uplifting thing.

From November 6, 2002

—

MR. MOSKOW. For instance, the corrugated box industry, which had been showing signs of strength, now has flattened out, you could say. Or you could say that those manufacturers now view the box as half empty rather than half full.

—

CHAIRMAN GREENSPAN. You say that with a smile? For the official record, we will indicate that he smiled.

—

Moreover, we had a fascinating exchange at our recent advisory council meeting between the steel workers’ union leader and one of the country’s leading duck farmers. The issue was how retaliation to the steel tariffs by some of our trading partners is hurting other subsidized industries.

CHAIRMAN GREENSPAN. What a “fowl” thought!

—

MR. JORDAN. Actually we were in Covington, Kentucky, so there were a lot of references to what it was like over half a century ago when the Chairman played with a band there. In fact, it was pretty exciting.

CHAIRMAN GREENSPAN. I don’t know if I should admit to this, but in the back room there were very peculiar things going on.

—

MS. BIES. However, since I still have a house in Memphis for sale, I’m less inclined to believe that there’s a widespread bubble.

MR. GRAMLICH. Is that house for sale?

MS. BIES. Oh yes.

VICE CHAIRMAN MCDONOUGH. Still.

CHAIRMAN GREENSPAN. Are you bidding?

MR. GRAMLICH. No, I’m just pointing out that there’s a bubble.

—

MR. BERNANKE. Mr. Chairman, I appreciate your analysis. I’m just wondering how you’re going to get all of that in the statement!

CHAIRMAN GREENSPAN. I wrote it in disappearing ink!

—

CHAIRMAN GREENSPAN. Okay, I’ll try my best. I can’t guarantee that what I say will always come out the way I want it to. But I’ve been around long enough that I can put more words into fewer ideas than anyone else I know! -

The Final Frontier

Posted by Eddy Elfenbein on April 11th, 2008 at 10:17 amThe theme for today is bankruptcies. Frontier Airlines (FRNT) is filing for bankruptcy. Until a few minutes ago, I was an embarrassed shareholder of Frontier. The stock had done so poorly that I had basically ignored it in my portfolio. It was part of my first tracking list in 2005 before I formalized my Buy List at the beginning of 2006. Now I’ve just taken a 95% loss. Let us never speak of this again.

-

Linens ‘n Things Expected to File for Bankruptcy

Posted by Eddy Elfenbein on April 11th, 2008 at 10:03 amOne of Bed Bath & Beyond‘s (BBBY) major competitors, Linens ‘n Things, seems to have come to the end of the road. The WSJ said that the company is expected to file for bankruptcy protection by Tuesday.

Two years ago, the company was part of a private equity buyout from Apollo Management, which has filed to go public (or as DealBook calls it, an Un-IPO). Bed Bath & Beyond is down a bit this morning but I don’t see how a competitors’ bankruptcy can be all that bad. -

Deep Inside an SEC Filing

Posted by Eddy Elfenbein on April 9th, 2008 at 9:05 pmEver heard of CHDT Corp. (CHDO)?

Me neither.

Anywho, I was reading their 10-K (page 29) and I came across this under the discussion of country risks.While dramatic anti-trade shit in Chinese policy or laws would seem to be clearly against the best interests of China and its current economic trends, China has a central government with the authority to make such changes.

It’s true. That shit would be so totally fucked up.

-

Ugh….

Posted by Eddy Elfenbein on April 9th, 2008 at 4:26 pmBed Bath & Beyond (BBBY) just reported that it earned 66 cents a share for its fourth quarter.

Here are the earnings results going back a few years:Quarter Sales Gross Profit Operating Profit Net Profit EPS $356,633 $146,214 $28,015 $17,883 $0.06 $451,715 $185,570 $53,580 $33,247 $0.12 $480,145 $196,784 $50,607 $31,707 $0.11 $569,012 $238,233 $77,138 $48,392 $0.17 $459,163 $187,293 $36,339 $23,364 $0.08 $589,381 $241,284 $70,009 $43,578 $0.15 $602,004 $246,080 $64,592 $40,665 $0.14 $746,107 $311,802 $101,898 $64,315 $0.22 $575,833 $234,959 $45,602 $30,007 $0.10 $713,636 $291,342 $84,672 $53,954 $0.18 $759,438 $311,030 $83,749 $52,964 $0.18 $879,055 $370,235 $132,077 $82,674 $0.28 $776,798 $318,362 $72,701 $46,299 $0.15 $903,044 $370,335 $119,687 $75,459 $0.25 $936,030 $386,224 $119,228 $75,112 $0.25 $1,049,292 $443,626 $168,441 $105,309 $0.35 $893,868 $367,180 $90,450 $57,508 $0.19 $1,111,445 $459,145 $155,867 $97,208 $0.32 $1,174,740 $486,987 $161,459 $100,506 $0.33 $1,297,928 $563,352 $231,567 $144,248 $0.47 $1,100,917 $456,774 $128,707 $82,049 $0.27 $1,273,960 $530,829 $189,108 $120,008 $0.39 $1,305,155 $548,152 $190,978 $121,927 $0.40 $1,467,646 $650,546 $283,621 $180,980 $0.59 $1,244,421 $520,781 $150,884 $98,903 $0.33 $1,431,182 $601,784 $217,877 $141,402 $0.47 $1,448,680 $615,363 $205,493 $134,620 $0.45 $1,685,279 $747,820 $304,917 $197,922 $0.67 $1,395,963 $590,098 $148,750 $100,431 $0.35 $1,607,239 $678,249 $219,622 $145,535 $0.51 $1,619,240 $704,073 $211,134 $142,436 $0.50 $1,994,987 $862,982 $309,895 $205,842 $0.72 $1,553,293 $646,109 $154,391 $104,647 $0.38 $1,767,716 $732,158 $211,037 $147,008 $0.55 $1,794,747 $747,866 $203,152 $138,232 $0.52 $1,933,186 $799,098 $259,442 $172,921 $0.66 -

Irony Overload

Posted by Eddy Elfenbein on April 9th, 2008 at 1:55 pmHere’s a report from Bear Stearns on falling business optimism.

(Via: RCM) -

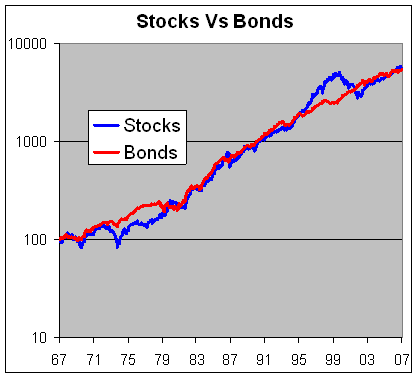

Stocks Against Bonds

Posted by Eddy Elfenbein on April 9th, 2008 at 1:31 pmI recently received the latest Ibbotson Yearbook in the mail the other day. If you’re not familiar with it, the book is a great source for long-term returns of different asset classes (click here for more info).

What I find interesting is that the spread between the returns of stocks and bonds really isn’t that much. I think would surprise many investors that boring bonds have held their own. Over the last 40 years, stocks have beaten bonds by a final score 10.5% to 8.4%.

The difference is theoretically due to greater risk for stocks. (Note: This is different from the usual equity risk premium which looks at stocks versus T-bills. Here I’m looking at stocks and long-term corporate bonds.)

Here’s a chart I made of stocks and long-term corporate bonds. The only difference is that I stretched out the bond returns by 2% a year.

These two lines have tracked each other remarkably closely. In the 1970s, bonds took a big lead over stocks, and in the late 1990s, stocks shot ahead of bonds. Besides that, it’s been pretty close. You can also see that the market rally of the 1980s really wasn’t much of a bubble, nor is today’s market out of whack by historical standards.

Let me add that I do not think this is a good way to time the market. -

The Joys of Living in Washington

Posted by Eddy Elfenbein on April 9th, 2008 at 1:02 pmI went out for lunch just now and my entire house started to rumble. What was it?

-

Passing Along Without Comment

Posted by Eddy Elfenbein on April 9th, 2008 at 11:35 amI apologize for including the first few tedious paragraphs but they’re needed for the surprise coming at the end.

Climate change tops list of risks to insurers

Potential climate change is the greatest strategic risk currently facing the property and casualty insurance industry, according to an Ernst & Young report. Demographic changes and catastrophic events follow closely behind.

For the study, Strategic Business Risk 2008, Ernst & Young and Oxford Analytica interviewed more than 70 industry analysts from around the world to identify the emerging trends and uncertainties driving the performance of the global insurance sector over the next five years.

The Top 10 risks identified were: climate change; demographic shifts in core markets; catastrophic events; emerging markets; regulatory intervention; channel distribution; integration of technology with operations and strategy; securities markets; legal risk; and geopolitical or macroeconomic shocks, a release says.

Many of the risks are interlinked, a company release notes, and raise questions about how these risks will change what companies offer customers, the way that they offer their services and where.

The analysts identified five additional emerging risks (not part of the Top 10) that have the potential to become as significant during the next five years.

These include: over reliance on model-based risk management; threats to industry reputation; losing the war for talent; increasing exposure to global regulatory heterogeneity; and the possible emergence of entirely new risks.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His