-

The SI Swimsuit Indicator

Posted by Eddy Elfenbein on February 12th, 2008 at 1:27 pm

This year’s cover features Marisa Miller which could be very bullish for stocks. When an American, such as Ms. Miller, appears on the cover, the Dow has gained an average of 13.9%. When there’s no American on the cover, the Dow has only gained 7.2%.

To think that some people still believe in EMH.

(Via Bespoke). -

The S&P 500 and Its Earnings

Posted by Eddy Elfenbein on February 12th, 2008 at 1:15 pmHere’s a look at the S&P 500:

The chart follows a logarithmic scale. (If I were smarter, I’d know how to make a logarithmic chart in Excel where I could zoom in on my high and low points. Since I can’t, this will have to do.)

The black line is the S&P 500 and it follows the left scale. The blue line is earnings and it follows the right scale. Where the lines intersect is a P/E ratio of 15.85 (which is 10^1.2).

In my opinion, this really wasn’t a valuation bubble where valuations overshot prices. Instead, the fundamentals tumbled beneath prices. -

The Porn IPO

Posted by Eddy Elfenbein on February 12th, 2008 at 9:46 amFrom the Guardian:

The stock market is to provide its first listing for a pornography publishing group as the adult magazines empire founded by Express owner Richard Desmond next week seeks a listing on the junior Plus Market.

Interactive Publishing, a shell group, is floating at the same time as agreeing a reverse takeover deal with Trojan Publishing, a private business that has built up a large portfolio of top-shelf titles such as Asian Babes, Forty Plus and New Talent.

Before buying rights to about 30 former Desmond titles last year, Trojan acquired about a dozen mostly adult magazines from British Virgin Islands-registered AML Publishing Trust in June 2006. A month later it signed a deal with Penthouse, licensing rights to Forum, an adult magazine for which Alastair Campbell once wrote a column entitled Riviera Gigolo. -

Gilead on Wall Strip

Posted by Eddy Elfenbein on February 11th, 2008 at 3:37 pm

Today, Julie looks at Gilead (GILD). What I find amazing about this company is that it’s able to maintain 40% net profit margins. That’s crazy. I think if you go any higher, you’re officially in the mafia. -

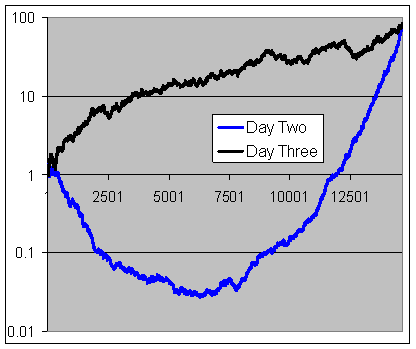

Do Stock Prices Have Memory?

Posted by Eddy Elfenbein on February 11th, 2008 at 1:44 pmFelix Salmon recently had a post about a bet between Justin Wolfers and Barry Ritholtz on the stock market and trends. Barry took the pro-trend view while Justin stood for random walks. (For the record, Justin won $20 from Barry.)

There’s an emerging amount of literature on this topic and it’s starting to point toward the trend camp. As strange as this may sound, stock prices seem to have a bit of “memory.” One day’s move has an impact on the next day’s move. It’s not big, but it’s there. If the market followed a random walk, this shouldn’t happen. In my mind, this is another chink in the armor of EMH that can’t be easily dismissed.

Here’s a good example of what I mean. Plus, I guarantee you that this is one of freakiest charts you’ll see all day:

Ok, some explanation is needed. I took every daily change of the S&P 500 from 1950 to today and ranked them, left to right, going from worst to best. The blue line shows the cumulative gain of the next day’s market.

As you can see, if you stayed in after bad days, the market kept going down. After flat days, the market remained somewhat flattish. And after good days, the market continued to rally. Whatever one day’s trend was, it followed through to the next day.

The blue crosses 1.0 at a point that corresponds with a daily gain of 0.64%. This means that the market’s entire gain has come on days following a 0.64% up move. The rest of the time (over 80%), the market is net flat. Half the market’s gain came on day’s following 3.2% up moves. On average, that happens slightly less than once a year.

The black line shows the market’s behavior two days later and it’s much closer to what we would expect, a growing line without any strong discernable trend. Actually, to the extent there is a trend, it seems to be a small reversal from what the market did two days before (notice the strong rise early on followed by a weaker rally). Roughly speaking, two days after the market drops more than 0.8%, the market rises at an annualized rate of nearly 28%.

If the market is trend sensitive, then these reversals are crucial. They appear to happen after extreme moves.

-

W.R. Berkley’s Earnings

Posted by Eddy Elfenbein on February 11th, 2008 at 12:56 pmW.R. Berkley (BER) just reported its fourth-quarter earnings. For the last three months of the year, net income dropped to from $198.1 million to $184.1 million. On a per-share basis, that’s a fall from 98 cents to 97 cents. With insurance companies, it’s better to look at operating results. Here, BER saw its number drop from $193.7 million to $183.2 million, which is actually a penny per share increase to 97 cents a share. That beat Wall Street’s estimate by two cents a share.

For the full year, Berkley’s operating income was $3.73 per share which was a nice increase over the $3.46 per share from 2006. Wall Street currently sees BER earnings $3.86 for 2008 which is a pretty small increase. Still, it means that the shares are going for less than eight times this year’s earnings. This is a good company going for a good price. -

Changes to the Dow

Posted by Eddy Elfenbein on February 11th, 2008 at 9:09 amThe gatekeepers of the Dow Jones Industrial Average (^DJI) have decided to boot Altria (MO) and Honeywell (HON) from the index. The two new additions will be Bank of America (BAC) and Chevron (CHV).

Chevron was in the index from 1930 to 1999, though for much of the time it was known as Standard Oil of California. Honeywell was first included in the index in 1925. Altria was added in 1985. Personally, I would get rid of Alcoa (AA) and General Motors (GM).

Here’s a look at all the changes to the Dow going back to the original rail index.

The Dow is often criticized for being unrepresentative of the market. That’s true and I prefer to the use the S&P 500 (^GSPC) which is market-weighted. Still, the Dow isn’t that bad. The index that should be ignored is the Nasdaq (^IXIC). That index is dominated by a few big names that are highly correlated to each other and little else.

Being added to the Dow isn’t much of a buy signal. Here’s what happened since AIG (AIG), Pfizer (PFE) and Verizon (VZ) were added in 2004:

Here’s what happened when Microsoft (MSFT), Intel (INTC), SBC (SBC) and Home Depot (HD) were added in 1999:

The Dow is zero for the last seven. -

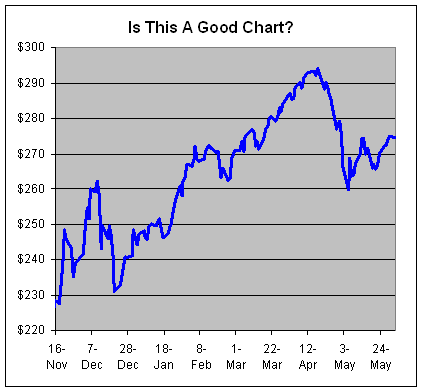

Calling All Technical Analysts

Posted by Eddy Elfenbein on February 8th, 2008 at 2:21 pmIs this a good chart?

-

Department of Strained Metaphors

Posted by Eddy Elfenbein on February 8th, 2008 at 1:26 pmThe goal of monetary is famously described as taking away the punchbowl once the party gets started. Dallas Fed president Richard Fisher explains his dissenting vote:

In the current financial-market turmoil, credit markets have been cutting back on lending to important segments of the nation’s economy. As a result, “instead of taking the punchbowl away, the Fed is now faced with the task of replenishing the punch,” Dallas Fed president Richard Fisher said Thursday.

Monetary policy acts with a lag, much like “good single malt whisky or perhaps truly great tequila,” Fisher told an audience in Mexico City.

“It takes time before you feel its full effect,” he explained.

“My dissenting vote last week was simply a difference of opinion about how far and how fast we might re-spike the monetary punchbowl,” Fisher said.Yes, but cutting 125 points in eight days is less like tequila and closer to doing lines of blow off the hooker’s ass.

-

The $72 Billion Social-Climber

Posted by Eddy Elfenbein on February 7th, 2008 at 12:30 pmIf you get a chance, I recommend Irwin M. Stelzer’s article on Jérôme Kerviel and Société Général. It’s a complex story and there’s more going on than appears. The scandal seems to have taken on a Tom Wolfe-like angle with socio-political dimensions as well.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His