-

SEI Investment’s Earnings

Posted by Eddy Elfenbein on October 18th, 2006 at 9:09 amSEI Investments (SEIC), our top performer on the Buy List this year, just reported earnings of 60 cents a share for the third quarter. This is three cents more than the Street was looking for.

Net income climbed to $60.5 million, or 60 cents per share, from $49.2 million, or 48 cents per share, in the year-ago period.

Revenue rose 54 percent to $298.1 million, including $75.1 million from the consolidation of SEI’s 43 percent stake in LSV Asset Management, versus $193.7 million last year.

Analysts polled by Thomson Financial expected profit of 57 cents per share on revenue of $289.6 million.

Operating profit in SEI’s private banking and trust business rose 21 percent to $27.9 million, while operating margin improved to 38 percent from 36 percent. Total operating profit grew 59 percent to $97.6 million, with operating margin up a percentage point to 33 percent.The stock is up 58.8% for the year.

-

Investment Don’ts

Posted by Eddy Elfenbein on October 17th, 2006 at 2:56 pm

Steve Wynn recently sold Picasso’s “Le Reve” (pictured above) for $139 million. Art can be a great investment. He bought it nine years ago for “just” $48.4 million. That’s an annualized return of 12.4%.

Unfortunately for Steve-o, he accidentally poked a hole in it:“Oh shit,” he said. “Look what I’ve done.”

The rest of us were speechless.

“Thank God it was me,” he said.

For sure.

The word “money” was mentioned by someone, or perhaps it was the word “deal.”

Wynn said: “This has nothing to do with money. The money means nothing to me. It’s that I had this painting in my care and I’ve damaged it.”Oopsie.

-

BBBY’s Back-Dating

Posted by Eddy Elfenbein on October 17th, 2006 at 1:42 pmHere’s Jack Ciesielski’s take on Bed Bath & Beyond’s back-dating probe:

Lots of other interesting stuff, though. For instance, Wall Street wonders why it takes so long to complete these investigations. One reason: Bed Bath & Beyond’s investigation covered 19,000 individual grants. The special committee’s counsel interviewed 31 officers, directors, employees, advisors and others.

Also interesting is the way the company “positioned” the occurrence of the improper transactions. There were a variety of options grants made over BBBY’s publicly-traded life: annual grants, monthly grants, and special grants. They were handled by two different compensation committees: one composed of inside directors (”Committee A”), the other composed of outside directors (”Committee B”). The most interesting conclusion about the process: “Excluding grants only to Form 4 filers beginning in 2003, almost all annual grant dates in 1998-2004 likely were selected with some hindsight.” At the same time, “the special committee found no evidence that either the Company or any person involved in the grant process had engaged in willful misconduct.” Seems contradictory: how can you select grant dates with some hindsight without willfully doing so? Only if you’re completely mistaken, probably. And that leaves open the question of negligence. (We’ll leave that to the attorneys to fight over.)As they say, read the whole thing.

-

Are Liberal Stocks Better?

Posted by Eddy Elfenbein on October 17th, 2006 at 11:14 amResearch from Blue Investment Management found that stocks with “Democratic Values” (note large D) significantly outperform the rest of the stock market. The company even offers investors a Blue Large Cap fund and a Blue Small Cap fund (blue…as in state, get it?).

Color me skeptical. First, as Jane Galt points out, back-testing can show lots of thing, or really, almost anything. I’ve carefully back-tested data and come up with the rule that you should always sell on the 29th year of each century. Hey, it’s a proven strategy.

But my greater concern is the idea that “progressive values” yield business success. Well, it could be. There are certainly lots of left-leaning businesses that I admire. The Sandlers of Golden West Financials or Peter Lewis and Progressive (check out this chart).

But my hunch is that this blue investing theory might be the wrong way around. Progressive values don’t breed success, but success may breed progressive values. To quote one well-known progressive, Willie Sutton: “That’s where the money is.” -

The Cubs Have Bought the White Sox!

Posted by Eddy Elfenbein on October 17th, 2006 at 9:50 amWell, not exactly…but the CME and CBOT are merging:

The combined company will be named CME Group Inc., and will be headquartered in Chicago (no duh). The news sent CBOT shares soaring $21.50, or 16 percent, to $156.01 in premarket trading on the INET, indicating the stock may open above its 52-week high of $140.67. CME shares rose $17.75, or 3.5 percent, to $521 in early electronic activity.

CBOT stockholders will have the right to receive 0.3006 shares of CME common stock for each CBOT share, or cash equal to the value of the exchange ratio based on a 10-day average of closing prices of CME common stock at the time of the merger.

The cash portion of the purchase price won’t exceed $3 billion. If no shareholders elect to receive cash, shareholders of CME will own 69 percent of the merged company and CBOT holders will own 31 percent, with CME issuing about 15.9 million shares valued at about $8 billion. -

SEC To Ease Margin Rules

Posted by Eddy Elfenbein on October 16th, 2006 at 10:27 pmIt’s not often that the SEC does something I like, but this one is long overdue. The SEC is likely to approve the New York Stock Exchange’s request to alter its margin rule. Under current rules, the margin requirement is the same no matter what kind of asset you hold; stocks, options or futures. This is truly unnecessary, and what’s worse is that it put us far behind bourses in other countries.

Margin has gotten a bad rap ever since John Kenneth Galbraith identified it as one of the major causes for the stock market crash in 1929. The market eventually dropped by nearly 90%, but even in those loose days, margin buying probably represented less than 10% of the market’s total value. If anything, the level of margin buying is actually negatively correlated with stock volatility.

The Federal Reserve sets the margin rules under its Reg T. The Fed used to move the margin requirement around a lot. In fact, it completely banned margin during World War II. In 1974, the Fed set the margin requirement at 50%, and it hasn’t touched it since.

I should also mention that investors who use margin should also consider how much leverage the stock itself is using. Most investors never think of this. Take a company like FactSet Research Systems (FDS). The company doesn’t have a nickel of long-term debt. I’m not advocating buying it on margin, but it’s balance sheet is something to consider.

On the other hand, we can look at General Motors (GM). According to GM’s balance sheet, the company has $11.6 billion in equity and $457.7 billion in liabilities. Yikes! That’s about $800 a share in liabilities for a $32 stock. Call me crazy but I think that’s margined well enough.

If we mathimaticate the Dow divisor, that means that $1 in share price is about eight Dow points, so GM’s liabilities are about 6400 points on the Dow.

Talk about debt relief! Forget Africa; send Bono to Detroit. -

300 Million Americans

Posted by Eddy Elfenbein on October 16th, 2006 at 10:43 amWe’re closing in on the Big Three Oh (oh, oh, oh, oh, oh, oh, oh).

Here’s the Census count.

The 300 millionth American should arrive sometime tomorrow morning. For reference, we crossed 200 million on November 20, 1967. We broke the 100 million mark in 1915.

According to estimates, we should break 400 million in 2043. -

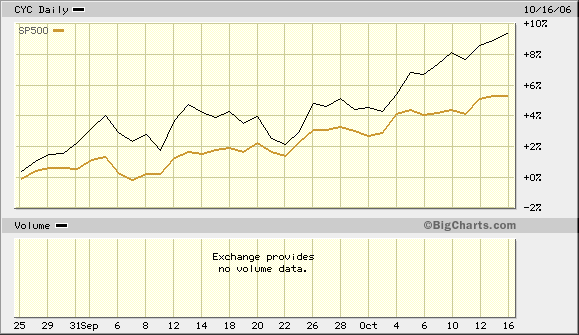

If the Economy Is In Such Rough Shape…

Posted by Eddy Elfenbein on October 16th, 2006 at 9:58 am…how come cyclical stocks are leading the bull?

Maybe the market sees something we don’t? -

Wachovia’s Earnings

Posted by Eddy Elfenbein on October 16th, 2006 at 9:23 amWachovia (WB) announced today that its earnings rose 13% to $1.06 a share. Excluding merger costs, the bank earned $1.19 a share which was in line with expectations.

The other big news of this morning is that UnitedHealth (UNH) said that Bill McGuire will step down as CEO, apparently the latest victim of the options backdating scandal. Reuters has a timeline of key events in the scandal. -

The Hitch and I

Posted by Eddy Elfenbein on October 15th, 2006 at 9:44 pmSo I was walking down Connecticut Avenue today, and I spotted a man in a bookstore who looked strangely familiar.

I went in and asked, “excuse me, sir, are you Christopher Hitchens?” The man said, coyly, “who wants to know?” I’m assuming that’s an answer generally given by correctly identified parties. Also, he had a British accent. Yep, it was Hitch. So I tried to mumble something clever about being with George Galloway’s office.

We chatted for a bit, as I did my best not to come off as Crazed Stalker Guy. Let’s face it: Even when I try to look threatening, it doesn’t come off too well. My coolness must have worked because as Hitchens was leaving the store, he asked if I was going uphill. I wasn’t but said yes anyway, and we chatted a little more.

I was I could say that we had some fancy highbrow conversation, but it wasn’t that impressive. I mentioned that I had just finished Mark Steyn’s book, America Alone. He thanked me for reminding him that he had been asked to review the book. Those Brits, they have such good manners.

It turns out that we’re both fans of Steyn. Hitchens said that he’s impressed with the amount of writing Steyn does, which I could imagine most people saying of him. Funny, I thought all these guys knew each other, but Hitchens said he doesn’t recall ever meeting Steyn, although he said that Steyn claims that they had once met.

I told him that I liked Steyn’s book, but found it a bit alarmist. He said that in the case of Islamism, alarmism is justified. Then we reached his building, said our “good days” and that was it.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His