-

Updating CAPM

Posted by Eddy Elfenbein on October 14th, 2006 at 12:23 pmWilliam F. Sharpe says that his baby, the Capital Asset Pricing Model, is due for an extreme makeover. I think we ought to pay attention. This model is the bedrock of much of modern finance.

Sharp’s new book, “Investors and Markets: Portfolio Choices, Asset Prices and Investment Advice,” argues in favor of a “state/preference” approach instead of the fancy math of his “mean-variance” method.

Pensions and Investments has the details (Hat Tip: All About Alpha). -

Play the Ultimatum Game

Posted by Eddy Elfenbein on October 14th, 2006 at 6:29 amImagine that you are sitting next to a complete stranger who has been given £10 to share between the two of you. He must choose how much to keep for himself and how much to give to you.

He can be as selfish or as generous as he likes, with one proviso: if you refuse his offer, neither of you gets any money at all. What would it take for you to turn him down?According to classical economics, people are supposed to be rational. But in the Ultimatum Game, they’re not.

Indeed, if the sum is less than £2.50, four out of five of us tell the selfish so-and-so to get lost.

Come to think of it, so would I. Why is this? Neuroeconomists say, it’s all in the brain.

-

Two Articles of Note

Posted by Eddy Elfenbein on October 13th, 2006 at 1:06 pmI saw two articles in the Wall Street Journal that I wanted to pass along. The first is from Susanne Craig who looks at how partners are selected at Goldman Sachs. This is Wall Street’s equivalent of being a “made man” in the mafia. Once you’re a PMD (partner managing directors), no one can mess with you. You’re even allowed to have three people killed. It’s one of the perks. Ok, I made that up, but still, it’s a sweet gig.

For years since Goldman’s founding in 1869, anyone who joined the firm and showed promise had a good shot of becoming partner. Until a couple of decades ago, the firm was much smaller and kept the number of partners to a minimum; in 1982 there were just 70.

The stakes for this year’s class are high. In recent quarters, Goldman has been posting impressive quarterly profits — $1.59 billion in the third quarter — and its stock is up 40% so far this year, eclipsing the 17% gain for the Dow Jones Wilshire U.S. Financial Services Index. As some other large securities firms have pushed to become global financial supermarkets, Goldman, the world’s No. 1 merger-advisory firm, has moved deeper into trading and investment banking. It has put more of its own money on the line both to trade and to invest in other companies, a move that has increased risk but beefed up profits.

Goldman’s partners have always viewed their firm as a cut above the rest of Wall Street. Mr. Blankfein, a hard-driving former gold salesman who took the top job at Goldman in June, likes to refer to an intangible secret sauce that makes Goldman smarter and savvier than its competitors. Although Goldman is known for the fat pay partners receive, Mr. Blankfein bristles at the suggestion that money-making is all that drives his partners and the firm’s selection process.

Successful partner candidates are expected to be “culture carriers,” he says. The firm encourages public service by partners, he says, and many partners have pursued that path, including former Chief Executive Officer Henry Paulson Jr., who is now Treasury Secretary. “Sure, Goldman partners make a lot,” Mr. Blankfein says. “But I can pay people a lot of money without going through this process.”The other article looks at Wachovia’s future with Golden West. As you may know, I’m rather skeptical of this merger, and I’m not a big fan of most large mergers. In December when I decide on next year’s Buy List, Wachovia will probably be gone.

First, WB paid too much. I think the Sandlers wanted a way out, and they got the right deal from Wachoiva. The Golden West business model is extremely simple, yet I’m not sure how well it will be integrated into Wachovia. I still haven’t recovered from the Fifth Third/Old Kent deal, and that was six years ago.Frustrated Wachovia officials insist the payoff from the Golden West purchase looks as promising as ever. “We go in with a little bit of a chip on our shoulder because we’ve got something to prove,” says Bob McGee, leader of the Wachovia integration team at Golden West, the second-largest U.S. savings and loan behind Washington Mutual. Wachovia also points out that this is by far the biggest deal of Mr. Thompson’s tenure, and the bigger the deal, the more investors tend to fret.

Supporters of the deal, including some institutional investors, argue Wachovia is being unfairly tarnished by comparisons with previous acquisitions that turned out to be disastrous, like the bank’s 1998 purchase of the Money Store, a lender to consumers with blemished credit histories, for $2.1 billion. The unit was shut down two years later. In contrast, Mr. Thompson has deftly handled the integrations of three major bank takeovers, most recently SouthTrust Corp., a Birmingham, Ala., bank acquired in 2004 for $13.7 billion, while improving customer service, supporters say.

“We’ve got a lot of faith in Ken Thompson and his team that they know what they’re doing. That’s why we’re sticking with the stock,” says William Hackney III, managing partner of Atlanta Capital Management, an Atlanta firm with $8.9 billion in assets under management, including about 1.2 million Wachovia shares valued at $67 million.

Softening in real estate is starting to show up in Golden West’s numbers. Through the end of August, loan originations declined 7.3% from a year earlier. While Golden West has a conservative record for underwriting loans, nonperforming assets and restructured debts rose to 0.41% of total assets from 0.28% in August 2005. -

Stock Market Report

Posted by Eddy Elfenbein on October 12th, 2006 at 1:53 pmFrom Monty Python.

-

Looking At Executive Pay

Posted by Eddy Elfenbein on October 12th, 2006 at 12:26 pm

The WSJ has a fascinating story today (sorry, but it’s a paid link) on the history of soaring executive pay:Amid the economic downturn and corporate restructurings of the early 1990s, complaints about such awards found receptive audiences. In 1992, Democratic presidential candidate Bill Clinton made executive pay a campaign issue. Washington responded.

The SEC said it would require more disclosure about compensation, particularly stock options and executive perks. The following year, after Mr. Clinton was elected, Congress decided companies could no longer take tax deductions on executive compensation of more than $1 million, unless it was related to performance.

Neither approach slowed the upward march of executive compensation. In fact, the disclosure rules allowed CEOs to see what others were getting, encouraging a competitive spiral. The tax law, meanwhile, drove up the compensation of CEOs who were making less than $1 million. Executives considered the cap a “minimum wage for CEOs,” says Mr. Koppes, the former Calpers official.

SEC Chairman Christopher Cox recently said the 1993 law belongs in “the Museum of Unintended Consequences,” because it encouraged the growth of “less transparent forms” of pay, such as pensions and deferred compensation. -

TradeSports on the Election

Posted by Eddy Elfenbein on October 12th, 2006 at 10:25 amTradesports has started a new series of contracts on how many seats the Democrats will pick up in the House this election. I’m not sure why they started these contracts just a few weeks before the election, but here are the prices as of this morning:

Democrats pick up at least:

Contract……………….Price

0.5 seats……………….95

4.5 seats……………….88

9.5 seats……………….68

14.5 seats……………..60

19.5 seats……………..41

24.5 seats……………..20

29.5 seats……………..13

We can bust out a little math and find some interesting numbers.**Inserting Pocket Protector**

If there’s a 60% chance of the Democrats getting at least 14 seats (they need 15 to get control), and a 41% chance of getting at least 19 seats, we can find the implied standard deviation.

A 60% probability works out to +0.2533 standard deviations (=normsinv(.6) in Excel), 41% comes to -0.2275 standard deviations. So those five seats are worth the difference, or 0.4809 standard deviations, and 5/0.4809 equals 10.3973 seats.

So Tradesports currently thinks the Democrats will pick up about 17.1 seats with a standard deviation of 10.4 seats.

This is pretty similar to how the VIX is calculated. -

Harley Beats By 10 Cents a Share

Posted by Eddy Elfenbein on October 12th, 2006 at 9:23 am

Harley-Davidson (HOG) had a huge quarter. The company earned $312.7 million, or $1.20 a share. Wall Street was expecting $1.10 a share. This is a 25% increase over last year’s third quarter when the company made 96 cents a share. Sales rose 14.3% to $1.64 billion.

The stock is up sharply this morning (so we’ll just ignore this). Here’s how the company has done for the past few years:Year………..Sales (mil)………EPS

1996……….$1531.2…………$0.47

1997……….$1762.5…………$0.57

1998……….$2064.0…………$0.69

1999……….$2452.9…………$0.87

2000……….$2906.4…………$1.13

2001……….$3363.4…………$1.43

2002……….$4091.0…………$1.90

2003……….$4624.3…………$2.50

2004……….$5015.2…………$3.00

2005……….$5342.2…………$3.41

2006……….$4298.1…………$2.96 (nine months) -

The Morning Blog Needs Your Help

Posted by Eddy Elfenbein on October 12th, 2006 at 12:59 am

I always love how Liz Claman begins her Morning Blog entries with, “hey bloggers.” Isn’t that just adorable? It’s so perky!

I know. I know. As much as I adore Liz, she’s committed a slight faux pas. The aforementioned bloggers are in fact, us, the readers. She’s the blogger.

Ok, so Liz isn’t hip to our new fangled techno-lingo. Big deal, right?

Apparently, The Man has put an end to it:Okay gang, Now I *really* need your help. I have been informed by THE POWERS THAT BE at CNBC.com that while they think TheMorningBlog is terrific and that you guys are terrific, they did want me to know (lower voice here:) that ‘people who read blogs, Liz, really *aren’t* called Bloggers, like you’ve been calling them.”

Oh yeah, I got the harsh word from CNBC.com Executive Producer Alex Crippen that *I’M* the blogger, not you guys. So when I write, “Hey Bloggers!” I’m totally uncool and wrong.

But then we both decided that there really isn’t an official word for people who READ Blogs, so I NEED YOUR HELP!! Do you have any ideas of what I should call you? Alex and I threw around “Blog-o-shperians”, “Blogees” or “Bleagers” (Blog + Reader? I know, lame.) But none of these sounds right. Submit Submit Submit!!! If we like one, we’ll start using it!

As always, Thank you, Blog-o-ponders. (Blog + Responder? I know. Totally LAME!)

xoxo

Liz (Ms. Blog)My first effort was to combine Claman and Media, and I got Chlamydia. I don’t think that works.

Liz, let’s just call them “readers.” -

Does the Bond Market Rule the Country?

Posted by Eddy Elfenbein on October 11th, 2006 at 10:52 pmI’m a fan of predictions markets, although I think they’re mostly just for fun. There is, however, some evidence that one of the best political markets is the bond market—specifically—short-term interest rates.

The direction of short-term interest rates has had a fairly strong correlation with the political environment of the electorate. I should warn you that this is a soft relationship, and not to read too much into it. But as short-term interest rates rise, the country generally turns to the right. Conversely, when rates fall, the country shifts to the left. Generally,

It’s not that the Federal Reserve “pushes” the country in either direction, but instead, the electorate is reacting to the same things causing the Fed to act. Few things make a country more conservative than a bout of inflation (google Weimar and Germany for more details). The value of a country’s currency is one of those weird mystical bonds that connect a citizen to the state. When that gets ruptured, people don’t like it. It’s almost like a daily referendum on the legitamacy of the state.

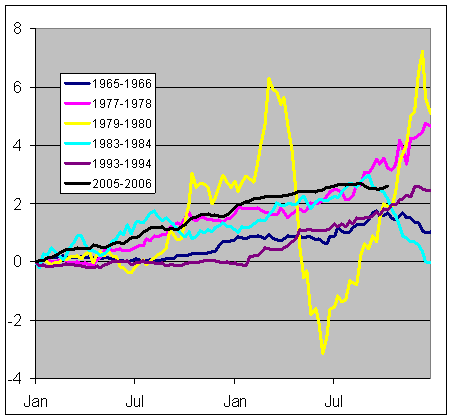

Here’s a chart showing the change in short-term interest during the last five GOP-heavy election cycles. The elections were 1966, 1978, 1980 (a particularly crazy time), 1984 and 1994. In each of these elections, voters went to the polls facing higher short-term rates. I’ve also include the current cycle.

Here’s the GOP gain in the House in each of those cycles:

1966……………………47

1978……………………15

1980……………………34

1984……………………16

1994……………………54

James Carville once said that if he could be reincarnated, he’d want to come back as the bond market: “You can intimidate everybody.” -

Bed Bath & Beyond Admits Backdating

Posted by Eddy Elfenbein on October 11th, 2006 at 9:09 amBed Bath & Beyond (BBBY) just completed a big internal probe and has found that the company practiced options backdating. The Wall Street Journal reports:

Bed Bath & Beyond said its internal probe examining the period from its 1992 initial public offering through May 2006 found that the company had misdated options on 44 occasions, 37 of them in favor of the recipients. In many cases, the probe concluded, executives used “hindsight” to select favorable grant dates in the past when the stock was trading at low points.

As a shareholder, I’m not happy with what BBBY has done, but I’m impressed with the way the company has handled this. Here’s the company’s report.

This should have no effect on the stock. The company said that it won’t restate historical results, but it will take an $8 million charge next quarter, which is about three cents a share.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His