-

The Objection of Gross’ Affection

Posted by Eddy Elfenbein on June 2nd, 2006 at 6:05 amI agree with John Carney at DealBreaker, it’s time we lay off Daniel Gross. Almost.

Gross, as you may know, promised to eat the first chapter of Dow 36,000 if Bush nominated an A-list Wall Streeter as the next Treasury Secretary. Well, you don’t get much more A-list than Hank Paulson, so we all had a good laugh at Gross’ expense.

But here’s a question: Of all the books to eat, why did Gross choose Dow 36,000? I mean, why not go for, say…Finnegan’s Wake? It still gets the point across, plus you get points for pretension. Or he didn’t even have to eat a book at all. I think a hat is more traditional. Or he could have gone with “I’ll eat Cleveland.” You really have lots of options to work with.

But there’s something about Gross and Dow 36,000. He has a rather bizarre history with this book. I’m not sure what to call it. An obsession? Gross simply MUST reference it, no matter how tangential it is to his topic. He can’t not do it. As “wine-dark” is to sea,” so Dow 36,000 is to…well, everything! Especially everything Republican.

Consider this from his Web site last year:Of course, very few of the proponents of HSAs actually have them. How many people at the American Enterprise have them? Probably the same number who think the Dow should be fairly valued at 36,000–which is to say, two.

See! The book must be mentioned, even when it doesn’t help his argument. Perhaps the idea of Republican journalists entering financial economic theory is just too much. (Hassett, of course, is a professional economist.) How come Gross doesn’t refer to Paul Krugman’s “stock bubble” call of three years ago? I’d eat that column (someone’s got to).

But no, it’s always Dow 36,000. There was this from a Slate article last December:There was a nice jobs report on Friday. The folks at CNBC are busting out the “Dow 11,000” hats again (though the “Dow 36,000” Windbreakers remain in deep storage).

Why? What does that even mean?

We can even go back in time. Here he is January 2003, attacking the Bush tax cut:Council of Economic Advisers Chairman Glenn Hubbard, the Bush administration’s one-man-economic-policy-band, apparently believes that this move will boost the market by 20 percent. “This will provide a lot of juice to the market,” said Kevin Hassett, a co-author of Dow 36,000, told the New York Times. But if they believe that this proposal will achieve such results, then I’ve got some calls on Dow 36,000 to sell them.

Well, that’s no so bad. At least Hassett is mentioned so it’s not coming out of left field. Incidentally, was that another prediction?

Here he is in the New York Times last December:In 2001, the stock market meltdown and a brief recession threw cold water on the widely held belief that the U.S. economy, juiced by a technological revolution, had entered a new era of limitless, inflation-free growth. But today, as bubble-era books like “Dow 36,000” collect dust on library shelves, evidence is mounting that there may be a New Economy after all.

Yuck. I certainly hope he doesn’t eat a dusty copy. DealBreaker has been kind enough to offer to buy a new copy for him. Gross noted that at Amazon, the book is going for four cents. But look! He’s checked the price before:

Why is Bush’s strategy stalled? I’d propose a few reasons:

1) Long Muscle Memory. It’s been five years since the market peaked. Though the S&P 500 has notched up three years in a row, Americans remain scarred by the bad end of the ’90s boom. (The mere mention of the words Dow 36,000, a copy of which is available on Amazon.com for 11 cents, can cause a room to empty.) It took nearly two generations for investors to get over the debacle of 1929. Psychological recovery from the ’90s bubble is going to take time.Gross just can’t let it go. There were two other books written at the same time as Dow 36,000. One was Dow 40,000, the other was Dow 100,000. Neither had the benefit of being written by James Glassman.

Here’s Gross again:And as we know from bitter experience (Dow 36,000, anyone?), optimism is always highest just when stocks are about to tank.

From his Web site, more parentheses:

Now, as deputy chief of staff at the White House and director at OMB, Bolten has been present in the room when every decision on fiscal policy was made–the reckless tactics, the reckless spending, the creation of the Medicare drug program, the absurd Social Security reform proposals, and so on. Brad DeLong has rightly dubbed the Bush administration fiscal policy as a “clown show.” I think it’s clear who the Bozo of the bunch. But Bolten has been putting on the red noses, frizzy wigs, and oversized shoes with the rest of them. Kevin Hassett may earnestly believe in what he says. (He also may earnestly believe that the Dow would be fairly valued at 36,000 today). But it doesn’t mean a reporter should (a) credit it; and (b) end the piece with it.

I could go on. There are more D36K mentions here and here.

Gross is one of my favorite business writers (look, he’s on my blogroll). But he clearly has an obsession. It’s madness! It’s hysteria! Wait…what was Dow 36,000 about again? -

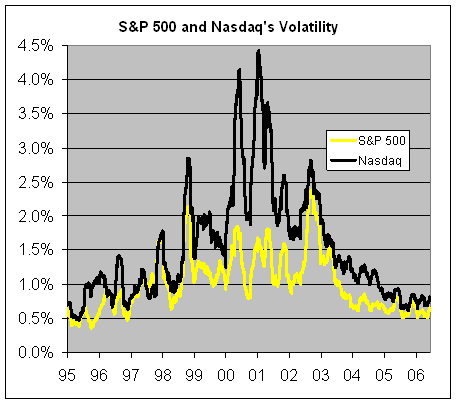

The Return of Volatility, Part III

Posted by Eddy Elfenbein on June 1st, 2006 at 3:26 pmOne of the interesting aspects of market volatility is that it’s not linear. By that, I mean that when the market becomes more volatile, the volatile stocks get REALLY volatile. When volatility fades, volatile stocks then only become slightly more volatile than the market.

Here’s a chart of the trailing 50-day average swing (standard deviation) of the S&P 500 (yellow line) and the Nasdaq (black line):

Notice how the Nasdaq used to be two and three times more volatile than the S&P 500. But today, the two are practically identical. -

UnitedHealth expects 2006 revenue of $72 billion

Posted by Eddy Elfenbein on June 1st, 2006 at 3:22 pmFrom Reuters:

UnitedHealth Group Inc. on Thursday reiterated its expected 2006 per share earnings of $2.88 to $2.92 a share with total revenue near $72 billion and operating earnings between $6.8 billion and $6.9 billion, according to a regulatory filing.

The company also said that it expects its UnitedHealthcare unit to produce 2006 revenue of about $35 billion and its Ovations unit to produce about $25 billion in 2006 revenue, according to the filing with the U.S. Securities and Exchange Commission.

UnitedHealth forecast providing 5.7 million to 6 million seniors with prescription drug benefit plans under Medicare Part D by year end, generating full-year revenue of $5.7 billion to $6 billion.

UnitedHealth shares rose $1.20, or 2.7 percent, to $45.16 in afternoon trade on the New York Stock Exchange, where health-insurer stocks broadly were trading higher. -

Crocs Shoe Company Co-Founder Arrested

Posted by Eddy Elfenbein on June 1st, 2006 at 2:43 pmFrom the AP:

A Crocs shoe company co-founder who resigned as a director last week was arrested on misdemeanor charges of threatening to slit his former brother-in-law’s throat, police said.

That’s only a misdemeanor?

George Brian Boedecker Jr., 44, was arrested May 27, a day after the confrontation in the law office of his sister’s ex-husband, David Moorhead, the Daily Camera reported in Thursday editions.

According to a police report, Moorhead said Boedecker called him and said, “I’m going to slit your throat,” then went to Moorhead’s office and tried to start a fight. Moorhead told investigators Boedecker appeared drunk, the report said. -

Reader Q&A

Posted by Eddy Elfenbein on June 1st, 2006 at 2:34 pmDear Sir:

I am a new investor and know squat about the market. I came across your site via Google and after reading through your site, I had a couple of questions. They are quite naïve I am sure. What would you recommend for a short term gain of at least 50%? Does it exist? Let’s say I have $5,000 to invest. Would you (suggest) any stocks or shares that would return double my money by the end of the year or sooner? Note that I encased “suggest”, as I know you are not here to recommend as you stated. I have called (2) brokers to date, and they really make me nervous with their tactics. Whatever info you can provide would be helpful. To be honest, I have about $20,000 I can invest, BUT that $20,000 NEEDS to be returned at least two fold under a year. I must be really making you laugh about now with my expected returns, but I have to ask. Thanks for your help sir.No, no…we would never laugh at you. But I have to be honest—you have to bring your expectations back down to earth! Holy Toledo! According to the best statistics, it’s reasonable to assume that the stock market goes up about 10% a year. It doubles, on average, every seven years. Sometimes better, sometimes worse.

I would never, EVER say a stock could double by the end of the year. It’s ahistorical, and I would be highly suspicious of anyone who made that claim.

To quote Gordon Gekko (pbuh): You’re walking around blind without a cane, pal. A fool and his money are lucky enough to get together in the first place.

Don’t be that fool!

Best regards,

Eddy -

Balchem

Posted by Eddy Elfenbein on June 1st, 2006 at 1:36 pmHere’s another unknown stock that’s made tons of money for investors, Balchem (BCP). This is from the company’s Web site:

Balchem provides state-of-the-art solutions and the finest quality products for a range of industries worldwide. The company consists primarily of three business segments: Encapsulated/Nutritional (Balchem Encapsulates) Products, ARC Specialty Products and BCP Ingredients, Inc. Balchem employs over 200 people in the United States who are engaged in many diverse activities, developing our company into chosen market leadership positions.

Our Encapsulated/Nutritional segment (Balchem Encapsulates) utilizes proprietary microencapsulation technologies in an ever-expanding variety of applications – seeking out and answering key market needs. Through microencapsulation – essentially providing a protective coating designed to “control, protect and deliver” any of a wide range of ingredients – Balchem Encapsulates enables manufacturers to speed production, overcome challenges, enhance shelf life and improve the quality or effectiveness of their end-product. Our encapsulation segment continues to identify new and innovative applications for this delivery technology and includes our Chelated products (produced by our subsidiary, Chelated Minerals Corporaiton) which provide enhanced nutrient absorbtion for many animal species.

Through ARC Specialty Products, Balchem provides packaged specialty chemicals for use in healthcare and other industries. ARC Specialty Products is the major supplier of packaged 100% Ethylene Oxide sterilant to contract sterilizers, medical device manufacturers, and others in the healthcare field. In addition to packaged 100% Ethylene Oxide, ARC Specialty Products supplies Ethylene Oxide blends, Propylene Oxide and Methyl Chloride in two-way, environmentally safe containers.

BCP Ingredients, Inc., a wholly owned subsidiary of Balchem, manufactures and supplies choline chloride, an essential nutrient for animal health, predominantly to the poultry and swine industries. Choline, part of the vitamin B complex, plays a vital role in the metabolism of fat and the building and maintaining of cell structures. Choline deficiency can result in, among other symptoms, reduced growth and perosis in chicks, and fatty liver, kidney necrosis and general poor condition in baby pigs. In addition, certain derivatives of choline chloride are also manufactured and sold into industrial applications.

Across all operations, our Company is committed to, and known for, customer service and satisfaction.Balchem isn’t even a member of the S&P 600 Small-Cap Index. The stock is currently followed by one analyst.

Here’s a 20-year stock chart against the S&P 500:

-

Joseph Weisenthal on Anya Kamenetz

Posted by Eddy Elfenbein on June 1st, 2006 at 1:26 pmBravo to Joseph Weisenthal, who skewers professional whiner and “Generation Debt” columnist Anya Kamenetz:

At the risk of of sounding like Holden Caulfield, Kamenetz is the worst kind of phony. It’s common that in wealthy societies privileged persons seek to identify with and give voice to an oppressed class. This can be a good thing when such a class actually exists. But Kamenetz goes a step further. She brilliantly created a new oppressed class and made a lucrative career out of being its spokesperson. Surely it will be a new model for similarly ambitious people for years to come.

Nah, she’ll just grow up to be Gretchen Morgenson (oooh burn).

-

The Bambi Blog

Posted by Eddy Elfenbein on June 1st, 2006 at 1:20 pmFor no reason in particular, I give you the Bambi Blog!

Watch as Bambi Francisco talks with assorted tech nerds about their nerdy start-up nerd farms. Enjoy! -

Zimbabwe Government Raids Stock Exchange

Posted by Eddy Elfenbein on May 31st, 2006 at 11:35 pmHARARE – A desperate Zimbabwe government, hard-pressed for cash, has raided the Zimbabwe Stock Exchange (ZSE) demanding Value Added Tax (VAT) on all brokerage incomes received on the bourse since 2004, a move that analysts say gives a graphic illustration of the Mugabe administration’s “policy deficiencies.”

The intelligence-led swoop on the ZSE, accused by government of failing to remit VAT for two years, was expected to raise a Z$15 trillion windfall for government.I’m selling my Zimbabwean stocks immediately.

-

The Cara 100

Posted by Eddy Elfenbein on May 31st, 2006 at 11:20 pmBlogger Bill Cara has unveiled his Cara 100. I’m happy to see that it features several stocks from our Buy List.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His