-

How Much Does Government Spending Really Change? Answer: Not Much.

Posted by Eddy Elfenbein on January 26th, 2006 at 1:16 pmEach January, the Congressional Budget Office releases its massive budget outlook report. This report details what the country is (in theory) going to spend over the next ten years.

The official release date is a big day for public policy geeks. That’s today, and the report was posted at 10 a.m this morning. The CBO’s Web site was so jammed that I couldn’t get through until a few minutes ago.

Personally, I think ten-year forecasts are a waste of time, and I ignore most of that data. What I like to look at is the historical numbers. By the way, the CBO should get major props for presenting so much data in an easy-to-read and accessible format.

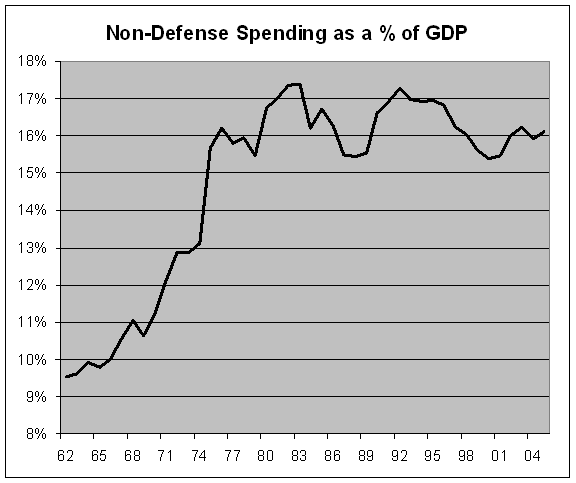

What I find fascinating is that despite all political rhetoric we hear, what the government spends each year is fairly consistent. This might upset some people who are convinced that government spending is either out-of-control, or hopelessly being slashed to the done. Sorry, but it’s just not true. The level of government spending is remarkable steady. I’m not saying that there aren’t major changes in spending patterns, but it’s far less than you might think.

Over the last thirty year, total government outlays minus defense spending as a percent of GDP, has averaged 16.31%. Quite simply, that number hasn’t fluctuated much. The high reading was 17.38% in 1983, and the low was 15.39% in 2000. As you might expect, government spending rises in recessions and falls during expansions. The standard deviation is just 0.63%.

Last year, non-defense spending rose to 16.10% from 15.93% in 2004 (this is the government’s fiscal year, which ends on September 30).

Some of you may take issue with me excluding defense spending. I understand that, so like me explain my reasoning. Defense spending can—and has—changed quite dramatically in response to real world events. Over the last 30 years, the standard deviation of defense spending is over 1%, which is higher than the budget as a whole.

I see defense spending as similar to a company declaring a one-time earnings charge. Obviously, defense spending is important and it affects our national debt, but I don’t see it as a reflection of Washington’s spending habit.

Here’s the big CBO report. You can download my data here (which is all pulled from the historical tables of the CBO report), and here’s my chart of non-defense spending as a percent of GDP. As you can see, the budget soared in the 60’s and early 70’s, but since 1976, spending hasn’t changed that much.

-

Respironics Soars

Posted by Eddy Elfenbein on January 26th, 2006 at 11:21 amIt’s a good day so far. Respironics (RESP) is soaring. The stock is currently up about 8%. Until today, it had been one of the poorer-performing stocks on our Buy List.

Danaher (DHR) is doing well. The stock is up about 2.6% today. Varian Medical Systems (VAR) is also having a strong day. The stock is up about 2.8% to a new 52-week high. The stock is up over 12% for us, year-to-date. Expeditors (EXPD) and SEI Investments (SEIC) are also looking good.

We don’t have any more earnings results this week. The next three Buy List stocks to report will be Sysco (SYY), Fiserv (FISV) and AFLAC (AFL) on Monday.

Today is the kind of market action I like to see. The energy sector is down sharply. The Energy Spyders ETF (XLE) is off 1.48%, and the Oil Service Holders ETF (OIH) is down 2.35%. The Financial Spyders ETF (XLF) is leading the market, rising 1.3%. The Consumer Staples ETF (XLP) is also doing well, currently up 0.6%.

As long as those core sectors do well, the overall market rally can last. When the market becomes so tilted towards energy and tech, I get concerned that a downturn is near.

Update: Chipotle (CMG) opened at $45. -

The Super Bowl Indicator

Posted by Eddy Elfenbein on January 26th, 2006 at 10:08 amNo matter who wins the Super Bowl, the indicator points to good news for investors.

-

GM’s Earnings Report

Posted by Eddy Elfenbein on January 26th, 2006 at 10:00 amWhat a disaster! General Motors (GM) lost a stunning $4.8 billion last quarter, or $8.45 a share. This is GM’s fifth straight quarterly loss. Bear in mind that this is a $23 stock, and they lost $8.45 a share! That loss comes to over $50 million a day. This figure includes “one-time” items which amount to $3.6 billion, or $6.36 a share. Excluding those charges, GM only lost $2.09 a share. Wall Street was expecting a loss of 12 cents a share. As lousy as Ford’s earnings were, they at least beat the Street.

President Bush said that the automakers should develop “a product that’s relevant.” Ouch. -

Danaher & Respironics

Posted by Eddy Elfenbein on January 26th, 2006 at 9:38 amThis morning, Respironics (RESP) reported earnings of 36 cents a share which was inline with Wall Street’s expectations:

Fiscal second-quarter net income was $24.1 million, or 33 cents per share, compared with $20.1 million, or 28 cents, a year ago. Net income for the current quarter included stock compensation expenses representing about 3 cents per diluted share after taxes.

Excluding items, the company reported a profit of 36 cents per share, matching the average analyst estimate, according to Reuters Estimates.

Net sales totaled $257.9 million, up 14 percent. Foreign currency exchange rates reduced revenue by about by 1 percent during the quarter.

Domestic revenue increased 15 percent to $176.9 million.

For fiscal-year 2006, Respironics forecast earnings per share, excluding equity compensation expense, in the range of $1.46 to $1.48. Earnings per share estimates for the quarter ending March 31, are expected to be 40 cents to 41 cents, excluding items.Danaher (DHR) earned 81 cents a share, which beat estimates by one penny a share:

Industrial tool maker Danaher Corp. on Thursday said fourth-quarter profit rose 20 percent, helped by stronger demand for professional instruments used in environmental science and medicine.

Earnings increased to $261.6 million, or 81 cents per share, from $217.7 million, or 67 cents per share, a year earlier.

Analysts on average expected profit of 80 cents per share, according to Reuters Estimates.

Sales also topped forecasts, rising 14 percent to $2.26 billion. Revenue rose 24 percent in Danaher’s professional instrumentation division, its biggest, to $1.17 billion.

Chief Executive Lawrence Culp said in a statement that he was confident the company would be able to deliver “excellent results in 2006,” but did not issue a specific earnings forecast.Also, Chipotle’s (CMG) IPO price was raised for the second time. The stock will now go public at $22, or 38 times earnings.

-

The Devil Wears Prada

Posted by Eddy Elfenbein on January 25th, 2006 at 5:50 pmWhen Ben Bernanke steps into Alan Greenspan’s shoes at the Federal Reserve on Feb. 1, he’ll be under pressure to prove he’ll be vigilant on inflation, several Wall Street economists say.

In two weeks, Ben Bernanke will try to fill the shoes of the venerable Alan Greenspan as Federal Reserve chairman and begin to shape policy for the largest free market economy in the world.

Academician has big shoes to fill as Fed Reserve head

Big shoes to fill

Following the legend of Greenspan, Bernanke certainly has big shoes to fill.

One focus is the transition at the Federal Reserve Board, where Alan Greenspan is on his way out as chairman and Ben Bernanke is stepping into those extra-large shoes.

Big Shoes to Fill

It will not be easy for Bernanke, who is tasked with overcoming domestic and external problems that could short-circuit the currently sound U.S. economy and to fill the big shoes of Greenspan, who has won international recognition for his economic policies.

NPR:

In terms of his role as a political player, analysts agree he has some big shoes to fill.

Bernanke knows he has big shoes to fill.

You’d think Alan Greenspan shows up to work in a clown costume with all the talk about the next Federal Reserve chairman having big shoes to fill.

Greenspan, Entourage Demolish Hotel Room

-

Fair Isaac Earns 52 Cents a Share

Posted by Eddy Elfenbein on January 25th, 2006 at 5:23 pmFair Isaac (FIC) just reported earnings of 52 cents a share. I was wrong on sales growth. Revenues came in at $202.8 million, growth of just 3.7%. The good news was net margins, which held up at 17%. With the addition of stock options, the company earned 43 cents a share. Overall, this looks very good. I’ll have to dig into the numbers a little bit more to see all the messy details.

The company also guided inline for next quarter (52 cents a share) and next year ($2.16 a share). I have to say that I’m very pleased with these results.

Varian Medical Systems (VAR) beat by a penny a share (34 cents versus 33 cents). The stock tends to be much more volatile, so it could react negatively.

Also, Bed Bath & Beyond (BBBY) announced a $200 million increase to its share buyback program. The old program was for $400 million.

Still more earnings to come. Tomorrow we’re going to get results from Danaher (DHR) and Respironics (RESP). Wall Street is expecting 36 cents a share from Respironics, and 80 cents from Danaher. -

Medicare Drug Benefit Sparks an Industry Land Grab

Posted by Eddy Elfenbein on January 25th, 2006 at 12:49 pm

The WSJ has a fascinating article today on the business impact of the new Medicare prescription drug benefit. Our own UnitedHealth (UNH) is one of the major beneficiaries:Defying early predictions that private insurers wouldn’t offer prescription-drug policies, dozens of companies are offering regional plans and 10 are selling them nationwide. The government is heavily subsidizing the policies, for which 42 million people are eligible. It’s a big and unexpected growth opportunity at a time when the industry’s traditional business — administering employer health benefits — is stagnant or shrinking.

UnitedHealth, based in Minnetonka, Minn., is one of the most aggressive players and one of the most successful so far. It has signed up about 2.8 million Medicare beneficiaries, either to stand-alone drug plans or within its more comprehensive Medicare plans. It picked up 1.5 million more sign-ups from its acquisition in December of PacifiCare Health Systems. -

Boston Scientific Wins

Posted by Eddy Elfenbein on January 25th, 2006 at 10:38 amThis time, it looks like it’s finally over. Guidant’s (GDT) board has accepted Boston Scientific’s (BSX) higher bid. BSX will pay $42 a share in cash, and $38 a share in stock. In my opinion, that’s way too much.

For its part, J&J will get $705 million for Guidant breaking its earlier agreement. BSX smartly stayed a step ahead of regulators by agreeing to sell part of Guidant to Abbott Labs (ABT).

This was a big victory for a couple of hedge funds and lots of lawyers and investment bankers. J&J nearly made a big mistake.

Speaking of bidding war, one of our Buy List stock, Danaher (DHR), will bow out of a bidding war for First Technology. Honeywell (HON) initially agreed to buy the company for 275 pence, then DHR bid 330. Honeywell came back and bid 365, which it’s going to get.

Disney (DIS) agreed to buy Pixar (PIXR) for $7.4 billion. Or more accurately, Pixar agreed to be bought by Disney. Steve Jobs will be the new chairman. Disney is too good a company for its current management. -

Profits Plunge at the New York Times

Posted by Eddy Elfenbein on January 24th, 2006 at 2:49 pmEarnings dropped 11% for the year and 45% for the quarter:

Circulation revenue remained under pressure, though the company, which owns The New York Times, The Boston Globe, The International Herald Tribune and other newspapers, as well as television and radio stations, reported a 6.2 percent increase in advertising sales for the quarter. But the company said revenue for January was “off to a slower start, especially in the entertainment and classified automotive categories.”

Newspaper companies, like other media companies, are in the midst of a struggle to adapt themselves to the new ways in which readers and viewers consume news and entertainment on the Internet and digital devices. While advertising rates and revenue are increasing online – the Times Company said advertising revenue at its newspaper Web sites jumped 30.3 percent – that growth has not completely made up for the decline in revenue and profits from newspapers and other older media.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His