-

Earnings Preview for Fair Isaac

Posted by Eddy Elfenbein on January 24th, 2006 at 2:36 pmFair Isaac (FIC) will report its earnings after the close tomorrow. If you’ve read this blog for awhile, you know that I’m a big fan of this company. They’re known for the FICO credit score, and they’re the dominant player in the industry.

Last year, Fair Isaac reported that its first-quarter (ending in December) sales jumped 15%, but its earnings were only 36 cents a share, the same as the year before. But the next three quarters were very strong. Fair Isaac beat estimates by six, then nine, then four cents a share. I think they’ll beat estimates again.

The current estimate is for 50 cents a share. If revenues come in at $210 million, which is just 7.4% sales growth, and net margins fall to 17% (the average has been about 17.5%-18%), then Fair Isaac will earn $35.7 million for the quarter. That would be about 55 cents a share.

I think I’m being cautious on the net margin number, but perhaps a little aggressive for sales growth. Sales growth is the hardest to pin down. Don’t think that Fair Isaac is heavily tied to mortgage lending. For example, when you get those “pre-approved” credit cards in the mail, have you ever wondered how they know you’re a good risk? Odds are Fair Isaac told them.

For the year, Wall Street expects Fair Isaac to earn $2.16 a share, and $2.46 a share next year. Here are the financial results from the past few years: -

Golden West Financial Beats Earnings

Posted by Eddy Elfenbein on January 24th, 2006 at 11:31 amThis is why I like dull stocks. Sure, Golden West Financial (GDW) is boring, but it never lets me down. While everyone else is reporting slower mortgage business, GDW keeps motoring along. Today the S&L reported better-than-expected earnings. For the fourth quarter, the company earned $1.37 a share, three cents more than estimates. The shares are up about 40 cents today.

Two more of our dull stocks report tomorrow, Varian Medical (VAR) and Fair Isaac (FIC). The estimate for Varian is for 33 cents a share. How’s this for consensus? All eight analysts who follow Fair Isaac estimate earnings of 50 cents a share. Our health care stocks got clobbered yesterday, but Varian is gaining back much of what it lost.

Earnings season is Judgment Day on Wall Street. Intel (INTC) has dropped for seven straight days. It looks like it may break that streak today. The company missed by three cents a share and fell 11% last Wednesday on 280 million shares. I really underestimated how much Advanced Micro (AMD) has cut into Intel’s business. Michael Sivy has a good analysis of Intel’s problems.

One stock that almost never fails during earnings time is Coach (COH). The company beat earnings by three cents a share, and the stock is up about 7% today.

Johnson & Johnson (JNJ) reported very good earnings today. Profits were up 79%. This reminds me of why I don’t want JNJ to win the war for Guidant (GDT). Guidant’s board has until tomorrow to accept Boston Scientific’s (BSX) higher offer. For the first time in 22 years, Johnson & Johnson reported that its revenue dropped. -

IPO for Chipotle Mexican Grill

Posted by Eddy Elfenbein on January 23rd, 2006 at 2:30 pmI have to confess that I’m a Chipotle’s addict. If you’re not familiar with the restaurant, they’re crack dealers. But instead of crack, burritos.

But they’re not ordinary burritos. They’re huge. They’re like… Nietzschean overburritos.

Sometime this week, Chipotle’s will IPO. Demand is stong. The company just raised its price range from $15.50 to $17.50 a share to $18 to $20 a share.

The symbol is CMG. -

The Hottest Market in the World

Posted by Eddy Elfenbein on January 23rd, 2006 at 2:06 pmA few months ago, I wrote about the hottest stock market in the world. It’s in Brazil, and things haven’t slowed down. The Brazil iShares (EWZ) are up about 500% in the last three years. (Chart.)

Brazil seems to be in the sweet spot of the global economy. Speaking of sweet spot, the price of sugar has doubled in the past year which helps Brazil, the world’s largest sugar producer. The reason for the rally is that more sugar is being converted to ethanol to cope with record gasoline prices.

There was some fear that the Brazilian economy might be slowing down. In response, the Brazilian Fed just cut interest rates by 0.75% to 17.25%, which helped spur the stock market.

There’s a presidential election coming up and “Lula” looked like he was on his way out, but he’s recovered in the polls. The financial situation has improved dramatically in Brazil. The government recently said that it has enough cash-on-hand to go four months without a debt offering. I would have thought someone was joking if I had heard that five years ago.

Some major Brazilian stocks include:

Petroleo Brasileiro (PBR)

Companhia Vale do Rio Doce (RIO)

Banco Itau Holding Financeira (ITU)

Banco Bradesco (BBD)

Companhia de Bebidas Das Americas (ABV)

Telecomunicacoes de Sao Paulo (TSP)

Gerdau (GGB)

Companhia Energetica de Minas Gerais (CIG) -

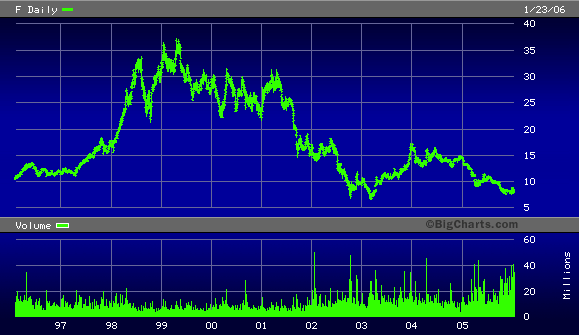

Black Monday

Posted by Eddy Elfenbein on January 23rd, 2006 at 11:46 amThe official announcement came. Ford said that by 2012, it will cut as many as 30,000 jobs and shut down 14 plants. The plan is expected to save $6 billion a year by 2010.

The company reported earnings of eight cents a share, two cents more than last year. For the year, Ford made $1.04 a share, down from $1.73 a share in 2004. The stock is currently trading about 8% higher.

The real number to watch at Ford is the pre-tax loss for North American operations. For the second quarter, Ford loss $907 million, and then another $1.2 billion in the third quarter. Today, Ford said that it only lost $143 million in the fourth quarter.

Excluding all the one-time charges, Ford made 26 cents a share for the quarter while Wall Street was expecting just a penny a share. The stock is currently trading about 8% higher. Bloomberg lays out some of the details Ford faces:Employees

Ford had 122,877 employees in its North American auto operations at the end of 2004, including 35,000 salaried employees. Detroit-based GM, Ford’s bigger U.S. rival, had 173,000 U.S. employees in North America at the end of September 2005, down from 181,000 at the end of 2004. GM had 106,000 hourly and 36,000 salaried U.S. employees at the end of September.

“If Toyota and Honda weren’t in the market, Ford and GM would be in fine shape,” said Sean Egan, managing director of Egan-Jones Ratings Co. in Haverford, Pennsylvania, said today before the restructuring announcement. “We don’t see anything on the horizon that is going to substantially change the slide.”

The plan is Bill Ford’s second restructuring since becoming CEO in 2001. Toyota passed Ford, which sold 6.8 million cars and trucks worldwide last year, as the world’s No. 2 automaker in 2003. Toyota has said it expects to report 2005 sales of 8.09 million cars and trucks. Wagoner said earlier this month GM sold 9.17 million cars and trucks worldwide last year.

Overcapacity

Ford in 2005 had the capacity to build 4 million vehicles annually in North America at 16 assembly plants. Last year, the company sold 2.95 million of its North American-built Ford, Lincoln and Mercury models in the U.S.

Ford’s U.S. sales overall fell 5 percent in 2005 compared with an industrywide gain of 0.5 percent. The company was hurt by a decline in sales of profitable sport-utility vehicles. The Explorer mid-size SUV hit a 15-year sales low in November and fell 29 percent for 2005.

The company’s North American car and truck plants operated at 79 percent of capacity in 2005, according to Harbour Consulting of Troy, Michigan. That was the lowest of six automakers surveyed by the consulting company. Toyota was No. 1, with its North American plants operating at 111 percent of capacity. -

The Way Forward

Posted by Eddy Elfenbein on January 23rd, 2006 at 6:03 amGood morning. Today is Black Monday—the day that Ford Motor (F) will announce its major restructuring plan.

I know you might be a little confused and thinking, “wait, aren’t they already in a restructuring plan?” Apparently not. Or rather, we may be in a new restructuring plan. I’m having trouble keep their bold initiatives apart. Perhaps the old turnaround plan is itself being turned around. It’s hard to say. Honestly, I think everyone’s lost track.

Personally I’m rooting for “bold leadership in an ever-changing world.” When you’re dealing with these announcements, bold’s like a blue blazer, it never goes out of style. The good news is that the plan already has a name—“The Way Forward” which unfortunately sounds like a plan for the East German economy circa 1971. Forward Comrades! But given Ford’s history, this too might be an improvement.

According to reports, The Way Forward (or TWAF) will reposition Ford as “America’s Car Company”—“Red, White and Bold” and “Bold, American and Innovative.” So we got “bold” in there twice along with “innovative.” That’s a double word score for your thematic marketing efforts. Of course, the problem will leadership by sloganeering is that is tells us more about Ford’s fears than it plans. I would call Bill Ford many things, innovative is not one.

I’ll make this very simple. Ford is a company that’s designed to make X number of vehicles per year. The public wants half-X. Therein lies our problem. There are many thousands of employees who need to be…well, x-ed out. I suppose restructuring is being a bit generous. The Ottoman Empire was restructured. But Ford? They’re screwed.

I’ll give you an example. Ford makes the Explorer. It really not that bad (by Ford’s standards), but sales have plunged. Ford used to make two assembly plants worth of Explorers. They don’t need that anymore. In the immediate future, Ford is actually in slightly worse shape than General Motors (GM). As hard as that is to imagine, GM at least has some new models coming out this year. Ford is empty. Also, their newer cars, like the Fusion, aren’t selling well. Truthfully, they haven’t been marketed well.

(By the way. Fusion? Good god, who named this? Rule #1: Car names should rock. Think Mustang. Don’t think 37-minute jazz improvisations. Fusion??)

It’s astounding how quickly Ford has sunk. The New York Times recently said: “Just five years ago, the talk in Detroit was about whether Ford could eventually outsell G.M. Now the talk is about which of these two companies is worse off.” Make no mistake, GM is in far worse shape.

Ford’s problems started a few years ago when the company went Google for trucks and SUVs. So the public stopped thinking of them as a car company. Now Americans turn to Accords and Camrys for that. In the past year, gas prices went up and Ford’s stock collapsed. The company’s market share is now down to 17.4%, and it’s still dropping.

In May, the company’s credit rating was downgraded to junk. Then recently, it was cut to even lower junk. Ford has basically been blackballed from the bond market. The company’s bonds were even evicted from the Lehman Brothers Bond Index.

Incidentally, Ford is the King of Extra-Long-Term Debt. They have non-callable bonds set to come due in 2043 (12% YTM), 2047 (12.3% YTM) and 2097 (11.5% YTM). I wonder how many restructuring plans Ford will have over the next 91 years.

When Bill Ford took over, his plan was to have the company make $7 billion in 2006. That’s not going to happen. It appears that Ford will shut down 10 assembly plants and cut around 25,000 jobs. Maybe 30,000. That’s a start. I’m afraid this is a year too late. Plus, Bill Ford always seems to move in half-steps when truly bold moves are needed. I should add that there’s some big double top-secret project that we’re going to learn about. Something about a recyclable, environmentally-friendly car. Yawn.

As I said, Ford isn’t in as much trouble as GM. At least Ford is making a profit, largely due to its finance arm. I hope to see Ford sell off some divisions. They already ditched Hertz.

What does the future hold? Who knows? I think Ford will exist in some form, but it won’t be a major automaker. Perhaps it will be closer to what AT&T is today. As Ford stands now, it’s trapped. The company is under attack from all sides. Any successful plan for the future isn’t The Way Forward, it’s The Way Out.

-

The Great Crash of 1906

Posted by Eddy Elfenbein on January 22nd, 2006 at 1:38 pmWe recently celebrated the 100th anniversary of the start of the longest bear market in history.

What’s that, you say never heard of the Crash of ‘06?

On January 19, 1906, the Dow peaked at 103. That date may not ring throughout the annals of history, but it was pretty important for the stock market.

The stock market soon crashed and by 1907, the Dow bottomed out at 53. Now that’s a bear market! None of this wussy 1.8% nonsense.

The Dow eventually recovered, but the January 19, 1906 high haunted the market for years to come. Even by 1914, the index was still in the 80’s when the exchange was shut down due to troubles “over there.” Soon traders started doing business on the street, so the NYSE opened again that winter. And once again, the Dow plunged 53.

Nevertheless, the Great War was good business, and the Dow finally hit a new record of 103.11 on September 28, 1916. The Dow nearly got to 120 in 1919, but there were still some nasty corrections. The Dow fell below 70 in 1917 and again 1921.

By 1923, the market took off. The Dow broke 100 in 1924. In early 1928, it hit 200, and a year later it smashed through 300. Over the summer, the Dow peaked at 380.

Three years later, it was at 42.

After Pearl Harbor, there was another slow sell-off. On April 28, 1942, the Dow finally bottomed out at 92.92.

Wanna read something scary? This is from FDR’s fireside chat that day:Yesterday I submitted to the Congress of the United States a seven-point program, a program of general principles which taken together could be called the national economic policy for attaining the great objective of keeping the cost of living down. I repeat them now to you in substance:

(1.) First. We must, through heavier taxes, keep personal and corporate profits at a low reasonable rate.

(2.) Second. We must fix ceilings on prices and rents.

(3.) Third. We must stabilize wages.

(4.) Fourth. We must stabilize farm prices.

(5.) Fifth. We must put more billions into War Bonds.

(6.) Sixth. We must ration all essential commodities, which are scarce.

(7.) Seventh. We must discourage installment buying, and encourage paying off debts and mortgages.Whoa! I can’t imagine any politician talking like that today.

The market started to rise. July 2, 1942 was the last time the Dow closed below 103—an astounding 36-1/2 years after it first hit that level.

For comparison, 36-1/2 years ago was the time of Woodstock and the Moon landing. Today’s Dow is over 12 times higher than it was back then. That’s a good fact to keep that in mind the next time you hear someone complain. -

Google Earth

Posted by Eddy Elfenbein on January 21st, 2006 at 7:48 pmis the greatest invention in the history of the world…or at least the most addictive (download).

A few things I’ve noticed:

21° 21′ 53″ N 157° 57′ 00″ W

The USS Arizona

You can see the whole ship underwater. You can even see the oil slick coming from the boat. I used the “Measure” function under “Tools.” It’s 590 feet long. I think that’s the “Lady Mo” to the southwest.

34° 04′ 24″ N 118° 14′ 25″ W

Chavez Ravine.

I measured 395 feet to straightaway.

41° 53′ 25″ N 12° 29′ 31″ E

The Colosseum

The Vatican is two miles to the northwest.

44° 35′ 24″ N 104° 42′ 55″ W

Dah Doo Di Dah Doo

37° 48′ 51″ N 122° 28′ 42″ W

The Golden Gate Bridge. Wow! Just amazing.

Alcatraz is the little island three miles due east. Hey, it’s only a 4,765-foot swim to the pier. But I’m guessing the water might be a little cold.

46° 12’00” N 122° 11′ 00″ W

Mount St. Helens

Extra cool. Click the “terrain” box, then “tilt” down a little, and slowly scan over the volcano from the north at about 12,000 feet. (Optional: Make airplanes noises).

40° 42’26” N 74° 00’33” W

40 Wall Street. Sorry Donald, but I will never call this the Trump Building. Ever. Forty Wall was designed to be the tallest building in the world, and it was for a time, until Walter Chrysler unveiled his top secret spire on his building (3.6 miles to the northeast).

Let me know if you find any cool places.

P.S. Quick, a parking space! (40° 42′ 27.18″ N 74° 00′ 28.46″ W) -

More Firms Are Refusing to Provide Earnings Guidance

Posted by Eddy Elfenbein on January 21st, 2006 at 4:29 pmSince the tech bubble burst nearly six years, regulators have declared war on research analysts. There was the global research settlement, plus new guidelines like Regulation FD.

When it comes to criticizing the Street, I take a back seat to no one. However, we’re now starting to see some unintended consequences of the anti-analyst movement. Perhaps the most troubling is that more and more companies are refusing to provide any earnings guidance whatsoever.

This week, Motorola (MOT) become the latest stock to say that it will no longer tell the public where it sees its earnings headed. Intel (INTC) said that it will no longer provide its mid-quarter sales updates. Today, only 71% of the publicly traded stocks give earnings guidance, which is down from 77% three years ago.

I really can’t blame these companies. The legal atmosphere has become toxic, and any misstep could result in legal action. As usual, an attempt for more transparency has resulted in less.

Hopefully, this will help more independent analysts, like stock bloggers, and any individual investor willing to do a little homework. There are lots of great stocks out there that almost no one knows about.

A few weeks ago, I mentioned a great little bank Northern Empire Bancshares (NREB). The company just report terrific earnings. For 2005, EPS came in at $1.59 compared with $1.23 for 2004. Not many banks are growing like that, yet not one single analyst follows the stock. There’s no guidance, no consensus, no upgrades or downgrades, just year after year of outstanding results.

Perhaps the lack of guidance isn’t as troubling as I think. The great stocks are still out there, but we may have to work a little harder to find them. -

What if They Held an Olympics

Posted by Eddy Elfenbein on January 21st, 2006 at 3:56 pmand nobody came?

Forty percent of the tickets to Turin(o) are unsold.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His