-

CWS Market Review – May 31, 2019

Posted by Eddy Elfenbein on May 31st, 2019 at 7:08 am“Intelligent investment is more a matter of mental approach than it is of technique.”

– Ben GrahamThere’s an old Wall Street adage: “sell in May and go away.” Indeed, the historical data shows that the best six-month stretch for investors has been from November to May while the worst has been from May to November.

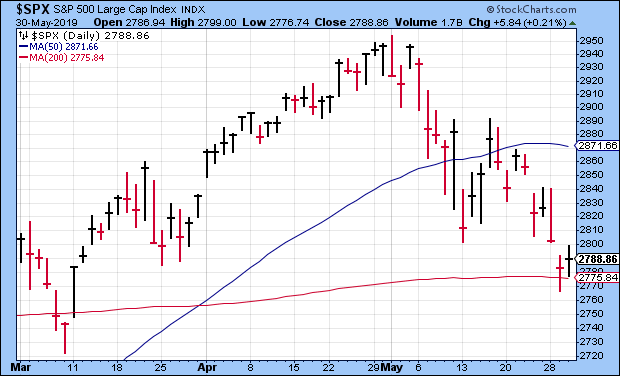

This year, that advice was exactly right. The S&P 500 had its all-time highest close on the final day of April when the index closed at 2,945.83. The following day, the index reached its intra-day high of 2,954.13.

Since then, the market has gradually drifted lower. On Wednesday, the S&P 500 closed at its lowest level since March 8. The same day, the Dow slipped below 25,000 for the first time in 16 weeks. The S&P 500 is now below its 50-day moving average, and this week it briefly fell below its 200-day moving average.

So what has everyone so nervous? The tipping point was President Trump’s tweet from May 5 which escalated the Great Trade War of 2019. What’s interesting about this latest downturn is that it was foreshadowed by the bond market. Not only has the bond market rallied (a lot) but it’s also become inverted, though only partially.

Confused? Fear not. In this week’s CWS Market Review, I’ll explain what it all means. I’ll also take a look at our two recent Buy List earnings reports, Hormel Foods and Ross Stores. Later on, I’ll preview next week’s earnings report from JM Smucker. But first, let’s look at what has Wall Street on edge.

The Yield Curve Gets Inverted…But Only a Little

While the stock market has been weak lately, the bond market has been quite strong. Since November 8, the 10-year yield is down more than 1% (3.24% to 2.22%.) That’s a huge move. We’re in an unusual position right now because the current Treasury yield curve is inverted, but only partially. Treasury yields gradually decrease from one month out until three years out. After that, yields rise again. It almost looks like a check mark.

What explains a check mark curve? Perhaps the market expects one or two therapeutic rates within a broader tightening cycle. The futures market thinks there’s a 65% chance that the Fed will cut by the September meeting. It could happen, but I’m a doubter. Going by the Fed’s statements, they seem to like things as they are. For a rate cut to be on the table, I would expect to see decidedly worse economic news (and worse financial markets). We’re just not seeing it.

The Fed meets again in mid-June. It’s also a meeting where they’ll update their economic forecasts. Personally, I think that meeting will be a big snoozer. The Fed doesn’t like the perception, not unfairly held, that they’re Wall Street’s lackey. It took a pretty big market hissy fit last year just to get the Fed to back off on planned rate hikes. Actual rate cuts are quite another thing.

The Fed also doesn’t want to be seen as bailing out a president in a trade spat they most certainly oppose. The latest is that President Trump is hitting Mexico with a 5% tariff. There is, however, a possible finale to all the trade rhetoric. In June, there’s a big G20 meeting, and it’s possible that President Trump will announce a trade deal with President Xi Jinping of China.

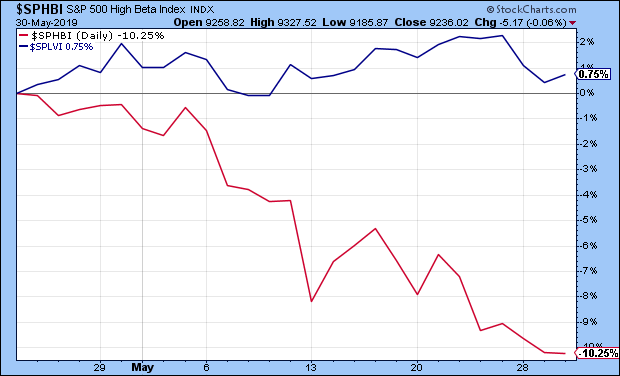

The trade talk and bond-market rally has had an interesting impact on the stock market outside of simply going down. Over the past few weeks, a wide gap has opened between “high beta” stocks and those with low volatility. The more volatile stocks have been dropping the most, while the low volatility sector has been holding steady. Over the last few weeks, the high beta sector is down 10.25% while the low vol sector is higher by 0.75%.

When the stock and bond markets act like this, it means that investors are shunning risk and seeking safety. The 30-year Treasury is now near its lowest point since Election Day in 2016. Within the stock market, sectors like tech, energy and industrials have been lagging. On the other hand, defensive areas have been doing well.

Since our Buy List is concentrated in high-quality stocks, we’ve been doing very well lately, in a relative sense. Or more precisely, we’re flat while everyone else is dropping. For the year so far, our Buy List is up 14.94% to the S&P 500’s 11.25%. But you can really see the divergence in the last month. Since April 22, the S&P 500 is down 4.10% while our Buy List is actually higher by 0.17%. That’s an unusually big gap for such a short time period. This is exactly why we own high-quality stocks. Now let’s take a look at two recent earnings reports from our Buy List.

Earnings from Hormel Foods and Ross Stores

We had two Buy List earnings reports last week. These were for companies that had quarters ending at the end of April. Let’s start with Hormel Foods (HRL). On Thursday, May 23, the Spam company reported fiscal-Q2 earnings of 46 cents per share. That beat expectations by one penny per share.

Despite the earnings beat, Hormel lowered its fiscal 2019 outlook. They now see sales of $9.5 billion to $10 billion. The previous guidance was $9.7 billion to $10.2 billion. They also lowered their EPS guidance to $1.71 to $1.85. The previous range was $1.77 to $1.91 per share.

Jim Snee, Hormel’s CEO, said that despite record sales, Q2 did not meet their expectations: “African swine fever in China started to impact global hog and pork markets this quarter, which led to rapidly increasing input costs. In response, we have announced pricing action across our branded value-added portfolio in the Grocery Products, Refrigerated Foods and International segments.”

Snee said that the lower guidance “is based on the input cost increases experienced in the second quarter and a forecast for volatile domestic pork prices in the second half of fiscal 2019.”

On Thursday, shares of Hormel gapped down at the open. At one point, HRL was off by 6.3%. After that, HRL rallied back, and it closed yesterday not far from where it was before the earnings. It’s as if the market thought it over and changed its mind.

Hormel’s outlook is troubling, but I’m still confident the company can manage its way through short-term issues. As a precaution, this week, I’m lowering my Buy Below on Hormel Foods to $42 per share.

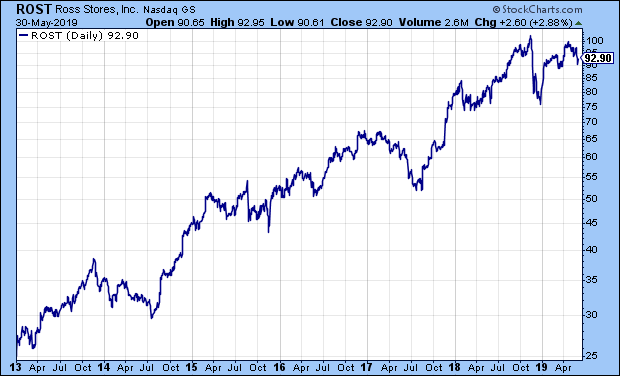

Also on Thursday, Ross Stores (ROST) released its fiscal-Q1 earnings report. For the February/March/April period, Ross made $1.15 per share. Previously, the deep-discounter had given us an earnings range of $1.05 to $1.11 per share. As usual, their guidance was conservative. Comparable-store sales were up 2%.

Barbara Rentler, Chief Executive Officer, commented, “For the first quarter, we delivered sales gains at the high end of our guidance as well as better-than-expected earnings-per-share growth despite continued underperformance in Ladies’ apparel. While operating margin of 14.1% was down from the prior year, it was above plan mainly due to higher merchandise margin. As expected, this improvement was more than offset by increases in freight and wage costs and the timing of packaway-related expenses that benefited the prior-year period.”

For Q2, Ross sees comparable-store sales growth of 1% to 2%. For EPS, the company sees the exact same as Q1, $1.05 to $1.11 per share. Wall Street had been expecting $1.14 per share.

The company also updated its full-year guidance. Ross now sees earnings of $4.38 to $4.52 per share. That includes seven cents per share thanks to a favorable tax benefit. The previous range was $4.30 to $4.52 per share. Adjusting for that, in effect, ROST’s guidance range narrowed thanks to a one-cent increase at the low end and a five-cent decrease at the high end.

The shares pulled back after the earnings report, but it was nothing too serious. At one point on Wednesday, ROST dipped below $90 per share. I’m still a fan. Ross Stores is a buy up to $95 per share.

Earnings from Smucker on June 6

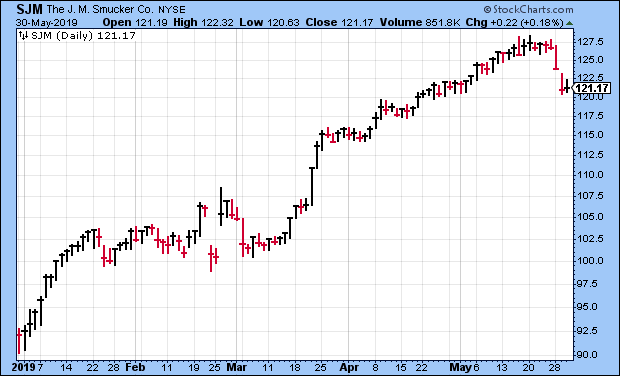

At the start of the year, I would not have guessed that JM Smucker (SJM) would be a 30% winner for us by May, but here we are. Of course, one of the best parts of our strategy is that we don’t have to make such guesses. We buy and we wait. The jelly people are due to report their fiscal-Q4 earnings next Thursday, June 6.

For their fiscal Q3, Smucker earned $2.26 per share, which nicely beat Wall Street’s estimate of $2.02 per share. Sales rose 6% to just over $2 billion. Most importantly, the company stood by its full-year forecast.

For the entire fiscal year, Smucker expects sales of $7.9 billion and earnings of $8.00 to $8.20 per share. They’ve already made $6.20 per share for the first three quarters, so that translates to a Q4 range of $1.80 to $2.00 per share. Wall Street expects $1.95 per share.

Smucker also said that results for FY 2020, which began on May 1, will be above Wall Street’s expectations. At the time, Wall Street had been expecting 2020 earnings of $8.22 per share. That consensus is now up to $8.33 per share. The current share price is about 14.5 times that, so the stock is reasonably valued.

Remember that Smucker is a lot more than jelly. Their divisions are coffee, retail consumer foods, retail pet foods and international. The stock actually got dinged on Tuesday and Wednesday of this week. Look for a solid earnings report.

After the Smucker report, we enter a dry patch for Buy List earnings. There’s not much until the Q2 earnings season heats up in mid-July. We have two Buy List stocks with quarters that ended in May. FactSet (FDS) will report its earnings on June 25. The other is RPM International (RPM), but they won’t report until mid-to-late July. Companies are allowed extra time with their fiscal Q4 report.

Speaking of FactSet, last week the company raised its dividend by 12.5%. The payout will rise from 64 cents to 72 cents per share. This is the 14th annual dividend increase in a row. The cash dividend will be paid on June 18 to holders of record at the close of business on May 31.

Before I go, I wanted to mention Check Point Software (CHKP). This is a very good company, but the shares have been knocked around lately. In April, CHKP beat earnings by a penny, but traders got spooked by poor guidance. In my opinion, that guidance wasn’t that bad. The day of the earnings report, the shares dropped 7.4%. What’s surprised me is that CHKP has fallen another 6.2% on top of that. Look for a bounce. I’m lowering my Buy Below on Check Point to $120 per share.

That’s all for now. Next week is the first week of June, and with that, we’ll get several of the key turn-of-the-month economic reports. The ISM Manufacturing report comes out on Monday. This is often a good gauge of the factory sector. ADP will release its payroll report on Wednesday. Then on Thursday, the jobless-claims report is due out. This all leads up to the big jobs report next Friday. That last report showed the lowest unemployment rate in five decades. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: May 31, 2019

Posted by Eddy Elfenbein on May 31st, 2019 at 7:04 amChina Threatens Sweeping Blacklist of Firms After Huawei Ban

Trump to Impose Tariff of Up to 25% on Mexico Over Migrants

Fed May Consider Lower Rates if Inflation and Global Risks Worsen

Trade War Starts Changing Manufacturers in Hard-to-Reverse Ways

How Tariff Hikes are Squeezing the U.S. Furniture Business

Falling Mortgage Rates Are Enticing U.S. Homebuyers to Trade Up

Uber Will Reduce Promotions After Losing $1 Billion in a Quarter

Amazon Interested in Buying Boost from T-Mobile, Sprint

Gap Brand, Old Navy Post Weakest Sales in Three Years

LaCroix Faces a Crippling ‘Free Fall’ as It Turns ‘From Bad, to Worse, to Disastrous,’

A 600-Page Textbook About Modern Monetary Theory Has Sold Out

Howard Lindzon: The Death of Retail Is The Birth of Retail…Part 2

Jeff Carter: Skimping on Legal

Ben Carlson: The Podcast Power Law & Credit Card Benefits You Never Knew About

Be sure to follow me on Twitter.

-

Morning News: May 30, 2019

Posted by Eddy Elfenbein on May 30th, 2019 at 7:04 amYes, India’s Economy Is Growing, but Can You Trust the Data?

The Bond Market Is Giving Ominous Warnings About the Global Economy

Stocks Have Had Enough Of The Bond Rally

Wall Street’s Darkening Trade-War Gloom Means Tossing Old Advice

China Puts U.S. Soy Buying on Hold as Tariff War Escalates

Taking Aim at U.S., China Says Provoking Trade Disputes is ‘Naked Economic Terrorism’

The Department of Energy Is Now Calling Fossil Fuels “Molecules of Freedom” and “Freedom Gas”

U.S. Wants T-Mobile to Create New Competitor as Part of Deal

Tesla Woes Send Panasonic’s U.S. Solar Cells to Philippines

The Fiat-Renault Merger: Pitfalls and Potential Profits

Safe Or Scary? The Shifting Reputation Of Glyphosate, AKA Roundup

Uber Will Ban Riders With Low Ratings

Nick Maggiulli: Not Efficient, But Effective

Jeff Miller: Technical Warning, Lookout Below?

Michael Batnick: Where Does My Money Go?, The Podcast Power Law & Should I Invest in Life Insurance?

Be sure to follow me on Twitter.

-

Morning News: May 29, 2019

Posted by Eddy Elfenbein on May 29th, 2019 at 6:51 amWhat History Says About The Current Correction

Why Singapore, Malaysia, Vietnam Were Added to U.S. Currency Watchlist

China Gears Up to Weaponize Rare Earths in Trade War

Trump Hands China an Easy Win in the Trade War

What If the Trade War is Really Deflationary?

Huawei Revs Up Its U.S. Lawsuit, With the Media in Mind

Amazon Gets a New High Target Price on Wall Street

A Fiat Chrysler-Renault Merger Would Put Nissan in a Bind

Arbitration Court Rejects India’s Plea in Case Against Nissan

MediaTek Aims to Take on Qualcomm with New 5G Chip

As E-Sports Grow, So Do Their Homes

MacKenzie Bezos to Give Half of Her $36 Billion Fortune to Charity

Howard Lindzon: Momentum Monday – Flat Lining

Ben Carlson: The David Bowie Hedge When Buying a Home

Be sure to follow me on Twitter.

-

Morning News: May 28, 2019

Posted by Eddy Elfenbein on May 28th, 2019 at 7:12 amVietnam’s Economy Could Soon Be Bigger Than Singapore’s

How the Fiat-Renault Mega-Merger Came Together

China’s First Bank Seizure in 20 Years Sets Investors on Edge

iPhone Profits Will Crash If China Seeks Huawei Revenge

Amazon Is Poised to Unleash a Long-Feared Purge of Small Suppliers

How Much for a China-Made Model 3?

McKinsey Said Disclosure Rules Were Confusing. It Ignored Its Own Primer.

Apple and Nike Brace for China’s Wrath After Huawei Ban

Alibaba Plans Bumper $20 Billion HK Listing to Boost Investment War Chest

Occidental to Sell Parts of Anadarko After Debt-Fueled Acquisition

Sports Illustrated, the Brand, Is Sold for $110 Million

Brexit Is Sending Students Packing, Straining Private Schools on Both Ends

Michael Batnick: Talk Your Book: Help With Your Down Payment From Unison

Ben Carlson: Wealth Is The Stuff You Can’t See

Be sure to follow me on Twitter.

-

Morning News: May 27, 2019

Posted by Eddy Elfenbein on May 27th, 2019 at 5:48 amBitcoin Climbs to Highest in a Year Amid Cryptocurrency Comeback

What Are Frontier Markets and Why Invest in Them?

Trump Presses Japan Over Trade Gap, Expects ‘Good Things’ From North Korea

Japan to Limit Foreign Ownership of Firms in Its IT, Telecom Sectors

Huawei’s CEO Talks Trump, Apple And Whether His Company Can Still Survive

Cisco Will Benefit From U.S. Attack On Huawei

Trump’s Throttling of Huawei Could Backfire on U.S. Tech

Fiat Chrysler Submits Proposal for a Merger with Renault

First Opiodal Trial Takes Aim at Johnson & Johnson

Craft Brewers Lighten Up and Take Aim at the ‘Sweaty Consumer’

It’s Never Been Easier to Be a C.E.O., and the Pay Keeps Rising

Blackstone’s Schwarzman Recalls the Advice That Changed His Life

Jeff Carter: The SEC and Crypto

Roger Nusbaum: The Wisdom of Others

Be sure to follow me on Twitter.

-

Morning News: May 24, 2019

Posted by Eddy Elfenbein on May 24th, 2019 at 7:05 amTheresa May, Britain’s Prime Minister, Resigns

Singapore Chases Tech ‘Jedi Masters’ for Silicon Valley Ambitions

Foreign Investors Hope India Dials Back Policy Shocks After Modi Win

Trump Sparks Oil Rally With Iran Spat, Then Rout With Trade War

Trump Gives Farmers $16 Billion in Aid Amid Prolonged China Trade War

China Denounces U.S. ‘Rumors’ and ‘Lies’ About Huawei Ties to Beijing

Huawei’s European Customers Are Put on Hold by U.S. Ban

Huawei Has Enough Inventory to ‘Weather’ US Blacklist for Months

To Get Boeing 737 Max Flying, Global Consensus Will Be Hard

‘We Have the Meatless?’ Never, Vows Arby’s President

Tesla Stock Is in Trouble and Elon Musk Has Gone From Iron Man to Inspector Gadget

Amazon Shares May Be Worth $3,000 in Two Years, Piper Says

Ben Carlson: My Personal Finance Mentor

Michael Batnick: What I Learned from Doing a Financial Plan

Cullen Roche: Is Vanguard Better at Predicting Future Returns?

Be sure to follow me on Twitter.

-

Ross Stores Earned $1.15 per Share

Posted by Eddy Elfenbein on May 23rd, 2019 at 4:40 pmRoss Stores (ROST) just released its first-quarter earnings report. The company earned $1.15 per share. Previously, the deep-discounter had given us an earnings range of $1.05 to $1.11 per share. As usual, their guidance was conservative. Comparable store sales were up 2%.

Barbara Rentler, Chief Executive Officer, commented, “For the first quarter, we delivered sales gains at the high end of our guidance as well as better-than-expected earnings per share growth despite continued underperformance in Ladies apparel. While operating margin of 14.1% was down from the prior year, it was above plan mainly due to higher merchandise margin. As expected, this improvement was more than offset by increases in freight and wage costs and the timing of packaway-related expenses that benefited the prior year period.”

For Q2, Ross sees comparable store sales growth of 1% to 2%. For EPS, the company sees the exact same as Q1, $1.05 to $1.11 per share. Wall Street had been expecting $1.14 per share.

The company also updated its full-year guidance. Ross now sees earnings of $4.38 to $4.52 per share. That includes seven cents per share thanks to a favorable tax benefit. The previous range was $4.30 to $4.52 per share. Adjusting for that, in effect, ROST’s guidance range narrowed thanks to a one-cent increase at the low end and a five-cent decrease at the high end.

The stock is down about 2.5% after hours.

-

Hormel Foods Earned 46 Cents per Share

Posted by Eddy Elfenbein on May 23rd, 2019 at 7:06 amThis morning, Hormel Foods (HRL) reported fiscal Q2 earnings of 46 cents per share. That beat expectations by one penny per share.

Hormel lowered its fiscal 2019 outlook. They now see sales of $9.5 billion to $10 billion. The previous guidance was $9.7 billion to $10.2 billion. They also lowered their EPS guidance to $1.71 to $1.85. The previous range was $1.77 to $1.91 per share.

Here’s the executive summary:

Volume of 1.2 billion lbs., up 1%

Record net sales of $2.3 billion, up 1%

Pretax earnings of $318 million, up 7%

Diluted earnings per share of $0.52

Excluding one-time gain on the divestiture of CytoSport, adjusted diluted EPS of $0.46 per share

Effective tax rate of 11.1% compared to 20.0% last year

Operating margin of 13.3% compared to 12.9% last year

Year-to-date cash flow from operations of $366 million, down 18% due to higher working capital

Fiscal 2019 earnings guidance decreased to $1.71 to $1.85 per share from $1.77 to $1.91 per share

COMMENTARY

“We achieved record sales this quarter as three of our four segments delivered volume and sales growth,” said Jim Snee, chairman of the board, president and chief executive officer. “Many of our innovative product lines such as Hormel® Bacon 1TM cooked bacon, Hormel® Fire BraisedTM products, Hormel® Natural Choice® snacks and Herdez® salsa delivered double-digit sales growth. We also grew core product lines such as Hormel® pepperoni, Dinty Moore® stew and Austin Blues® authentic barbeque products.”

“In spite of record sales, second quarter earnings did not meet our expectations,” Snee said. “African swine fever in China started to impact global hog and pork markets this quarter, which led to rapidly increasing input costs. In response, we have announced pricing action across our branded value-added portfolio in the Grocery Products, Refrigerated Foods and International segments.”

“Jennie-O Turkey Store profits declined due to a combination of plant startup costs and lower retail sales,” Snee said. “We made a large investment to automate our whole-bird facility in Melrose, Minn., and the startup was more difficult than anticipated. We made excellent progress through the quarter and are now on track to deliver the production efficiencies we expected. Retail sales declined for the quarter, but we are reactivating promotional activity and advertising in order to regain distribution.”

“We finalized the sale of CytoSport this quarter and used the proceeds to pay down the remaining debt from the Columbus Craft Meats acquisition and build our cash position,” Snee said. “We will use our strong balance sheet to continue to grow our company through disciplined and strategic investments, including acquisitions and capacity expansion projects.”

OUTLOOK

“Over the past three years, the intentional actions we have taken as part of Our Path Forward, which include evolving to a broader global branded food company, accelerating our foodservice business, modernizing our supply chain and divesting nonstrategic assets, has made our company stronger,” Snee said. “Our experienced management team, leading brands, focus on innovation, strong balance sheet and diversified businesses allow us to manage through times of uncertainty and volatility, as we are currently experiencing with African swine fever.”

The company’s revised fiscal 2019 earnings guidance range is based on the input cost increases experienced in the second quarter and a forecast for volatile domestic pork prices in the second half of fiscal 2019. The company has a proven ability to operate in elevated market conditions but expects short-term margin compression as branded value-added pricing actions lag input cost increases. Additionally, expectations for Jennie-O Turkey Store have been lowered as the company reinvests in the Jennie-O® brand in order to regain retail distribution.

Update: Shares of HRL fell 6.3% this morning, but later rallied back. The stock closed down 0.91% today which was less than the overall market’s drop of 1.19%.

-

Morning News: May 23, 2019

Posted by Eddy Elfenbein on May 23rd, 2019 at 7:04 amFull-Blown Trade War Is Quickly Shifting From Risk to ‘Baseline’

Mobile Carriers in Britain and Japan Begin to Turn Away From Huawei

If Huawei Loses ARM’s Chip Designs, It’s Toast

Amazon Shareholders Reject Facial Recognition Ban as Concern Grows in U.S. Congress

DOJ Attorneys Reportedly Ready to Block T-Mobile/Sprint Merger

Qualcomm’s Day of Reckoning May Have Arrived

iPhone Fights Apple’s Embarrassing Problem

Apple Secretly Tried to Buy Tesla, and It All Fell Apart for a Truly Stunning Reason

Deutsche Bank CEO Readies Investment Bank Cuts as Stock Hits Low

The Wealth Detective Who Finds the Hidden Money of the Super Rich

Roger Nusbaum: Retirement Reading Roundup

Jeff Miller: Throwing In The Towel At Exactly The Wrong Time?

Joshua Brown: What Are Your Thoughts: The $47 Trillion Question

Be sure to follow me on Twitter.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His