-

CWS Market Review – June 8, 2018

Posted by Eddy Elfenbein on June 8th, 2018 at 7:08 am“If you would know the value of money, go and try to borrow some.”

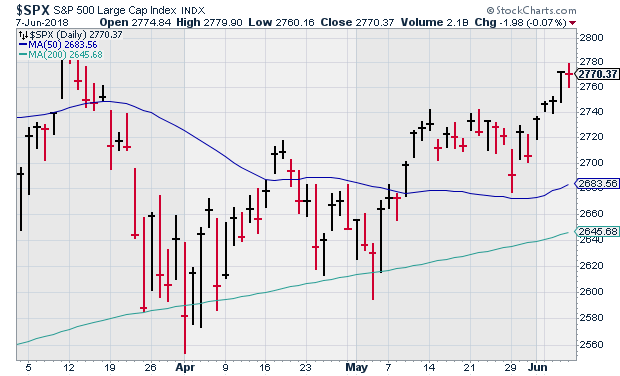

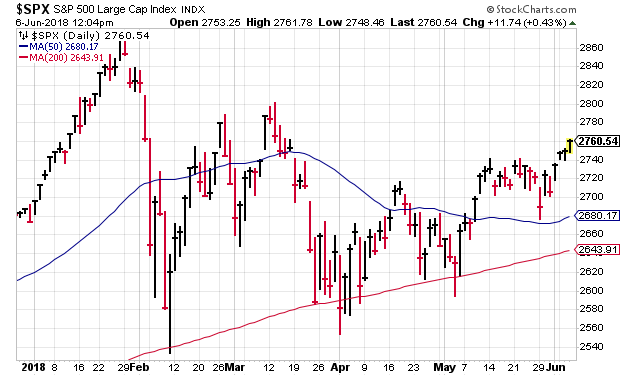

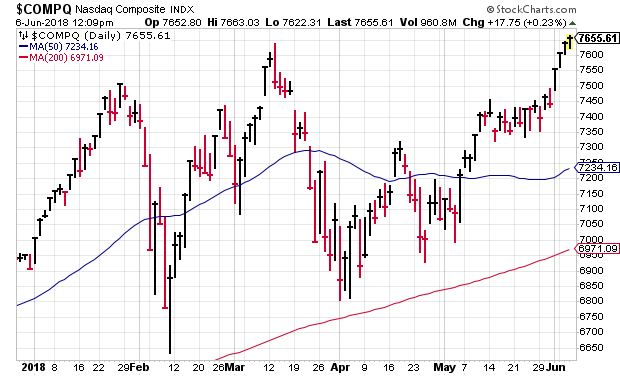

– Benjamin FranklinThe stock market suddenly got a lot more interesting this week. The Nasdaq Composite broke out to a new all-time high. So did the small-cap Russell 2000. The Dow is back over 25,000, and the S&P 500 rallied for four days in a row. The index recently touched its highest point in more than two months.

The market isn’t so much celebrating good news as it is feeling relieved that the prospect for bad news has dissipated. Global tensions seem to be relaxing. There may even be some sort of détente with North Korea. In the last few weeks, the price of oil has dropped more than 10%.

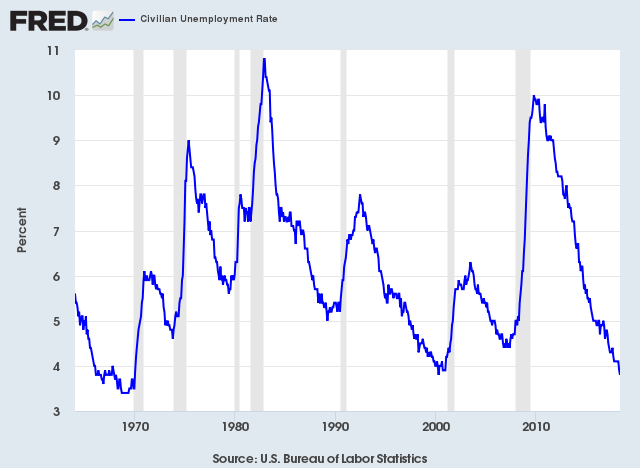

One piece of good news came last Friday when the government said that the unemployment rate fell to its lowest since the 1960s. In this week’s issue, we’ll take a closer look at the market and the economy. I’ll also discuss the disappointing earnings report from Smucker. I also have several Buy List updates for you this week (nice rebound for Ross Stores!). But first, is this really the best economy in half a century?

The Best Economy in 50 Years?

Last Friday, the government released the jobs report for May, and it said that the U.S. economy created 223,000 net new jobs last month. That figure beat expectations of 190,000 jobs. The unemployment rate ticked down to 3.8% which tied the cycle low from April 2000. However, if you work out the decimals, the jobless rate is actually the lowest since the 1960s. (Well, since December 1969.) For women, it’s the lowest jobless rate since 1953.

Despite the good news, there are some noticeable holes in the current expansion. For one, it’s always a bit dicey to compare unemployment rates over such a long period of time. The economy is quite different from what it was in 1960, and so is the labor market. While the economic numbers are improving, we’re still not seeing much in the way of wage growth. In the last year, average hourly earnings were up 2.7%. That’s okay, and it’s above inflation, but it needs to be better. The equation is simple: higher wages means more shoppers.

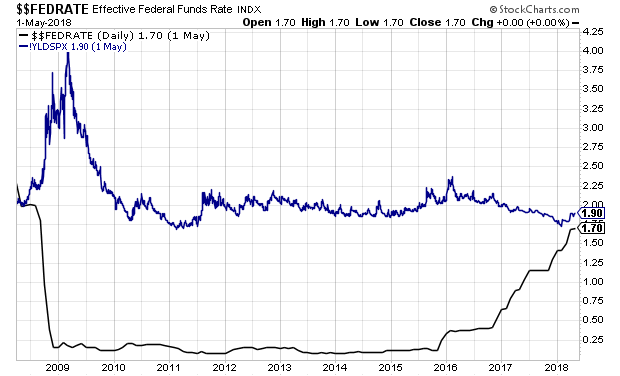

The Federal Reserve meets again next week, and it’s a near-certainty that the central bank will raise interest rates. This will be their seventh increase of this cycle. To recap, the Fed raised rates once in 2015, another time in 2016, then three times last year and already once more this year. This will bring the target range for Fed funds up to 1.75% to 2%.

Not too long ago, it looked like there might be four hikes this year, but that’s probably off the table. For now. With this meeting, we’ll get a post-meeting press conference with Chairman Jay Powell. The Fed members will also update their economic forecasts. These forecasts are notoriously poor, but I have to give the Fed some credit: they’ve largely stuck to their recent rate-hike plans.

I’ve tried to stress to investors that rising interest rates are Kryptonite to a stock rally. However, and this is crucial, it usually takes a few hikes to do any real damage. We’re now getting close to the point where the Fed funds rate is equal to the dividend yield of the S&P 500. In 2009, that would have seemed like it was light-years away.

I like to keep track of the “real” Fed funds rate. That’s the rate adjusted for inflation (I prefer using the core rate). After next week’s hike, the real Fed funds rate will be very close to something it hasn’t been in a long time—a positive number! In real terms, the Fed has been handing out free money for over a decade. I think we’ll need one more hike to finally push real Fed funds into positive territory. As a very general rule, it’s hard to be against stocks when the Fed is handing out free checks. The Fed’s low-rate policy has certainly been a key driver of this long rally.

But what about next year? According to the Fed’s last projections, they see three more hikes next year. But there was wide dispersion, meaning the individual estimates are far apart. That’s why next week’s meeting is so important. We’ll probably get a better idea of the Fed’s thinking. Three more hikes could do some damage to the economy and the market.

There are a few things to consider. One is that long-term rates have come down some. That’s kinda like the ceiling for short-term rates. Trouble usually happens when short rates exceed long rates. My favorite indicator is the 2/10 Spread which is now at 45 basis points. That’s down about 90 basis points in the last 18 months. We’re not in the danger zone yet, but it’s no longer unthinkable.

Smucker Drops after Poor Earnings

On Thursday, JM Smucker (SJM) got dinged for a 5.4% loss after the jelly company reported disappointing earnings. Smucker reported fiscal Q4 earnings (after a few adjustments) of $1.93 per share, which was well below the company’s own guidance of $2.17 to $2.27 per share. Wall Street had been expecting $2.18 per share. The CEO blamed the miss on “industrywide headwinds and certain discrete items.” More on that in a bit.

Smucker also had disappointing guidance for the coming year. Smucker sees this year’s earnings (ending in April) coming in between $8.40 and $8.65 per share. Wall Street had been expecting $9.18 per share.

There are a few reasons for Smucker’s slide. For one, Canada announced retaliatory tariffs on American jam which is a core SJM product. The company is also facing higher costs which places it in the tough position of passing said costs on to consumers. This is a tough environment in which to raise prices. Bear in mind that Smucker is a lot more than jelly. They also make Jif peanut butter and Folger’s coffee, and they have a pet-food division, which is the company’s largest.

Last quarter, sales of Smucker’s consumer foods fell by 1.8%. Pet food was flat, while coffee was up 0.5%. For the quarter, net sales fell by 0.1%. The issue really comes down to pricing and how much latitude Smucker truly has. Everyone in the industry is facing the same issue. These results suggest that Smucker may have to give in and deal with lower margins. To be fair, Smucker has already started to adjust its business model to better compete in a challenging market. For example, they’re looking to sell off their baking business.

Last year, Smucker made $7.96 per share. The stock closed Thursday at $100.80, which is exactly 12 times the lower bound of their full-year guidance. This week, I’m dropping my Buy Below on Smucker down to $114 per share. I still like Smucker, but the company needs to make some important adjustments in order to meet a difficult environment.

Buy List Updates

Our philosophy of investing is to focus on great companies and hold them as long as we can. This has two important benefits. The first is that it’s less work, which is always nice. But more importantly, it’s a superior system because it removes us from the irrationality of the day-to-day market. I often stress this, but we got a good lesson recently from Ross Stores (ROST).

I’m a big fan of Ross, and it’s been part of our Buy List for several years. The deep-discounter reported earnings on May 24. They beat expectations, but their guidance wasn’t that hot. Well, that’s what Ross always does, so I paid it no mind. I thought the earnings report was just fine, but the market gods were not pleased. Shares of ROST dropped nearly 7% the next day.

In last week’s issue, I wrote, “I’m not at all worried about Ross Stores.” Sure enough, Ross has rallied six times in the last seven days. The stock closed Thursday at $85.09. Not only did Ross make back everything it lost, but the stock is even higher than it was going into earnings.

I will freely admit you that I had no idea Ross would snap back so quickly. Of course, I was puzzled by the drop in the first place. But this is the reality of stock investing. Sometimes, weird things happen. This is precisely why we lock in on great companies and let time do the heavy lifting. This week, I’m raising my Buy Below on Ross Stores to $90 per share.

Another stock that’s rising from the ashes is Alliance Data Systems (ADS). Poor ADS has been one of our worst stocks this year. The stock went from a high of $278 in January down to $192 in early May. The last earnings report was pretty good, but that wasn’t enough to halt the selling. Lately, however, ADS has turned a corner. The shares closed Thursday at $220.57. It’s too early to declare victory, but things are finally going in the right direction. Check out this recent article from Forbes, “Why Alliance Data Is Trading at a Discount.”

Carriage Services (CSV) made some news this week, which is pretty rare. The funeral-home company made some complicated moves to restructure its balance sheet. This was to correct for, in their words, “unforced errors.” Since the company had to issue more shares, they reduced their four-quarter EPS guidance to $1.33 to $1.38. I think the moves are to Carriage’s long-term benefit. Don’t abandon this one.

In early May, Continental Building Products (CBPX) missed earnings by a penny per share. During the next trading day, the stock got as low at $25.70 per share. That was a loss of over 7%. I was impressed that the company didn’t change its full year forecast. Here we are five weeks later, and CBPX is up to $31.45 per share. That’s a 14% gain in the last 23 days. I’m raising our Buy Below on Continental Building to $34 per share.

We’re done with Buy List earnings reports for a while. FactSet (FDS) is due to report on June 26, but that’s it until the Q2 earnings season starts up in mid-July. RPM International’s (RPM) fiscal fourth quarter ended in May, and their earnings will probably be out in late July.

That’s all for now. Get ready for a Fed rate hike next week. The Federal Reserve meets on Tuesday and Wednesday. The policy statement will come out at 2 p.m. on Wednesday. We’ll also get a look at the updated forecasts. There will also be some key economic reports. The retail-sales report will come out on Thursday. Then on Friday, we’ll get to see the latest report on industrial production. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: June 8, 2018

Posted by Eddy Elfenbein on June 8th, 2018 at 7:04 amArgentina Reaches $50 Billion Financing Deal With I.M.F.

Brazil Hosts Major Auction for Oil Fields

Oil Prices Fall on Dip in China Demand, Surging U.S. Output

As Utility Stocks Get Crushed, Possibilities Emerge

Betting on Crisis, Hedge Funds Short Italian Bonds

Banks Don’t Share Wells Fargo’s ‘Systemic’ Account Problems, Regulator Says

How the Gig Economy Is Reshaping Work: Not So Much

Jack Ma’s Ant Financial Valued Around $150 Billion After Funding Round

Google Renounces AI Weapons; Will Still Work With Military

Tesla’s Energy Storage Business Is Surging

KFC is Right — People Are Gobbling Up ’Meat Replacements’

Lawrence Hamtil: Not Even Buffett Can Escape the Reversion to the Mean

Roger Nusbaum: Indexing Will Fail? Really?

Blue Harbinger: Do You Start the Day With a Trading Plan?

Be sure to follow me on Twitter.

-

Smucker Drops on Earnings Miss

Posted by Eddy Elfenbein on June 7th, 2018 at 12:08 pmThis morning, JM Smucker (SJM) reported fiscal Q4 earnings (after a few adjustments) of $1.93 per share which was well below the company’s own guidance of $2.17 to $2.27 per share. The CEO blamed the miss on “industrywide headwinds and certain discrete items.”

The company also had disappointing guidance for the coming year. Smucker sees this year’s earnings coming in between $8.40 and $8.65 per share. Wall Street had been expecting $9.18 per share.

The WSJ reports:

J.M. Smucker is among several companies trying to figure out what consumers want in their kitchens. Other food companies like Kraft Heinz Co. and Campbell Soup Co. have struggled with sales in recent times as customers’ food choices change.

At the same time, J.M. Smucker has been working to change its business mix.

In April, the company said it was looking at options for its baking business, such as selling it. That business includes the Pillsbury brand. That same day, the company said it had agreed to buy Ainsworth Pet Nutrition LLC, a deal J.M. Smucker said it valued at $1.7 billion.

The company also launched a higher-end version of its Folgers brand in April. Mr. Smucker had said the company was “trying to strike the right balance between leading, iconic brands and emerging brands.”

-

Morning News: June 7, 2018

Posted by Eddy Elfenbein on June 7th, 2018 at 7:15 amHong Kong’s China Loan Pipe Is Gurgling Too Loud

U.S. Trade Deficit Falls to 7-Month Low as Exports Set Fresh Record

U.S. Congress Has Few Options to Stop Trump from Saving China’s ZTE

The Simple Message From the Trustees of Social Security and Medicare

Mick Mulvaney Effectively Fires CFPB Advisory Council

Landline Phone Service, Which Still Exists, Goes Down Across the U.S.

New Bitcoin ETF Would Set Buyers Back $200,000

Coinbase Expands With Deal for Broker-Dealer Keystone Capital

Uber Jumps Into Europe’s Crowded Bike-Sharing Market

How I Learned to Stop Worrying and Love Electric Scooters

You Can Now Drive As Many Mercedes-Benz Cars As You Want For $1,095 a Month

IHOP Is Changing Its Name And The Internet Can’t Handle It

Cullen Roche: The Vollgeld Proposal is Bad. Very Bad.

Ben Carlson: Animal Spirits: Big Mistakes

Be sure to follow me on Twitter.

-

The Surging Market

Posted by Eddy Elfenbein on June 6th, 2018 at 12:10 pmThe S&P 500 is now up for the fourth day in a row. The index is near its highest levels in more than two months.

The S&P 500 is also above its 50- and 200-day moving averages. The real winner lately has been the Nasdaq Composite which just touched a new all-time high.

I’m glad to see Alliance Data Systems (ADS) up to $220 today. ADS was down to $193 a month ago.

-

Morning News: June 6, 2018

Posted by Eddy Elfenbein on June 6th, 2018 at 7:16 amIndia Sees Record Low Solar Prices Returning on China Reforms

The Next Bond Rout: It’s Bigger Than Italy

The ECB is About to Take a Key Step Toward an Easy-Money Exit

Social Security to Tap Into Trust Fund for First Time in 36 Years

Teamsters Vote to Authorize Strike as UPS Contract Talks Heat Up

China’s ZTE Signed Preliminary Agreement to Lift U.S. Ban

Wells Fargo Pulls Back from U.S. Midwest, Selling 52 Branches to Flagstar

Elon Musk Appears Emotional As He Overcomes Vote to Remove Him as Tesla Chairman

David Koch Steps Down From Business and Conservative Political Group

Scooters Are Cool, But Not $1 Billion Cool

IHOP Is Getting a New Name. And It Doesn’t Include Pancakes

Why Women Hold the Majority of Student Loan Debt in America

Nick Maggiulli: Reps, Reps, Reps

Howard Lindzon: Momentum Monday…You Do Not Need to Own Everything

Michael Batnick: Animal Spirits: Big Mistakes

Be sure to follow me on Twitter.

-

College Investor’s Top Investing Blogs of 2018

Posted by Eddy Elfenbein on June 5th, 2018 at 12:50 pmThank you to College Investor for naming me as one of their top investing blogs for 2018. Check out the whole list here. There are many outstanding blogs listed.

-

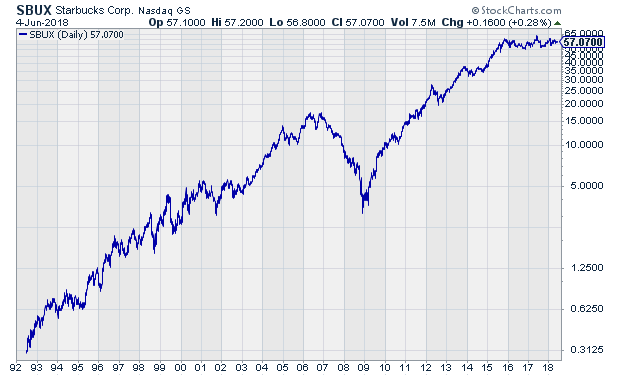

Howard Schultz is Stepping Down at Starbucks

Posted by Eddy Elfenbein on June 5th, 2018 at 10:40 amHoward Schultz said he’s stepping down as executive chairman of Starbucks (SBUX). There’s been talk that he might run for president.

I’ll skip that topic to focus on the long-term performance of Starbucks. It’s been a truly remarkable company. They IPO’d 26 years ago this month at 27 cents per share (that’s $17 adjusted for six 2-for-1 splits.) Today, it closed at $57.07. Not bad.

Schultz had two runs as CEO, from 1986 to 2000 and then again from 2008 to 2017. He came on after the stock’s one terrible stretch.

Thanks to over-expansion, the stock fell from an intra-day high of $10 per share on November 16, 2006 down to $1.765 on November 21, 2008. Eighty percent losses tend to upset shareholders and that’s why Schultz was brought back. He helped turn the ship around, and today, there are more than 26,000 locations.

The company started paying a five-cent quarterly dividend in 2010. That’s been raised every year since then, and it’s now up to 30 cents per quarter. That’s a payout ratio of around 50%.

-

Morning News: June 5, 2018

Posted by Eddy Elfenbein on June 5th, 2018 at 7:15 amCrude Oil Kissing $80, OPEC Whispers, and the Implications for E&P

Trump Plan to Prop Up Coal, Nuclear Won’t Protect the Electric Grid

ANZ, Citi, Deutsche Bank Accused of Engaging in Cartel Conduct

Gilt Groupe Sold to Rival Rue La La

What to Watch for as Tesla Investors Decide the Future of Musk’s Board

GitHub Billionaires Will Own More Microsoft Stock Than Its CEO

Toshiba to Close the Book on Its Laptop Unit

Qantas Gives In to Beijing’s ‘Orwellian’ Demand to Change How It Refers to Taiwan

Walmart Sheds Majority Stake in Brazil Operation

In Biotech, $6 Billion Can Vanish Quickly

McDonald’s Is Making a Big Bet on Self-Service Kiosks

Michael Batnick: The Next Fifty Years

Howard Lindzon: Financial Pardons (Do Not Count on Them) and Taking Profits is Not a Crime

Jeff Carter: Crypto And Term Sheet & Regulation and the Retail Investor

Be sure to follow me on Twitter.

-

Looking at Peter Drucker

Posted by Eddy Elfenbein on June 4th, 2018 at 12:16 pmThe subject of Peter Drucker recently came up. Here’s what I wrote about him upon his passing in 2005. This was one of my first blog posts to get attention.

He was born in Vienna during the reign of Emperor Franz Joseph (his middle initial F. stood for Ferdinand). Keynes and Schumpeter were his economics professors. His first book was reviewed by Winston Churchill in the Times Literary Supplement in 1939. The 29-year-old proved to be more prescient than the Great Man.

Mr. Drucker is one of those writers to whom almost anything can be forgiven because he not only has a mind of his own, but has the gift of starting other minds along a stimulating line of thought. There is not much that needs forgiveness in this book, but Mr. Drucker tends to be carried away by his own enthusiasm, so that the pieces of the puzzle fit together rather too neatly. It is indeed curious that a man so alive to the dangers of mechanical conceptions should himself be caught up in the subordinate machinery of his own argument. His proof, for example, that Russia and Germany must come together forgets the nationalism which has developed in Russia during the last twenty years and which would react very strongly against any new German domination of Russian life. But such excesses of logic are pardonable enough in a book that successfully links the dictatorships which are outstanding in contemporary life with that absence of a working philosophy which is equally outstanding in contemporary thought.

Within three months, Poland’s fate was sealed. When looking at Drucker’s work, the most arresting fact isn’t how much he got right but rather how much he’s still misunderstood.

Mr. Drucker thought of himself, first and foremost, as a writer and teacher, though he eventually settled on the term “social ecologist.” He became internationally renowned for urging corporate leaders to agree with subordinates on objectives and goals and then get out of the way of decisions about how to achieve them.

He challenged both business and labor leaders to search for ways to give workers more control over their work environment. He also argued that governments should turn many functions over to private enterprise and urged organizing in teams to exploit the rise of a technology-astute class of “knowledge workers.”

Mr. Drucker staunchly defended the need for businesses to be profitable but he preached that employees were a resource, not a cost. His constant focus on the human impact of management decisions did not always appeal to executives, but they could not help noticing how it helped him foresee many major trends in business and politics.

He began talking about such practices in the 1940’s and 50’s, decades before they became so widespread that they were taken for common sense. Mr. Drucker also foresaw that the 1970’s would be a decade of inflation, that Japanese manufacturers would become major competitors for the United States and that union power would decline.

For all his insights, he clearly owed much of his impact to his extraordinary energy and skills as a communicator. But while Mr. Drucker loved dazzling audiences with his wit and wisdom, his goal was not to be known as an oracle. Indeed, after writing a rosy-eyed article shortly before the stock market crash of 1929 in which he outlined why stocks prices would rise, he pledged to himself to stay away from gratuitous predictions. Instead, his views about where the world was headed generally arose out of advocacy for what he saw as moral action.

As for me, I’m a bit weary of the Cult of Drucker, which is often quite different from the man. I often hear his disciples pontificate his “ideas,” which wind up being little more than Benjamin Franklin-style truisms—only covered in jargon and masquerading as ideology. “An apple a day keeps the doctor away” becomes “pro-active management encourages and facilitates preventative-based strategies in order to ensure long-run objectives without negative and unforeseen downside effects.” So much Latin, and so little English. Such are the dangers in thinking outside one’s box.

But how far can the study of management go? For all of management’s influence, the most difficult question is: Why is this enterprise worth managing? My fear is that Drucker’s legacy is so liquid that his mantle can be claimed by most anyone. The race has been on for quite some time. Right now, the yellow-jersey belongs to Newt Gingrich. The former Speaker of the House, who’s an admirer of Alvin Toffler and other future babble, has clearly adopted Drucker as a political ally.

Too many of our business schools, academic centers, media moguls, and government leaders still rely on the Keynesian command-and-control bureaucratic model. They rely on almost nothing of Drucker and even less of the Austrian school and, as a result, routinely apply the wrong principles to structuring education, training, health care, and our role in international trade. Again and again they reject the marketplace. They reject the principles of management. They reject the essence of entrepreneurship. They reject the heart of Drucker and apply instead patterns and behaviors that simply don’t work.

That is the ultimate critique of big-city schools. It’s the ultimate critique of government-run health care. It is the ultimate critique of the way the federal government and state and local governments mismanage resources. It simply doesn’t work.

To be sure, Gingrich’s ideas can stand or fall on their own—with or without the support of Drucker. But we ought to be clear that Drucker’s ideas have little to do with what Gingrich says. In fact, Drucker was never particularly interested in economics. Too much theory, not enough people.

Drucker’s concern was studying institutions as institutions. That’s what he saw in 1939. The Nazis and Soviets had to come together. It was simply what they were. The institutions demanded it. For Drucker, it didn’t matter which institutions he looked at; governments, unions, corporations. He really didn’t find much use in analyzing the government. Drucker preferred the non-profit sector. He even looked at the Girl Scouts. To Drucker, an institution had an internal agenda simply because it is an institution.

Drucker saw the driver of an institution as its management. His goal was to isolate management as a separate concept and study what made some managers good and others bad. While it sounds a bit platitudinal now, it was quite new then.

Still, when reading Drucker I can’t help feeling undernourished. Consider this from Forbes a few years ago:

In 1989 C. William Pollard, chairman of the ServiceMaster Co., took his board of directors from Chicago to meet Drucker. In a back room of Drucker’s utterly unpretentious home, the sage of Claremont opened the meeting by asking the group, “Can you tell me what your business is?”

Each director gave a different answer. Housecleaning, said one. Insect extermination, said another. Lawn care, said a third.

“You’re all wrong,” Drucker said. “Gentlemen, you do not understand your business. Your business is to train the least-skilled people and make them functional.”

Groan. This is only the beginning of an exposure to Drucker. Soon, the “ideas” begin to flow freely. We’re now “knowledge workers.” And we’re moving to a “knowledge-based society.” But…what of it? Before we know it we’re “managing change,” yet I’m only interested in “making money.” Again, here’s Drucker:

One of the most important jobs ahead for the top management of the big company of tomorrow, and especially of the multinational, will be to balance the conflicting demands on business being made by the need for both short-term and long-term results, and by the corporation’s various constituencies: customers, shareholders (especially institutional investors and pension funds), knowledge employees and communities.

Call me unimpressed. I can’t say that I disagree with anything Drucker says, which is part of the problem. Truthfully, I think the study of management can only go so far. It’s important, but it’s easily overanalyzed. Just as the diplomat urges diplomacy and the general favors war, the management guru sees only the primacy of managers. To Drucker’s fans, it seems hard to conceive the fact that Grant crossed the James without the aid of a flow chart.

Here’s a large section of Druckerama. Apparently, everything is transformational. Everyone is empowered. It all sounds so epic, yet at the same time so…bland. The themes have taken over the building and they’ve smothered the plot. What’s left is Drucker’s true legacy, his boundless enthusiasm. If only all managers had it. To Churchill, Russia may have been a riddle wrapped in a mystery inside an enigma, but he saw Drucker clearly.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His