-

CWS Market Review – March 14, 2023

Posted by Eddy Elfenbein on March 14th, 2023 at 5:52 pm(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

This week’s news on Wall Street has been dominated by the stunning collapse of Silicon Valley Bank. This is the second-largest bank failure in U.S. history. Investors are still feeling the shockwaves. We’re not done. There could be others.

In this week’s issue, I want to explain what happened and why. I also want to discuss potential ramifications.

Banks Are Different

Before we dig into the remains of Silicon Valley Bank, I should explain that free enterprise is often referred to as the “profit system,” but that’s not quite right. It’s really the profit and loss system. It’s the “and loss” part that helps make it so successful.

When a business goes bust, it’s an unfortunate thing, but it’s necessary to close unprofitable enterprises. You don’t want zombie businesses that are kept alive by endless streams of funding.

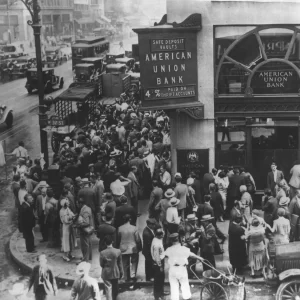

A crowd of outside the American Union Bank during the Great Depression.

When a business goes bankrupt, there’s a standard playbook to follow. The business goes to a bankruptcy court. A judge orders all the assets to be sold. The creditors get first dibs, and the equity holders get whatever’s left. That’s basically it.

Again, it’s unpleasant but necessary. The worst part is that employees lose their jobs. While that’s also unpleasant, most people can find something new rather quickly. Of course, there’s also unemployment insurance.

Some studies have shown that being laid off can often be a blessing in disguise in that it forces people to leave an unsatisfying job for something more rewarding. I’ve seen many examples of that personally. I’m sure you have as well.

The other downside of a bankruptcy is that your suppliers lose your business, but, for the most part, the world moves on. The ending of one business leaves a wound that tends to heal surprisingly quickly.

Now we come to the one, giant exception to what I’ve said. When a bank goes under, it’s a very big deal because the damage isn’t limited to a few parties. If a bank goes under, it can take all its depositors with it.

That means that several other businesses could go bust even though they were perfectly healthy. Bank runs can quickly become self-reinforcing cycles. That’s happened many times in history, not just in “Mary Poppins” and “It’s a Wonderful Life.” In fact, it’s the volatile and viral nature of bank runs that led to the creation of the Federal Reserve in the first place.

One of the foundational issues in finance is, “how do we let bad banks fail without ruining the depositors?” Frankly, there are no good answers, but there are several less-bad answers such as deposit insurance and risk capital ratios. We make do the best we can.

What Happened at Silicon Valley Bank

Having said that, let’s turn to what happened at Silicon Valley Bank. What’s interesting is that what impacted SVB was many of the same things we’ve talked about in recent months.

When Covid struck, the Federal Reserve responded quickly by lowering interest rates to the floor. That sparked a furious rally in high-risk assets. Our Buy List certainly felt the effect. In Silicon Valley it led to a venture capital-funded investment boom. Every start-up was getting funding. When rates are at 0.%, why not?

SVB was the banker of choice for Silicon Valley. If you’re a start-up and you got, say, $5 million in Series A funding, then you most likely stuck it in SVB. All the cool kids were doing it.

This led to a large surge in deposits for SVB. As odd as it may sound, that’s not always a good thing for a bank. SVB had to invest those assets to make money to cover its deposits. The bank selected to invest in longer-term government bonds, agency bonds and mortgage-backed bonds.

Then came inflation and game changed. The Fed aggressively raised interest rates and high-risk assets faltered. The venture capital spigot for Silicon Valley was shut off, so the start-ups withdrew money from their SVB accounts. Start-ups can burn through cash at an alarming rate.

To cover those withdrawals, SVB had to sell those bonds. The problem was that the values of the bonds had tanked thanks to the Fed and inflation, so SVB was selling for a big loss. It also didn’t help that for nine months, SVB didn’t have a chief risk officer.

One of our Buy List stocks, Moody’s (MCO), told SVB that it was looking to downgrade the company’s stock credit rating.

SVB came up with an idea. On Wednesday, SVB announced a plan to raise money by selling stock. That was truly a massive flop.

Instead of calming investors, the stock sale news frightened depositors and they withdrew their money, nearly all at once. Nowadays, it only involves the click of a mouse to move money, instead of waiting in line at the old Bailey Building & Loan. In one day, depositors withdraw one-quarter of the bank’s total deposits. The bank’s website was having difficulty keeping up which isn’t a good look for anything based in Silicon Valley.

Peter Thiel, an influential figure in Silicon Valley, withdrew his money from SVB. On Thursday, SVB’s stock crashed 60%. The government had seen enough. They stepped in and shut SVB down. A bank hadn’t failed in the U.S. in more than two years.

Typically, when the government takes over a bank, it aims to sell it off quickly to a nearby competitor, even at a steep discount. The Feds would rather do a deal fast than good. The government was desperately looking for a buyer and, apparently, no one was interested.

Even if the government could sell off some of SVB’s assets, that could meet limited withdrawal needs. In 1907, J.P. Morgan famously stopped the financial panic by serving as the lender of last resort. Alas, in 2023, no one on Wall Street wanted anything to do with SVB.

FDIC insurance covers deposits up to $250,000 but that was a tiny portion of SVB’s deposits. The large majority of deposits were uninsured. On Sunday, the government announced a plan to insure all SVB’s deposits, whether they had been insured or not.

Make no mistake – this is a bailout, but it’s different from what happened in 2008. This is more of an indirect bailout. To be clear, SVB’s shareholders are getting nothing and all the top people will be fired.

Still, thanks to the government, lots of Silicon Valley startups have been pulled from the fire. For example, a company called Wrapbook, which does payroll processing for the entertainment industry, said its payments might be delayed. If their deposits were wiped out, that could have hurt a lot of regular Joes. Don’t think this was all about protecting the fat cats.

This is the problem with a financial mess like this. You don’t know who has exposure to whom until the house of cards comes tumbling down.

Over the weekend, there were some panicky voices predicting bank runs on Monday morning. That didn’t happen.

I’ve noticed that people like to overlay a highly moralized narrative on a financial breakdown. That can be a mistake. Not that there aren’t heroes and villains, but that it may cloud what really happened. SVB was in a lousy position – they had bad luck and they made some dumb mistakes. Very dumb. It didn’t help matters that this happened so shortly after FTX and the same time that Silvergate announced its voluntary liquidation.

I am, however, curious about well-timed stock sales from senior SVB management. I hope this will be looked into.

Signature Bank Also Comes to an End

The government also shut down Signature Bank (SBNY) which was a former Buy List stock. The government is also standing by SBNY’s uninsured deposits. We sold out of SBNY three years ago. We even made a small profit. The bank decided to become a major financial resource for crypto. Let’s just say that I don’t have any regrets in selling SBNY.

There’s a Regional Bank ETF (KRE) that’s become an unofficial bellwether for the current crisis. The ETF dropped 4% last Thursday and another 8% on Friday. Yesterday, KRE dropped another 12%.

The other bank that’s teetering on the edge is First Republic (FRC). Its stock plunged 62% on Monday. Trading was halted in several banking stocks yesterday. Wall Street seems to be breathing a lot easier today. Shares of FRC gained 27% today. Charles Schwab (SCHW) was up 9%. KRE closed 2% higher.

I suspect that the worst is behind us, but we’re not out of the woods just yet. Earlier today, Moody’s cut its view on the banking sector from stable to negative.

If you want to take advantage of the crisis, I would say that SCHW is a speculative buy here, but expect a lot of volatility.

There’s also the question of what happens to deposit insurance now. Is there no longer a $250,000 limit? I don’t know, but if you make an exception for one group, then others will expect the same. Some observers have said this will cause an exodus from smaller banks to only the largest banks. I’m not sure if that’s right but it could happen.

It doesn’t seem right to expect every bank customer to review the soundness of each bank. Just insure all bank deposits. This crisis reveals that that’s what would happen anyway.

Another effect of Silicon Valley has been a big jump in Treasuries in the last few days. Over Thursday, Friday and Monday, the yield on the two-year Treasury fell 103 basis points (or 1.03%). Ironically, some of the recent rally certainly helped SVB’s bond portfolio.

The Federal Reserve meets again next week, and the expectations are for a rate increase of 0.25%. Earlier, traders had been expecting an increase of 0.50% but the banking system may be too fragile. Traders also expect to see a few rate cuts later this year. I’m not fully convinced that will happen but it’s not out of the question.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

-

Morning News: March 14, 2023

Posted by Eddy Elfenbein on March 14th, 2023 at 7:00 amJapan Has a Low Risk of a Wage-Price Spiral and That’s a Mixed Blessing

Russia Built $80 Billion Offshore Cash Pile in Year of Sanctions

To Rein in China’s Banks, Xi Uses Familiar Playbook

Inflation Report Arrives as Fed Confronts Bank Failures

Regional Banks Slammed by Fear of a Broader Financial Crisis

Brainard Must Help Contain SVB Crisis She Warned Was Coming

Don’t Call It a Bailout: Washington Is Haunted by the 2008 Financial Crisis

Collapse of Silicon Valley Bank, Signature Bank Calls Fed Interest Rate Path Into Question

KPMG Gave SVB, Signature Bank Clean Bill of Health Weeks Before Collapse

Too-Big-to-Fail Lenders Rake In Deposits After Three Banks Fail

Moody’s Puts First Republic, Five US Banks on Downgrade Watch

First Republic, PacWest Lead US Bank Rebound From Post-SVB Rout

Credit Suisse Finds ‘Material’ Control Lapses After SEC Prompt

Billionaire Charles Schwab’s Fortune Is Slammed by SVB Fallout

Free IRS TurboTax Competitor Is Closer After Biden Funding

Meta Winds Down Support for NFTs on Instagram and Facebook

Uber, Lyft Score Victory as California Court Affirms Right to Treat Drivers as Contractors

Pfizer Agrees to Buy Seagen for $43 Billion

Smithfield Foods CEO Defends Pork Producer’s Chinese Ownership

Be sure to follow me on Twitter.

-

Morning News: March 13, 2023

Posted by Eddy Elfenbein on March 13th, 2023 at 7:03 amHSBC Buys SVB’s UK Unit for £1 in Reprieve for Tech Sector

Italy Says Hopes EU Acts to Shore Up Banks If Needed, After SVB Collapse

Regulators Face Urgent Task to Stem Spread From Silicon Valley Bank

Fed’s New Backstop Shields Banks From $300 Billion of Losses

Regulators Close Another Bank and Move to Protect Deposits

Signature Bank Seized by Regulators as Pain Spreads From SVB

SVB’s Failure Exposes Lurking Systemic Risk of Tech’s Money Machine

SVB Collapse May Prompt Fed to Go Slow on Rate Hikes

Silicon Valley Bank’s Failure Threatens California Winemakers

Stocks Are Poised to Rise Monday as Regulators Act on Silicon Valley Bank

Used Rolexes Are Beating the Stock Market

Global Economy Gets Tailwind From Falling Energy Prices

Saudi Aramco Posts Record $161 Billion Profit for 2022

Four Takeaways as Oil Giant Saudi Aramco Reports a Huge $161 Billion Profit

An A.I. Start-Up Boomed, but Now It Faces a Slowing Economy and New Rules

As Economy Falters, China’s New Premier Tries to Boost Business Confidence

How Beijing Boxed America Out of the South China Sea

Gen Z Spending Gets Supercharged by Inflation and Wage Growth

A Supermarket Megamerger Will Redefine What You Buy at the Grocery Store

Chick-fil-A Wants to Serve Its Chicken Sandwiches in Asia and Europe

SAP-controlled Qualtrics accepts $12.5 Billion Offer from Silver Lake, CPPIB

MLB to Stream Games for Free Amid Looming Diamond Sports Bankruptcy

Be sure to follow me on Twitter.

-

Morning News: March 10, 2023

Posted by Eddy Elfenbein on March 10th, 2023 at 7:02 amBank of Japan Keeps Low Rates as Kuroda Sticks to Script at Swan Song Meeting

ASML, China Customers Haunted by Uncertainty on New Dutch Chip Export Rules

Biden and E.U. Leader to Discuss Ukraine and Trade Spat

Traders Run for Cover as US Banking Woes Spur Haven Demand

SVB Races to Prevent Bank Run as Funds Advise Pulling Cash

Ackman Says US Should Mull SVB Bailout as Possible Option

Stocks Will Be Stuck on Fed Until Recession Is Evident, BofA Says

Falling Survey-Response Rates Undermine Economic Data

Missing From Biden’s Budget: His Plan for Social Security

More Retiree Health Plans Move Away From Traditional Medicare

Jobs Data Poses Extra Market Risk as Bank Funding Drama Unfolds

The Promise of Higher Pay Woos MBAs, Yet Earnings Haven’t Kept Up With Inflation

Elon Musk Is Planning a Texas Utopia—His Own Town

Disney’s Robert Iger Hints at Raising Streaming Prices

New Drugs for Cancer, Rare Disease Can Now Cost More Than $20,000 a Month

General Motors Is Offering Buyouts in an Effort to Cut $2 Billion in Costs

More Than $70 Billion Wiped Off Crypto Market in 24 Hours as Bitcoin Drops 8% Below $20,000

Disgraced Goldman Banker Roger Ng Gets 10 Years for Helping Steal Over $4 Billion

Be sure to follow me on Twitter.

-

Morning News: March 9, 2023

Posted by Eddy Elfenbein on March 9th, 2023 at 7:00 amAmerica’s $52 Billion Plan to Make Chips at Home Faces a Labor Shortage

How the U.S. Spent $1.4 Trillion in Debt Last Year, Explained With Pennies

Biden’s Budget Would Cut Deficits by $3 Trillion Over 10 Years

CFOs Warily Watch—and Wait—for an Acceleration in Fed Interest-Rate Hikes

Frontier Countries to Suffer Most if Fed Rate Gets to 6%

The Fed’s Struggle With Inflation Has the Markets on Edge

Companies Are Telling Us the Real Reason They’re Still Raising Prices

How ‘Excuseflation’ Is Keeping Prices – and Corporate Profits – High

Biden to Urge 25% Billionaire Tax, Levies on Rich Investors

Even Wealthy Landlords Are Skipping Payments on Office Buildings

Silvergate Bet Everything on Crypto, Then Watched It Evaporate

Baidu Scrambles to Ready China’s First ChatGPT Equivalent Ahead of Launch

Where Musk’s Twitter Gambit Stands, Nearly Five Months In

Instagram Founder Says the Time Has Come for a New Social Network

The Perils of Working on a C.E.O.’s Pet Project

Executives Lose a Coveted Status Symbol—Their Assistants

How One Guy’s Car Blog Became a $1 Billion Marketplace

Adidas Profit Falls 83% After Split With Yeezy

Be sure to follow me on Twitter.

-

Morning News: March 8, 2023

Posted by Eddy Elfenbein on March 8th, 2023 at 4:49 amChina’s Financial Regulatory Revamp Raises Hope, Some Concern Over Control

London Bankers Hope for Brexit Thaw After Northern Ireland Deal

Fed Chair Opens Door to Faster Rate Moves and a Higher Peak

Oil Extends Declines on Rate Hike Concerns

Global Investors Contemplate Fallout From US Rates Reaching 6%

Deepest Bond Yield Inversion Since Volcker Suggests Hard Landing

Citadel’s Griffin Sees Setup for US Recession After ‘Traumatic’ Inflation

Biden’s Plan to Avert Medicare Funding Crisis Includes Tax Hikes

SoFi Bank Sues to Block Biden’s Student Loan Payment Pause

Justice Dept. Sues to Block JetBlue’s Acquisition of Spirit

F.T.C. Intensifies Investigation of Twitter’s Privacy Practices

How Google Became Cautious of AI and Gave Microsoft an Opening

Credit Suisse Obtains Key Approval to Launch Wealth Business in China

Bank of America CEO Says ‘We Are Capitalists’ as Anti-ESG Critics Gain Steam

Walgreens Faces Blowback for Not Offering Abortion Pill in 21 States

Hershey Unveils Plant-Based Reese’s Cups, Chocolate Bars — That Cost More

Sold-Out Girl Scout Cookie Flavor Hits the Resale Market

It Turns Out Money Does Buy Happiness, At Least Up to $500,000

Be sure to follow me on Twitter.

-

CWS Market Review – March 7, 2023

Posted by Eddy Elfenbein on March 7th, 2023 at 6:51 pm(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

There’s a classic bit from the original Saturday Night Live cast where they parody the Carter-Ford presidential debates from 1976.

During the skit, Jane Curtin, as one of the panelists, asks a very wonkish question alluding to several facts and figures. Chevy Chase, as President Ford (who doesn’t bother trying to look like the president), appears completely bewildered and famously responds, “it was my understanding that there would be no math.”

I mention this because the question Jane Curtin asks has to do with the Humphrey-Hawkins Act, which at the time was only a bill.

Today, it’s a law and its official name is the Full Employment and Balanced Growth Act of 1978. The act is more informally known for its two major sponsors, Congressman Augustus Hawkins and Senator Hubert Humphrey. The act was signed into law a few months after Humphrey died.

The act has an interesting history because it started out as a classic Keynesian bill that aimed for full employment. Instead, the final bill was stripped of those provisions, and it was given a Friedmanite flair. For example, the act requires the Fed to outline its targets for monetary aggregates.

Another mandate of Humphrey-Hawkins is that the Chairman of the Federal Reserve must testify before Congress twice a year on monetary policy. Each testimony lasts two days, one day each before the House Financial Services Committee and the Senate Banking Committee.

Several years ago, I went to the Senate hearing to see the festivities live. I was surprised to find that except for the senators and a few cameramen, the room was nearly empty. I even got the seat directly behind Chairman Bernanke.

Today, Jerome Powell gave his Humphrey-Hawkins testimony before the Senate Banking Committee. In his remarks, Powell said that interest rates will likely go higher than the central bank had expected. The big change is that inflation appears to have reversed its direction and it may be accelerating again.

“The latest economic data have come in stronger than expected, which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated,” Powell said in remarks prepared for two appearances this week on Capitol Hill. “If the totality of the data were to indicate that faster tightening is warranted, we would be prepared to increase the pace of rate hikes.”

Home prices appear to be one of the few areas where prices are going down. This news is especially difficult for the Fed because it had recently downshifted to 0.25% rate hikes. That was seen as a sign that the Fed was winning the battle against inflation. Now that’s in doubt.

In December, the Fed updated its economic projections. At the time, the Fed saw interest rates peaking at 5.1%. In fact, Wall Street thought the Fed was being unduly alarmist. Not anymore. Now traders think the Fed was too optimistic.

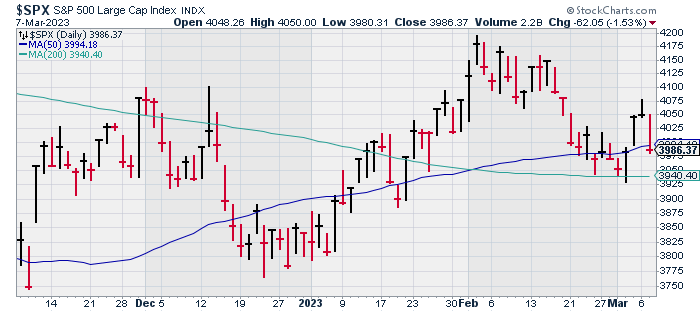

Interestingly, Powell didn’t specify how high he thinks rates could go but his remarks had an immediate impact on the market. The two-year Treasury yield broke above 5% for the first time since 2007. Yesterday’s traders thought the odds of a 0.5% hike at the Fed’s next meeting (in two weeks) was 31%. Now it’s up to 70%.

After that, traders expect two more 0.25% increases, one in May and another in June. Traders then expect the Fed to hold tight through the end of the year. There are even some bets that the Fed will start cutting early next year.

I should caution that the futures market is merely a mass of traders placing bets on the future. There are no guarantees, but it’s interesting to note that the perceived ceiling for interest rates keeps rising.

I often talk about the 2/10 Spread because it has a good historical track record in predicting recessions. Today, the 2/10 Spread dropped below -100 basis points. The two-year Treasury now yields more than 1% over the 10-year Treasury. This hasn’t happened in 42 years.

The stock market did not take the Powell news well. At its low, the Dow lost 593 points. The S&P 500 lost over 1.5% today and the index closed below 4,000. The banks got hit especially hard today. The S&P 500 Financial Index lost 2.54% today.

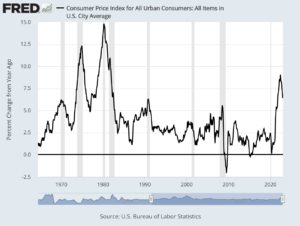

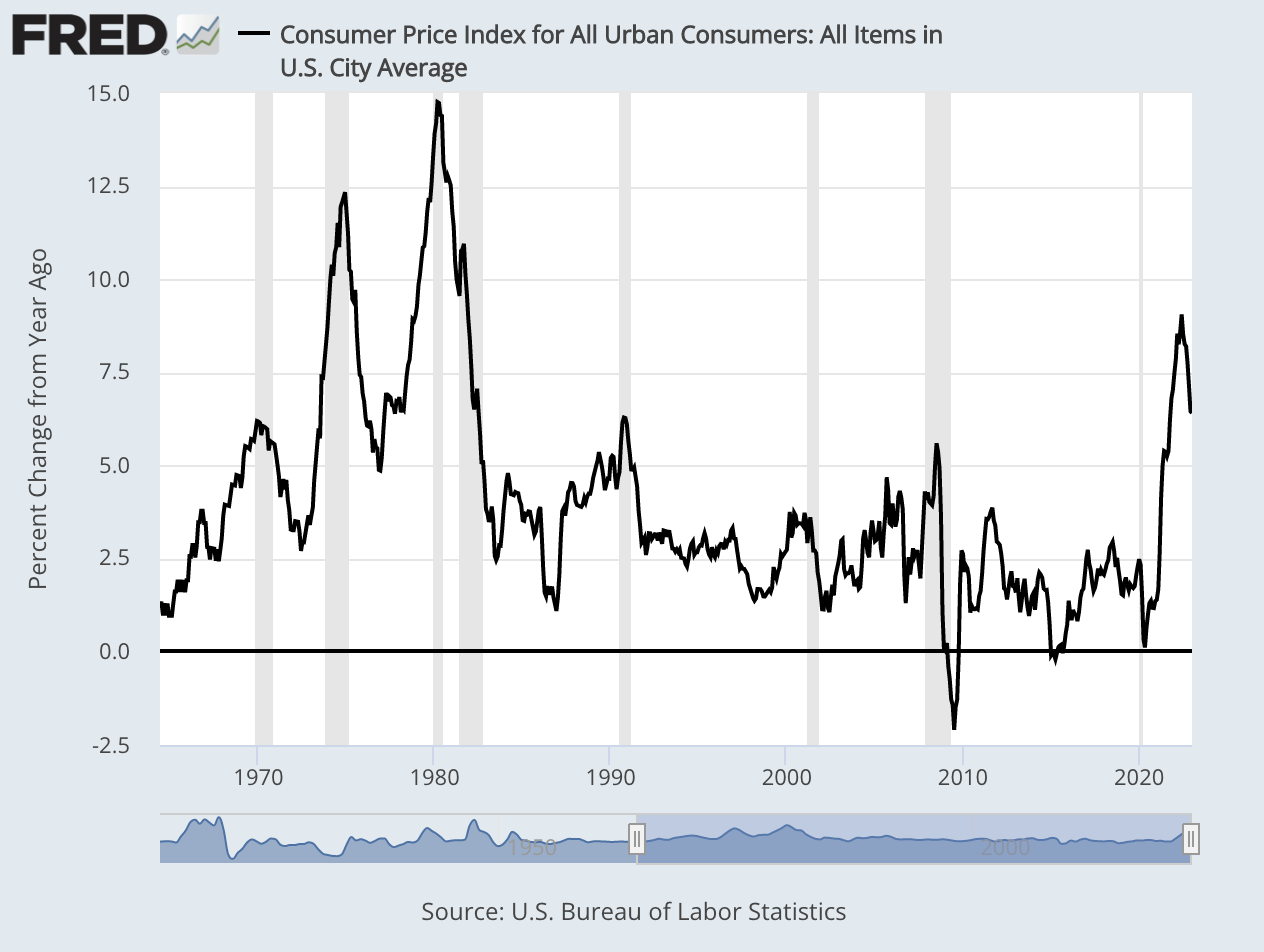

I need to stress how dangerous inflation is for investors. The recrudescence of inflation is the most important obstacle Wall Street currently faces. A depreciating currency may appear beneficial in the short-term, as anyone who remembers the 1970s can attest, but it’s eventually very destructive. In 1977, Warren Buffett wrote an essay on this subject called, “How Inflation Swindles the Equity Investor.”

For businesses, inflation has an unusual impact on the bottom line. Bear in mind that not all earnings are the same. Inflation exacts a heavy toll on asset-heavy businesses. Inflation has an impact similar to putting a magnet near a compass. Everything gets a little screwy. For example, companies with high assets relative to their profits tend to report ersatz earnings.

At first, inflation gives the illusion of prosperity. Businesses create their products in fewer and more expensive dollars and then sell them for cheaper dollars and more numerous dollars. As an accounting item, the business may appear more profitable, but no wealth has been created.

Inflation also favors the debtor in favor of the creditor. Again, any benefit is short-lived. In fact, once lenders see the impact of inflation, the ultimate outcome is to price the marginal borrower out of the credit markets.

Stocks have historically not performed well during periods of high inflation. Inflation is, at root, a tax on capital. In the late 1970s, the stock market’s P/E Ratio dropped well below 10. I don’t even want to think we could return to those kinds of valuations. It’s no accident that Walmart was such a big winner during the 70s since it was so focused on giving shoppers lower prices.

Professor Robert Shiller, a Nobel prize winner, maintains an online database of historical market data. It goes back 150 years. A few years ago, I went through the numbers to see how the stock market has responded to differing levels of inflation.

The stock market has performed well up until inflation gets to about 7%. Anything above that, and the stock market gets ugly. The math isn’t hard. Equity prices are squeezed on two ends. Inflation causes interest rates to rise and that makes for higher borrowing costs. Also, equity valuations are discounted at a higher rate, which translates to lower earnings multiples.

Things may get more dramatic soon. The February jobs report is due out this Friday. Wall Street’s consensus is that the U.S. economy added 250,000 net new jobs last month. After that, the February CPI report comes out next Tuesday.

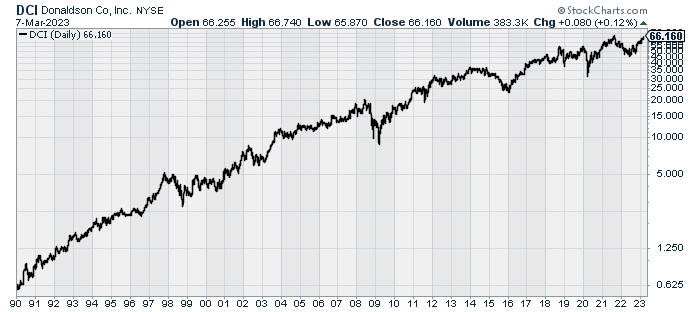

Stock Focus: Donaldson

This week, I want to feature Donaldson (DCI). This was a former Buy List stock that I stupidly let get away. Since 1990, shares of DCI are up more than 10,800%.

Donaldson is in the filtration biz which is one of those areas that few people ever think about, but it’s a lot bigger than you might imagine. The company was founded by Frank Donaldson in 1915 and it’s based in Minneapolis, MN.

Donaldson currently has a market value of about $8 billion. It’s a member of the S&P 400 Mid-Cap Index. A few Wall Street analysts follow it, but not many. In the last 35 years, Donaldson has split its stock 2-for-1 five times and once 3-for-2. That works out to 48-for-1.

Last week, Donaldson reported fiscal Q2 earnings of 75 cents per share. That was two cents more than estimates. Donaldson also narrowed its full-year guidance to a range of $2.99 to $3.07 per share. That’s an increase of eight cents to its low end. The company has already made $1.50 per share for its first two quarters. Donaldson expects sales to rise by 2% to 6% this year.

Donaldson currently pays out a dividend of 23 cents per share. The company has increased its dividend for 27 consecutive years. In 1987, DCI paid out a dividend of about one-third of a penny per share.

Wall Street expects DCI to earn $3.17 per share next year. That means the stock is going for just under 21 times next year’s earnings. That’s not bad.

Donaldson reminds me of Peter Lynch’s advice to find companies that are boring. They sound boring. The product is boring and industry is boring. I’d rather not have to wince each time the CEO decides to tweet something.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

-

Morning News: March 7, 2023

Posted by Eddy Elfenbein on March 7th, 2023 at 7:06 amIran’s Rulers, Shaken by Protests, Now Face Currency Crisis

China Jan-Feb Trade Slumps Again as Global Demand Falters

European Bonds Get a Respite From Softer Inflation Expectations

Roubini Fears Hard Landing Amid Persistent Global Inflation

Why the Federal Reserve Won’t Commit

Why the Recession Is Always Six Months Away

Biden Proposes Tax Hike on Income Over $400,000 to Fund Medicare

The Debt Ceiling Is the Risk Wall Street Doesn’t Want to Think About

Debt Default Would Cripple U.S. Economy, New Analysis Warns

US Payrolls Have Beat Forecasts 10 Straight Months. What’s Next?

How Seasonality Affects Our View of Inflation and Jobs, as Explained With Hot Dogs

Grayscale-SEC Fight Could Clear the Way for Anybody to Speculate on Bitcoin

A Bank President Who Embraces the Unconventional

JPMorgan Is Growing in Florida and Texas, States That ‘Like Business,’ Dimon Says

U.S. to Challenge Mexican Ban on Genetically Modified Corn

A Mega Airline Merger Hits Turbulence

How Lego Beat Barbie and Monopoly

Adidas Could ‘Literally Burn’ $500 Million in Unsold ‘Yeezy’ Apparel

Be sure to follow me on Twitter.

-

Morning News: March 6, 2023

Posted by Eddy Elfenbein on March 6th, 2023 at 7:04 amMissing Banker Reignites Fear of Xi Among China’s Tech Bosses

World’s Riskiest Markets Stumble Into Crisis With Dollars Scarce

Chinese Companies Hang Onto Dollars, Hedge to Prepare for Volatile Yuan

Japan Piled Back Into U.S. Treasurys This Year. Investors Worry It Won’t Last

Republican Votes Helped Washington Pile Up Debt

Powell Set to Lay Groundwork for Higher Rates on Capitol Hill

Fed’s Rate Moves Put Manufacturing Sector at Risk

The Paul Volcker Narrative Imagines an Economy That Doesn’t Exist, and That Never Has

Holding Cash Will Be a Winning Strategy in 2023, Investors Say

Billion-Dollar Power Lines Finally Inching Ahead to Help US Grids

The Trillion-Dollar Debate Over Share Buybacks

Credit Suisse Loses One of Its Biggest Backers

EVs Boost Chip Demand Despite Semiconductor Makers’ Woes

Here’s How Much $1,000 Invested In Tesla Will Be Worth If Cathie Wood’s 2026 Price Target Comes True

Housing Market Momentum Stalls as Critical Spring Season Approaches

Bars, Hotels and Restaurants Become the Economy’s Fastest-Growing Employers

You’re Now a ‘Manager.’ Forget About Overtime Pay.

What Is a CEO’s Pay Actually Worth?

How Chili’s Is Prepping for Tough Times, Starting With the Fries

Toblerone Chocolate Is No Longer ‘Swiss’ Enough for Alps Logo

Be sure to follow me on Twitter.

-

Morning News: March 3, 2023

Posted by Eddy Elfenbein on March 3rd, 2023 at 7:02 amHow Gas From Texas Becomes Cooking Fuel in France

Nigeria’s Supreme Court Orders Halt to Cash Replacement Policy

Rules to Curb Illicit Dollar Flows Create Hardships for Iraqis

What Wall Street Gets Wrong About Xi Jinping’s New Money Men

Academic Fight Erupts Over Measuring the West’s Pressure on Russian Economy

The World Economy Is Doing Well—This Is Bad News for Central Bankers

Fed Official Says Hotter Data Will Warrant Higher Rates

Clueless Wall Street Is Racing to Size Up Zero-Day Options Boom

Investors Shore Up Stablecoins as Silvergate Exodus Worsens

iPhone Maker Plans $700 Million India Plant in Shift From China

Office Mandates. Pickleball. Beer. What Will Make Hybrid Work Stick?

Zoom Abruptly Fires President Greg Tomb ‘Without Cause’

Key American Allies Aren’t Following Governmentwide TikTok Bans

Why Barnes & Noble Is Copying Local Bookstores It Once Threatened

Nordstrom to Close All Its Canadian Stores, Lay Off 2,500 Workers

Adani Shares Surge After $1.87 Billion GQG Investment; More Road Shows Lined Up

Ericsson to Pay About $207 Million After DOJ Finds It Breached Deal

Be sure to follow me on Twitter.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His