-

A Few Words on Executive Compensation

Posted by Eddy Elfenbein on May 8th, 2013 at 3:00 pmThe topic of executive compensation receives a lot of attention in the financial media, and I think much of it is misguided. As an investor, I’ve looked at countless companies, and I can’t remember an instance where the level of executive pay has steered me away from the stock.

From my experience, investors are perfectly willing to put up with just about anything from a CEO as long as the stock is rising. Of course, that’s a big “as long as.”

There seems to be a built-in cynicism with many investors, and they’re predetermined to believe that the executives are looting the company at their expense. Human nature being what it is, yes, Enrons do exist. However, I prefer to focus on high-quality companies so the management has almost certainly proven themselves to be efficient by the time I look under the hood.

A few years ago, I was at the Wharton Economic Summit and one professor said that if we magically chopped the pay of every CEO by 25%, it would have almost no impact on market valuations. It’s simply not that big a portion of expenses.

I’m also afraid that many companies have reformed themselves backward. Since large cash payments don’t look good for senior managers, especially for a money-losing company, we’ve moved to a world of stock options. That had the added benefit of managers having, to borrow a tired phrase, “skin in the game.” But for me, as an investor, I hate the endless watering down of shares.

Plus, stock options aren’t the independent variables they’re made out to be. They’re great to use for companies with rising share prices. Hey, it’s free money! Here are some more grants! But when the shares start dropping, it’s not so much fun.

Executive compensation also distorts how much management really has at stake. I’m obviously a big fan of AFLAC and the company got tons of great press for their say-on-pay measure. Sure, that’s nice, but how important is it really? The Amos family has a fortune tied to shares of AFLAC. What Dan Amos takes in each year as CEO is probably pretty small compared to what he and his family have at stake. Mind you, I’m not criticizing him. I’m just saying let’s look at the big picture. He’s already rich and if next year’s pay is $3 million or $6 million, it won’t impact his life very much.

The problem is that any metric a board uses to base executive compensation will create problems. If they say that the CEO will get a bonus of, say, $5 million if ROE for the year hits, say, 18%, then the CEO will do whatever it takes to make the accounting work. The same for EPS or revenue growth – it doesn’t really matter. The benefit for the board is that their decision seems far more rational and dispassionate than it truly is. Well, it’s not.

If I had my way, the board would be in complete control of executive pay and they would decide by fiat each year. No formulas or stock options. Simply, here’s how well we think you did, and that’s that. For untested companies I see the drawbacks, but for successful ones, I think it’s better for everyone, especially shareholders.

Which brings me to another point. While I’m not so bothered by executive pay, I am bothered by the lack of independence of corporate boards. Their job is to represent shareholders, and far too many are lackeys for kingpin CEOs. It’s taken me a long time to reach this point but I don’t believe any CEO should be on the board of directors. None. Just cut the two entities entirely. CEOs should not be media celebrities.

Jamie Dimon at JPMorgan Chase is a perfect example, and I say this as someone who has JPM on their Buy List. Mr. Dimon should be CEO or on the board, but not both. My preference is to see him leave the CEO suite.

-

Cognizant Beats and Guides Higher

Posted by Eddy Elfenbein on May 8th, 2013 at 10:02 amThe S&P 500 has now risen for 11 of the last 13 days. We had more good news this morning as Cognizant Technology Solutions ($CTSH) reported impressive results. For Q1, CTSH earned $1.02 per share which was eight cents better than estimates. Going into the earnings report, I think some traders were expecting a big miss after seeing what happened to CTSH’s competitors. Revenues rose 18.1% to $2.02 billion which was just ahead of estimates.

Cognizant’s guidance was also good. For Q2, they see earnings at $1.06 per share which is seven cents above Wall Street, and they expect quarterly revenues of $2.13 billion which is $20 million above consensus.

For all of 2013, CTSH expects earnings of $4.31 per share which is well above consensus of $4.05 per share. For revenue, they expect $8.60 billion which just below the Street’s forecast of $8.63 billion. The company is also expanding its stock buyback program.

The stock gapped up to $68 right after the opening, then pulled back, and is climbing again. CTSH is currently up 3.8% today.

-

Warren Buffett in 1962

Posted by Eddy Elfenbein on May 8th, 2013 at 9:18 am -

Morning News: May 8, 2013

Posted by Eddy Elfenbein on May 8th, 2013 at 7:19 amChina Reports Stronger April Trade Growth

European Telco Revenues Drop As Price Wars Heat Up

PBOC Signals Resumption of Bill Sales as Capital Inflows Rise

ING Will Accelerate Sale of European Insurer as Profit Rises

U.S. Brings Charges In First Criminal Case For Consumer Agency

Hedge Funds Rush Into Debt Trading With $108 Billion

Toyota Full-year Net Profit Triples to $9.7 Billion

Deutsche Telekom Earnings Top Estimates on German Wireless

Stanchart Sees Q1 Profit Decline On Increased Costs

Whole Foods 2nd-Quarter Profit Rises; Raises Outlook, Announces Stock Split

Yahoo CEO Mayer Said to Seek Ways to End Microsoft Search Deal

Symantec Forecasts Weak Results As Yen Depreciates

Solid Sales, and Criticism, for Latest Version of Windows

Phil Pearlman: Reflexivity and the Employment Numbers

Howard Lindzon: The ‘Eclectic Opportunist’…and My Tesla Investment/Trade

Be sure to follow me on Twitter.

-

Strong Earnings at CA Technologies

Posted by Eddy Elfenbein on May 7th, 2013 at 10:44 pmFor the first time ever, the Dow closed above 15,000. This was the 17th-straight Tuesday rally for the index. The Dow closed today at 15,056.20. The S&P 500 rose 0.52% to close at 1,625.96. This was also another all-time high close.

The cyclicals once again led today’s rally. Interestingly, the tech-heavy Nasdaq was only up 0.11% today while the Nasdaq 100 was slightly negative.

Our Buy List did well today thanks largely to DirecTV ($DTV). The good earnings report propelled the shares to a 6.9% gain today. Bed Bath & Beyond ($BBBY) finally broke through $70 per share today. That hasn’t happened since September.

After the bell, CA Technologies ($CA) reported fiscal fourth-quarter earnings of 68 cents per share. This was well above Wall Street’s forecast of 55 cents per share.

“While we were able to achieve GAAP and non-GAAP diluted earnings growth for the year, we know we can do better to drive new sales and revenue performance,” said Mike Gregoire, CA Technologies chief executive officer. “When I look at the significant assets at CA Technologies, I believe there is an opportunity for us to improve our performance by stronger focus on product innovation, leveraging customer relationships and better execution in new customer adoption.

“The traditional ways we’ve looked at systems, data, applications and security are being challenged by disruptive technologies like Mobility, Cloud, SaaS and Big Data. Businesses have higher expectations from IT, demanding far greater speed and agility and anytime, anywhere secure connectivity. These are areas where CA has expertise and can help,” he continued. “To better meet this customer demand, today we announced a plan and corresponding charge of approximately $150 million for fiscal year 2014 that will enable us to rebalance our resources to drive greater innovation and collaboration in product development and greater efficiency and better sales execution.”

For 2014, the company expects to earn between $2.35 and $2.43 per share. Wall Street had been expecting $2.53 per share, and the stock is down after-hours. However, I’m not sure if CA’s forecast includes the $150 million charge mentioned above. By my calculation, that’s 33 cents per share pre-tax.

-

The Battle at Ebix

Posted by Eddy Elfenbein on May 7th, 2013 at 3:56 pmThere’s an interesting battle going on at the company Ebix ($EBIX). Goldman Sachs recently offered to buy the company for $20 per share and the board said yes. Some shareholders are fighting back claiming the price is far too low. I have to agree. The price is too low.

Even putting the valuation argument aside, there should be far greater pushback from investors on these types of mergers. I don’t believe the majority of acquisitions are to the benefit of shareholders (for either party). The Sprint-Dish merger seems to be an obvious mistake. With Ebix, they have to wait 45 days for a counter-offer. I doubt one will come. Who wants to piss off Goldman?

The Ebix story gets more interesting because the company is being investigated the SEC due to “accounting issues.” Yeah, that’s not good.

Interestingly, the first event that took down shares of Ebix was a posting at Seeking Alpha two years ago under the name Copperfield Research. Since then, it’s been one long headache for Ebix. There have been accusations and denials, and I can’t keep it straight.

Sorry to sound conspiratorial, but this sounds like a good time for a board to sell out at any price. If Ebix is private, then who cares about their accounting, right? My assumption is that Goldman is a lot less dumb than they are evil.

-

Note to Some Intrepid Journalist

Posted by Eddy Elfenbein on May 7th, 2013 at 2:58 pmIt’s not exactly a secret that Janet Yellen will most likely become the next chairman (chairperson?) of the Federal Reserve. Yellen has a long and distinguished career which includes stints at the Fed, the Council of Economic Advisors and many years in academia, first at Harvard and later at Berkeley. She’s also married to George Akerlof, a Nobel Prize-winning economist.

Here’s a listing of her articles and academic papers going back nearly forty years. It’s an impressive body of work. She was addressing the topic of long-term unemployment long before that became a topic of conservation among policy elites.

There is, however, one paper that Yellen wrote that seems quite different from much of her other work. In 1996, she and Akerlof wrote, “An Analysis of Out-of-Wedlock Childbearing in the United States.” I believe that’s the only time she has addressed that subject in depth.

Abstract:

This paper relates the erosion of the custom of shotgun marriage to the legalization of abortion and the increased availability of contraception to unmarried women in the United States. The decline in shotgun marriage accounts for a significant fraction of the increase in out-of-wedlock first births. Several models illustrate the analogy between women who do not adopt either birth control or abortion and the hand-loom weavers, both victims of changing technology. Mechanisms causing female immiseration are modeled and historically described. This technology-shock hypothesis is an alternative to welfare and job-shortage theories of the feminization of poverty.

At the time the paper was written, that was a hot topic. There was a lot of talk about the root causes of poverty and what to do about welfare. That year, Bill Clinton signed the Welfare Reform Act. Well, 1996 was a long time ago and now we know a lot more about effects of out-of-wedlock births.

I haven’t read the paper, but I’m curious…were they right?

-

DirecTV Crushes Earnings

Posted by Eddy Elfenbein on May 7th, 2013 at 9:58 amExcellent news today for DirecTV ($DTV). The company absolutely demolished its earnings report. For Q1, DTV earned $1.43 per share which was 33 cents better than Wall Street’s forecast. The earnings were higher than all 18 forecasts made by analysts on Wall Street. Revenues rose 7.6% to $7.58 billion which was $50 million better than estimates.

Once again, Latin America was the key to DTV’s success. Subscriber count grew by 583,000 in that region and there are now 16 million subscribers in Latin America. They’re not doing so badly in North America either. DTV added 21,000 subscribers in the U.S.

I’ve often highlighted DTV as a company that does share repurchases right. Last quarter, they bought back $1.38 billion worth of their shares. The stock closed yesterday at $57.96. It’s been as high as $61.50 this morning, which is a 6.1% gain. Right now, it’s hanging in at $60.36, which is a 4.1% gain.

-

Morning News: May 7, 2013

Posted by Eddy Elfenbein on May 7th, 2013 at 6:44 amIMF’s Lagarde Urges All Euro Members To Push For Banking Union

China Names Yuan Convertibility Plan as Goal This Year

Senate Passes Online Sales Tax 69-27 But You Can Avoid It For Now

King Coal Losing Crown as U.S. Gains Energy Independence

HSBC Says Quarterly Profit Almost Doubles on Cost-Cutting

Munich Re First-Quarter Profit Jumps Led by Reinsurance Revenue

Facebook Still Worth Probably No More Than $25 A Share: Barron’s

Commerzbank Posts Second Quarterly Loss on Staff Reductions

Baidu Buys PPS Online Video Business to Contend With Youku Tudou

YouTube Is Said to Plan a Subscription Option

Facing Black Market, Pfizer Sells Viagra on Web

DirecTV Spurns Dish’s View That Wireless Is Satellite-TV Savior

Jeweler Agrees To Plead Guilty In KPMG Insider-Trading Case

Edward Harrison: How Bond Market Vigilantes Force Rates Higher

Cullen Roche: What’s Unique About Monetary Realism?

Be sure to follow me on Twitter.

-

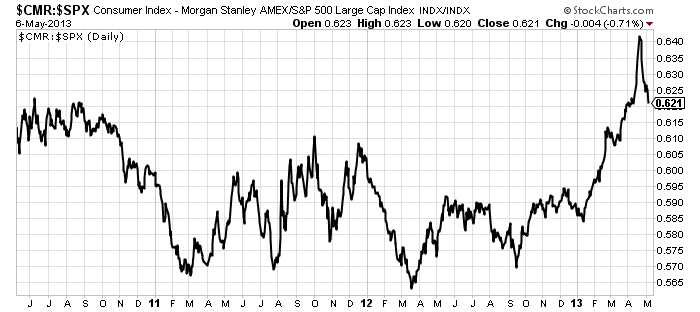

The Strength of Consumer Stocks

Posted by Eddy Elfenbein on May 6th, 2013 at 11:24 pmHere’s an interesting chart. This is the Morgan Stanley Consumer Index ($CMR) divided by the S&P 500.

The CMR is heavily defensive although it’s not an exact match for a defensive index. The consumer names have performed very well this year, although since April 19th, their relative performance has suffered a dramatic turn back. It’s unusual, but not unheard of, for defensive stocks to lead a rally. The post-election rally seems to have continued in stride with a quick change in leadership. The change occurred just after the big plunge in gold.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His