-

Dow 15,000

Posted by Eddy Elfenbein on May 3rd, 2013 at 10:25 amIt just happened.

The Dow first closed above 150 on October 20, 1925, and above 1,500 on December 11, 1985.

-

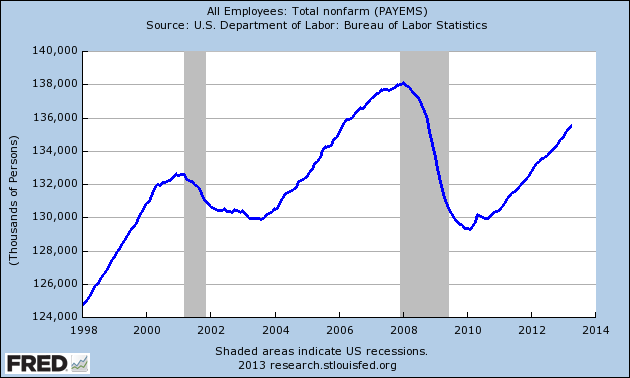

April NFP = 165,000

Posted by Eddy Elfenbein on May 3rd, 2013 at 9:25 amThe April jobs report is out and the economy created 165,000 jobs last month. The unemployment rate dropped to 7.5%. But what really caught everyone’s attention were the big revisions to the numbers for February and March. February’s NFP was revised higher from 268,000 to 332,000, and March went from 88,000 to 138,000. That’s a total of 114,000 jobs in revisions. The stock market looks to open higher today.

-

CWS Market Review – May 3, 2013

Posted by Eddy Elfenbein on May 3rd, 2013 at 8:31 am“They say you never go broke taking profits. No, you don’t. But neither do

you grow rich taking a four-point profit in a bull market.” – Jesse LivermoreI’m starting to feel a bit sorry for the bears. All the headlines have been in their favor (Debt Ceiling! Fiscal Cliff! Cyprus!), but stock prices don’t seem to be cooperating. On Thursday, the S&P 500 closed at—I hope you’re sitting down—yet another all-time high. April marked the index’s sixth consecutive monthly gain, and we’ve rallied for ten of the last eleven months.

But I have to confess that I’m starting to grow more cautious about this rally. We’ve gone a long way up so we’re probably due for bumps soon. Mind you, I don’t think we’re anywhere close to the danger zone. Instead, I think we’ll see more subdued gains for the rest of the year.

Fortunately, our style of investing doesn’t rely on broad market predictions. Trust me, those “forecasts” are a sucker’s game. Instead, we focus on good stocks going for favorable prices. Just look at our two top-performing stocks this year, Bed Bath & Beyond and Microsoft. Both are excellent examples of how we profited by picking good stocks when the market had soured on them.

In the February 22nd issue of CWS Market Review, I highlighted Microsoft ($MSFT) as an exceptionally good buy. Since then, the software giant has climbed more than 20%, and it just touched a five-year high. This week, I’m raising my Buy Below on MSFT to $35 per share.

In our February 15th issue, I said that Bed Bath & Beyond ($BBBY) was finally looking cheap. The stock has since rallied 18%, and it’s close to cracking $70 per share. This week, I’m raising my Buy Below on BBBY to $72 per share.

The lesson isn’t that every beaten stock eventually goes up. It’s that high-quality stocks that have been beaten down have a very good chance of going back up. Make sure your portfolio has enough of these, and you’re tilting the odds in your favor. That’s the heart of all sound investing.

In this week’s issue of CWS Market Review, I’ll cover our recent Buy List earnings reports and highlight the last batch for next week. Before I get to that, let’s look at how the market has been behaving recently.

The Market’s Leadership Has Changed

The stock market has responded well since its recent low on April 18th. The S&P 500 has rallied for eight of its last 10 days. What’s interesting is that up until the 18th, many of the defensive sectors had been leading the market. By defensive, I mean sectors like healthcare, consumer staples and utilities. That’s rather usual, but not unheard of. Typically, cyclical stocks lead the rallies, and defensive stocks take charge when the market sours (meaning, they fall the least).

So what’s going on? My take is that the recent rout of commodities, gold in particular, helped give the lead to defensive sectors. Energy and Material stocks have been laggards this year. I don’t think we can say yet whether this is a precursor of a broad decline in the economy, but it’s true that some of the recent economic data has been weak. The jobs report for March was lackluster, and last Friday’s GDP was decent but far from strong. But those reports covered periods earlier this year. We’re now well into Q2 and since April 18th, the market has been rallying on strength from cyclical stocks. Technology has been particularly strong.

The Federal Reserve’s policy statement this week specifically said that “fiscal policy is restraining economic growth.” The Fed also said that it may increase or reduce its bond buying to help the economy. I take this to mean that rates will remain very low. As a result, the math continues to be very favorable for stocks. Stocks may be less cheap but they’re still a lot cheaper than bonds. Just look at Apple. The company made news this week with its massive bond offering. Apple was able to issue five-year bonds with a negative real interest rate. Apple’s dividend yield is higher than their cost to borrow, so it wouldn’t make sense not to borrow.

What to do now: Investors should concentrate on high-quality stocks and particularly those that pay generous dividends.

Good News from Harris, Bad News from WEX Inc.

Last Friday, Moog ($MOG-A), the maker of flight control systems, reported first-quarter earnings of 80 cents per share which was two cents better than analysts’ estimates. The CEO said that the first half of this year has been difficult but the second-half should be better for them.

Moog now sees full-year earnings coming in between $3.40 and $3.50 per share but that includes a 15-cent charge for restructuring costs. Not counting the restructuring charge, this is an increase in their guidance. Originally, Moog said they saw full-year earnings ranging between $3.50 and $3.70 per share. Then they took the top end down to $3.60 per share. Now Moog sees earnings, without the charge, between $3.55 and $3.65 per share. This was a good quarter for them. Moog remains a solid buy up to $50 per share.

After the closing bell on Tuesday, Fiserv ($FISV) reported Q1 earnings of $1.33 per share which was one penny below consensus. Due to the earnings miss, the stock got hit for a 4.5% loss on Wednesday. Fiserv has done very well for us, and last week I cautioned you not to chase it. Honestly, I’m not at all worried about Fiserv. A one-penny miss is meaningless for a company like this. In the short-term, of course, it’s not pleasant, but let’s look at the larger picture.

For last year’s Q1, Fiserv made $1.15 per share so earnings are growing quite nicely. Fiserv’s CEO, Jeffery Yabuki, said the company is “on-track to achieve our targeted results for the year.” For the entire year, Fiserv expects adjusted revenue growth in excess of 10%, and earnings-per-share are expected to rise between 15% and 19% to a range of $5.84 to $6.03. The Street had been expecting $5.97 per share. For now, I’m keeping my Buy Below price at $88 per share.

On Tuesday morning, Harris ($HRS) reported fiscal Q3 earnings of $1.12 per share which matched Wall Street’s estimate. I think this was a big relief for traders who were expecting something much worse. The shares got a nice spike after the earnings report.

The most important news was that Harris reiterated its full-year earnings guidance of $4.60 to $4.70 per share. If you recall, the company originally expected earnings between $5.00 and $5.20 per share but lowered guidance due to the federal government’s sequester. Shares of HRS currently yield 3.2%. I’m raising my Buy Below on Harris to $47 per share.

WEX Inc. ($WEX) is turning into our problem child for the year. The stock got hammered this week after the company lowered its full-year guidance. So what’s causing them trouble? The Maine-based company processes fuel payments for fleet vehicles and they’re being impacted by lower fuel costs and unfavorable exchange rates.

First-quarter earnings came in at 98 cents per share which was two cents better than estimates. The results were also better than the range the company gave us three months ago of 89 to 96 cents per share. That’s the good news.

Their guidance, however, was lousy. For Q2, WEX expects earnings to range between 98 cents and $1.05 per share. That’s well below Wall Street’s consensus $1.11 per share. WEX also lowered their full-year guidance from $4.30 to $4.50 per share to $4.20 to $4.35 per share. The stock dropped over 10% on Wednesday. Frankly, the numbers here are pretty ugly. I’m very disappointed with WEX and I’m dropping my Buy Below down to $70 per share.

Four More Earnings Reports Next Week

Next week is the final big week for our Buy List stocks this year earnings season. On Tuesday, May 7th, CA Technologies and DirecTV are due to report. Cognizant Technology Solutions follows on Wednesday, May 8th. Nicholas Financial should also report next week but I don’t know which day.

CA Technologies ($CA) got off to a great start this year but has pretty much stagnated ever since. In January, I predicted the company would beat earnings, and that’s exactly what happened. On the surface, CA appears to be a dull company, but don’t let that fool you. The stock currently yields just over 4%. Wall Street expects earnings of 55 cents per share. I’m holding my Buy Below at $27 per share.

Shares of Cognizant Technology Solutions ($CTSH) recently shed 21% in two weeks. Traders are clearly nervous that a lousy earnings report is coming. For one, Infosys ($INFY), a similar company to CTSH, gave terrible guidance. IBM ($IBM) also had a big earnings miss. Plus, there are also concerns that new legislation will impact the status of foreign workers. But all of this is speculation. The company hasn’t reported yet. Wall Street currently anticipates earnings of 93 cents per share. My analysis says CTSH should beat that. Last week, I lowered my Buy Below to $70 per share.

Three months ago, DirecTV ($DTV) had a monster earnings report. The satellite TV operator crushed earnings by 28 cents per share. The company said they see earnings for this coming in at $5 or more. I’m not a fan of share buybacks, but DTV is a company that truly uses them to lower the amount of outstanding shares instead of a cover for executive compensation. Wall Street expects $1.09 per share for Q1. On Thursday, DTV hit a fresh 52-week high. DTV is a buy up to $59 per share.

There’s still not a single analyst on Wall Street who follows Nicholas Financial ($NICK) so I can’t say what the earnings estimate is. But I can speak for myself. Honestly, I don’t care what NICK’s bottom line is as long as it’s somewhere close to 45 cents per share (excluding any charges). A few pennies per share here or there don’t matter. What does matter is that they’re business continues to deliver steady earnings.

I also expect an update on the buyout offer. It’s been a while so I’ll be curious to hear what they have to say. Unfortunately, if a buyout offer falls through, which is fine by me, the stock will probably take a short-term hit. Nicholas Financial continues to be a good buy up to $15 per share.

Before I go, I want to raise my Buy Below price for AFLAC ($AFL) to $57 per share. The stock has responded well to its last earnings report. The underlying business continues to do well. On Thursday, AFL got over $55 for the first time in two years. Our patience is starting to pay off.

That’s all for now. Next week is the last big week for earnings. We have four Buy List earnings reports coming. Also, on Tuesday, the Federal Reserve will release its report on consumer credit. Then on Thursday, the Commerce Department will report on wholesale trade. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: May 3, 2013

Posted by Eddy Elfenbein on May 3rd, 2013 at 7:20 amRBS Drops After Operating Profit Misses Estimates

Slovakia Set to Meet Budget-Deficit Ceiling, EU Forecasts

EU Lowers Forecast as Euro Area Heads For Two-Year Slump

Bangladesh Fears an Exodus of Apparel Firms

JPMorgan Caught in Swirl of Regulatory Woes

American Auto Industry Has Best Performance in 20 Years

Dish’s Charlie Ergen on Sprint Offer: We’re Not Going to Lose

Verizon Says Will Not Pay A Premium For Vodafone Stake

Visa’s Fiscal 2nd-Quarter Results Beat Estimates, Shares Gain

Intel CEO-Designate Krzanich Plans Faster Shift to Mobile

GM’s 1Q Profits Of $865M Beat Analysts’ Expectations

Westpac Posts $3.5 Billion Profit

New York Preserves Weapon Against Wall Street In Case Of Ex-AIG Chief

Jeff Carter: Entrepreneurial Hammers in Search of Nails

Phil Pearlman: Facebook Will Remain Patient Before Monetizing Instagram

Be sure to follow me on Twitter.

-

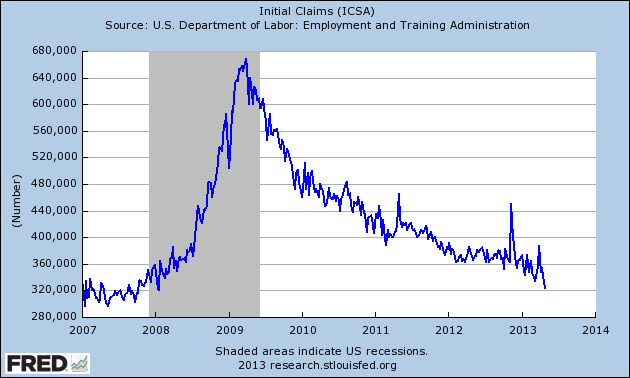

Jobless Claims Fall to a Five-Year Low

Posted by Eddy Elfenbein on May 2nd, 2013 at 12:47 pmTomorrow is the big April jobs report but we got an important piece of data this morning. The government reported that first-time jobless claims fell to 324,000. That’s the lowest number since January 2008. Economists were expecting 345,000.

The consensus for tomorrow’s non-farm payroll is a gain of 145,000. We got a sneak preview yesterday when ADP, the private payroll firm, reported a gain of 119,000 jobs for April.

The stock market is up cautiously today. The S&P 500 hit an intra-day high of 1,597.86 which is just above the high from Tuesday, which was also the close that day. Shares of AFLAC ($AFL) finally broke through $55 per share. Bed Bath & Beyond ($BBBY) is getting very close to hitting $70 per share. The home furnisher has had an impressive run. Two months ago, BBBY was below $57.

Yesterday, Ford ($F) reported an impressive 18% sales gain for April. The Fusion continues to be a big hit for them. The stock got as high as $13.78 yesterday although it pulled back late in the day.

-

Morning News: May 2, 2013

Posted by Eddy Elfenbein on May 2nd, 2013 at 7:39 amHere Comes The Most Anticipated ECB Rate Decision In A Long Time

JGBs Mostly Rise, Underpinned By BOJ Bond-Buying Operations

China Cyberspies Outwit U.S. Stealing Military Secrets

China Data Confirm Slowdown in Factories

Philippines Beats Indonesia to S&P Investment Grade Rating

Some Retailers Rethink Role in Bangladesh

Fed Open to Expanding QE as It Counters Talk of Tapering

Facebook’s Mobile Business Expands In First Quarter

Merck Cuts Profit Forecast as Buyback Boosted $15 Billion

BMW Sticks to 2013 Target After Earnings Exceed Estimates

Siemens Cuts Full-Year Forecast Amid Train, Energy Charges

Demise of Coda Automotive Means Lonelier Electric-Car Owners

Shell Chief Executive Peter Voser To Leave In Surprise Move

Howard Lindzon: We Didn’t Know What We Had…Stock Market Edition

Jeff Miller: April Employment Report Preview

Be sure to follow me on Twitter.

-

Today’s Fed Statement

Posted by Eddy Elfenbein on May 1st, 2013 at 2:01 pmHere’s today’s Fed statement:

Information received since the Federal Open Market Committee met in March suggests that economic activity has been expanding at a moderate pace. Labor market conditions have shown some improvement in recent months, on balance, but the unemployment rate remains elevated. Household spending and business fixed investment advanced, and the housing sector has strengthened further, but fiscal policy is restraining economic growth (shots fired at Congress! – Eddy). Inflation has been running somewhat below the Committee’s longer-run objective, apart from temporary variations that largely reflect fluctuations in energy prices. Longer-term inflation expectations have remained stable.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that, with appropriate policy accommodation, economic growth will proceed at a moderate pace and the unemployment rate will gradually decline toward levels the Committee judges consistent with its dual mandate. The Committee continues to see downside risks to the economic outlook. The Committee also anticipates that inflation over the medium term likely will run at or below its 2 percent objective.

To support a stronger economic recovery and to help ensure that inflation, over time, is at the rate most consistent with its dual mandate, the Committee decided to continue purchasing additional agency mortgage-backed securities at a pace of $40 billion per month and longer-term Treasury securities at a pace of $45 billion per month. The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. Taken together, these actions should maintain downward pressure on longer-term interest rates, support mortgage markets, and help to make broader financial conditions more accommodative.

The Committee will closely monitor incoming information on economic and financial developments in coming months. The Committee will continue its purchases of Treasury and agency mortgage-backed securities, and employ its other policy tools as appropriate, until the outlook for the labor market has improved substantially in a context of price stability. The Committee is prepared to increase or reduce the pace of its purchases to maintain appropriate policy accommodation as the outlook for the labor market or inflation changes. In determining the size, pace, and composition of its asset purchases, the Committee will continue to take appropriate account of the likely efficacy and costs of such purchases as well as the extent of progress toward its economic objectives.

To support continued progress toward maximum employment and price stability, the Committee expects that a highly accommodative stance of monetary policy will remain appropriate for a considerable time after the asset purchase program ends and the economic recovery strengthens. In particular, the Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and currently anticipates that this exceptionally low range for the federal funds rate will be appropriate at least as long as the unemployment rate remains above 6-1/2 percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee’s 2 percent longer-run goal, and longer-term inflation expectations continue to be well anchored. In determining how long to maintain a highly accommodative stance of monetary policy, the Committee will also consider other information, including additional measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial developments. When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent.

Voting for the FOMC monetary policy action were: Ben S. Bernanke, Chairman; William C. Dudley, Vice Chairman; James Bullard; Elizabeth A. Duke; Charles L. Evans; Jerome H. Powell; Sarah Bloom Raskin; Eric S. Rosengren; Jeremy C. Stein; Daniel K. Tarullo; and Janet L. Yellen. Voting against the action was Esther L. George, who was concerned that the continued high level of monetary accommodation increased the risks of future economic and financial imbalances and, over time, could cause an increase in long-term inflation expectations.

-

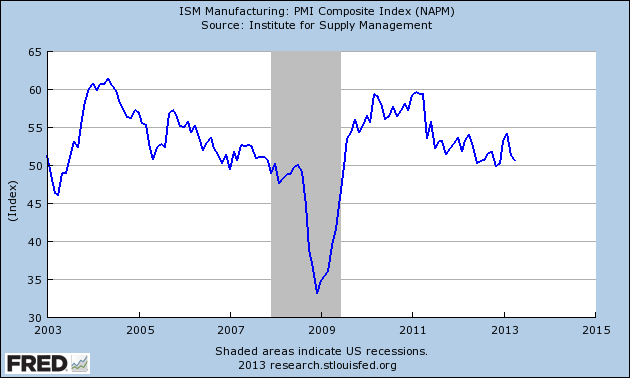

April ISM = 50.7

Posted by Eddy Elfenbein on May 1st, 2013 at 10:12 amThe ISM for April was 50.7 which is down from 51.3 for March. Economists were expecting 50.8. For the 46th month in a row, the ISM has been 49.9 or better.

-

WEX Inc. Reports Earnings of 98 Cents per Share

Posted by Eddy Elfenbein on May 1st, 2013 at 10:01 amWEX Inc. ($WEX) reported first-quarter earnings of 98 cents per share which was two cents better than estimates. Revenue rose 18% to $165.4 million.

“We kicked off 2013 with first quarter revenue and adjusted net income exceeding our guidance, increasing 18% and 8%, respectively, over last year driven by strong transaction growth, exceptional credit loss performance and investments in our business to support future growth,” said Michael E. Dubyak, WEX chairman and chief executive officer. “Year to date we have made strides in executing on all fronts of our multi-pronged strategy. We advanced our international presence within Asia-Pac, Brazil and Europe as a result of investments in WEX Travel, our virtual payment solution for the travel industry, and further diversified our business all while expanding our Americas Fleet business with some marquee wins. With positive momentum in the business and a robust pipeline of opportunities, we have also positioned WEX for future success as we leverage our investments in our burgeoning growth platforms.”

For Q2, WEX expects earnings to range between 98 cents and $1.05 per share. For the entire year, the company sees earnings ranging between $4.20 to $4.35 per share. Wall Street had been expecting $4.46 per share. The stock is off 7% this morning.

-

Morning News: May 1, 2013

Posted by Eddy Elfenbein on May 1st, 2013 at 7:39 amChina’s Manufacturing PMI Drops in April

Chinese Way of Doing Business: In Cash We Trust

We Now Know That An Anti-Corruption Drive In China Helped Cause The Crash In Commodities

Slovenian Credit Lowered to Junk by Moody’s as Bond Sale Delayed

Fed Seen Slowing Stimulus With QE Cut by End of This Year

Consumer Confidence Jumps as U.S. Home Values Climb

Pfizer 1st-Quarter Profit, Sales Miss Estimates as Lipitor Pressure Continues

New York Times Leads Major Newspapers With 18% Circulation Gain

IBM Assures Shareholders of Profit Goals After Earnings Stumble

Merck First-Quarter Sales Disappoint

To Satisfy Its Investors, Cash-Rich Apple Borrows Money

Yahoo Scraps Deal for French Video Site

Yahoo’s Mayer Offers Paid 16-Week Leave After Birth of Child

Marc Chandler: Enrico Letta’s Italy

Cullen Roche: NYSE Margin Debt Approaches All-Time High

Be sure to follow me on Twitter.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His