-

DirecTV Jumps 6%

Posted by Eddy Elfenbein on March 15th, 2013 at 10:42 amHere are a few quick hits this morning.

The Dow is currently down 44 points, so we may have trouble keeping the streak going.

DirecTV ($DTV) is up strongly this morning, about 6%, after the company said it won’t bid for Vivendi’s Brazilian division GVT. I think they dodged a bullet. The stock is at a new 52-week high.

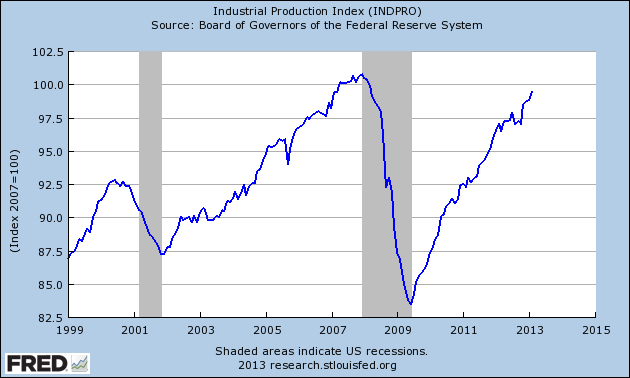

More good economic news today. The Federal Reserve reported that industrial production rose by 0.7% last month. Economists were expecting an increase of 0.4%. Industrial production is one of four keys to follow to see if we’re in a recession (see how well it aligns with the grey recession bars below). The other three are non-farm payrolls (which we got last Friday), real personal income excluding transfer payments and real manufacturing and trade sales.

The Labor Department said that inflation rose 0.7% last month, but that was largely due to higher gasoline prices. That’s the biggest rise in more than three years. However, the core rate, which excludes food and energy, rose by just 0.2%.

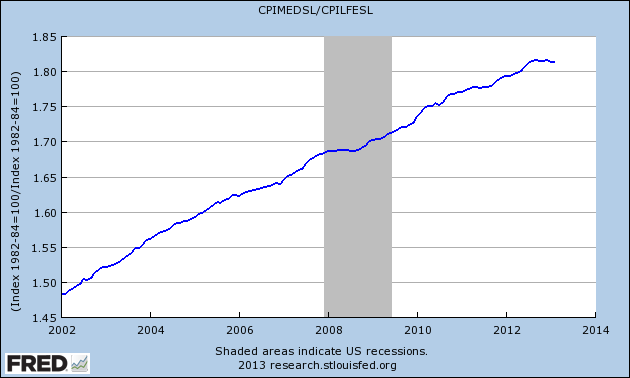

Once again, health care inflation came in below core inflation. Core inflation rose by an annualized rate of 2.11% in February while medical inflation was up just 1.85%. That may not sound like a big deal, but consider that medical costs have risen about 2% faster than core inflation, pretty consistently, for more than 40 years. For the last six months, they have behaved very much the same.

Here’s the medical prices sub-index of the CPI divided by core inflation. The ratio looks like it a hit a brick wall a few months ago, though I’m cautious because it’s a very short time span.

-

Mila Kunis Likes Stocks

Posted by Eddy Elfenbein on March 15th, 2013 at 8:20 amThe Dow’s winning streak may be in jeopardy.

-

CWS Market Review – March 15, 2013

Posted by Eddy Elfenbein on March 15th, 2013 at 7:18 amGrace Kelly: Where does a man get inspiration to write a song like that?

Jimmy Stewart: He gets it from the landlady once a month.

– Rear WindowTen days in a row! Through Thursday, the Dow has risen for an amazing ten straight trading days. This is the longest winning streak in more than 16 years. The big question on Wall Street is which will happen first—the Miami Heat will lose or the Dow will fall. This one might be close. It’s true that much of the Dow’s strength has been due to IBM. Thanks to price weighting, Big Blue now makes up more than 11% of the Dow.

For those keeping track, the Dow’s longest-ever winning streak came at the start of 1987 when the index rose for 13 days in a row. In this case, unlucky 13 may have been an omen for what came later that year.

The S&P 500 has been no slouch. That index, which is the one I prefer to follow, has been up for nine of those ten days; it dropped slightly this past Tuesday. The S&P 500 is now just inches away from cracking its all-time high close from October 9th, 2007. Daily volatility continues to be very mild. On Thursday, the VIX finished the day at 11.30 which is its lowest close in more than six years. Since the high point on New Year’s Day, the VIX has been cut in half.

It’s times like this that we need to remind ourselves not to get carried away. Sure, it’s fun watching your stocks go up each day but we have to temper our expectations. Markets don’t always do what they’re told. Remember that since this bull market started four years ago, the S&P 500 has fallen by 10% three separate times. We rode out all of those bumps and were rewarded each time. Our strategy continues to have three prongs—be patient, be disciplined and focus like a laser on high-quality stocks going for decent valuations.

In this issue of CWS Market Review, I want to take a closer look at the economy. The broader economic trends are stronger than many people realize. Although growth was pretty weak during the fourth quarter of 2012, the economy is poised to do fairly well this year, especially during the latter half of the year. Let’s look at some of the recent good news.

The Economic Recovery Is Gaining Strength

When I say that the economy is doing better, I don’t want to overstate my case. There are still 12 million Americans out of work, and Uncle Sam is piling up red ink. But there are concrete signs that the economy is fighting back.

Last Friday, the government reported that the U.S. economy created 236,000 new jobs in February which was 65,000 more than Wall Street had expected. There was actually a net decrease in the number of public-sector jobs by 10,000, so the private sector added 246,000 jobs. We still have a long way to go, but the numbers are moving in the right direction. The jobless rate for February fell to 7.7%, which is the lowest since 2008.

On Wednesday, we got more good news when the Commerce Department reported that retail sales jumped by 1.1% last month. That was more than double the rate economists were expecting. This is good news because it mollifies two concerns. One was the fear that higher payroll taxes would cause Americans to hold off on shopping. That doesn’t appear to be the case. The other concern was that retail sales would only go up due to higher gasoline prices. True, that had an impact, but even after subtracting for gas prices, retail sales still rose by a healthy 0.6%. Economists also like to look at core retail sales which ignore volatile sectors like gasoline, cars and building supplies. For February, core sales had risen by 0.4%. The positive retail-sales report is good news for Buy List stocks like Ross Stores ($ROST) and Bed Bath & Beyond ($BBBY).

On Thursday, the Labor Department reported that first-time jobless claims dropped by 10,000 to 332,000. That’s the lowest in two months. Economists were expecting 350,000. This number tends to jump around a lot, so many folks prefer to follow the four-week moving average, which is now at a five-year low.

We even had some bright news on Uncle Sam’s worrisome finances. The Treasury Department said that the monthly budget deficit for February dropped by 12% from a year ago. The CBO now estimates that the deficit for this year will be a mere $845 billion. Pocket change! But seriously, this would be lowest deficit, by far, in four years.

JPMorgan Chase and Wells Fargo Raise Their Dividends

Our Buy List continues to do well, and several of our stocks like Fiserv ($FISV), Oracle ($ORCL) and Stryker ($SYK) are at new 52-week highs. JPMorgan Chase ($JPM) also just touched a new 52-week high, but I need to confess some embarrassment here. In last week’s CWS Market Review, I predicted that House of Dimon would soon raise its dividend to 30 cents per share. The problem was that JPM’s dividend already was 30 cents per share. My goof! What makes this all the more embarrassing is that I correctly predicted that increase a year ago.

At least I was right about a dividend increase. After the closing bell on Thursday, JPMorgan announced that it plans to pay out 30 cents per share for the first quarter and increase that to 38 cents per share for the second quarter. That’s a planned increase of 26.7%. The Federal Reserve gave the bank approval to increase its dividend, but they need to resubmit their capital plans. Unfortunately, the bank is still in the political hot seat due to the London Whale fiasco. JPM remains a very good buy up to $52 per share.

Wells Fargo ($WFC) also raised its quarterly dividend. Their dividend will increase from 25 cents to 30 cents per share, which is a 20% raise. This is the second dividend increase from WFC this year. In January, the bank increased its dividend from 22 cents to 25 cents per share. WFC is a very solid bank. I’m raising the Buy Below on Wells Fargo to $40 per share.

Bed Bath & Beyond Is a Buy up to $62

In the CWS Market Review from four weeks ago, I said that Bed Bath & Beyond ($BBBY) had become a very attractive value. The home-furnishings retailer had been slammed a few times last year after it gave weaker-than-expected guidance. I think the market had overreacted, which is what markets often do.

I was pleasantly surprised to see that last weekend, Barron’s jumped on the BBBY bandwagon. The magazine said that BBBY “could” fetch as much as $85 per share. True, “could” is a rather broad word, but the key fact for us is that BBBY is a very well-run outfit. Barron’s wrote:

Bed Bath has had no direct competition since Linens ‘n Things was liquidated in 2008 after a bankruptcy. It controls an estimated 25% of the domestic home-furnishings market. Department stores offer limited competition because clothing generally generates higher profits per square foot of selling space than housewares.

Bed Bath’s strategy is unlike any other major retailer’s. It rarely advertises and usually avoids markdowns except on seasonal items, while providing excellent customer service. It targets customers with coupons offering a 20% discount, or $5 off, a single item (with a wide number of excluded products) to help drive traffic. As savvy shoppers know, Bed Bath & Beyond generally accepts expired coupons, and it’s known for a liberal returns policy—customers sometimes needn’t present a receipt. And they often present multiple coupons. The approach works because many customers come for a single item and leave with many, as they walk around the “racetrack” layout of the narrow-aisled stores.

Bed Bath & Beyond has zero debt and impressive operating margins. They’re sitting on nearly $4 per share in cash. While they don’t pay a dividend, BBBY is one of a few companies that truly buys back its own shares in an effort to reduce share count. Since 2004, share count has dropped by 100 million to 226 million. The next earnings report is due out in mid-April. I’m raising the Buy Below on BBBY to $62.

Moog Is a Buy up to $50

I’ve also been impressed with Moog ($MOG-A), which is one of our quieter stocks. On Thursday, Moog touched a new high and is now up 15.5% on the year for us. If you recall, the shares fell after the company lowered the high end of its full-year guidance. At the time, I told investors not to worry about Moog, and the stock has already made back everything it lost. The lesson is that good stocks often bend, but they rarely break. Moog is up more than 38% in the last four months. This continues to be a very good stock. I’m raising the Buy Below on Moog to $50.

Next week, we have three earnings reports coming up: Oracle ($ORCL), FactSet Research Systems ($FDS) and Ross Stores ($ROST). I previewed the earnings reports in last week’s issue. I think Oracle is the strongest candidate for a big earnings beat. The company told us to expect earnings to range between 64 and 68 cents per share. I think Oracle made at least 70 cents per share, but I suspect they’ll be conservative with their guidance.

That’s all for now. The Federal Reserve meets on Tuesday and Wednesday of next week, and it will include a Bernanke presser. I’ll be very curious to see any language changes from the Fed. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: March 15, 2013

Posted by Eddy Elfenbein on March 15th, 2013 at 7:02 amGreece Counts on Gas, Gambling to Revive Asset Sales Tied to Aid

India Ratings Constrained By Slowing Growth, Says S&P

CNPC and Eni Seal $4.2 Billion Mozambique Deal

Fed To Hold Course On Stimulus Despite Debate Over Risks

New Jobless Claims at a 5-Year Low

JPMorgan Chase CEO Jamie Dimon Is Accused Of Hiding Information About Big Losses

Samsung Introduces New Galaxy Phone

Anschutz Says Luring NFL Team Is Priority After Ending AEG Sale

VW Says Profit Won’t Grow as BMW Sees Global Economy Woes

Arctic-Specific Rules Required After Shell’s 2012 Mishaps

E*Trade Slumps After Citadel Says It’s Selling Stake

Dynegy Buying 5 Coal Power Plants From Ameren

Bain’s $17 Billion Retail Bet Not Looking So Special

Phil Pearlman: The Freudian Put

Joshua Brown: How Wall Street Raped Detroit

Be sure to follow me on Twitter.

-

Morning News: March 14, 2013

Posted by Eddy Elfenbein on March 14th, 2013 at 6:16 amEuro Minister Cautious On Size Of Any Cyprus Bailout

EU Summit Set to Loosen Deficit Shackles

Under Jordan Swiss National Bank Returns to Being Boring

IMF To Visit Ukraine For Talks On $15 Billion Loan

Fed Changes Release Time of All Policy Statements

Cities Weigh Taking Electricity Business From Private Utilities

Private Equity Squeezes Out Cash Long After Its Exit

China Mobile Sees Profits Rise 2.7% for 2012

China Probes Coca-Cola For Alleged Spying

Lego Builds New Billionaires as Toymaker Topples Mattel

Google Puts Android and Chrome Under One Boss

Samsung Needs No Steve Jobs as Low-Key Shin Showcases Galaxy

SAP as Most Valuable German Company Validates Deals Spree

Edward Harrison: Grillo: French Revolution without the Guillotine

Cullen Roche: Ritholtz: The Truth About Market Timing

Be sure to follow me on Twitter.

-

The Dow Jones IBM Index

Posted by Eddy Elfenbein on March 13th, 2013 at 6:21 pmSo what’s been powering the Dow? Much of the heavy lifting is due to Big Blue. Thanks to price-weighting, IBM ($IBM) is the largest component of the Dow. It currently makes up 11.3% of the index.

Since August 2006, IBM has crushed the Dow.

-

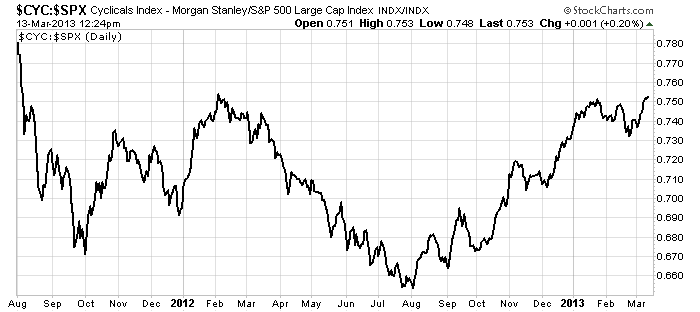

Cyclicals to S&P 500 Ratio 19-Month High

Posted by Eddy Elfenbein on March 13th, 2013 at 12:29 pmAfter a brief pause, cyclicals stocks are again in the lead. The ratio of the Morgan Stanley Cylical Index (^CYC) to the S&P 500 is very close to hitting a 19-month high.

Since the low point reach in October 2011, the cyclical index is up close to 60%.

-

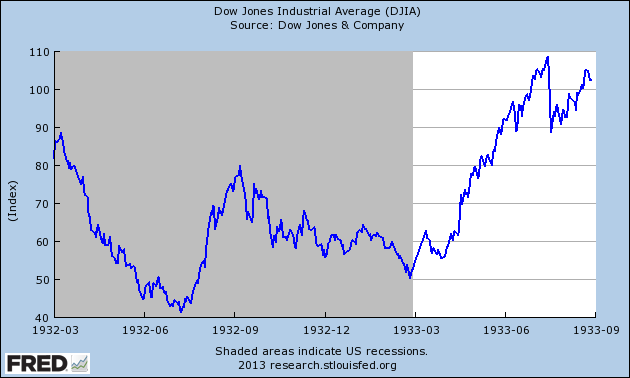

80th Anniversary of the Dow’s Best Day Ever

Posted by Eddy Elfenbein on March 13th, 2013 at 10:42 amThis Friday marks the 80th anniversary of the greatest gain in the Dow’s history. On March 15th, 1933, the Dow soared 8.26 points to 62.10 for a gain of 15.34%. That would be like a gain of 2,200 points today.

Technically, I’m not sure if it counts as the greatest single-day gain because FDR had declared a national bank holiday. There hadn’t been any trading since March 3rd.

The Dow had peaked more than three-and-a-half years earlier at more than 380. By the summer of 1932, the Dow was in the 40’s. Back then, the new president was sworn on March 4th. Some historians say that the long interlude from the election until FDR’s inauguration had caused uncertainty and that hurt the market. The 20th Amendment shifted Inauguration Day to January 20th. Interestingly, the new Amendment was ratified a few week before, but it didn’t take effect until October.

-

Retail Sales Jumped 1.1% Last Month

Posted by Eddy Elfenbein on March 13th, 2013 at 10:25 amI’m afraid don’t have much to say about the stock market this week. Things have been pretty quiet around here. Yesterday was the S&P 500’s first day down after a seven-day win streak. Despite being down, the market only pulled back by 0.24%. In other words, volatility continues to be very low. On Monday, the Volatility Index dropped down to 11.50 which was its lowest reading since early 2006.

The good news today was that the government reported that retail sales rose by 1.1% last month. December and January sales were revised higher as well. This is the biggest increase since September and it was more than double the increase economists were expecting. One of the worries is that the higher numbers for February were due to higher gasoline prices, but if we knock out gasoline, retail sales were up 0.6% which isn’t so bad.

Looking towards the stock market, I see that Walgreen ($WAG) is at a new 52-week high. Unfortunately, the stock is still where it was more than 12 years ago. The thing is, the earnings have been quiet strong. The issue is that its P/E Ratio has gotten squeezed. Even when you get a good company, a bad price can ruin your investment.

-

Morning News: March 13, 2013

Posted by Eddy Elfenbein on March 13th, 2013 at 7:43 amProperty Concerns Weigh on China Market

Euro-Region Industrial Output Declines More Than Forecast

Iran Oil Exports Seen Rising 13% by IEA Even as Sanctions Widen

Treasuries Gain as Six-Day Price Decline Boosts Auction Demand

White Says Her S.E.C. Would Be Tough on Wall St.

Google Concedes That Drive-by Prying Violated Privacy

Cathay Pacific Profit Beats Estimates as Travel Demand Gains

Icahn’s Dell Campaign Shows Activism (of a Sort) Is Back

U.S. Tax Cheats Picked Off After Adviser Mails It In

BHP Billiton Faces Corruption Probe Over Beijing Olympics

Hostess Sells Twinkies Brand to Investment Firms

An Energy Coup for Japan: ‘Flammable Ice’

Dimon’s Extra $1.4 Million Payout Hangs on Fed Decision

Jeff Carter: Bullish Capital Market Outlook

John Hempton: Vodafone: The Only Deal That Makes Sense

Be sure to follow me on Twitter.

- Load More

China has 105 cities with over 1 million people.

In 1940, Ida May Fuller got the first social security check. The check number was 00-000-001. She lived to 100 and collected $22,888 in benefits.

Airline fares are cheaper than they were 25 years ago.

-

-

Archives

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His