-

Morning News: October 20, 2022

Posted by Eddy Elfenbein on October 20th, 2022 at 7:00 amGlobal Housing Market Pain Has Echoes of a Crash 30 Years Ago

China Summons Chip Firms for Emergency Talks After US Curbs

Why Another Xi Jinping Term Might Be in U.S.’s Interest

Truss and UK Market Turmoil: What You Need to Know

Truss Resigns as PM, Hunt Rules Out His Candidacy

After U.K. Market Blowout, American Officials Ask: Could It Happen Here?

Biden Expands Effort to Secure U.S. Energy Independence

Ahead of the Midterms, Energy Lobbyists Plan for a Republican House

Appeals Court Says Financial Watchdog Agency CFPB’s Structure is Unconstitutional

Businesses Expect Economy to Weaken, Fed’s Beige Book Says

Your Paycheck Next Year Will Be Affected by Inflation. Here’s How.

Drugmakers Look to Curb Medicare’s New Power to Negotiate Lower Drug Prices

Tesla Drops as Musk Says Demand ‘A Little Harder’ to Come By

Tesla’s Valuation Doesn’t Add Up Today, Never Mind $4.4 Trillion Tomorrow

Blackstone’s Earnings Fall 16% on Sharp Drop in Asset Sales

JPMorgan, Goldman Face Probe by 19 States Over ESG Investing

Small Gunmakers Find State Weapons Bans Offer a Lucrative Niche

Philip Morris Raises Offer for Swedish Match and Buys U.S. Rights for IQOS

Burned Out on Your Personal Brand

Be sure to follow me on Twitter.

-

Morning News: October 19, 2022

Posted by Eddy Elfenbein on October 19th, 2022 at 7:05 amHong Kong Offers Visas, Perks to Reverse Brain Drain After Losing 140,000 From Workforce

Bread Prices Skyrocket as Inflation Grips Europe

UK Inflation Returns to 40-Year High

Britain Scales Back Foreign Aid, Threatening Progress in Global Health

Biden to Sell More Oil From Strategic Reserve to Keep Gas Prices in Check

The Fed, Staring Down Two Big Choices, Charts an Aggressive Path

Three Hidden Words From Fed Insiders Point to Much Higher Rates

Inflation Causes IRS to Raise Tax Brackets, Standard Deduction by 7%

Weary of Snarls, Small Businesses Build Their Own Supply Chains

US Housing Market in ‘Free Fall’ as Builder Confidence Suffers ‘Disastrous’ Drop

Dubai’s Luxury Property Market Is Cashing in on the Global Slowdown

Billionaire Ambani Splurges $163 Million on Priciest Dubai Villa

Nestlé to Acquire Seattle’s Best Coffee Brand From Starbucks

Netflix Returns to Growth, Saying the Worst of Slowdown Is Over

The Great Netflix Debate: Do Its Movies Belong in Theaters?

John Mack, Who Led Morgan Stanley Into a Crisis, Regrets Little

Rarely-Humbled Goldman Sachs Concedes Missteps in Plan to Take on Megabanks in Retail Finance

Deutsche Bank HQ Raided by German Prosecutors in Tax Probe

Be sure to follow me on Twitter.

-

CWS Market Review – October 18, 2022

Posted by Eddy Elfenbein on October 18th, 2022 at 6:34 pmThe stock market is surging again. Yesterday, the S&P 500 gained 2.65%, and today the index was up another 1.14%.

I’m fine with the gains, but we’ve been burned before. As we know, the stock market loves to use big short-term gains to lure investors back. We’re not falling for it. We’re still in the market, but we’re cautious about it.

Here’s an interesting stat: Prior to today, the S&P 500 was up only five times in the last 20 sessions, but all of those up days were up big. The smallest of the five was a gain of 1.97%.

In other words, the stock market has been working in two modes. Stocks are either zooming higher or they’re down. There seems to be no middle ground. The last two days were in up mode.

Right now, Wall Street’s attention is on focused on earnings season. It’s still early, but we’ve already had several important earnings reports. Goldman Sachs (GS) crushed its earnings ($8.25 versus the estimated $7.69). Johnson & Johnson (JNJ) made $2.55 per share which was a seven-cent beat. Lockheed Martin (LMT) earned $6.71 per share which beat the Street by four cents. Netflix (NFLX) had good news (finally!). The stock is up 14% after hours.

The good news may have calmed the market for the time being. Instead of worrying only about inflation, interest rates and the Federal Reserve, investors are seeing clear evidence that many companies are still making a healthy profit.

The first Buy List stocks will report earnings later this week, and I’m expecting good results. I think there’s a good chance that Stepan (SCL) will announce its 55th dividend increase in a row. There aren’t many companies that can say that.

Our strategy continues to work very well in this market. Here’s a look at the AdvisorShares Focused Equity ETF (CWS) since mid-June:

I need to be clear that our ETF is based on the Buy List, but it’s not exactly the Buy List. Still, it mimics it very well. When investors get scared, they seek out quality and for the last several months, that’s us. Also, we just got our fifth star from Morningstar for our overall rating. You can learn more about the ETF at the AdvisorShares website.

Last Thursday, the stock market got spooked again by another lousy CPI report. Instead of showing that inflation is fading away, the data says it’s still plaguing the economy. For September, headline inflation was up by 0.4% which was 0.1% more than estimates. Core inflation was up by 0.6%. Wall Street had been expecting 0.4%.

This report has pretty much ended discussion on the next Fed meeting. The futures market now places a 95.2% chance that the Fed will hike by 0.75% at its November meeting. I’d say that’s about 4.7999% too low, but that’s me.

It’s not just the November meeting; futures traders are now placing a 66% chance of another 0.75% hike in December. If that’s right, that would mean the Fed will hike by 0.75% five times in a row. These rate hikes are going to do some damage.

Economists See a Recession Coming Next Year

Speaking of which, the Wall Street Journal recently surveyed economists and they placed the odds of a recession starting in the next 12 months at 63%. That’s up from 49% in July. They expect the economy to contract in the first two quarters of 2023.

In July, the economists were expecting the economy to grow in real terms at an annualized rate of 0.8% in Q1 of 2023. Now that’s been pared back to -0.2%. For Q2, the forecast has been pulled back from +1% to -0.1%.

Most economists expect the Fed to raise interest rates too far. That’s a serious concern that I share. The problem with the Fed’s interest rate policy strategy is that it takes a long time to see the results. Historically, that’s caused Fed members to see the lag time as evidence that they’re not pursuing their policy hard enough.

The Fed may also soon impact the labor market.

Economists believe that nonfarm payrolls will decline by 34,000 a month on average in the second quarter and by 38,000 in the third quarter. According to the last survey, they expected employers to add about 65,000 jobs a month in those two quarters.

If there’s a silver lining, it’s that economists see the recession being shorter than the historical average. I would not be surprised to see the Fed start cutting interest rates sometime in 2023. A more pliant Fed would also convince me that any rally is real and not some head-fake.

The healthcare sector has done very well this year in relative terms. That’s not much of a surprise since healthcare tends to be one of the better defensive sectors. Even in a recession, people don’t cut back much on their medical expenses. At least, not the way they do for cars or houses.

Before this year, healthcare had been lagging the market for six years. Beginning in late November, the tide started to turn. At the same time, this is when we saw so many of the high-flying stocks of the Covid era start to lose momentum. More than a few have crashed.

The healthcare sector briefly lagged again this summer during another bear-market rally. As that rally faded, healthcare again started to lead the market. This is a trend that may continue into next year.

Stock Focus: Mettler-Toledo International (MTD)

I’m a big of Mettler-Toledo International (MTD) but the stock doesn’t seem to get much attention, despite having a market cap of $26 billion and a remarkable performance history.

Mettler-Toledo makes scales and lab equipment. It’s a competitor of Thermo Fisher Scientific (TMO). The company is incorporated in the United States, but the headquarters are in Switzerland. The stock IPO’d 25 years ago at $14 per share, and it’s been a huge winner. MTD has never split or paid a dividend. The shares are currently trading at $1,200 (on the nose!). That works out to an annualized gain of nearly 20%.

Mettler-Toledo is having another strong year. For Q2, MTD reported earnings of $9.39 per share. That was a 16% increase over last year’s Q2. It topped Wall Street’s forecast by 63 cents per share. The company also increased full-year EPS guidance to a range between $38.85 and $39.05. That was an increase of 65 cents per share to the low end and 55 cents per share to the high end.

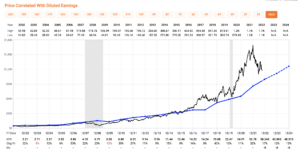

But what I like best about MTD is its “earnings line.” By that I mean that the company’s annual EPS line (the blue line below) is very consistent.

(The chart is from FastGraphs.)

This is an important point about stock valuations. Consider this hypothetical:

Imagine you have two companies that are equal in every way. Both are expected to earn $1 per share next year. However, there’s one important difference. Company A is expected to earn $1 per share, plus or minus two cents per share. Company B is expected to earn $1 per share, plus or minus 20 cents per share. Which stock will have the higher share price?

In almost all normal cases, company A will have a higher share price. This is because Wall Street values the stability of earnings. The premium of A over B will ebb and flow over time depending on the market’s appetite for risk. The premium probably won’t be very much, but it will be visible over the long term.

I use this thought exercise because Mettler-Toledo may have the steadiest earnings line I know of, and that’s why Wall Street gives it a high valuation. Going by today’s price and the company’s latest guidance, MTD is trading at more than 30 times earnings—and that’s in a bear market. The stock is down in 2022. Late last year, MTD was trading north of $1,700 per share.

I also like that Mettler-Toledo has bought back so many shares over the years. I’ve been critical of many companies that use share buybacks as a way of enriching executive bonuses, but MTD has reduced its share count.

For Q3, Mettler-Toledo expects earnings between $9.75 and $9.85 per share. The consensus on Wall Street is for earnings of $9.83 per share. I would be surprised if Q3 earnings came in at less than $10 per share.

In summary, I like Mettler-Toledo a lot. The sad part is that I understand why it’s so expensive.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want to learn more about the stocks on our Buy List, please sign up for our premium service. It’s $20 per month, or $200 per an entire year.

-

Morning News: October 18, 2022

Posted by Eddy Elfenbein on October 18th, 2022 at 7:12 amXi Jinping’s Ideological Ambition Challenges China’s Economic Prospects

China Abruptly Delays GDP Release During Communist Party Conference

In the Netherlands, Balancing Energy Security Against Climate Concerns

Russia Wipes Out Exxon’s Stake in Sakhalin Oil-and-Gas Project

Putin’s War Escalation Is Hastening Demographic Crash for Russia

Economists Now Expect a Recession, Job Losses by Next Year

Looming Leadership Void at I.R.S. Raises Concerns Over $80 Billion Overhaul

Treasury Dept. to Ask Insurers for Data on Climate Risks to Measure Coverage Affordability

Even as US Inflation Climbs, Wall Street Sees Steep Fall Coming

Retailers, Brands and Tech Platforms Bet Big on Live-Streamed Shopping in the U.S.

BofA Survey ‘Screams’ Capitulation Among Investors

How Switzerland’s Oldest Bank Became a Meme Stock

Goldman Sachs Unveils Revamp as Third-Quarter Profit Falls

Meta Ordered Again to Sell Giphy as UK Watchdog Blocks Deal

Netflix Looks to Put an End to Subscriber Losing Streak

All This Talk About “Quiet Quitting” Is Absurd

Be sure to follow me on Twitter.

-

Morning News: October 17, 2022

Posted by Eddy Elfenbein on October 17th, 2022 at 7:00 amIn Xi’s China, the Business of Business Is State-Controlled

China Delays Indefinitely the Release of G.D.P. and Other Economic Statistics

China’s Economy Needs to Double in Size to Meet Xi’s Ambitious Plans

New U.K. Finance Minister Drops Almost All of Tax-Cut Plan

How Russian Ships Are Laundering Grain Stolen From Occupied Ukraine

Saudi Arabia’s Super Fund Leans on Influence of BCG Power Broker

Big Coal Uses This Playbook to Avoid Cleaning Up its Messes

New England Risks Winter Blackouts as Gas Supplies Tighten

Democrats Spent $2 Trillion to Save the Economy. They Don’t Want to Talk About It.

Despite What the Experts Told You, This Was Never ‘Inflation’

What the $24.6 Billion Kroger-Albertsons Merger Could Mean for Groceries

Goldman Shakes Up Leadership Ranks in Yet Another Overhaul

Bank of America Profit Drops on Loan-Loss Reserve Build

Procter & Gamble Bets Inflation Won’t Push Shoppers to Trade Down

Families Still Struggle to Find Baby Formula Nearly One Year After Shortages Began

Sports TV Rights Are Costlier Than Ever — But They’re Cable’s Last Lifeline

Ye to Buy Controversial Social Networking App Parler

Be sure to follow me on Twitter.

-

Morning News: October 14, 2022

Posted by Eddy Elfenbein on October 14th, 2022 at 7:02 amWar Colliding With Recession Risks Leave Energy Markets on Uncertain Path

The UK’s Crisis Is Threatening the Global Inflation Fight

Kwasi Kwarteng Out as UK Chancellor

Inflation Is Unrelenting, Bad News for the Fed and White House

Inflation Report Seals Case for 0.75-Point Fed Rate Rise in November

Why Social Security’s Inflation Protection Is Priceless

Retirees Catch a Break With the Social Security COLA

Private Bets Shield World’s Largest Investors From Market Mayhem

BofA Strategists See More Pain in Store Before Stocks Reach Low

Investing for Your Values, but Betting on Growth

Computer Buyers Curtail Purchases After Pandemic Splurge

Kroger, Albertsons Forge $24.6 Billion Grocery Giant Combination

Chinese Drone Billionaire’s Dominance Threatened by US Blacklists

It Shouldn’t Matter So Much Whether Elon Musk Buys Twitter

Want to Get Ahead? Pick the Right Company

Netflix to Get Nielsen Ratings as Streaming Giant Rolls Out Ad-Supported Plan

A Pair of Levi’s That Sold for $76K Reflects Anti-Chinese Sentiment of 19th Century

Be sure to follow me on Twitter.

-

Morning News: October 13, 2022

Posted by Eddy Elfenbein on October 13th, 2022 at 7:02 amIMF Urges Governments Restrain Spending to Fight Inflation

OPEC+ Supply Cut Could Tip Global Economy Into Recession, IEA Says

Bad Policies Are Greasing the Wheels for a Global Recession

A Weed Gummy Theory for the Fed’s High-Stakes Interest Rate Gamble

Volatility Is Only Certainty for Stocks With Inflation Data Due

Bitcoin Becoming Less Volatile Than Stocks Raises Warning Flag

As Bond Investors’ Bets Blow Up, They Might Usher In Era of Higher Rates

TSMC to the World: We Have No Good News for You

Battle Over Wage Rules for Tipped Workers Is Heating Up

BlackRock Profit Beats as ETF Demand Holds Up Against Market Rout

Exxon’s Exodus: Employees Have Finally Had Enough of Its Toxic Culture

Walgreens Beats Sales Expectations, As It Expands its Health-Care Business

TikTok Parent ByteDance Sets Sights on Spotify With Music-Streaming Expansion

TikTok Wants to Open Warehouses in Amazon’s Backyard to Expand e-Retail Business

Delta Reports Profit and Projects Strong Travel Demand in Coming Months

Be sure to follow me on Twitter.

-

Morning News: October 12, 2022

Posted by Eddy Elfenbein on October 12th, 2022 at 7:07 amA Warning for the World Economy: ‘The Worst Is Yet to Come’

Bailey Pressed to Extend Gilt Purchases Amid Deadline Confusion

US Core Inflation Seen Returning to 40-Year High as Rents Rise

U.S. Mortgage Interest Rates Rise to Highest Level Since 2006

Hedge Fund Managers Paid for Stockpicking Genius Aren’t Showing Much of It

Wall Street Braces for an Earnings Season of Mixed Signals

Credit Suisse Shares Drop on US Tax Probe Over Accounts

Biden Proposal Could Lead to Employee Status for Gig Workers

Companies Hoarding Workers Could Be Good News for the Economy

Amazon Labor Union, With Renewed Momentum, Faces Next Test

Twitter Faces Only Bad Outcomes If the $44 Billion Musk Deal Closes

Philips to Take $1.3 Billion Write-Down on Sleep-Apnea Business

PepsiCo Raises Guidance Again as Higher Prices Lift Sales

Nissan Sells Russian Business for Less Than $1, Takes $687 Million Loss

Toyota Starts Plant in Junta-Led Myanmar Making 1 to 2 Cars a Day

Federal Officials Trade Stock in Companies Their Agencies Oversee

A Nobel Prize for the Economics of Panic

Be sure to follow me on Twitter.

-

CWS Market Review – October 11, 2022

Posted by Eddy Elfenbein on October 11th, 2022 at 8:11 pmThe Nasdaq Falls to a Two-Year Low

In last week’s issue, I included a picture of Lucy holding the ball in place for Charlie Brown to kick. The reference is to how bear-market rallies tempt us into thinking the coast is clear, only to punish us again.

In this week’s issue, I’m including this update:

Once again, Lucy pulled the ball away and poor Charlie Brown went flying head over heels. That’s pretty much what happened on Wall Street over the last week.

Last week, the market gave us a brief but strong rally on Monday and Tuesday, and it’s taken it all back since then. The Nasdaq Composite closed today at its lowest level since July 28, 2020 (see chart below). Today’s intra-day low for the S&P 500 was its lowest since November 23, 2020. The index closed the day a hair above its recent low from September 30, which itself was a two-year low.

It’s a mess out there. Meta Platforms (formerly Facebook) is lower than where it was six years ago. We’re still seeing the trend I’ve talked about many times: risky stocks are getting hammered while conservative stocks are holding up relatively well. In today’s trading, the S&P 500 Low Vol Index rose 0.57% while the S&P 500 High Beta Index fell by 1.85%. It’s all about the Fed, the Fed and the Fed.

The recent selling was spurred in part by last Friday’s jobs report. To be fair, the report was a combination of good and bad news.

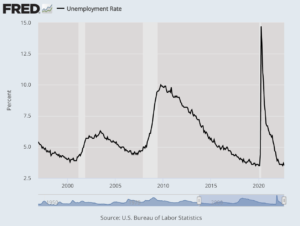

According to the report, the U.S. economy created 263,000 new jobs last month. That was below Wall Street’s expectations of 275,000. It also tied for the smallest monthly increase since April 2021. The unemployment rate ticked down to 3.5%.

Even though the jobs number was short of estimates, the futures market increased its odds that the Fed was going to raise interest rates by 0.75% at its November meeting. The odds are now up to 83% and the meeting is only three weeks away. I think it’s clear that the Fed intends to hike by 75 basis points in November.

More important than my opinion is the bond market’s. The one-year Treasury got to 4.28% today. That’s a 15-year high.

Also in the jobs report, the government said that the labor force participation rate fell to 62.3%. The U-6 unemployment rate, which is a broader measure, fell to 6.7% from 7% in August.

From a sector view, leisure and hospitality led the gains with an increase of 83,000, a rise that still left the industry 1.1 million jobs short of its February 2020 pre-pandemic levels.

Elsewhere, health care added 60,000, professional and business services rose 46,000 and manufacturing contributed 22,000. Construction was up 19,000 and wholesale trade climbed 11,000.

A drop of 25,000 in government jobs was a big contributor to the report missing expectations. Hiring at the state and local level is highly seasonal, so the decline points to a report that otherwise was largely in line with expectations and that shows a resilient jobs market.

Also on the negative side, financial activities and transportation and warehousing both saw losses of 8,000 jobs.

Another weak spot continues to be wages. For September, wages rose by 0.3%, which matched estimates. Over the past year, wages are up by 5%. While that sounds good, it’s less than the rate of inflation. In real terms, many Americans are seeing their wages getting cut. Inflation hurts so many folks who are already struggling. There are now 1.7 jobs per every unemployed person.

The next big test for the market will come on Thursday when the government releases the inflation report for September. The last report shocked Wall Street as it showed that inflation is still not under control.

Over the last 12 months, inflation is running at 8.26%. For Thursday, Wall Street expects to see consumer prices increase by 0.2% for September, and it expects the 12-month rate to fall to 8.1%.

The price for oil plays a major role in the inflation stats. While the price for gasoline had been dropping for several weeks, that seems to have ended about a month ago, and gasoline has been steadily increasing since then.

In last month’s report, the core rate of inflation came in at 0.6% which doubled expectations. That was a shocker. For September, Wall Street expects the core rate to rise by 0.4%. For the last 12 months, economists expect the core inflation rate to be 6.5%.

The equation is simple. Once inflation is under control, then the Fed won’t have to raised rates as aggressively. That’s good for the economy and earnings. It also takes some pressure off the dollar which has jumped higher against so many currencies. In the U.K., the Bank of England has been buying bonds in an effort to protect pension funds. The bond market there has has crumbled.

Inflation impacts so many different sectors at the same time. It’s so important that the Fed puts inflation back in its bottle.

Giving Another Look at Ansys

I’ve been a big fan of the company Ansys (ANSS) for some time. Unfortunately, I’ve not been such a big fan of the stock. The shares have often been very expensive. Very, very expensive.

Ansys makes simulation software for engineers. Whenever you see a designer working with a 3-D model on a computer screen, there’s a good chance that he or she is using Ansys software. Before building a bridge, a skyscraper or an airplane, the designer wants to make sure that it can withstand the pressure it will experience in real life.

Ansys is a classic “wide moat” company. Once a customer starts using their software, there’s a good chance he or she will become a long-term buyer. Ansys maintains an operating profit margin in excess of 35%, and their gross margin runs around 90%. That’s very attractive.

As you might guess, Ansys is not exactly a value stock, but I think there are occasions when it’s worth it to pay extra for an outstanding company. I saw a good opportunity for us to add Ansys to the Buy List. That was at the beginning of 2020 and the stock did very well for us. In 2020, Ansys gained more than 41% for us. I kept ANSS on in 2021, and it gained another 10% for us.

I loved the profits but again, I was concerned about the valuation. After some careful consideration, I decided to not include it on our Buy List for 2022. That’s a tough move to sell your winners. You can’t help but feel attached to them, but investing is about business, and loyalty to a stock is not important. The simple fact was that Ansys had become way too expensive.

As it turned out, our decision was almost perfectly timed. Shares of Ansys are down more than 50% this year. The business has been holding up well and Ansys has continued to beat expectations. In August, Ansys reported very good Q2 earnings. The company made $1.77 per share which beat estimates by 17 cents per share.

For Q3, Ansys expects earnings to range between $1.56 and $1.70 per share. For the entire year, Ansys expects earnings to range between $7.50 and $7.88 per share. For next year, Wall Street expects $8.49 per share.

That means that Ansys is going for less than 24 times next year’s earnings. That’s pricey, but it’s not bad for Ansys. It’s funny how a good stock can drop in half and suddenly, everyone’s afraid to own it. I can tell you that I’m seriously considering adding Ansys back onto our Buy List. I won’t make our final decision until late December.

Before I go, I have a quick story to share with you. In last week’s issue, I discussed how Elon Musk finally agreed to buy Twitter. I thought I’d ingratiate myself so I tweeted:

Elon Musk is the kindest, bravest, warmest, most wonderful human being I've ever known in my life.

— Eddy Elfenbein (@EddyElfenbein) October 4, 2022

Most people recognized the line from the movie, The Manchurian Candidate. One outfit that did not was the newspaper, The Independent. My tweet is quoted at the end of their story. Apparently, old Sinatra movies don’t hold the shared cultural value I thought.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want to learn more about the stocks on our Buy List, please sign up for our premium service. It’s $20 per month, or $200 per an entire year.

-

Morning News: October 11, 2022

Posted by Eddy Elfenbein on October 11th, 2022 at 7:01 amCan This Man Solve Europe’s Energy Conundrum?

U.K. Government Plans an Update to Its Tax and Spending Agenda

Bank of England Further Expands Bond-Market Rescue

China’s Shot at Overtaking the US Economy Is at Stake in Xi’s Next Term

World’s Emergency-Lending Capacity Is Getting Stretched

Fed’s Vice Chair Nods to Global Risks but Stays Focused on Inflation

Credit Suisse May Face $8 Billion Capital Shortfall in 2024

Chipmaker Rout Engulfs TSMC, Samsung With $240 Billion Wiped Out

GM Looks to Parlay Battery Work Into New Energy Business

Cathie Wood Buys Adobe as Stock Tumbles After $20 Billion Deal

The Great Post-Covid Online Shopping Bet Was a Costly Delusion

A Prime Day Warning: Some Discounts May Be Price Hikes, Study Shows

Delta to Invest in Flying-Taxi Maker to Offer Rides to Airports

Ben Bernanke Led the Fed During the Worst Financial Crisis in Generations

Douglas Diamond and Philip Dybvig Created an Influential Model About Bank Runs

Be sure to follow me on Twitter.

- Load More

You can do very well by betting on the big winners before they became the big winners.

"Japan’s births mark record low in 2024, plummet below 700,000." They predicted it would get here by 2039 but made it 15 years early. ?

Florida's Housing Market 'Turning Down Fast'

-

-

Archives

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His