-

Morning News: August 20, 2012

Posted by Eddy Elfenbein on August 20th, 2012 at 7:41 amBundesbank Steps Up ECB Bond Plan Criticism; Rift Widens

Euro Area Leaders Plan Shuttle Talks to Support Greece

Thailand Signals Slower Growth as Export Outlook Wanes

CME Planning Europe Exchange to Compete With Eurex, Liffe

Spanish Banks Next For Greek-Style ECB Shakedown

China’s Rural Migrants Key To Consumption -Government Report

Oil Rises as European Leaders Prep for Debt Talks

Banks Use $1.77 Trillion to Double Treasury Purchases

Aetna to Acquire Coventry Health Care

Carlson Chief Steps Down To Take Best Buy’s Top Job

Lowe’s Reports Second Quarter Sales and Earnings Results

Chevron, Shell Swap Natural-Gas Assets

In Apple’s Patent Case, Tech Shifts May Follow

Credit Writedowns: FHA’s 30x Leverage On Mortgages Is Creating A New “Subprime” Market

Jeff Miller: Weighing the Week Ahead: A Lull Before the Storm?

Be sure to follow me on Twitter.

-

Partly Cloudy

Posted by Eddy Elfenbein on August 17th, 2012 at 2:01 pmIt’s beautiful outside so I’m shutting down and starting the weekend early. I hope you can do the same.

Here’s some magic from the brilliant folks at Pixar.

Note that the sound isn’t the original but I’m sure you can follow along.

-

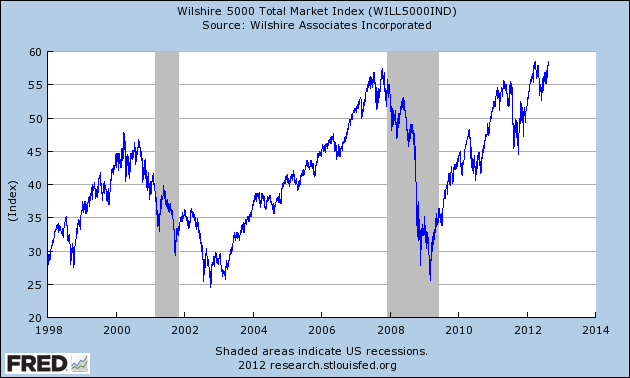

The Wilshire 5000 Total Return Index Nears All-Time High

Posted by Eddy Elfenbein on August 17th, 2012 at 10:46 amThe broadest stock market index, the Wilshire 5000 Total Return Index, which includes dividends, closed yesterday just shy of its all-time high from April 2.

Of course, measuring from the highs in 2000 or 2007, the total return is positive but nothing special. And once we add in inflation-adjusted returns, then things don’t look nearly as good.

-

CWS Market Review – August 17, 2012

Posted by Eddy Elfenbein on August 17th, 2012 at 8:02 am“The race is not always to the swift, nor the battle to the strong, but that’s how the smart money bets.” – Damon Runyon

YAWN!

Oh dear Lord, this is the most boring market possible. August 2012 has turned into the Great Summer Snoozefest. The VIX recently dipped below 14. Trading volume is at the lowest point since 2007. Just look at the S&P 500’s daily performance from August 8th to August 15th: +0.06%, +0.04%, +0.22%, -0.13%, -0.01% and +0.11%. Wake me when it’s over.

The good news is that our Buy List has been doing quite well lately. On Monday, a good earnings report prompted Sysco ($SYY) to leap 4.5%, and the stock has continued to rally. Harris Corp. ($HRS) just made another 52-week high; it’s now up 27.64% for us on the year. DirecTV ($DTV) is up nearly 20% in two months. Since August 2nd, our Buy List is up 5.37% compared with 3.70% for the S&P 500.

In this week’s CWS Market Review, we’ll look at some facts hiding just below the surface of this somnolent market. I’ll also highlight the good earnings out of Sysco, and we’ll discuss the upcoming earnings report from Medtronic ($MDT). But first, let’s look at what’s driving this low—very, very low—volume rally.

The Quiet Rotation from Bonds to Stocks

On Thursday, the S&P 500 closed at 1,415.51. The index is just 0.25% away from cracking its 51-month high. The rally is even more impressive when you consider the amount of dividends that have been paid out. Fact: More companies in the S&P 500 are now paying dividends than at any time since 1999. Adjusted for dividends, the S&P 500 now stands at an all-time high. You wouldn’t know that from watching the financial media.

It’s amazing to contrast the low volatility we’re seeing this August with the dramatic action we saw one year ago. The raucous debt-ceiling debate mercifully came to an end on August 2, 2011, but the market’s fireworks were just starting. The Dow dropped 512 points on August 4th and another 644 points on August 8th. Gary Alexander notes that the Dow moved at least 423 points on four straight days from August 8th to August 11th. Gary writes, “From August 2 to September 9, 2011, the Dow went up or down over 250 points on 12 of 28 trading days.” In the last five months of 2011, the S&P 500 had daily swings of 2.5% or more 22 times. But that hasn’t happened once this year.

Looking back on it, the panic of last summer was a great buying opportunity for patient investors like us. Those who kept cool while everyone else was freaking out did very well. Remember some of these prices from last August—Reynolds American ($RAI) below $32 per share, or Fiserv ($FISV) below $51? Thank you, panicked investors!

What’s catching my attention about this rally is the quiet move away from Treasuries. The yield on the 10-year Treasury is now up to 1.83%. That’s a 45-basis-point jump in three weeks. Of course, that was off the lowest yield ever for the 10-year in the history of the Republic so it’s kind of odd to say that yields have “shot up all the way to 1.83%.” That’s still very, very low.

But the move is significant, and it’s been matched by other bonds at the long end of the yield curve, particularly beyond five years out. Typically, a sell-off in long-term bonds would be matched with a rotation towards cyclicals. And as I described last week, that’s what we’ve seen (Harris and Ford, for example). But really, the rotation hasn’t been as large as I would have expected.

What’s going on here? Frankly, I can’t be certain. My suspicion is that the market is slowly beginning to realize that the economy is better than most people believe. This week’s report on industrial production was another piece of evidence supporting this thesis. In the CWS Market Review from two weeks ago, I included a chart showing the performance of stocks and long-term bonds since March. My point was to show how much better bonds had performed than stocks, reflecting the market’s strong defensive posture. My timing was impeccable because the relationship has completely reversed itself since then. Here’s an updated version:

If the economy is indeed stronger than is commonly believed, what can we expect as investors? For one, we can shelve all the silly babble about QE3. As far as stocks are concerned, we can expect to see a slow, steady melt-up in equity prices. Don’t expect to see any sudden vaults of 3%, 4% or more. We’ll also see the market focus on domestic industries, small-caps (due to their size, smaller companies often have less international exposure) and cyclicals. I doubt higher-yielding stocks and defensive plays in general will get burned. But then again, they won’t see the lion’s share of the gains.

Some of the stocks on our Buy List that are poised to thrive, assuming the stronger-economy thesis is correct, include Ford ($F), JPMorgan Chase ($JPM), Moog ($MOG-A), Nicholas Financial ($NICK), Wright Express ($WXS), Fiserv ($FISV) and Bed Bath & Beyond ($BBBY).

By the way, have you noticed how much BBBY has recovered from its so-called “poor” guidance? The stock plunged 17% in one day after the company said this quarter’s results would be 5% to 10% below the Street’s consensus. I thought the reaction was crazy, and I said so. BBBY is an excellent buy any time you see it below $70 per share.

Sysco Rallies on Strong Earnings

On Monday, Sysco ($SYY) reported earnings of 55 cents per share for the fourth quarter of their fiscal year. That’s basically what I had been expecting. Wall Street’s consensus was for 54 cents per share. For the entire fiscal year, Sysco made $1.93 per share. That’s a good result, and investors should be pleased.

Let’s look at some of the numbers: Quarterly sales came in at $11 billion, which is a 5.9% increase over last year’s Q4. What Sysco calls “adjusted operating income” increased by 2.2% to $608 million. The company faces rising food costs, but I’m impressed by how well they’re managing the issue. The Street expects earnings for the current fiscal year of $1.98 per share. That means the stock is going for about 15 times earnings.

Shares of Sysco gapped up 4.5% on Monday, and the shares advanced on Tuesday and Wednesday as well. But the best thing about investing in Sysco is the dividend. Sysco has increased its payout every year for the last 42 years. There aren’t many companies that can claim a record like that. This November, I expect them to do it again. The stock currently yields 3.7%. Sysco is a solid buy for income-oriented investors up to $32 per share.

Medtronic Is a Buy up to $44 Per Share

On Tuesday, August 21st, Medtronic ($MDT) is due to report earnings for the first quarter of their fiscal year. The stock has been gaining ground recently, and it just poked its head above $40 per share. In May, Medtronic told us to expect revenues to rise between 2% and 4% for this year. They see full-year earnings-per-share ranging between $3.62 and $3.70. That’s decent growth in this environment. Last year, Medtronic made $3.46 per share. The stock is close to breaking its high from six months ago.

I like Medtronic a lot and frankly, the company often doesn’t get the credit it deserves. I’ve been impressed that demand has returned for their pacemakers and defibrillators. My rough numbers say that Medtronic earned 87 cents per share for Q1 (give or take), while the Street expects 85 cents per share. Honestly, I’m not too worried about a minor earnings miss or beat this early in the fiscal year. Instead, what I want to see is if the company is executing well, and I have little doubt that they are. In June, Medtronic raised its dividend for the 35th year in a row. Thanks to the recent rally. I’m bumping up my buy price on Medtronic to $44 per share.

Before I go, several readers have written in, thanking me for my avoid-at-all-costs recommendation on Facebook ($FB). Folks want to know if I like it at this heavily reduced price. The short answer is no. The longer answer is nooooooo.

That’s all for now. Outside of Medtronic’s earnings report on Tuesday, next week should be another sleepy week on Wall Street. I doubt we’ll see much action until after Labor Day. But I’ll be here. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Tips on Spotting Financial Fraud

Posted by Eddy Elfenbein on August 17th, 2012 at 7:50 amFor those of you who never got around to taking ancient Greek in college, the word of the day is hubris.

Webster’s dictionary, 8th ed.: “Excessive pride or self-confidence, often entailing a loss of contact with reality and an overestimation of one’s own capabilities, especially on the part of those in positions of power.”

That pretty much sums up the psychology behind the ongoing debacle that is Peregrine Financial, whose founder and CEO, Russell Wasendorf, Sr., was indicted in Cedar Rapids, Iowa, on Monday on 31 counts of lying to U.S. financial regulators.

By his own admission, Wasendorf bilked investors out of nearly $100 million over the course of nearly two decades (just days before his arrest, the National Futures Association reported a deficit of more than $200 million in funds that Peregrine Financial had claimed to be on deposit at U.S. Bank). To hide the theft, he cooked up fake bank statements using Photoshop, Microsoft Excel, and high-quality printers. These he then handed over to Peregrine’s CFO, who appears to have adopted an “OK, you’re the boss” attitude after Wasendorf used what he called “blunt authority” to cow him into submission. Wasendorf seems to have taken special pride in his forger’s art, bragging of how adept he eventually became at falsifying not just hard copies, but online statements as well, none of which the financial regulators appear to have questioned.

Then, this summer, Peregrine hit the wall. Wasendorf couldn’t keep all the balls bouncing. On July 9, he tried to kill himself by inhaling fumes from a hose hooked up to his car’s tailpipe. Needless to say, the firm had been run into the ground. Wasendorf’s son was devastated at finding the company he was supposed to inherit was now a mound of useless paper—and that his father was a crook. Peregrine’s workers were out of a job. And of course, thousands of investors were left holding the bag.

Excessive self-confidence? Check. Grotesque overestimation of one’s abilities? Check. Loss of contact with reality? Check. (Sooner or later someone had to notice that there was no actual money in those U.S. Bank accounts.)

But the hubris didn’t stop there. It was also abundantly on display in Wasendorf’s suicide note, in which, far from showing any remorse, he actually seemed to thumb his nose at financial regulators. Evidently even his would-be last moments were ego-driven:

Where executives [like Wasendorf] have committed crimes, “it is not remorse that motivates” them to kill themselves, said Dr. Alan Berman, executive director of the American Association of Suicidology, a suicide education and prevention group. “Rather it’s a refusal to accept a changed public persona.”

As he prepared to take his life, Wasendorf confessed to massive fraud in a document whose tone often sounded more boastful than ashamed. He explained in detail how he had used “careful concealment and blunt authority” to steal hundreds of millions of dollars over two decades from clients of his brokerage firm. His scheme to falsify bank statements and balance sheets started 20 years ago, he wrote, because “my ego was too big to admit failure.”

In the cases of executive criminals, Berman said that “the suicide dies having preserved in his mind that the world’s view of him will remain that of before his death. Death is preferred to losing face, suffering media coverage of the felonious behavior, prison and other consequences.”

Incredible, an ego that massive. But seeing as how egotistical delusions are the enemies of realistic risk assessment pretty much 100% of the time, investors would do well to take a cold shower before forking over money to any proposal that appears too good to be true. Specifically, they should learn to recognize Ponzi schemes, of both the Waserdorf and the Bernie Madoff variety. These schemes have several tell-tale traits:

- They promise minimum or steady returns;

- They claim their opportunities are exclusive, available only to a select few;

- Their means of making money is too complicated or secret to explain;

- They make it difficult to withdraw your money, saying that funds have been frozen;

- They issue statements that lack detail, or that frequently show discrepancies that cannot be explained;

- They are frequently run by a single individual whose charm and charisma allow him maximum leverage over investors’ fears—and greed.

Con artists like Wasendorf prey upon the egotistical hopes and equally egotistical anxieties that come out in just about all of us whenever money is involved. Knowledge and financial realism are their enemies. That’s why, whenever you’re about to embark on a new financial venture, it pays to check your ego at the door.

-

Morning News: August 17, 2012

Posted by Eddy Elfenbein on August 17th, 2012 at 7:48 amEuro-Area Exports Rose 2.4% in June, Led by Germany

London Firings Seen Surging as Finance Firms Add NY Jobs

India Lost $33 Billion Giving Away Coal Mines, Auditor Says

U.S. Reliance on Saudi Oil Heads Back Up

Scorched Corn Belt Still Reaps Top Dollar

Treasury to Amend Terms of Fannie, Freddie Bailout

Why the N.Y. Fed’s Empire State Survey Still Matters

Facebook Second-Worst IPO Performer After Share Lock-Up

Verizon Wireless Clears Hurdles In Cable Spectrum Deal

IBM Plans More Storage Acquisitions After Texas Memory Purchase

Cisco Jumps On Dividend Hike, Props Up Network Gear Makers

Gap Quarterly Profit Rises 29% To Beat Analyst Estimates

Sina Shares Up As 2Q Earnings Triple

Jeff Carter: Corzine Will Not Be Prosecuted

Cullen Roche: The Economy Is Stronger Than You Think

Be sure to follow me on Twitter.

-

Progressive Comes Tumbl-ing Down

Posted by Eddy Elfenbein on August 16th, 2012 at 11:22 amIn case you still had some faith remaining, post-2008, that big financial institutions have your best interests at heart, or that insurance companies are motivated first and foremost by a desire to serve their policyholders, or that they will even honor their contractual obligations, Matt Fisher is here to set you straight.

Matt is a New York-based comedian and blogger. He had the great misfortune, two years ago, to lose his younger sister Katie in a car accident. And now he’s been subjected to a legal ordeal that would make even Franz Kafka’s head swim.

To all appearances, the case involving Katie’s death was pretty much open-and-shut. She was driving on a Baltimore street and had stopped at a red light. When the light turned green, she proceeded to cross the intersection. Another car ran the light and slammed into her. The driver’s insurance company, Nationwide, tacitly admitted fault and agreed to settle right away. For most people, this is the very definition of a no-brainer.

For most people. But then most people aren’t lawyers for huge insurance firms.

The difficulty arises from the fact that the other driver was underinsured, and that Katie had taken out a policy with Progressive ($PGR) that protected her against the possibility of an accident with an underinsured motorist. When Matt’s family tried to get the insurance giant to make up the difference in the value of his sister’s policy—i.e. to make good on the contract for which Katie had been spending her hard-earned money, i.e. to obey the law—Progressive said no way.

Now this in itself is perhaps not surprising, especially for many Americans who have had the misfortune to find themselves obligated to squeeze money out of the stone that is the heart of a large insurance company. What is surprising, or rather horrifying, is the series of barriers that Matt’s family then found between themselves and justice.

First off, they found that Maryland law prohibits clients from suing an insurance firm for non-payment on a policy. This probably comes as no shock in a post-AIG world. Second, they found that if they wanted some semblance of fairness, they’d have to bring a civil suit against the other driver (which they really didn’t want to do) as a way of gaining legal leverage and so hopefully getting Progressive to pay up. Third, they found that Progressive was willing to stoop to anything, anything, to avoid doing the right thing.

What does “anything” mean? Well, ordinarily, insurance companies pay their lawyers to crucify those who are on the opposing team, which is to say, those who have caused accidents that the companies’ clients are not responsible for. But this wasn’t what Progressive did. Instead, they actually took sides against their own client and offered legal counsel to their opponent, namely the underinsured driver. As Matt puts it:

At the trial, the guy who killed my sister was defended by Progressive’s legal team.

At the beginning of the trial on Monday, August 6th, an attorney identified himself as Jeffrey R. Moffat and stated that he worked for Progressive Advanced Insurance Company. He then sat next to the defendant. During the trial, both in and out of the courtroom, he conferred with the defendant. He gave an opening statement to the jury, in which he proposed the idea that the defendant should not be found negligent in the case. He cross-examined the plaintiff’s witnesses. On direct examination, he questioned all of the defense’s witnesses. He made objections on behalf of the defendant, and he was a party to the argument of all of the objections heard in the case. After all of the witnesses had been called, he stood before the jury and gave a closing argument, in which he argued that my sister was responsible for the accident that killed her, and that the jury should not decide that the defendant was negligent.

I am comfortable characterizing this as a legal defense.

Aside from the baroque legal issues this “defense” raises—if Katie was in fact responsible for the accident, then wouldn’t the underinsured motorist have the right to sue Progressive for his damages?—it really adds another twist of the knife for Matt’s family. But even then, Progressive wasn’t done with the Fishers.

The jury, in a moment of sanity, found for Matt’s family, awarding them some $760,000. As yet, the Fishers haven’t seen a penny. But when Matt decided to make public the whole ordeal on his blog—which then proceeded to be picked up far and wide by the chatterati, Twitted and Tumbl-ed ad infinitum—Progressive made the mistake of trying to do damage control. With predictable results. After thousands of people went on the company’s Facebook page, threatening to cancel their policies, Progressive’s PR people issued via Twitter what has to be the single lamest apology ever penned:

This is a tragic case, and our sympathies go out to Mr. Fisher and his family for the pain they’ve had to endure. We fully investigated this claim and relevant background, and feel we properly handled the claim within our contractual obligations.

Yep, that’s right, “within our contractual obligations.” And to make matters worse, in the face of growing public outrage, Progressive simply continued to Tweet the same robotic post. It’s been all downhill from there. Gawker has picked up the story, excoriating the insurance firm for its handling of the whole affair. Meanwhile, for the tens of thousands of other online readers who have chimed in, Progressive’s ass-covering has come to epitomize the soullessness and dehumanization, the lack of even the most rudimentary human decency, that seem to characterize so much of modern corporate behavior.

How will this affect the company’s bottom line? That remains to be seen, but some fallout is probably inevitable. Progressive is a solid company, but it’s going through a rocky period right now, and this can only make it rockier. Last quarter, rising health expenses led to higher claims costs, which in turn led to falling profits. Net income and operating profits have also fallen short. To top it all off, there’s even talk of the company’s retiring Flo, the bizarrely bubbly counter girl in its highly successful ad campaign, whose grin has suddenly come to seem a liability, even disturbing. The upshot? A glaring sign above the stock’s ticker: DO NOT BUY.

Progressive seems not to have learned one of the key lessons of the social-media age. There is no privacy anymore. Every move a company makes can, and given the public’s endless need for stimulation, inevitably will, be broadcast on the huge Jumbotron that is the internet. Corporate decision-makers would be well-advised to behave as though their every move were being played before a capacity crowd at the Rose Bowl. The distance between in-house and viral is exactly two mouse clicks, the time it takes to send an angry blog post into the cybersphere. Caveat venditor: let the seller beware.

-

Morning News: August 16, 2012

Posted by Eddy Elfenbein on August 16th, 2012 at 9:00 amEuro-Area Inflation Held Steady in July After Economy Contracted

Merkel Cites Canada as Debt-Deficit Model in Europe’s Crisis

China Stocks Fall to Two-Week Low After Foreign Investment Drops

Nikkei Hits 6-Week High As Soft Yen Puts Focus on Exporters

Gold Runs Out in Lisbon as Price Drop Compounds Money Misery

Risk Builds as Junk Bonds Boom

Treasury Yields Rise to Three-Month High Before Housing Report

HSBC, Credit Suisse Sacrifice Employees to U.S., Lawyers Say

Facebook Freeing 60% More Shares Seen Weighing on Its Stock

Sears’s Loss Narrows, but Sales Keep Declining

Deere Third-Quarter Net Up 11% But Cuts Profit, Sales Outlooks

Cisco Still Pessimistic on Europe, Hikes Dividend

China Mobile First-Half Core Profit Slips, Shares Down 5 Percent

Roger Nusbaum: Stocks Will Not Make You Rich

Be sure to follow me on Twitter.

-

Industrial Production Jumps 0.6% in July

Posted by Eddy Elfenbein on August 15th, 2012 at 2:01 pmThe government released the industrial production report for July and the news was mixed. The good news is that industrial production rose 0.6% in July which beat economists’ forecasts by 0.1%. The downside is that industrial production for June was revised down to an increase of 0.1%.

The pickup in industrial production, the most in three months, may ease concerns that the industry that’s powered the expansion is faltering. At the same time, recessions in parts of Europe and the prospect of fiscal tightening in the U.S. are hurdles for American factories.

“There are still strong trends in the auto industry and a number of other sectors which will keep industrial production from dipping into the negative this year,” Guy LeBas, fixed- income strategist at Janney Montgomery Scott LLC in Philadelphia, said before the report.

I’m still a QE3 doubter and I think is more evidence that it’s not on its way. The crucial piece of the puzzle is jobs and that’s still not doing well.

I like to follow the industrial production report because it has a very strong correlation with recessions and expansions. Check out the chart below.

-

Industrial Production Jumps 0.6% in July

Posted by Eddy Elfenbein on August 15th, 2012 at 2:01 pmThe government released the industrial production report for July and the news was mixed. The good news is that industrial production rose 0.6% in July which beat economists’ forecasts by 0.1%. The downside is that industrial production for June was revised down to an increase of 0.1%.

The pickup in industrial production, the most in three months, may ease concerns that the industry that’s powered the expansion is faltering. At the same time, recessions in parts of Europe and the prospect of fiscal tightening in the U.S. are hurdles for American factories.

“There are still strong trends in the auto industry and a number of other sectors which will keep industrial production from dipping into the negative this year,” Guy LeBas, fixed- income strategist at Janney Montgomery Scott LLC in Philadelphia, said before the report.

I’m still a QE3 doubter and I think is more evidence that it’s not on its way. The crucial piece of the puzzle is jobs and that’s still not doing well.

I like to follow the industrial production report because it has a very strong correlation with recessions and expansions. Check out the chart below.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His