-

Who Was Responsible for the Great Moderation

Posted by Eddy Elfenbein on March 31st, 2009 at 1:08 pmIn The Atlantic, Virginia Postrel looks at what made the Great Moderation possible. The Federal Reserve thought it was them, and that was a big mistake:

In 2001, the Fed aggressively cut interest rates, driving them down much lower than its policies since the mid-1980s would have predicted. The goal was to stave off recession and avoid the kind of deflation that Japan had experienced in the 1990s. But the cuts backfired. Those excessively low rates set off a housing bubble and all the consequences that flowed from it. The peak of the boom, Stanford economist John B. Taylor estimates, saw about 250,000 more new housing starts a year than there would have been if the Fed had followed its old practices. (Similar patterns of low interest rates and housing bubbles also occurred in many European countries.)

To make matters worse, Taylor argues, once the financial crisis began in August 2007, policy makers and many Wall Street traders misdiagnosed the problem as a shortage of liquidity—something the Fed could address by making it easier for banks to borrow from the government. But the problem was really so-called counterparty risk: financial institutions couldn’t trust the securities they were buying from and selling to each other. To compensate for this risk, banks charged each other much higher interest rates.

“This was not a situation like the Great Depression where just printing money or providing liquidity was the solution; rather it was due to fundamental problems in the financial sector,” Taylor writes in a survey of his published research on the crisis. The only way to fix the problem is to clean up the banks’ balance sheets, bringing in more capital to make them stronger and marking down bad loans (reducing their principal amounts) to make them more trustworthy. -

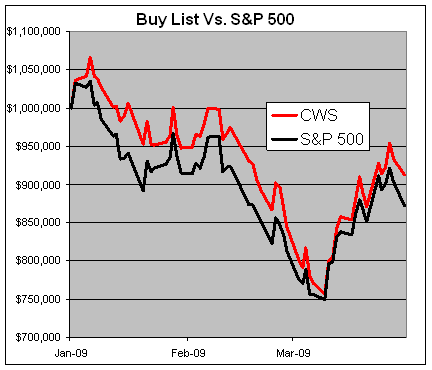

Buy List YTD

Posted by Eddy Elfenbein on March 30th, 2009 at 5:54 pmSince the first quarter ends tomorrow, I thought I’d give an update on the Crossing Wall Street Buy List. It’s not been a good year, but we’re still doing better than the market.

We’re on pace to beat the S&P 500 for the third straight year. Through Monday, the Buy List is down 8.82% while the S&P 500 is off by 12.81% (neither figure includes dividends).

Six of our stocks are in the black for the year while 14 are in the red. The top performer is Nicholas Financial (NICK) which is up 18.7% followed by Amphenol (APH) which is up by 17.8%. Interestingly, NICK was our biggest loser in 2008.

The huge outlier is Aflac (AFL) which down over 60% for the year. Nothing else comes close. In fact, the stock was down a lot lower. Aflac has nearly doubled from its March low to its March high.

The Buy List rules dictate that I’m not allowed to make any changes throughout the year. I think that helps me in the case of a stock like Aflac.

Last month, Aflac said to expect operating earnings-per-share to grow by 13% to 15% this year. Remember that with insurance stocks we want to look at the operating figures. That translates to $4.51 to $4.59 per share, and it doesn’t include the impact of the yen, which is stronger against the dollar this year, so Aflac’s estimate is probably on the low side.

Bottom line, we’re talking about a stock going for around four times earnings that yields 6.4%. Stay tuned for Q1 earnings which will come out at the end of April. -

Morgan Says Sell Into Bear Market Rally

Posted by Eddy Elfenbein on March 30th, 2009 at 11:49 amI’m not selling, but I think Morgan may be right. Stocks have climbed so much so quickly.

Investors should sell into the recent stock market rally, Morgan Stanley’s strategist said Monday, arguing that it can’t last as corporate earnings deteriorate further.

“We simply do not believe that the market has completely priced in the prospect of further earnings weakness or that it will, without interruption, look through this weakness to recovery,” Morgan Stanley strategist Jason Todd wrote.

On March 18 the S&P 500 rallied 25% to above 800 points since its low of 666 on March 6 – a technical bull market – spurred by positive comments by bank chief executives about improving business conditions as well as a favorable market reaction to the government’s efforts to support the financial system.That’s right. The S&P 500 bottomed at 666.

-

The Golden State Fizzles

Posted by Eddy Elfenbein on March 29th, 2009 at 7:18 pmCalifornia is not in good shape:

California’s unemployment rate will soar to between 12 percent and 15 percent by next spring and remain in the double digits until at least the beginning of 2012, according to forecasts released by two teams of University of California economists.

The state’s unemployment rate has not reached those heights since the Great Depression.

The projections – one released today by UCLA’s Anderson Forecast, the other last week by UC Santa Barbara’s Economic Forecast – paint a grim picture of declining economic growth, lower retail sales, a troubled housing market and falling office prices lasting through much of 2010.

“It looks like it will be a nasty recession, but not a depression, although the possibility that we could get to a depression has increased,” said Dan Hamilton, director of the UCSB forecast. “Every month and every quarter that goes by is noticeably worse than the month or quarter that went before.” -

Weekend Reading

Posted by Eddy Elfenbein on March 29th, 2009 at 3:12 pmThere are many good articles this weekend. Here are a few:

“The Quiet Coup” by Simon Johnson

“Now the Long Run Looks Riskier, Too” by Mark Hulbert

“It Pays to Understand the Mind-Set” by Robert Shiller

“America’s liberals lay into Obama” by Edward Luce

“Stocks Through a Wide-Angle Lens” by Lawrence C. Strauss

Money quote from the last article:Now, while corporate-credit markets remain firmer than they were at their 2008 worst levels, debt values have backed up a bit without the close attention of equity markets. Bank-issued debt, in particular, has eroded in value without gaining much attention.

As a result, once again (nominally) high-grade corporate bonds are looking rather attractive by several measures.

J.P. Morgan Chase credit analyst Eric Beinstein last week noted that the high-grade bond benchmark is pricing in “a default rate of about 45%” over the next 10 years — and 10 years is the average life of the bonds in the index. He says this means a hypothetical investor could buy the components of the index, funding the purchase at the London Interbank Offered Rate, watch 45% of the bonds go bust, then recover only 20% of face value, and still break even for the decade.

The worst 10-year default rate for high-grade debt since 1980, he says, was 5%, implying the market is building in truly cataclysmic credit losses, in part because liquidity in this market remains so scarce.

This is an extended way of illustrating that — outside the ultra-high-quality slice of the market — corporate debt now should reward prudent risk-taking. -

WaMu: Not Stodgy Old Banking

Posted by Eddy Elfenbein on March 29th, 2009 at 2:59 pmI bashed this WaMu commercial a few years ago. Who really thinks a banker looks like Mr. Monopoly?

In retrospect, perhaps WaMu should have paid attention to those stodgy guys. -

Laid Off Wall Streeters Turning to Stripping

Posted by Eddy Elfenbein on March 29th, 2009 at 2:53 pmFrom The New York Post (of course):

Randi Newton, 28, who lives in Midtown, was a financial analyst at Morgan Stanley before the crash but was fired.

“A few nights after I got laid off, I went with friends to a strip club to get drunk and forget my unemployment troubles,” Newton said. “The manager offered me a job as a dancer. I thought it was different. And fun.”

Today, Newton, who calls herself an “independent contractor,” pole dances at Rick’s Cabaret in Murray Hill three or four nights a week and says she makes “$160,000 a year on tips alone.”You can read more about Ms. Newman as her blog, Wall Street Stripper.

(HT: WSF). -

Weekend Poll

Posted by Eddy Elfenbein on March 27th, 2009 at 6:33 pm -

Freeman Dyson: A Civil Heretic

Posted by Eddy Elfenbein on March 27th, 2009 at 4:48 pmThe New York Times profiles Freeman Dyson:

Dyson is well aware that “most consider me wrong about global warming.” That educated Americans tend to agree with the conclusion about global warming reached earlier this month at the International Scientific Conference on Climate Change in Copenhagen (“inaction is inexcusable”) only increases Dyson’s resistance. Dyson may be an Obama-loving, Bush-loathing liberal who has spent his life opposing American wars and fighting for the protection of natural resources, but he brooks no ideology and has a withering aversion to scientific consensus. The Nobel physics laureate Steven Weinberg admires Dyson’s physics — he says he thinks the Nobel committee fleeced him by not awarding his work on quantum electrodynamics with the prize — but Weinberg parts ways with his sensibility: “I have the sense that when consensus is forming like ice hardening on a lake, Dyson will do his best to chip at the ice.”

-

Corporate Bonds Don’t Believe the Rally

Posted by Eddy Elfenbein on March 27th, 2009 at 1:34 pmDavid Merkel makes a good point: The spread between corporate bond and stocks is getting pretty big. In fact, way too big. Corporates seem to be sitting out this rally. Bottomline: Anything that’s not a Treasury is looking pretty good here.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His