-

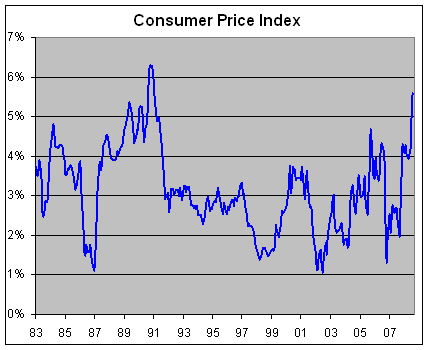

Inflation at 17-Year High

Posted by Eddy Elfenbein on August 14th, 2008 at 4:09 pmUgh.

Inflation reached a 17-year high last month, fueled by high gasoline and food prices, all but assuring that the Federal Reserve will keep interest rates at their current level for the time being.

Consumer prices were 5.6 percent higher last month than they were in July 2007, a brisker pace than economists had expected, the Labor Department said on Thursday.

That was the sharpest annual increase since January 1991, as Americans paid more for clothing, food, transportation and recreational products.

The news was distressing for investors and the stock markets initially fell on the report. The major exchanges recovered, however, and the Dow Jones industrials up more than 80 points in early afternoon trading. Investors returned to buying financial stocks, taking advantage of a sector that has fared poorly in recent sessions. The broader S.&P. 500-stock index was up 0.46 percent. Wal-Mart also reported a better-than-expected rise in quarterly profits, but the discount retail giant also issued a gloomy sales forecast for the rest of the year. In addition, crude oil prices continued to fall, dropping below $113 a barrel.

The overall Consumer Price Index, considered the benchmark gauge of domestic inflation, rose 0.8 percent in July. Economists had forecast a rise of half that rate. In June, prices rose 1.1 percent, the second highest monthly pace in 26 years.

-

Stat of the Day

Posted by Eddy Elfenbein on August 13th, 2008 at 6:42 pmFrom its peak in 1980, if the price of gold had kept pace with total return of the Wilshire 5000, today gold would be worth over $21,000 an ounce.

-

When All the Small Things Includes Your Portfolio

Posted by Eddy Elfenbein on August 12th, 2008 at 4:25 pmHe lost

It all

So screwed

he is

Oh no!

Must tour

A-gain

Ha Ha

Dumb Ass

Say it ain’t so

Where did it go

One Point Five Mil

See you in Court

Na, na, na, na….. -

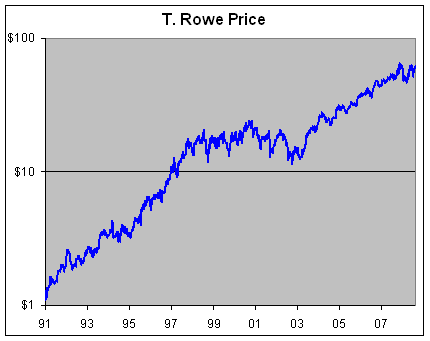

A Very Short Post

Posted by Eddy Elfenbein on August 12th, 2008 at 12:06 pmI’d really like to buy T. Rowe Price (TROW) but I think it’s about $10 too expensive here.

Pretty sweet chart tho. -

Sysco’s Earnings

Posted by Eddy Elfenbein on August 12th, 2008 at 11:17 amIn terms of relative performance, these have been great times for the Buy List. Yesterday, Sysco (SYY) added 4% on good earnings news. Typically, this is one of the most stable large-cap stocks on Wall Street. For Q2, Sysco earned 55 cents a share, three cents more than estimates. Last year, Sysco netted 49 cents a share so the company is growing well.

-

Thank You NICK

Posted by Eddy Elfenbein on August 12th, 2008 at 10:43 amI’m up 27% in three weeks since my last purchase of Nicholas Financial (NICK). It takes patience but the market is not efficient. The stock is still going for less than 80% of book.

-

From the NYT Corrections

Posted by Eddy Elfenbein on August 11th, 2008 at 10:54 amThe Arts

A listing of credits on April 28, 1960, with a theater review of “West Side Story” on its return to the Winter Garden theater, misstated the surname of the actor who played Action. He is George Liker, not Johnson. (Mr. Liker, who hopes to audition for a role in a Broadway revival of the show planned for February, brought the error to The Times’s attention last month. ) -

Gas Prices fall for 24 Straight Days

Posted by Eddy Elfenbein on August 11th, 2008 at 10:45 amSupply and Demand continues to work its magic:

Retail gasoline prices have fallen for the 24th straight day, a AAA survey of gas station sales showed.

The national average price for a gallon of regular gas are down more than 7 percent from the record high of $4.114 on July 16, CNNMoney.com reported Sunday.

Even with gas prices falling, Friday’s national average price is more than $1 higher than it was a year ago.

In Alaska, the state with the highest prices, drivers pay an average of $4.63 a gallon, the AAA study found. Oklahoma and Missouri have the lowest gas prices, at $3.58 a gallon.

Diesel, meanwhile, is up nearly 55 percent from last year’s levels. The national average price for diesel fuel fell Sunday to $4.557 a gallon.

The AAA study is based on data from credit card swipes at 85,000 U.S. fuel stations. -

Citigroup Trader “Dooced”

Posted by Eddy Elfenbein on August 8th, 2008 at 1:08 pmMichael J. McCarthy aka “Large” has been fired from his job as a Citigroup trader for running his blog, Take A Report.

“This employee was terminated for behavior that violated the firm’s code of conduct and policies,” Citigroup spokeswoman Danielle Romero-Apsilos said. McCarthy, a vice president, declined to comment on his departure from the New York-based bank. Financial industry regulatory records show he’s been at Citigroup for seven years, most recently trading shares of utility and power companies.

“It’s a little over the top,” said Barry Ritholtz, director of equity research for New York-based Fusion IQ, who has looked at the site and has his own financial blog at www.bigpicture.typepad.com. “I can see why a conservative bank is not going to be happy with it. It’s funny as hell.” -

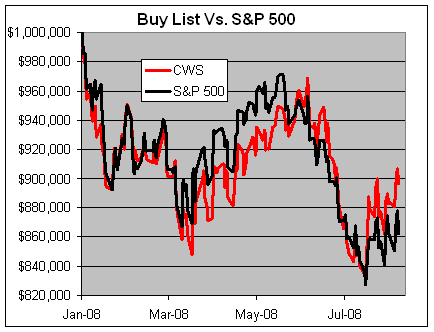

My Buy List YTD

Posted by Eddy Elfenbein on August 7th, 2008 at 10:47 pm

Through today, the Buy List is down -10.39% while the S&P 500 is down -13.78%. Neither figure includes dividends. The daily volatility of the Buy List is 7.17% greater than the S&P 500.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His